SAFE - 2 REITs With Huge Upside Potential

2023-09-12 08:25:00 ET

Summary

- REITs are now priced at some of their lowest valuations in years.

- As a result, some REITs offer huge upside potential in a future recovery.

- I share two of my "top picks" to accumulate today.

Co-produced by Austin Rogers.

When you think about real estate investment trusts ("REITs"), you probably expect investments with moderate yield, steady growth, and little upside. Typically, these aren't "get rich quick" stocks. They offer the average investor the chance to own high-quality, institutional-grade commercial real estate with moderate yields and growth profiles.

At least, that's usually the case for REITs.

But amid rising interest rates, market sentiment about REITs has turned sharply negative, leading professional and retail investors alike to dump the asset class at a greater rate than at any time since the Great Financial Crisis of 2008-2009.

The publicly traded real estate sector ( VNQ ) is down ~30% from its high in early 2022, while the broader stock market ( SPY ) is down only ~7%.

That is a massive delta, indicating major market pessimism for REITs!

We think this level of pessimism is overdone for the real estate index as a whole, but there are certain individual names for which the market pessimism is majorly overdone. Some REITs have fallen into deep value territory, such that even a reversion to their historically average valuations would render massive upside.

In what follows, we highlight two of these high-upside REITs.

1. Crown Castle Inc. ( CCI )

CCI owns one of the largest networks of telecommunications infrastructure in the United States, including over 40,000 cell towers, about 120,000 small cells (mini-towers), and ~85,000 route miles of fiber.

CCI Presentation

The telecom infrastructure portfolio commands strong positioning in every major city in the US, giving CCI immense leverage over its customers, 75% of which are the big three carriers: AT&T ( T ), Verizon ( VZ ), and T-Mobile ( TMUS ).

For most types of real estate, the space can only accommodate one tenant. What makes CCI's telecom infrastructure unique is its ability to co-locate multiple tenants onto the same asset, whether it be towers, small cells, or fiber. This colocation feature causes CCI's cash yields on invested capital to surge well into the double-digits over time as more tenants are added.

Plus, CCI's long-term leases feature 2-3% annual rent escalations, which also gradually increase the effective yields.

This model has resulted in extraordinary growth for CCI since its conversion to a REIT in 2014, including dividend growth averaging around 9% annually.

{kind=link}

So, why the 50%+ selloff since the beginning of 2022?

In short, the market's two biggest worries about CCI have been:

- The company's floating rate debt exposure, which was as high as 20% a year ago but is now down to 9%.

- The cancellations of a number of Sprint leases in connection with its merger with T-Mobile.

These two factors are causing CCI's cash flow growth to slow from the high single-digits to low single-digits over the next few years.

