PEUGF - 2 Underappreciated Risks Facing Cleveland-Cliffs

2023-09-25 15:34:38 ET

Summary

- Recent talks surrounding Cleveland-Cliffs have not ventured far from its potential takeover of U.S. Steel.

- However, the stock's underperformance relative to peers and the broader market this year underscores significant immediate risks that remain underappreciated.

- The combination of fluid macroeconomic uncertainties, as well as added pressure from recent UAW negotiations that have gone contentious risks further pressure on domestic steel demand and prices.

- Despite having ~45% of its volumes based on fixed contract pricing, we expect CLF's volumes to be weighted heavily on softening index pricing through 2H23. Meanwhile, the resurgence of inflationary headwinds also risk derailing its cost-reduction ambitions.

Cleveland-Cliffs' stock ( CLF ) has been going through a rough patch this year, underperforming both its steel-making peers as well as the broader market amid uncertainties in the macroeconomic backdrop. In addition to moderating HRC prices on the back of concerns over a slowing economic outlook and tightening financial conditions, the resurgence of energy prices over the summer also risks derailing CLF’s cost reduction efforts. With substantial exposure to the automotive end market, CLF now faces incremental near-term pressure from the expansive UAW strike as well, which we think remains an underappreciated risk. Taken together, the clouded visibility on both the global macroeconomic and commodity environments will likely remain limiting factors on the near-term performance of CLF's stock.

Macro Uncertainties Remain a Key Overhang

Despite easing inflationary pressures observed during the first half of 2023, resilient strength observed in the broader U.S. economy coupled with the robust labour market has urged policymakers to keep rates “ higher for longer ”. Based on the latest quarterly projections from the FOMC, Fed policymakers expect another 25 bps increase before the end of the year, which would take the Fed Funds Rate range to 5.5% to 5.75%. Expectations for easing in 2024 have also been tempered, with the latest Fed dot plot showing a reduction in the FFR range to 5.1% by the end of next year, compared to 4.6% projected in June.

{kind=link}

Bloomberg News

Although the U.S. economy has stayed relatively resilient amid one of the Fed’s most aggressive paces of tightening in decades, the elevated rate environment remains a risk to overall spending levels and, inadvertently, domestic steel demand. This is corroborated by the recent decline in HRC prices, as supply shortages are coming into a better balance with demand over the past several months.

The resurgence of energy prices over the summer also risks reversing some of the progress that monetary policy tightening has made on reining-in decades-high inflation. This is likely to support the Fed’s case in keeping rates in restrictive territory for longer in order to drive a “contraction in credit [needed to] significantly slow economic activity” – which, again, will inadvertently impact domestic steel demand and prices. We expect ongoing macroeconomic challenges to CLF’s near-term growth and profitability performance to unpack in the following adverse combination – declining prices and rising costs:

1. Declining average net selling price per ton – CLF’s revenues and profitability have significant exposure to domestic HRC price performance, despite having close to half of its contracted sales portfolio under a fixed-pricing arrangement. Although the company had previously expected healthy domestic steel demand in its latest 2Q23 10Q filing, the combination of weakening sentiment among buyers based on recent industry checks and ongoing HRC price pressures are likely to weigh further on CLF’s average price per net ton (“ASP”). We expect this backdrop to bode unfavourably for CLF through 2H23, especially as its volume mix is likely to shift away from fixed to spot pricing.

This is corroborated by management’s clarification that CLF’s ASP strength during the second quarter was primarily driven by robust demand from the automotive end-market, which had been pulled forward ahead of the UAW negotiations. Now, with the UAW strikes becoming more pervasive and potentially longer-lasting than previously expected, the adverse impact on demand is likely to become more challenging. The combination of broader HRC pricing weakness and a greater mix shift to spot-driven volumes expected at CLF heading into 2H23 is likely to drive its ASP down. This risks weighing further on CLF’s profitability and cash flows critical to its ongoing deleveraging efforts and shareholder returns program.

2. Rising cost pressures – The resurgence of energy costs also risks a direct impact on CLF’s profit margins. Recall in 2022 when CLF faced acute inflationary pressures due to elevated energy and input costs, as well as the subsequent improvements observed through 1H23 on the back of easing input prices – both scenarios underscore the business’ significant sensitivity to energy price fluctuations.

