EPRT - 2 REITs Trading At Less Than 15X P/AFFO And Offering Double-Digit Upside

2023-12-01 09:00:00 ET

Summary

- Several REITs currently present buying opportunities due to the rise in interest rates.

- Highwoods Properties stock is down 35%, and trades less than 15x P/AFFO, offering great upside potential.

- Both REITs continue to face headwinds from the current macro environment. Investors should pay close attention to declining occupancy rates from both going forward.

- EPRT also trades less than 15x earnings and pays a growing dividend that is well-covered by growing AFFO.

- Additionally, their portfolio is well-diversified and stood at 99.8% leased at the end of Q3, signifying a strong tenant base.

Introduction

Depending on who you ask, you're going to get several different answers when it comes to how or where to invest. But for the most part, no one ever wants to overpay for a stock. Value matters and it matters a lot. Warren Buffett has been known to say and I've referenced it before, Price is what you pay, value is what you get. In short, it's never good to overpay for any stock, no matter how quality you consider it. But like I mentioned it all depends on who you ask. Some people don't mind overpaying for their investments, especially those who invest for the long-term as they assume the stock will only go higher over time. But most of us love a great sale. Especially when you can get two quality stocks at a great value.

Unless you're brand spanking new to investing, you know that REITs have suffered with the rapid rise in interest rates, and many present great buying opportunities right now. Those familiar with Benjamin Graham know he said you should never pay more than 15x earnings for a stock. Sentiment is beginning to shift in the sector and investors should consider these two REITs currently trading below 15x P/AFFO before it's too late.

#1 Highwoods Properties

I last covered Highwoods Properties (HIW) where I stated they were an underrated dividend payer . Disclaimer: Most stocks I choose to write on are ones that I own, previously owned, or would like to own.HIW I previously owned but sold. Not because of deteriorating fundamentals, but for stocks that I considered to be better buying opportunities at the time. REITs have experienced major headwinds, especially HIW. As an office REIT, it still faces major headwinds, still recovering from the pandemic 3 years ago. Some office REITs may never recover. So one might say, What makes HIW so special?

Well for one, the stock is down nearly 35%, much more than its peers in the sector, and the Real Estate ETF ( VNQ ) is down 4% on the year. So, right now the stock is a massive bargain and could offer great upside if one is willing to hold for a while. While I think REITs will recover nicely in 2024 unless something drastic happens, it will take HIW longer in my opinion. But I do think they will eventually, just slower than the rest. Are any of you familiar with the second Captain America movie? When Falcon told Nick Fury, Don't look at me, I do what he does, just slower. That's how I feel about Highwoods.