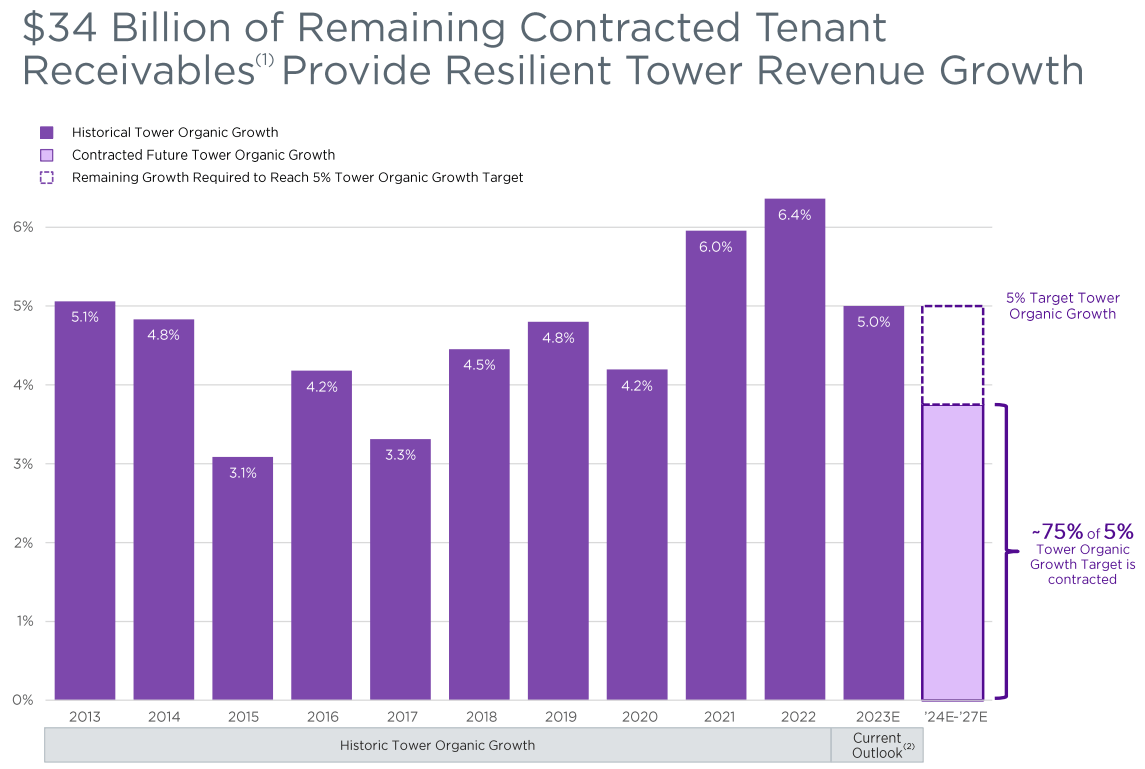

But the management remains confident that CCI will be able to return to 5%+ revenue growth and 7-8% dividend growth after the last Sprint lease cancellations take effect in 2025. Given projections for double-digit growth in mobile data usage as far as the eye can see, we share management's confidence in this expected to return to growth.

In fact, about 75% of management's target 5% revenue growth is already contracted for 2024 through 2027.

{kind=link}

Even including the effect of Sprint lease cancellations, CCI still generated 4% organic revenue growth in Q2 2023.

CCI is now valued at a 6.3% dividend yield and 13.3x AFFO, compared to its historical average yield of 3.4% and AFFO multiple of 23x. Just to return to its historically average valuation (not its highs) would generate upside of 70-75%.

While it may take a few years, we find it highly likely that CCI will realize this upside eventually.

2. Safehold Inc. ( SAFE )

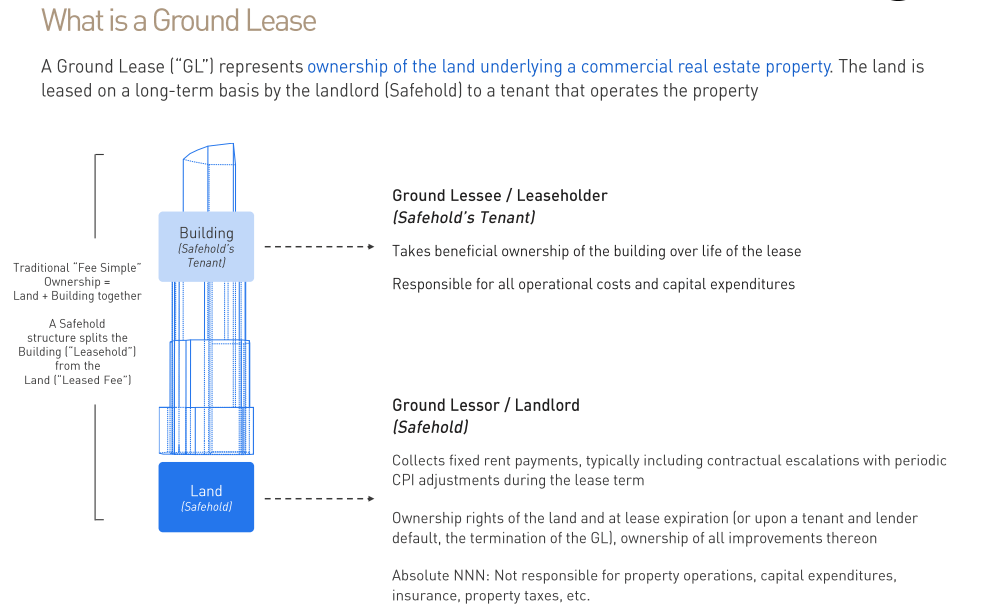

SAFE is a unique REIT that specializes in ground leases for large properties.

This is a structure in which the values of the land and the improvements/buildings are separated. As a source of long-term capital/financing, the freehold owner of a property will sell the land portion of the property to SAFE while simultaneously signing an ultra-long-term ground lease (typically 99 years) at a low rent rate.

{kind=link}

As the company name would imply, SAFE's revenue streams are extremely safe, as ground lease rent is the most senior form of capital for a commercial property, on the same level as taxes and utilities. Ground lease rent must be paid even before interest on debt!

