KREF - 2 'Strong Buy' REITs At Steep Discounts

2023-07-25 08:05:00 ET

Summary

- REITs rose quite a bit in recent weeks.

- But many still have a lot of room of run.

- We highlight two REITs that offer significant upside potential.

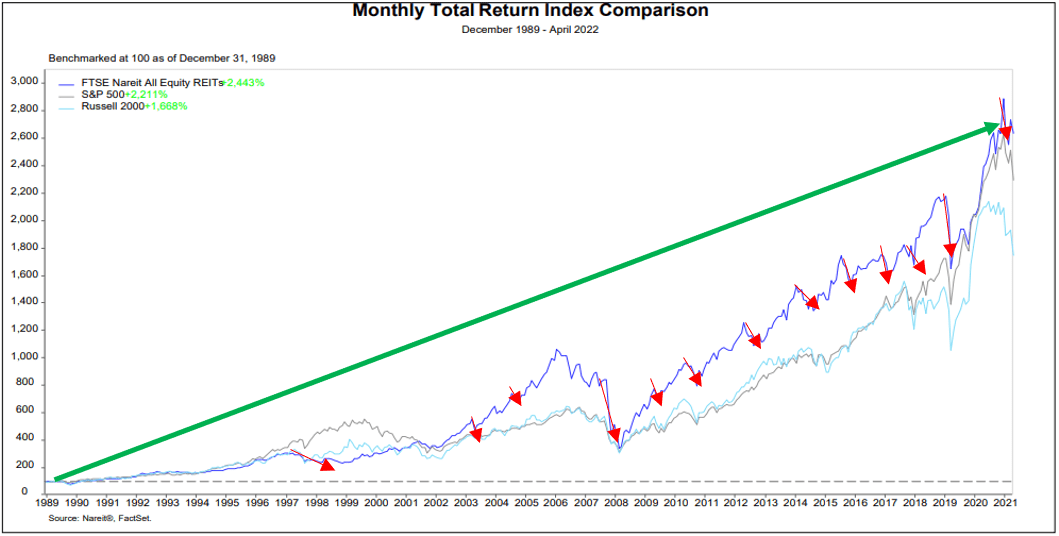

REITs appear to have finally begun their recovery.

The market is finally recognizing that rising interest rates aren't a big threat for most REITs. Balance sheets are the strongest they have ever been and rents continue to grow at a rapid pace, resulting in growing cash flow and dividend payments even in today's environment.

Second quarter results are now rolling in and the good news have sent REIT share prices 7% higher:

But that's still just the beginning of the recovery.

REITs have dropped by over 30% since the beginning of 2022 and this drop happened even as most REITs grew their cash flow by 5-10% since then. Therefore, the real drop in valuations is closer to 35-40%, and most REITs remain heavily discounted even after the recent rally:

While I can't predict what the market will do over the short run, I would note that REITs have historically always fully recovered from every previous market correction , and many of them are today still offering over 50% upside potential just to get back to where they were in early 2022:

{kind=link}

NAREIT

Will REITs recover this time again, or will "this time be different"?

I am strongly in the camp of bulls here.

The high inflation has led to materially higher rents and property replacement costs, and it is only the high-interest rates that have held REIT share prices down.

But now as we get the inflation back under control, interest rates will eventually return to lower levels as the Fed turns to stimulating our weakening economy. Historically, the Fed has always been quick to cut rates following periods of interest rate hikes:

{kind=link}

Fed

This will remove the primary headwind that has been hurting REITs.

And here's the kicker: the now higher rents will remain because the high inflation of recent years won't be "canceled".

Therefore, I expect REITs to rapidly return to new all-time highs, unlocking substantial upside for those who buy them today while valuations remain discounted.