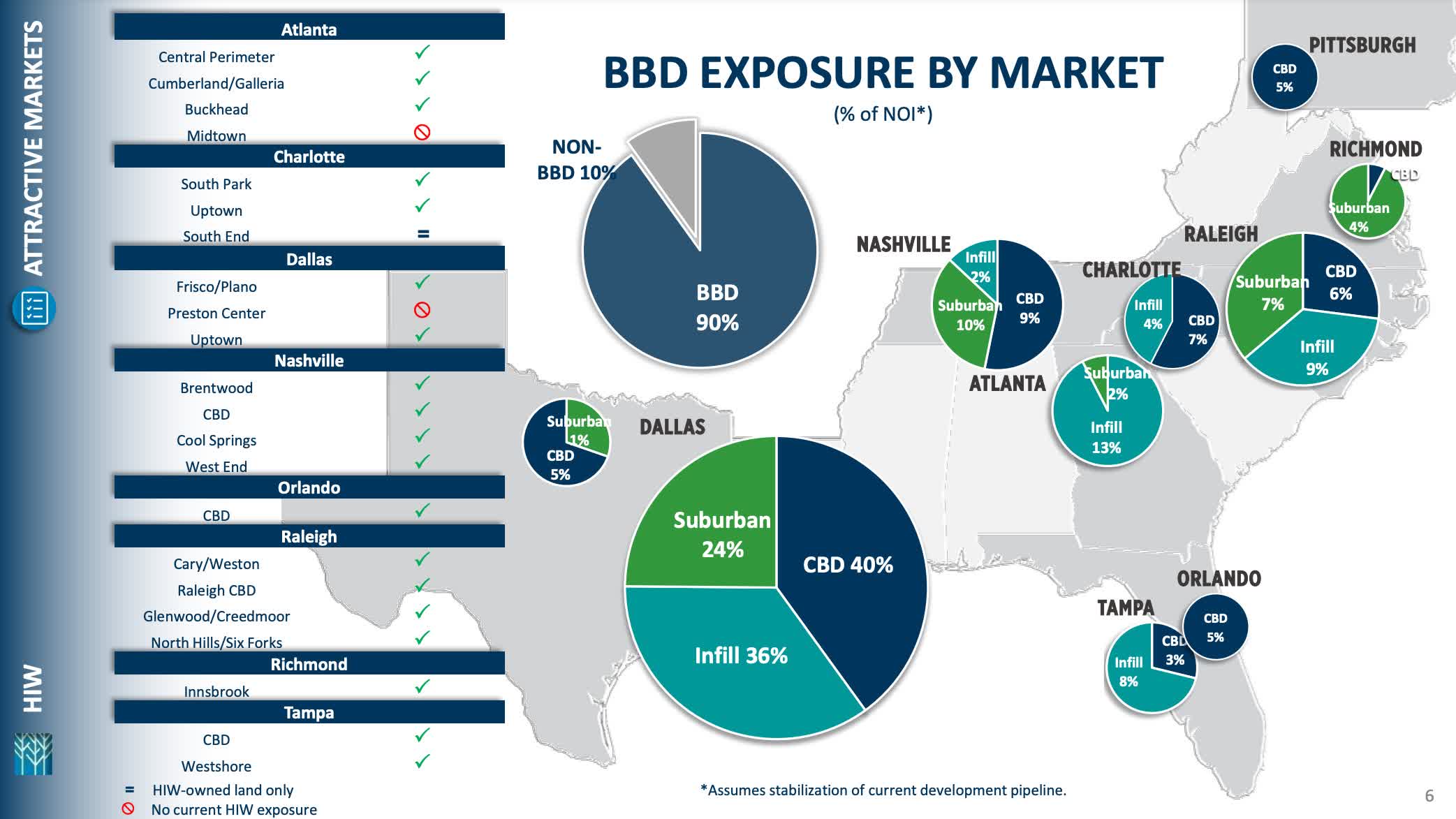

I think they will recover faster than other office REITs. One reason is they don't own office properties just anywhere, they own attractive properties in the Better Business District or BBD. Their properties are located in attractive, growing cities like Atlanta, Nashville, Raleigh, and Dallas to name a few. And these cities also happen to be in some of the fastest-growing states by population.

{kind=link}

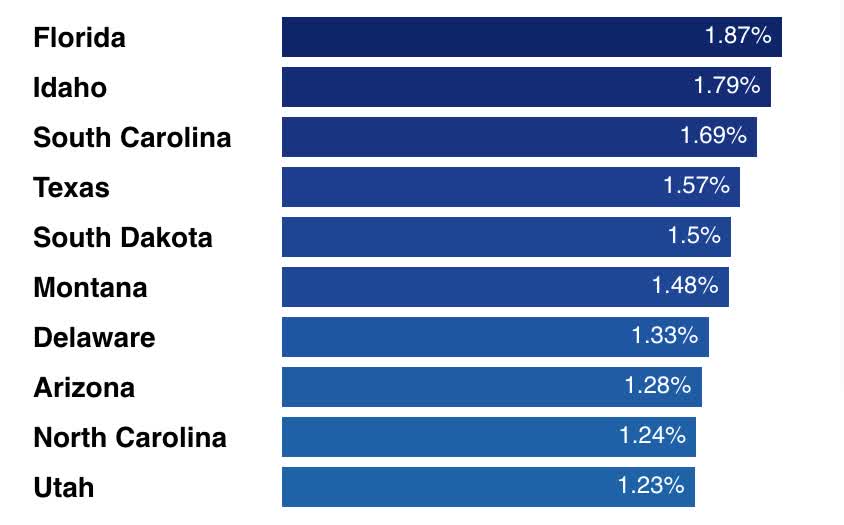

Being from Alabama I can personally attest to the growth of Orlando, Tampa, and Atlanta because they seem to be getting all the Alabamians, lol. If anyone has been there they can probably tell you there's not much to do in Alabama. And since these three cities are closest to the state, they get a large influx of our residents. That was the main reason for me joining the military. To get away and travel and see the world because I knew if I didn't then, I may never leave. If you look up the fastest-growing cities in the U.S., you'll probably see a common theme. Several of the cities are in the states like Texas, Tennessee, North Carolina, and Florida. HIW has properties located in all four states.