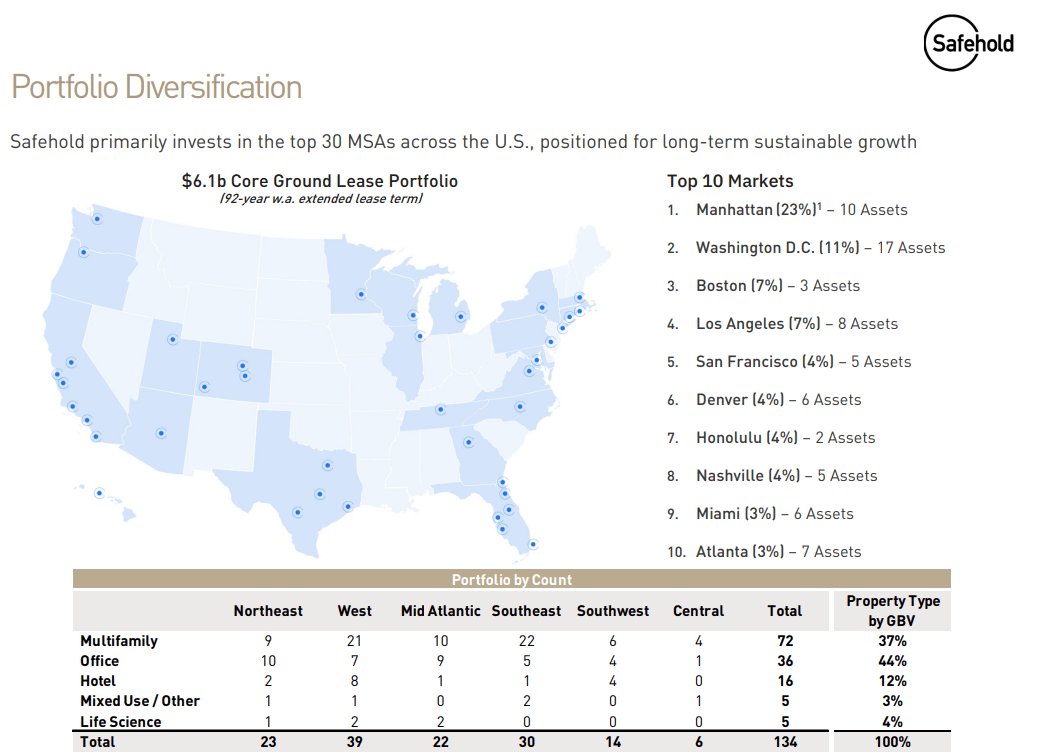

As of Q2 2023, SAFE owns 134 ground leases worth roughly $6 billion in various markets across the United States. By book value, 44% of GLs are for office buildings, 37% for multifamily, 12% for hotels, and 4% for life science/laboratories.

{kind=link}

Moreover, despite being very long-term and stable revenue streams, SAFE's ground leases are superior to corporate bonds in a number of ways.

- 95% of the portfolio has some sort of inflation protection, typically a rent increase based on previous years' inflation, capped at 3% to 3.5% per year. Although these rent resets come only after an initial fixed-rent period of 10-20 years.

- Ground leases are essentially "secured" by the underlying real estate. If the leasehold owner defaults on rent, the building reverts to SAFE at no cost.

- Likewise, at the end of the 99-year lease term, the building reverts to SAFE at no cost.