Oil prices have surged 30% since late June, as the tightening physical market is quickly overshadowing previous skepticism on weak demand prospects from the downward-spiralling U.S. and Chinese economies. We believe CLF’s optimistic expectations that lower energy and input costs experienced in 1H23 will persist through 2023 and beyond, as disclosed in its latest 10Q filing, might have been premature. This risks derailing management’s target for a $50 per ton reduction in steel costs through 2H23 (~$40 per ton reduction expected to be realizable in Q3, and another $10 per ton reduction realizable in Q4).

The UAW Strike Remains an Underappreciated Risk

In addition to “muddled visibility” on the global macroeconomic backdrop, CLF’s near-term performance also faces heightened risks of an extended UAW strike. We believe the ongoing UAW negotiations remain an underappreciated risk – even by management, as CEO Lourenco Goncalves reiterates his expectations that the strike will not have a material impact on near-term steel demand.

Instead of targeting the strongest of the Big 3 like it has done in past contract negotiations, the UAW has instead opted for a strategic walkout this time around. When the Big 3 and UAW negotiations ended in no deal upon expiry of the preceding contract on September 14, the union started striking at select facilities across all of Ford ( F ), GM ( GM ) and Stellantis ( STLA ) on the following day. About 13,000 UAW workers from three manufacturing facilities joined the picket line during the first week of the strike, with another 38 plants affecting GM and Stellantis added to the list this week as negotiations progress. The strategy is likely to drag the strike through at least October, when the $825 million strike fund is expected to near exhaustion – even on a spaced-out strike strategy – and vehicle inventories are expected to take a hit.

Current market projections expect lost output of as many as 100,000 vehicles over the same period, which is expected to displace more than 98,000 tons of steel production. As a result, HRC prices could mirror the 17% drop observed during the six-week 2019 UAW-led strike at GM, and approach the $600 range from current levels .

This is a significant risk to CLF’s near-term growth outlook, given its significant exposure to demand dynamics in the automotive end market – more than a third of its quarterly revenues are currently generated from automotive steelmaking and other automotive sales. While Goncalves is optimistic CLF will emerge from the latest debacle unscathed, the company’s peers have already started to pre-emptively idle capacity, in addition to pre-scheduled maintenance outage. The Big 3 collectively commands close to half ( STLA 11% ; GM 17% ; F 13% ) of U.S. light vehicle market share, and is poised to impact automotive steel demand and market prices in the face of an extended UAW strike and ensuing disruptions to production. This circles back to our concerns raised in the earlier section that near-term volumes risk being index-pricing weighted, which will add pressure to CLF’s ASP.

In addition to anticipated impacts on near-term steel demand and pricing, the ongoing UAW strike could also adversely affect prime scrap availability due to reduced auto production. This is expected to counter management’s optimism to CLF’s ongoing cost reduction efforts, which has been alluded in part to lower scrap costs observed during the first half of the year. The overall expectation for reduced scrap availability also risks impacting CLF’s vertically integrated cost advantage achieved following its 2021 acquisition of Ferrous Processing and Trading Company (“FPT”) – one of the largest prime scrap processors in the U.S. CLF also uses close to 30% scrap in its basic oxygen furnace (“BOF”) footprint, underscoring its exposure to impending scrap pricing pressures. The near-term risk is also broadly in line with “ growing bullish sentiment for the September U.S. ferrous trade” driven by uncertainties over the UAW negotiations.