{kind=link}

Another reason to consider HIW is more large corporations are moving their HQs to these cities. Many are looking for cheaper real estate and to cut operational costs. This will allow them to save money in the long run. 2022 and 2023 saw the highest rate of corporate relocations in seven years. And can you guess which states led the way for the highest net gains in relocations? Florida & Texas. As far as cities Atlanta, Nashville, Tampa, and Dallas were among the biggest net gainers as well. It's likely HIW will benefit, I'm not saying that it's a guarantee, but a lot of these corporations that are relocating will need office spaces to rent. And the REIT can and will likely benefit from this in the future. Even with businesses adopting a hybrid work schedule now, they still will need somewhere to work and having properties in these attractive areas would benefit HIW.

Solid Quarter

The company reported Q3 earnings in October and reported some solid numbers. FFO of $0.93 was in line and revenue of $207.1 million was beaten by $0.26 million. They also refreshed their outlook from $3.69-$3.81 to $3.73-$3.77. FFO was down nearly 12% from $1.04 a year ago. Revenue was up slightly over the same period from $207 million. Occupancy stood at 88.7% at the end of the quarter, down from 91.1% year-over-year. So, although occupancy and FFO are down, considering the macro environment, HIW didn't do too badly.

Another reason to own this stock is they're a dividend shower. Those who've read my articles know what I'm talking about. Those who continuously grow their dividend, and who continuously pay a steady one, a shower. Furthermore, HIW has a strong, investment-grade rated balance sheet with no debt maturities until 2025, which is impressive. Especially since several popular and higher-rated REITs like Realty Income ( O ) and Simon Property Group ( SPG ) have a good amount of debt maturing next year. And did I mention you get paid a well-covered dividend of $0.50 while you wait for the price and sector to recover?

#2 Essential Properties Trust

I last wrote on Essential Properties Trust ( EPRT ) a few months ago where I compared them to the now private STORE Capital. I was an owner and actually bought EPRT shortly after my analysis of them back in August. I currently hold them in my ROTH IRA, which I'll admit I don't pay enough attention to nowadays. But now may be a good time for me to start as investors may be looking to sell off some stocks for tax-loss harvesting purposes, and they're trading at an attractive valuation.

Similar to their peer HIW, EPRT has also experienced a price decline, although not as significant. Reason being is the REIT is not exposed to office properties like the latter. EPRT focuses on tenants you've probably never heard of but operate strong, recession-resistant businesses such as car washes, Early Childhood Education facilities, Medical & Dental offices, and Quick & Automotive services to name a few. EPRT is one of the smaller and less popular REITs in the sector but have some of the longest WALTs at 13.9 years! I really like this stock because they're smaller, so unlike Realty Income they have a lot of room for exponential growth.

