SCGLY - 2 Undervalued Finance Picks With Massive 3-Year RoR

2023-07-28 10:27:48 ET

Summary

- I'm currently investing in two BBB-rated companies with a 6.5% yield and a triple-digit conservative RoR on a 3-year basis.

- The first company is Société Générale, a French bank with a well-covered dividend yield of nearly 7% and an A rating by S&P Global, the second is Lincoln National.

- Despite a longer-than-expected restructuring period, the SocGen's earnings are expected to recover in 2024, making it a good investment opportunity due to its undervaluation and mispricing.

Dear readers/followers,

It's time for an article where I compare, and show you two companies that I am currently investing in. For one of them, if you haven't been buying, you've already missed a bit of the opportunity here.

For the other, the opportunity is still very much there.

What do these companies have in common then?

- Both companies are BBB rated or above.

- Both companies have a 6.3% yield, well-covered, or above

- Both companies have a triple-digit conservative RoR on a 3-year basis, where I have a high conviction.

- I have more than 1% of my private or commercial portfolio - or both - in each. I have skin in the game.

Pretty convincing qualities and stats, right?

So let's get going and let's see what we have here.

First up, we have Société Générale ( SCGLY ).

1. Société Générale

For those of you across the pond, meaning in the US, this is a French bank. It also happens to be France's third largest bank in terms of pure assets after BNP Paribas (BNPQF) and Credit Agricole ( CRARY ).

I own all three of these banks, but my by far largest position is in Société Générale or SocGen.

Why is that?

The company is one of the oldest banks in Europe, being founded in 1864 under the original name of Société Générale pour favoriser le développement du commerce et de l'industrie en France (English: General Company to Support the Development of Commerce and Industry in France).

The company has been a ubiquitous part of France's finance world for over 150 years and being privatized again in 1987, it's one of the higher-rated banks in France.

For European/investors with access to the Paris stock market, the ticker is GLE.

For US Investors, the ticker here is the ADR SCGLY.

The bank yields nearly 7% well-covered dividend yield. It's rated A by S&P Global.

The reason it's been trading down in the dumps for a number of years is a bank-wide restructuring that's taken longer than anticipated, and where reversal to impressive growth has also been impacted for longer than expected.

But as of the latest quarterly, we now have better visibility for recovery in the bank's earnings. It's not in 2023 - but in 2024E . The bank relatively recently reported its 1Q23 , an d the results here were partially encouraging.

SocGen is one of the more expensively-managed banks in Europe with a C/I of 60.5%, compared to some Scandinavian ones coming in below 40%. However, given its size, it has an extremely low cost of risk at 13 bips. It has a very conservative portfolio of loans - less than €200M are in stage 3/NPL.

SocGen has a liquidity coverage ratio of 171%, and for the past few years, we've seen stability in both earnings and revenues. Despite ongoing inflation and European troubles, the company's NPL ratio is actually down.

SocGen IR (SocGen IR)

The company's ongoing provision for NPLs and defaults are more than 2x what they need to be, based on realistic stage 1, 2, and 3 loans. The company's corporate exposure is one of the best in the industry. It's a 66/34 Non-corporate to corporate EaD, and the corporate sector has no more than 7.1% exposure to any one sector - finance - and nothing except finance has more than 3.2% of the total exposure.

Exposure to real estate is less than 3.2% of corporate EaD, of which less than 2% is to commercial real estate. The company's entire loan portfolio in origination is at an average LTV of 50% and unlike most banks, it has a low office exposure.

Direct LBO exposure is less than 0.4% of the total bank exposure at default - and the company has a very conservative process for LBOs.

Russia, seeing that French finance had some ties here?

There's some left - but it's down 50% since late 2021. The total exposure at default is now down to €1.6B, which might sound much but isn't for a bank the size of SocGen.