We have cherry-picked a portfolio of the 24 best opportunities to maximize gains in the recovery, and here are two of our Top Picks to buy today:

BSR REIT ( OTCPK:BSRTF / HOM.U)

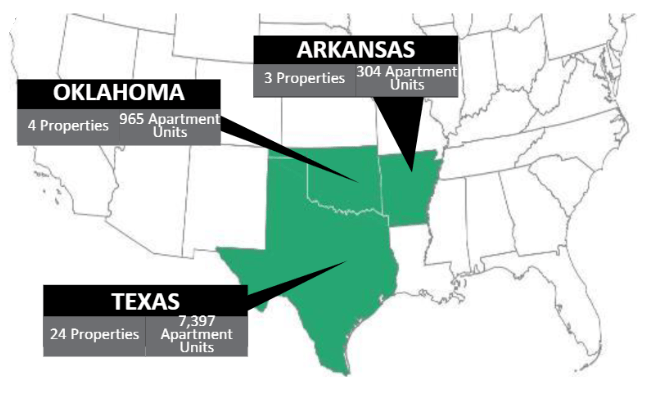

BSR REIT is an apartment REIT that owns a portfolio focusing on the Texan triangle: Houston, Austin, and Dallas.

{kind=link}

BSR REIT

{kind=link}

BSR REIT

I have pitched it quite a few times in the past, but I think that it is especially interesting today because most of its peers have recovered in recent weeks, but BSR missed out on this upside:

I think that this is a market anomaly that's caused by BSR's unique listing.

Despite owning only assets in the US, it is primarily listed in Canada and as a result, its investor base is also very different from those of US-based apartment REITs like Essex Property Trust ( ESS ) and AvalonBay ( AVB ).

I suspect that Canadian investors have been slow to react to the latest good news and this explains why BSR hasn't recovered quite as much as its US peers.

This is an opportunity because, from a fundamental perspective, BSR is actually doing very well.

We all know that Dallas, Austin, and Houston are booming cities and this is well-reflected in BSR's growing rents. In the first quarter of this year, its rents rose by 10.3% and the management made the following statement:

"The results were in line with our expectations and reflect the very strong fundamentals of our core Texas markets...

So our business outlook remains highly positive as we continue to benefit from owning a high quality portfolio in high-growth Texas MSAs."

The REIT also has a strong balance sheet with a low 35% LTV and a strong management team that's well-aligned with shareholders.

And yet, they are today priced at a 38% discount to their latest net asset value estimate. This essentially means that you get to invest in the equity of these properties at 62 cents on the dollar and then you get the added benefits of liquidity, diversification, and professional management on top of that.

The valuation has gotten so low that the management is now buying back shares to create value for shareholders. Here is what they said about their buybacks in the most recent conference call:

"We remain focused on building unitholder value. As previously disclosed, we repurchased approximately 1.08 million units last year under our NCIB and our automatic share purchase plan.

We will continue to take advantage of opportunities to repurchase units as part of our normal evaluation of capital deployment options. It’s obviously an attractive option when our unit price is trading at a significant discount to NAV as it is presently."

I think that as their rents keep on rising, they buy back a bunch of shares, and their share price eventually recovers closer to their NAV, shareholders will enjoy 50%+ upside from here in the coming years.

While you wait, you also earn a 4% dividend yield, which may seem low, but keep in mind that the REIT retains a large chunk of its cash flow to buy back shares. The real cash flow yield is about 7% at today's share price.

We give it a Strong Buy rating.

KKR Real Estate Finance Series A Preferred Shares (KREF.PA)

I know that some of you won't be interested in BSR because of its relatively low dividend yield.

So here is an alternative that yields materially more.

KKR Real Estate Finance is a mortgage REIT that lends capital to other real estate investors and earns interest in exchange for it.

I think that the common equity is relatively risky, especially in today's environment, but I really like its preferred equity, which enjoys greater safety but still offers a generous 8.7% dividend yield at today's share price.