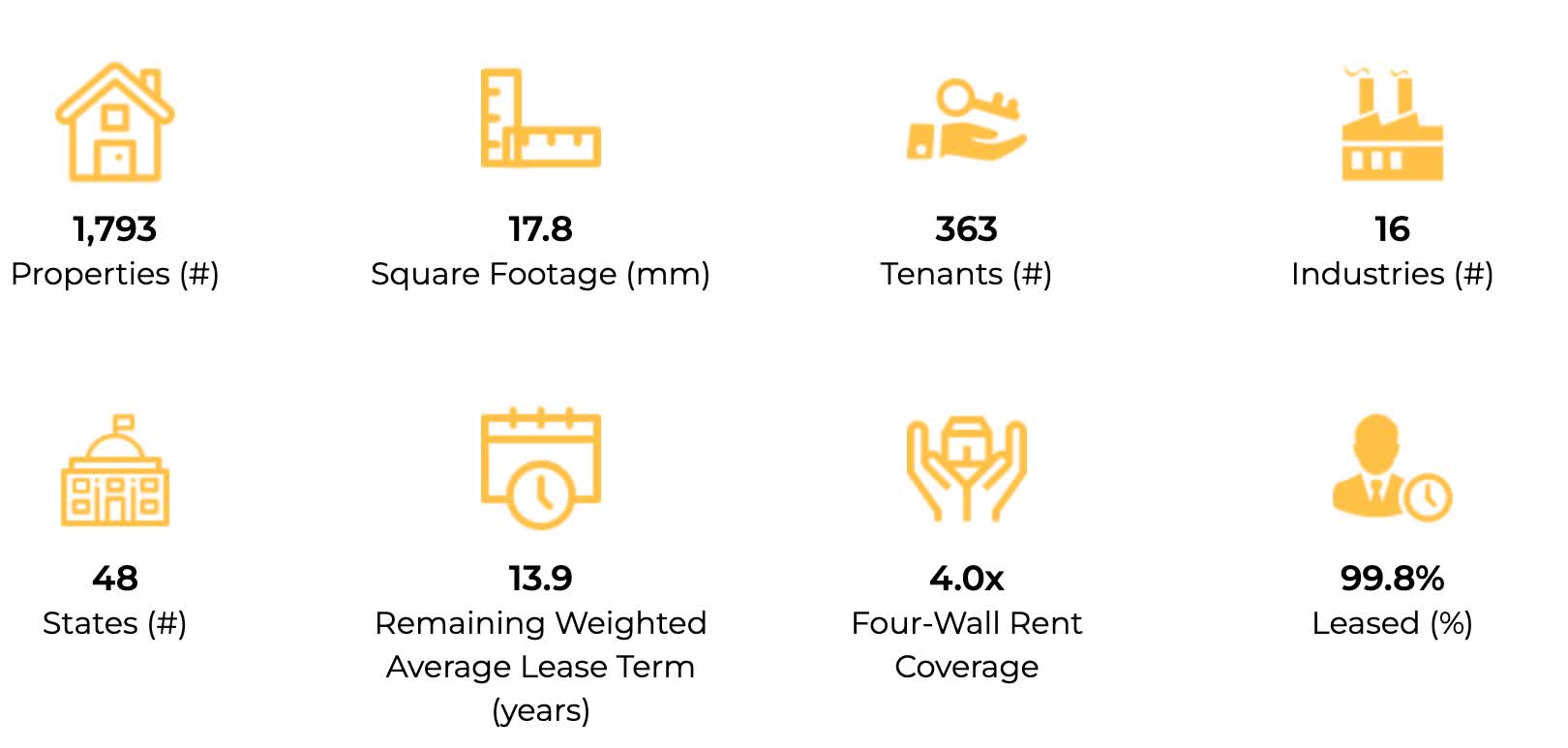

As you can see below, the REIT has a strong, well-diversified portfolio. As I previously mentioned, they're on the smaller side with 1,793 properties with a market cap of less than $4.0 billion. They also have 363 tenants across 16 industries in 48 states. One thing I worry about with companies like EPRT is what we've seen recently with Realty Income and Spirit Realty Capital ( SRC ). In the current macro environment stocks like EPRT are takeover targets from larger peers in the sector, and I can see O or others looking to acquire them in the future. I'm not saying that's going to happen nor do I have any inside information on whether it will happen or not. But like we've seen in the past, it can. Or maybe they will be bought out by a private company similar to STORE. Who knows, I hope not as I own them and plan to hold them for the long term.

{kind=link}

Latest Earnings

The company reported its Q3 earnings a day after HIW back on October 26th. EPRT actually did the opposite of HIW and missed on FFO. The REIT missed analysts' estimates by a penny reporting an FFO of $0.42 and beat revenue estimates by $1.16 million at $91.66 million. Both FFO and revenue increased by 10.5% and 29.7% respectively year-over-year, which is impressive all things considered. Like HIW, EPRT also refreshed its outlook and now expects FFO of $1.64 to $1.65, up from $1.62 to $1.65 prior. Additionally, they gave 2024 guidance and are expecting a range of $1.71-$1.75, a growth of 5% mid-point to mid-point.

Furthermore, EPRT does offer some growth in its dividend, a good reason why the two REITs complement each other well in a dividend-focused portfolio. The company has a much shorter track record than HIW with only 5 years worth of dividend payments. But investors do get some growth. They are also investment-grade rated and have one of the strongest debt maturity ladders I've seen in the sector besides Agree Realty ( ADC ). Both have no debt maturing for quite some time, ADC in 2028 and EPRT in 2027. So with HIW and EPRT, you get stable dividends and the chance for some nice upside in high-quality REITs that don't have to worry about debt maturities for a while. I think it's safe to say rates will be below their current range by the time these two have to worry about their debt maturing.

Valuation

Both REITs trade at attractive valuations at the moment. Quant gives HIW a grade of A while EPRT has a grade of B- . HIW offers the better entry price right now as they have been obliterated by not only rising interest rates but being an office-focused REIT as well. Both also offer double-digit upside to their price targets. HIW offers slightly higher at 16.35%.