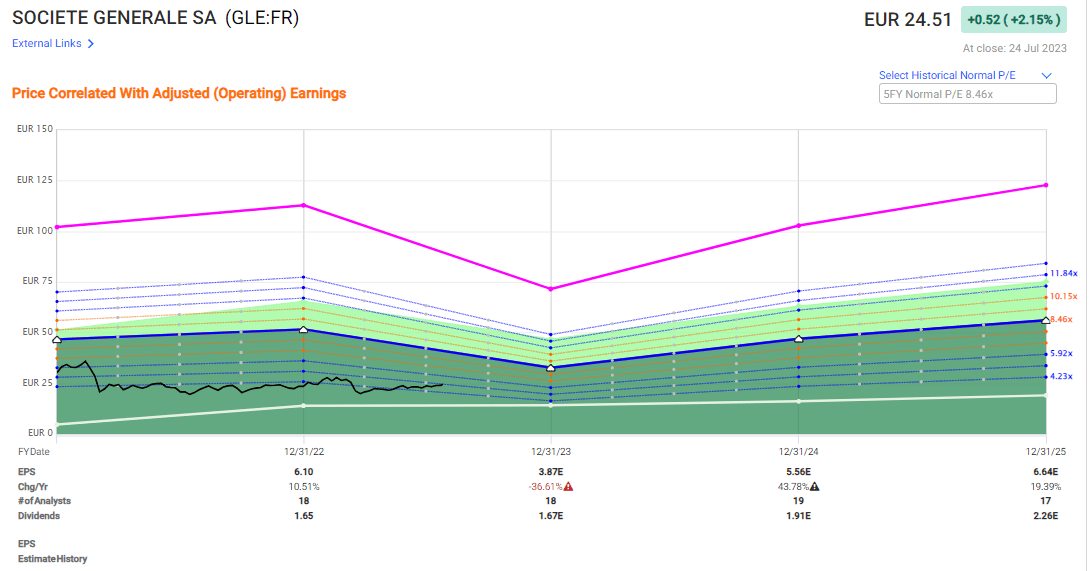

The opportunity here, as I see it, is simple. Take advantage of an undervaluation and mispricing of a French bank and buy shares at a P/E of less than 5x for the 2023-2024 earnings.

{kind=link}

Societe Generale Valuation (F.A.S.T graphs)

This might be one of the lowest-valued A-rated credit companies you've been able to buy all 2023. No, 2023 won't be a good year. Yes, it seems all but inevitable that the bank goes up in earnings in 2024. Unlike many banks, SocGen is, due to the French retail market, the impact of regulated savings, usury loan rate, and some other factors, not yet seeing the advantages of the high-interest rates.

That will likely turn around in 2024, at least according to these estimates - and I view them with a high amount of conviction. This company has been through a long series of restructurings. Still, if you followed my articles in conjunction with the COVID-19 pandemic, and bought when I did at around €12-€13, not even the lowest, you'd have made 30% RoR annualized, or over 130% total return.

That's obviously a very good RoR, but I expect a lot more from this bank.

'Even at just normalized 8X P/E, which is the company's historical 5-year valuation target, you could make almost 150% RoR in less than 4 years going forward, at an annualized RoR of 44.34%.

Too high? Fine - forecast it at a range of 5-6x P/E. That's where it trades today. A 5-5x P/E range at those profit levels would still imply a 26% annualized RoR, increasing your investment by a 75%+ RoR at the same time - and that's the very conservative case that I would see here.

In short, the upside for SocGen here is significant - and I see very little reason not to invest here.

The one thing you should note as a US-based investor, or if you don't have a DTS with France where you live, is that the withholding taxes may be significant. I'm able to recover over 99% of them - so it's not a concern to me - but you should check this prior to investing.

Let's look at option #2 - because this one isn't affected by withholding taxes.

2. Lincoln National Corporation ( LNC )

I've been beating the drum for Lincoln National since they crashed and I've been building both my private and commercial positions to sizeable allocations at good prices. My commercial position is currently at the best RoR - I'm up close to 33% with dividends and FX, having managed to enter the investment at a very appealing cost basis overall. My private stake is still in the negative - I went in early here.

This does not faze me. I believe the reversal potential in this company has only just begun.