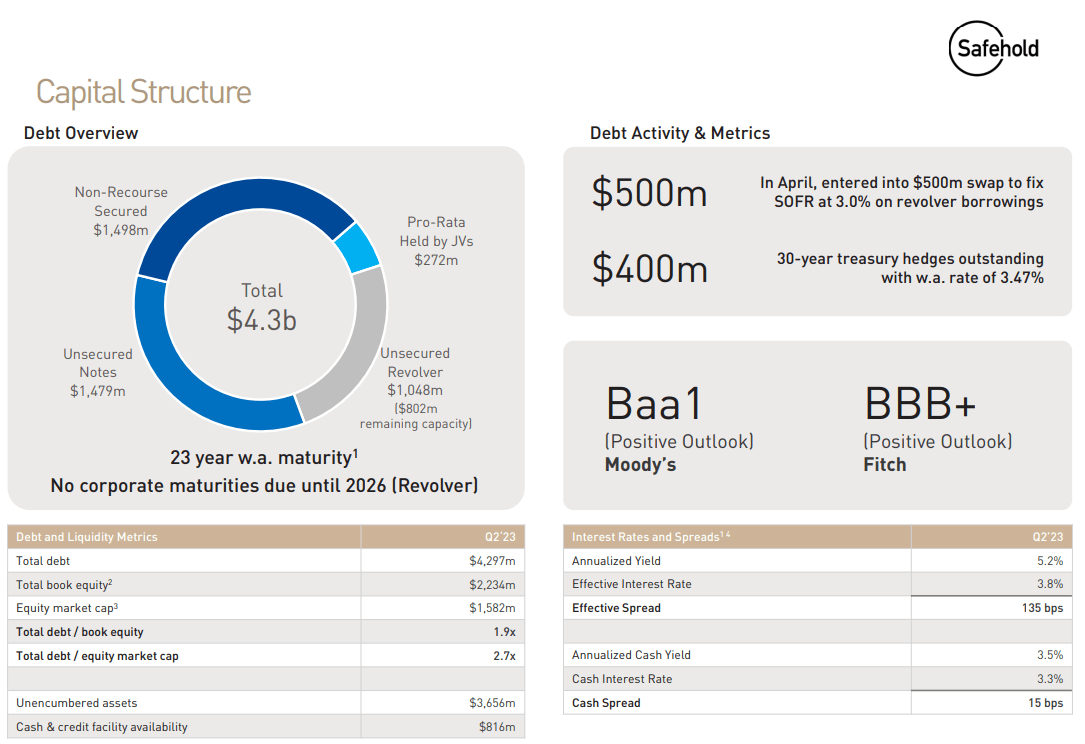

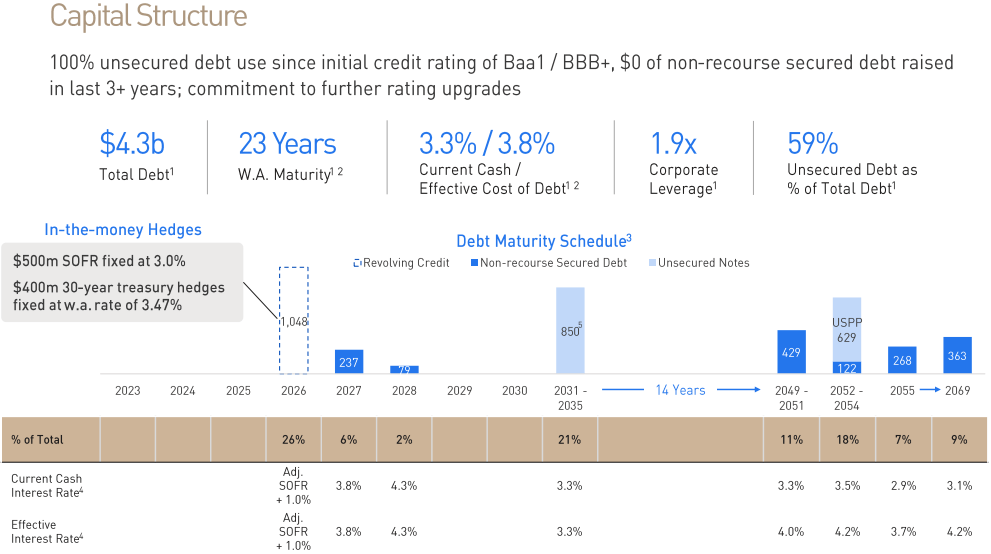

Thanks to SAFE's ultra-defensive assets and strong credit ratings of BBB+/Baa1 (with positive outlooks), the REIT has been able to borrow money at very low interest rates (~3.3% weighted average) for very long periods of time (~23-year weighted average maturity).

{kind=link}

Since SAFE's GL cash yields start out fairly low at about 3.5%, the investment spread begins fairly narrow, but it expands over time as rent escalations gradually kick in.

Of course, the worst enemy of long-term, contractually fixed revenue streams is rising interest rates. Fortunately, SAFE has zero debt maturing until 2026, but even that debt has already been fixed for 30 years if and when SAFE extends the maturity.

{kind=link}

SAFE is basically a leveraged investment in ultra-long-term fixed-income assets with inflation protection and additional upside from the buildings eventually reverting back to it. As such, the market treats it like a leveraged version of long-term corporate bonds ( VCLT ).

Anything with leverage is going to outperform when interest rates are falling and underperform when rates are rising, which explains SAFE's massive selloff over the last year and a half.

But interest rates are widely expected to fall within a year or so. What's more, it appears that we are at or near the peak in interest rates for the current rate-hiking cycle.

As such, now could be the perfect time to load up on SAFE and its 3.4% yielding dividend. We think SAFE could easily double in price from here if and when interest rates fall, even if rates don't go back to zero.

Bottom Line

Although we usually think of entrepreneurs and CEOs as being visionaries, it is critical for the average investor to be visionary as well. We need to envision what the future most likely holds and invest our money for that world, rather than whatever situation we find ourselves in currently.

At the present moment, growth has slowed to a crawl for CCI, and SAFE's business model is being challenged by the highest interest rates in nearly two decades.

But we are confident that neither situation will persist for more than a few years.

- Mobile data usage will continue to grow, spurring telecom carriers to continue expanding their infrastructure, which will fuel continued growth for CCI beyond the T-Mobile/Sprint tower consolidations through 2025.

- High interest rates will strain the economy and government budgets until some sort of negative consequences force central bankers to lower rates again, which will turn SAFE's downward trend into an upward trend.

We envision huge upside for these two defensive REITs if our investment theses play out, and we have high confidence that things will eventually play out as we expect. REITs like this with generous yields, solid growth prospects, and huge upside potential are our favorite kinds of investments.

For further details see:

2 REITs With Huge Upside Potential