{kind=link}

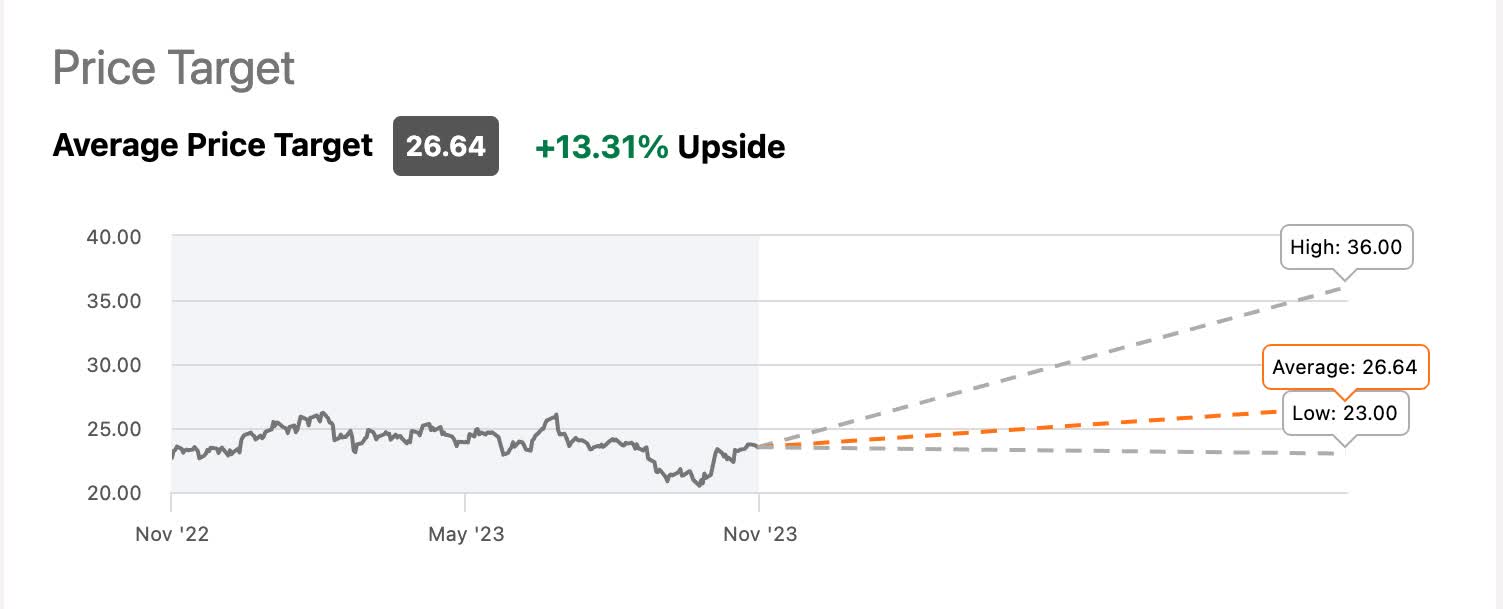

EPRT offers some nice upside as well. Either way, investors get good entry prices for both as I think the strong volatility days within the sector are behind us. As we move into 2024 and many are expecting rates to come down sometime during the year, I only see REITs moving higher.

{kind=link}

Risks To Consider

A huge risk to consider for the sector is normally debt maturities for REITs, but as noted previously, these two don't have any debt maturing for quite some time. Another risk factor is declining occupancy rates. Especially if the FED decides to hike rates further from here; they did leave the door open for more during their last meeting. Next month investors will be watching closely to see what comes out of the December meeting. In Q3, EPRT did fail to collect rent on two of its properties, operated by the same tenant. The operator was a gym owner in Oregon who filed for bankruptcy, but management expects to find a replacement tenant soon.

HIW also faces the same risk as they have seen their occupancy rates decline slightly during the year. In Q3, occupancy of 88.7%, a decline from 89% in Q2, and from 90.4% in Q1. If the economy does fall into a recession, both companies' tenants could be at an even greater risk of rent defaults and bankruptcies. So, investors looking to start a position in either one should be mindful and keep a close eye on stable occupancy rates going into Q4 and the new year.

Bottom Line

I know REITs have not been attractive investments in the past year due to rising rates, and the attractive offerings in safer, fixed-rate investments like CDs and bonds. But using Graham's Theory, both trade below 15x P/AFFO and offer double-digit upside to their price target. I suspect the sentiment is already beginning to shift in the sector and investors waiting to add may miss out on some capital appreciation. The market is forward-looking and will price in declining interest rates well before they happen at which point many may be trading well above 15x earnings. If you can stomach some volatility in the coming months and believe in the long-term outlook of the sector, then these two are attractive investments for income-focused investors.

For further details see:

2 REITs Trading At Less Than 15X P/AFFO And Offering Double-Digit Upside