LNC is an insurance company that's fallen on hard times due to risk re-evaluation. Whenever a company holds a fair bit of risk on its balance sheet, there are always assumptions for how this risk is calculated and how this impacts, from a capital perspective. This is why, no matter how great the company is, I never go above a 4-5% holding size - not even in world-class companies like Allianz ( ALIZY ) and Munich RE ( MURGY ).

I'm no stranger to this sort of risk or these sorts of plays. In fact, one of the better investments that's trackable here in SA I've made in the U.S. market is Unum ( UNM ), where I ended up with a 150% RoR in a very similar situation. The difference with UNM was that they did not drop quite as low as LNC did.

For Unum, the closest similar company, it was a trip starting at below $16/share, to where it traded at over $44/share.

Let me make something clear here.

I have no doubt that LNC will recover as a business. Otherwise, I wouldn't be still holding the position, I would have sold it. However, that recovery is likely to take a year, two, or potentially more.

My personal stance is that the market grossly overreacted to this company's situation and that there exists a whole lot of sentiment based not on logical understanding of what the company does, and the actual risk involved.

This lack of understanding for insurance companies is not surprising, because insurance businesses are not easily-understood entities. They are often compared to banks, but this is not relevant. Insurance companies are far less vulnerable to risks faced by banks, because they match liabilities and assets far better, making "runs" on the companies is unlikely - and even impossible. Sudden liquidity needs for insurers, especially in P&C, which is most exposed due to their climate/natural disaster exposures, are in turn matched with reinsurance protection.

Any sort of insurance liquidity crunch, even though finance is being punished, in this sector is extremely unlikely, as I see it. You can't compare asset/liability matching in the two industries.

Higher interest rates mean higher reinvestments in bond portfolios and as long as they can sit out those losses, which they typically can because there is no scenario where an immediate need for capital in the business is apparent, there really isn't an issue. Also - insurance bond portfolios tend to be much shorter durations than banks on average.

This is why I believe that Lincoln National remains far less risky than some of its earnings trends would suggest. The company is likely to see an excellent reversal in earnings, and over the past few quarters, Lincoln has also made good headway. While earnings are expected to stay muted for the foreseeable few quarters, the reversal is likely.

