EFA - 2 Takeaways From BlackRock's Student Of The Market (March) Report

2023-03-30 13:59:19 ET

Summary

- BlackRock's Student of the Market report is a monthly publication that provides insights and analysis on current market trends and developments.

- The report for March 2023 offers some valuable insights for investors. Among the key takeaways are two important observations that can guide future investment decisions.

- This article reveals the historical performance of stocks following inflation peaks and discusses how global equities perform when U.S. stock returns are lackluster.

- This article lays the groundwork for us to make the most of a possible reversal in inflation trends in the coming quarters.

This article was published for members of Leads From Gurus on March 21, 2023.

BlackRock's Student of the Market report is a monthly publication that provides insights and analysis on current market trends and developments. The report for March 2023 offers some valuable insights for investors. Among the key takeaways are two important observations that can guide future investment decisions. The first observation is related to the performance of stocks following the peak of inflation, and the second observation highlights the outperformance of international stocks when U.S. stock returns are low. Both insights can be extremely relevant for investors looking to navigate the volatile and uncertain market conditions in the coming months.

Let's take a closer look at each of these observations and how they can inform investment strategies.

Market Performance Following an Inflation Peak

Inflation is a key economic indicator that has significant implications for investors. Historically, periods of high inflation have been associated with weaker stock market performance, as investors tend to become more cautious and demand higher returns to compensate for the increased uncertainty and risk. However, the relationship between inflation and stock market performance is complex and not always straightforward. For example, in the short term, a sudden increase in inflation can lead to a stock market sell-off as investors reposition their portfolios to protect against rising costs. But in the long term, a moderate level of inflation can be positive for stock market returns, as it reflects a growing economy and rising corporate profits.

Moreover, the performance following peaks in inflation has been mixed. In some instances, a peak in inflation has marked the end of a period of economic expansion and preceded a recession, leading to negative stock market returns. In other cases, inflation has peaked but remained at moderate levels, and the stock market has continued to rise as investors adjusted to the new economic environment.

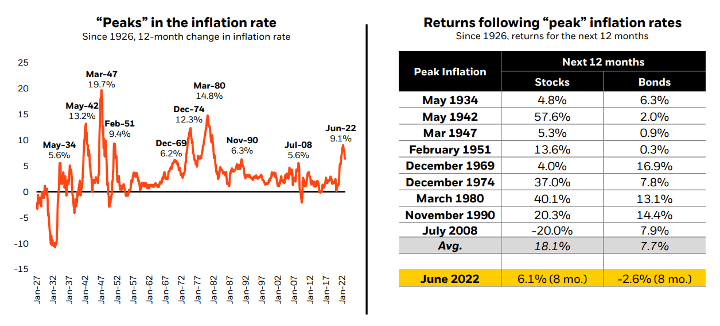

Exhibit 1: Performance of stocks and bonds following peak inflation

{kind=link}

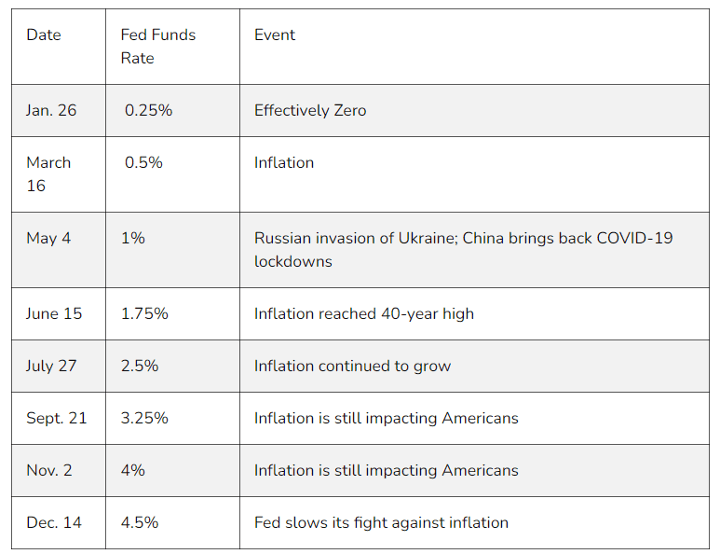

Exhibit 2: Interest rate hikes in 2022

{kind=link}

Based on the data presented in the chart and table above, it is evident that following the peak inflation in June 2022 - which was at a 40-year high of 9.1% - stocks returned a noteworthy 6.1% over the subsequent 8-month period amid a notable increase in the Fed funds rate. On the other hand, bonds lost more than 2.6% during the same period.