The Bottom Line

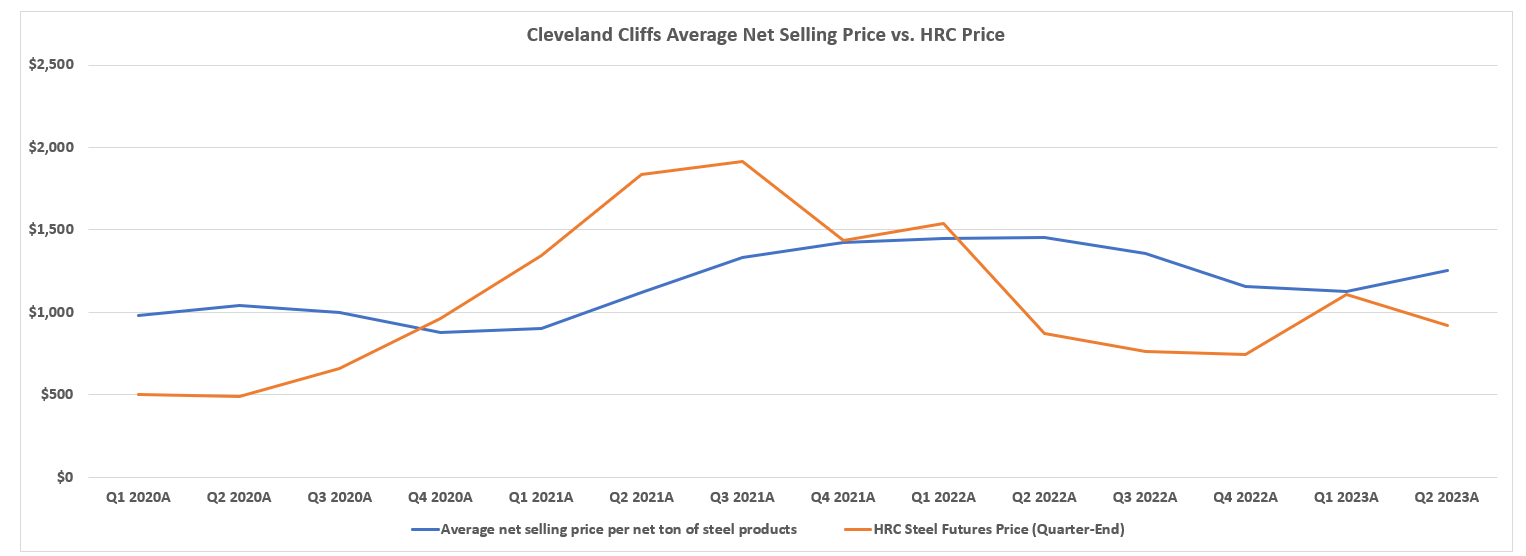

Admittedly, CLF has made some positive progress in 1H23 in maintaining operating leverage, driven primarily by a favourable sales mix weighted towards stronger-priced automotive volumes, as well as ongoing cost-reduction initiatives. Specifically, automotive steelmaking sales, which are primarily dictated by fixed pricing contracts that account for 45% of CLF’s portfolio, have been critical to shielding the company from HRC price fluctuations in 1H23. Leveraging its value proposition in being a key supplier of carbon-friendly steel to the automotive sector, the company was able to increase the ASP to its “direct carbon steel automotive customers” by 8% to $1,400 per ton under the full-year 2023 fixed pricing arrangement. The ensuing strength is corroborated by CLF’s rising ASP in recent quarters, defying a downward trend in HRC pricing:

{kind=link}

Author, with data from CLF quarterly filings

The company is also in the process of implementing an additional $40 per net ton “Cliffs H” surcharge on the sale of its blast furnace steel, with an intention to bolster its share of automotive dollars. Produced with hot briquetted iron (“HBI”) feedstock, CLF’s blast furnace steel boasts a competitive ESG advantage and appeals to automakers’ demand for more “carbon-friendly steel”.

However, persistent macroeconomic headwinds, exacerbated by limited visibility over the latest round of UAW strikes, risk reversing some of CLF’s progress. The company disclosed that it had 55% of its portfolio exposure to index pricing. And the expectation for lower automotive-related volumes in the second half is expected to increase CLF’s sensitivity to softening index prices.

Although CLF’s prescient engagement in ESG-conscious steelmaking has given it a first-mover advantage to peers, there is also much left to do in improving the strategy’s economics in order to drive a sustainable impact on the company’s profit expansion trajectory. Meanwhile, expectations for an elevated wage headwind on automakers’ longer-term profitability based on the UAW’s demands for a 36% pay raise could also structurally increase the end-market’s price sensitivity, especially as OEMs embark on a capital-intensive multi-year transition to electric. This keeps us skeptical of CLF’s implementation of the Cliffs H surcharge (and potentially a future H2 surcharge), which could become a deterrence factor to demand over the longer-term, instead of an accretive feature to margins – especially as competition picks up with rivals’ introduction of eco-friendly equivalents .

Taken together, we expect CLF’s ASP premium to index pricing to diminish again. Weakening durability to CLF's price advantage in the near-term could potentially thwart consistency in CLF’s impressive FCF generation observed in recent quarters. This accordingly raises risks of disruption to the company's full-year deleveraging prospects (CLF is still $1 billion out from its net debt target of $3 billion by year-end), and further sours our confidence in the stock.

For further details see:

2 Underappreciated Risks Facing Cleveland-Cliffs