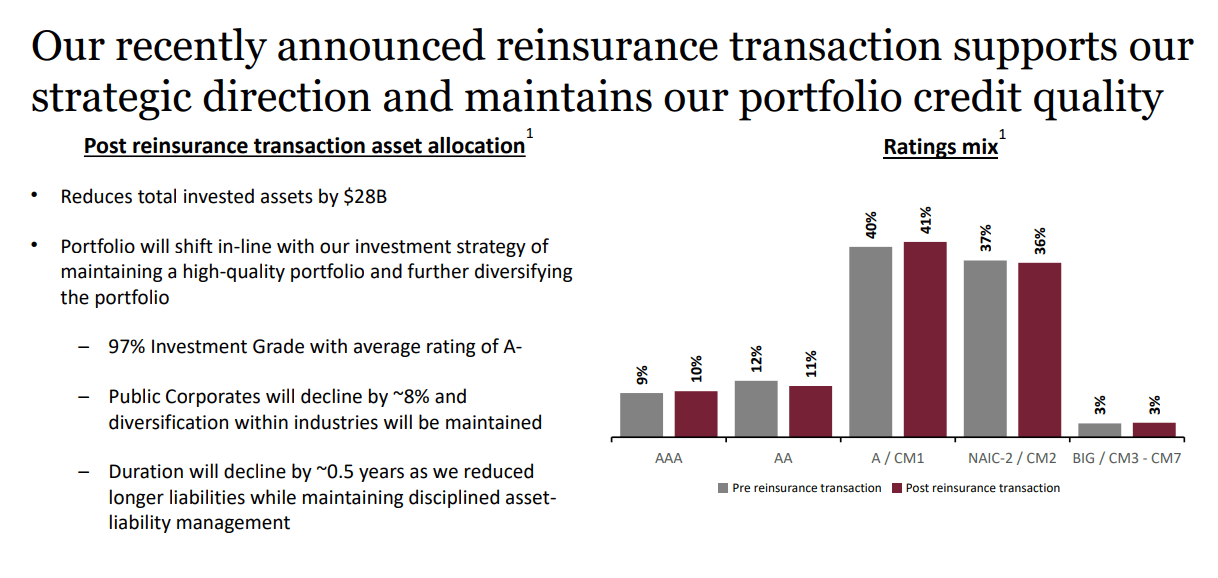

And remember, the company has already gone through some transactions in the reinsurance sector - $28B to be specific - that is in line with its overall target, including a now-97% investment grade A- or above. The company is in no way clear in its recovery or out of the woods just yet. The net loss available to common shareholders for 1Q23 is clear on that.

However , the market is underestimating the pace at which LNC is rebuilding its capital and the pace through which new capita is being generated. Business growth is solid, and the company is working on its overall product mix while delivering good sales. The Fortitude Re transaction to me is confirmation that LNC very much can move swiftly on the market to bolster its impaired numbers.

Earnings will continue to be lower than in previous years. For now.

But that's the key here "For now".

The problem for Lincoln has been, and still is the cadence and amount of legacy in-force life business. As of this Re transaction, management is very pleased with its overall life business, as well as sales. Optimization is ongoing, they're not "done" optimizing (that much is confirmed in the 1Q23 call), but the potential for normalization is massive.

I also want to give you some additional color on just how low-risk LNC has tilted its investment portfolio at this time.

But just to give you a sense of how this has worked in terms of the overall shift. So over the last couple of years, we have been shifting, first of all, away from public corporates. We have increased the overall credit quality. So if you look year-over-year, our single A and above has increased by about 200 basis points, and the decrease has come from -- we have a lower allocation now to overall BBBs.

And within there, the lowest allocation that we've ever had to BBB- and BBB minuses on negative outlook, and our below investment grade has also decreased by about another 100 basis points. And we've shifted out of cyclical sectors that tend to not hold up well during an economic cycle. In the mortgage portfolio, in particular, there, some of what we have done is that we have been shifting into industrial, in particular, and we've increased our overall industrial exposure inside of the commercial mortgage loan portfolio by about 600 basis points and a negative 400 basis points, as Chris highlighted, away from office and another about minus 200 as it relates to retail.

(Source: Ellen Cooper, 1Q23 Earnings Call )

It now looks like this post-transaction for reinsurance.

{kind=link}

LNC IR (LNC IR)

And this is in terms of the overall investment portfolio.

LNC IR (LNC IR)

The company's investment-grade exposure is the highest it's been in over 10 years, with less than 5% banking exposure, less than 1.5% regional banking exposure with 0.04% in failed regional banks. That's below a rounding error.

The fixed income portfolio saw, despite headwinds, the seventh consecutive quarter of positive net ratings migration, meaning the rating allocation, with BBB now up towards BBB+ and down in the BBB- quality. Banking exposure, to give some granularity, is more than 97.5% in A-rating, and it's focused on the largest banks in the world, with no exposure to Swiss AT1 securities, as some financials had.

Its CML portfolio is extremely well-diversified, with less than 2% maturities in 2023, less than 4% in 2024, and less than 5% in 2025. They also, as they said in the call, reduced office exposure by 400 bps in less than 3 years - and this portfolio is conservatively positioned with extremely few near-term maturities, an average loan size of $16M, average service coverage of 2.3x and occupancy at 88%+ with LTV at 46.

As I said - extremely conservative.