A recent study by the Leuthold Group revealed a positive correlation between high inflation rates and stock market performance following the peak of inflation. In contrast, low inflation rates of around 2% to 4% have a negligible impact on the stock market. However, when the inflation rate rises above 4%, the stock market becomes more susceptible to the impact of inflation. Interestingly, research suggests that stocks can perform well even if inflation rates remain high, as long as the rate of acceleration slows down.

The relationship between the Federal Reserve's interest rate policy and stock market performance has been a topic of debate for decades. In particular, there has been a long-standing assumption that when the Fed raises interest rates, stocks tend to decline. However, this assumption is not always accurate, particularly when it comes to peak inflation periods. When the Fed increases interest rates by more than 1% during these times, stocks have historically performed well, while bond performance has been disappointing when this happens.

To understand this, it is important to first consider what happens during periods of peak inflation. During periods of high inflation, the value of money declines, which leads to higher costs for businesses and consumers. This can ultimately lead to lower profits and weaker economic growth. To combat inflation, the Federal Reserve may decide to increase interest rates. Higher interest rates make borrowing more expensive, which in turn can slow down spending and reduce demand for goods and services. This can help to lower inflation rates and stabilize the economy. Although this can have a negative impact on certain sectors, a decrease in the inflation rate can create an opportunity for investors to purchase stocks at a discount.

Following peak inflation, when interest rates begin to increase, certain sectors of the economy tend to perform better than others. Theoretically, we are taught that a few sectors will prove to be winners in a high-interest-rate environment whereas many business sectors will suffer. Financials, for example, often benefit from rising interest rates as they can earn more money from loans and investments. The technology sector, however, may struggle as higher interest rates can make borrowing and investment more expensive. Real estate companies and construction industries may also be negatively affected as higher interest rates can lead to decreased demand for borrowing and buying homes. Consumer discretionary stocks may also struggle as consumers may have less disposable income to spend on non-essential goods and services. Utilities may also be negatively impacted as their costs of borrowing increase.

Although things are supposed to be this way from a theoretical perspective, real-world data shows a notable divergence. What is even more important to understand is that the performance of stocks following peak inflation in a business cycle can be contrastingly different from the market performance in the period leading up to peak inflation.

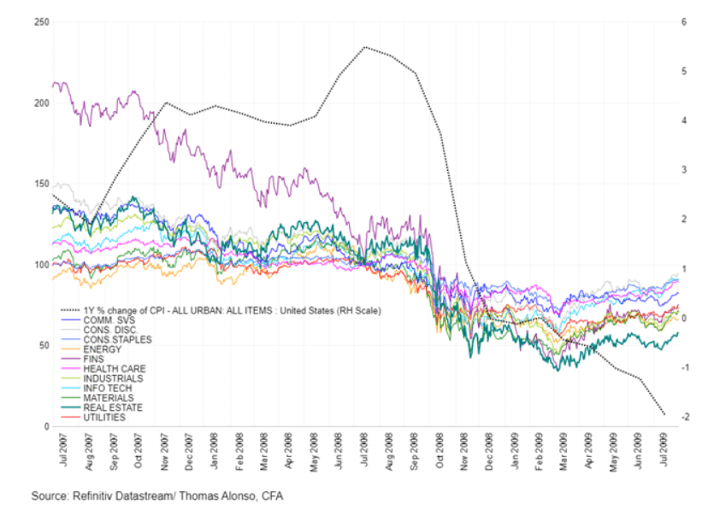

Exhibit 3: S&P 500 sector performance around 2008 inflation peak

{kind=link}

Refinitiv data reveals that during the July 2008 peak, the energy sector was the best performer with 10.5% gains followed by utilities and consumer staples, although the overall market performance was weak due to the global financial crisis. The financial sector was the weakest performer during this period with a loss of 52.2%, followed by consumer discretionary and real estate with losses of 32.1% and 23.9%, respectively. In the year following the peak, consumer discretionary performed the best with a loss of 5.5%, followed by information technology and consumer staples with losses of 8.9% and 9.4%, respectively. Real estate performed the worst with a loss of 42.2% followed by energy with a loss of 33.4%.

Identifying the peak in inflation can be a game-changer because it signals a possible rebound of the stock market after a decline due to inflationary concerns.

A possible reason behind the strong market performance of certain business sectors following peak inflation could be the rising expectations for a less aggressive Fed. The relationship between inflation, the Fed’s interest rate policy, and stock market performance is complex and depends on a variety of factors, including the state of the economy.

Today, with inflation continuing to cool down, empirical evidence gives us hope that better days are ahead for stock investors - especially for growth investors. However, things can still go south primarily because of supply-chain disruptions that could be caused by the ongoing political unrest in Eastern Europe.