There are other similar opportunities in its peer group, but the main reason why I favor the preferred equity of this mortgage REIT is that its loan portfolio is mostly backed by residential properties and they have relatively little exposure to the office and hotel sectors:

| SECTOR EXPOSURE |

| Residential |

| Office |

| Retail |

| Industrial |

| Hotel |

| Starwood Property ( STWD ) |

| 33% |

| 23% |

| 2% |

| 6% |

| 16% |

| Blackstone Mortgage ( BXMT ) |

| 27% |

| 34% |

| 4% |

| 9% |

| 19% |

| KKR RE Finance ( KREF ) |

| 44% |

| 25% |

| 0% |

| 13% |

| 5% |

| Apollo CRE Finance ( ARI ) |

| 19% |

| 18% |

| 16% |

| 3% |

| 23% |

| Ladder Capital ( LADR ) |

| 37% |

| 24% |

| 6% |

| 7% |

| 4% |

Moreover, 100% of its loan are senior secured and enjoy a floating rate, which is today resulting in growing interest income:

| PORTFOLIO METRICS |

| % Floating Rate |

| % Senior Secured |

| STWD |

| 99% |

| 92% |

| BXMT |

| 100% |

| 100% |

| KREF |

| 100% |

| 100% |

| ARI |

| 99% |

| 93% |

| LADR |

| 88% |

| 99% |

| NREF |

| N/A |

| 41% |

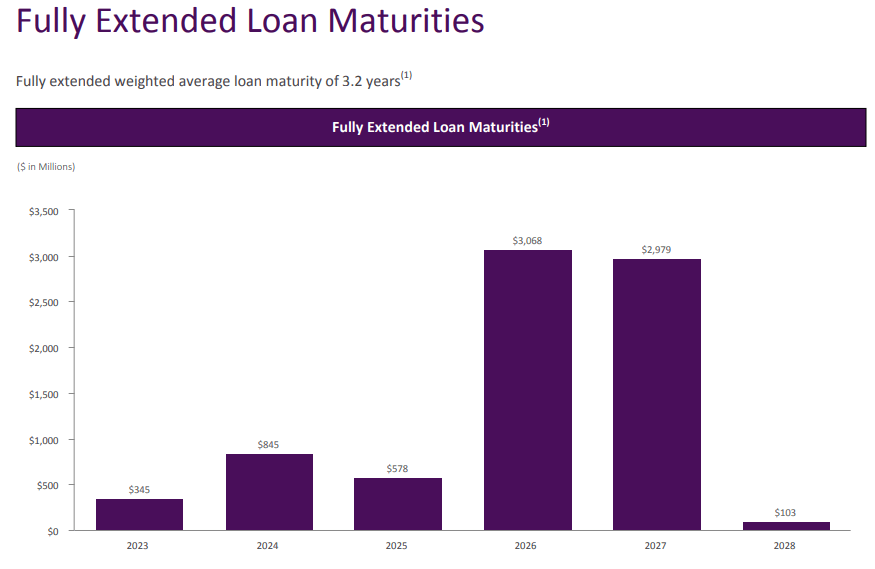

And importantly, they have very limited debt maturities before 2026 - limiting the impact of rising interest expense:

{kind=link}

KKR Real Estate Finance

In the first quarter of this year, the preferred dividend enjoyed a very strong coverage of over 700%. Put differentially, the preferred dividend payout ratio was only about 13.8%. So there is very significant margin of safety.

Moreover, the dividend is also cumulative, which means that they cannot just get away without paying it. Even if they had to temporarily suspend the preferred equity, they would still owe it and have to pay it all at a later date.

Therefore, I believe that the 8.7% dividend yield is very likely to be sustained. Despite that, the preferred shares are today priced at a 25% discount to their par value and offer about 30% upside as they eventually recover.

That's very attractive when paired with the high dividend yield.

Bottom Line

There are lots of opportunities remaining in the REIT sector, even after the recent rally. I think that this is still just the beginning and so I keep accumulating more shares while they remain discounted.

For further details see:

2 'Strong Buy' REITs At Steep Discounts