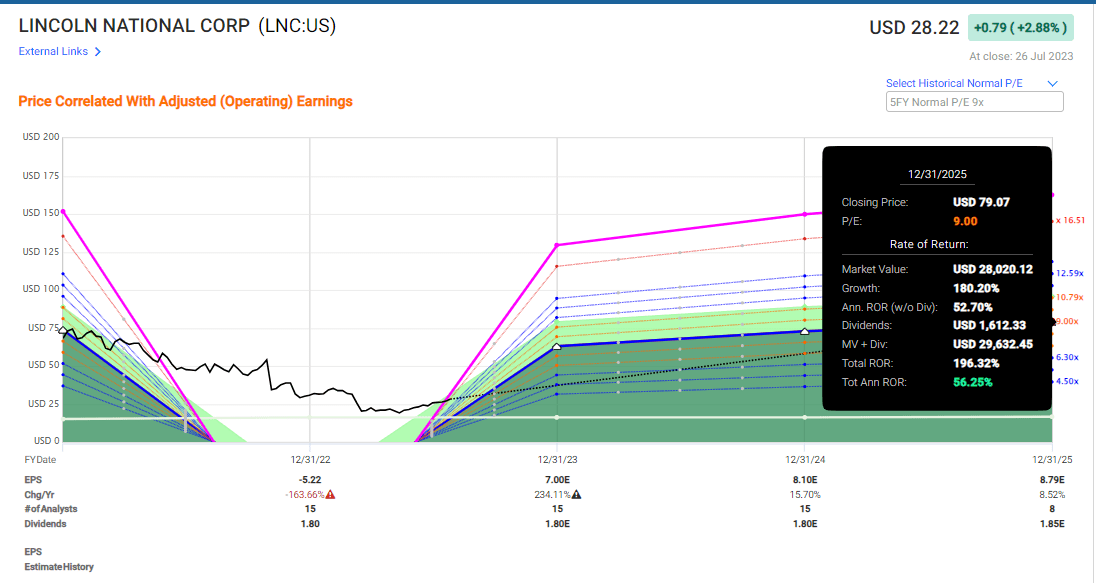

That's the thing. LNC has always been a very conservative insurance company. That's why I bought them in the first place. Then the crash happened, and while my original position went deep in the red, it went from an A-rated conservative investment with a 10-18% annualized to a high-RoR reversal investment with a realistic RoR of 190%+ at a P/E of 9x

That's right.

A forward P/E o f 9x gives you an annualized potential RoR of 56% - and mind you, that's at a current share price of $28.22

{kind=link}

LNC Upside (F.A.S.T graphs)

I bought the lion's share of my commercial position at below $21/share. You can imagine the potential RoR I see if the company does, over time, go back to that 9x P/E.

I also want to highlight the fact that while there is some forecast ambiguity to LNC, the bulk of that ambiguity is in fact on the positive side. Analysts miss their targets 42% of the time for the company with a 10% MoE, but that's because 42% of the time, LNC actually does better than expected.

There's no doubt that this was an unexpected development to what not long ago was an A-rated insurance company. It's now BBB+. The yield was below 4%. It's now 6.4%. At my cost basis, I have over 8% yield. I'm also up more than 30% already, but expect far more - and my original position will, without a doubt in my mind, revert as well.

S&P Global analysts have not yet adjusted or recovered their targets for LNC. 12 analysts are giving the company an average of $25/share from a low of $17/share up to $31/share high. That's compared to a low of $45/share up to $95/share 1 year ago, with an average of $70/share.

So what analysts are saying is that because of what happened with the company, LNC is worth about 33% as a company, compared to one year ago.

Does this sound realistic to you?

The same thing happened with UNM.

I was happy to take advantage of that and make triple-digit returns. This time around, I'm in "deeper" - both in conviction and in the amount of capital invested. I stand to make a fortune, if (or as I see it "when") the company reverts over time.

I'm willing to wait for that, as I was with UNM.

Are you?

Wrapping Up

I try to periodically take a break from company-specific articles to give you a small list, or a couple of companies that I consider to be especially worth investing in at this time.

These are two finance companies that have not yet seen the reversal in finance we're seeing in investments like Truist ( TFC ), overall Banks in Europe, Canada, or other financials in other areas.

When I find investments, I categorize them differently. Some are for income. Some are purely for reversal/capital appreciation, with only a very small dividend.

But in some cases, you can find combinations.

These two companies represent such strong combinations to me - and I'm long both.

Questions?

Let me know!

For further details see:

2 Undervalued Finance Picks With Massive 3-Year RoR