The Case for Global Equities

Investors often look to international stocks as a diversification strategy, especially when long-term U.S. stock returns are low. This approach is based on the assumption that international stock markets do not move in tandem with the U.S. stock market and therefore provides a way to mitigate risk.

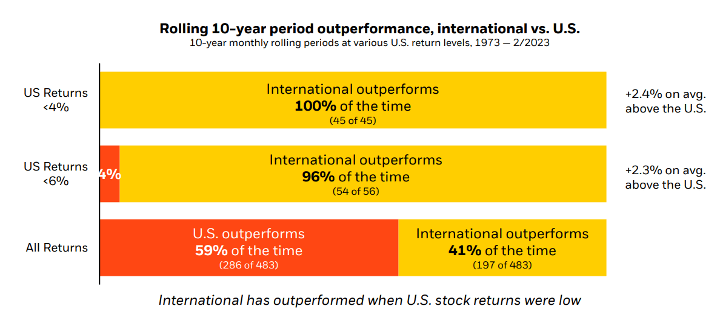

Exhibit 4: International vs U.S stock market returns

{kind=link}

The above chart highlights an interesting finding - international stocks have outperformed whenever U.S. stock returns were below 4%. This indicates that during times of low returns in the U.S. stock market, international stocks have proved to be a better investment opportunity.

The MSCI EAFE ETF, which monitors the progress of foreign stocks from developed economies, has started 2023 with a strong performance. As of today (March 30), the ETF has gained approximately 8.5% this year while the S&P 500 index has gained 5.56%.

The good start to 2023 – after years of U.S. stocks outperforming other developed markets – could be indicative of an opening for us to diversify into other developed markets in search of alpha returns this year. In any case, there are many benefits associated with international stocks.

By investing in international stocks, investors can gain exposure to different regions, industries, and economies, which may perform differently than the U.S. market and economy. In addition, during periods of U.S. market underperformance, institutional investors may shift their focus to international markets in search of higher returns. This can drive up demand for international stocks, leading to increased prices and returns. Additionally, the U.S. dollar may weaken during periods of low U.S. stock returns, which can also boost returns on international investments for American investors due to forex gains.

Over the past decade, the United States has been performing better than most other international markets, causing investors to question their global equity allocation. However, despite this recent performance, international stocks have historically shown positive returns over the long term. In addition, international stocks have shown a tendency to deliver stellar performances during the recovery period from a macroeconomic or geopolitical fallout, which makes this market segment very attractive to us today as the world enters the post-pandemic era. A classic example is the recent comeback of Chinese equities following years of strict mobility restrictions.

Between November 2022 and January 2023, the MSCI China Index delivered an impressive return of 51%, significantly outperforming the S&P 500, which returned only 6.39% during the same period. The reason behind this outperformance was the Chinese government's decision to relax its strict COVID-19 containment policies in November, leading to the reopening of borders and increased travel activity. Additionally, China's technology sector, which makes up a significant portion of the index, saw impressive growth as tech giants came out of regulatory pressures.

Although there is no doubt that investors stand to reap diversification benefits by investing in international equities, it is worth mentioning that the relationship between U.S. and international stocks is not always predictable. In recent years, we have seen a strong correlation between the performance of U.S. and global equities, which complicates the investment decision-making process for us.

The performance of international stocks is tied to the economic and political conditions of the countries where those companies are based. Analyzing each and every country and market sector is easier said than done, and we are bound to make mistakes when investing internationally. Navigating geopolitical risks could be the most difficult part when it comes to analyzing global equities. A classic example is how Russia's invasion of Ukraine wreaked havoc on global stock markets.

One research study analyzed the daily stock market returns of 94 countries from January 22, 2022, to March 24, 2022, and found that the ongoing Ukraine-Russia war had a significant negative impact on global stock indices. The negative effect stemmed from several factors such as geopolitical tensions leading to investor uncertainty, fear of economic sanctions on Russia, and disruption to global trade. When investing globally, it makes sense to use a discount rate in our valuation models that take into account the risks associated with these unforeseen developments.

Currency fluctuations can also impact the performance of international stocks. Therefore, while international stocks can offer diversification benefits, investors should not rely solely on them to provide better returns during periods of low U.S. stock returns. Instead, a well-diversified portfolio should include a mix of asset classes, including both domestic and international stocks, as well as bonds and other investments that can help manage risk.

Takeaway

We are at a crossroads today with inflation beginning to cool down - which could very well be the start of a new business cycle or a temporary distraction. Regardless, it makes sense to look for opportunities in sectors that have historically performed well following peak inflation. Stay tuned for updates on how we can capitalize on our historical findings.

For further details see:

2 Takeaways From BlackRock's Student Of The Market (March) Report