QQQ - 2007 Deja Vu

2023-10-19 16:43:18 ET

Summary

- Treasury yields just reached their highest levels since 2007, causing yesterday's selloff in equities and increasing my sense of "deja vu."

- Mortgage rates also just touched eight percent for the first time since 2000 and mortgage application volume just hit lows not seen since 1995.

- However, it is about the commercial real estate market that investors should be the most concerned right now.

- Delinquency rates are rising quickly, a huge amount of CRE debt needs to be refinanced in the years ahead, and the regional banking system has much exposure to this area.

- Just like in 2007, the economic forecast in the year ahead is looking increasingly problematic, and discretion is the better part of valor for investors at current trading levels.

Déjà vu is simply remembrance of the future .? Wayne Gerard Trotman.

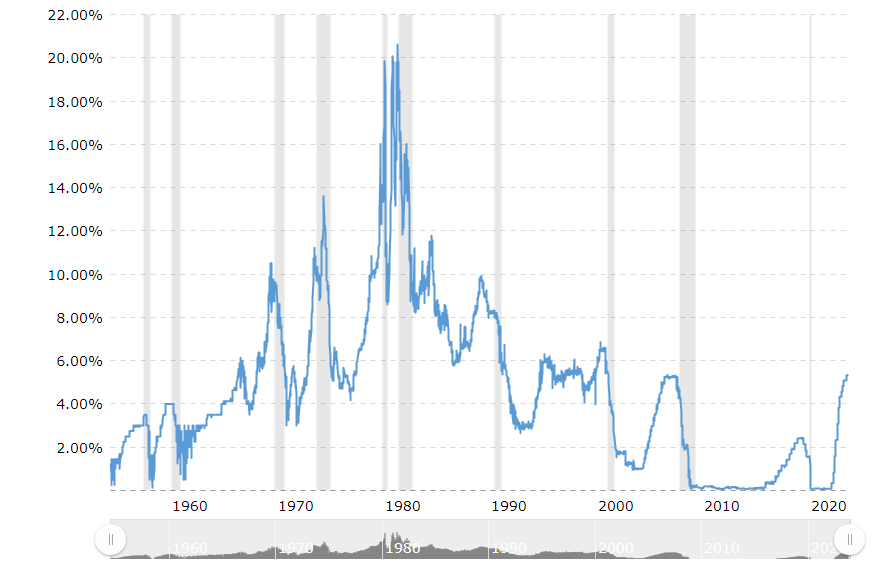

The yield on the two (US2Y), ten (US10Y), and 30-year (US30Y) treasury notes rose on Wednesday to their highest levels since 2007, some 16 years ago. This led to a broad-based selloff in equities, with the NASDAQ (COMP.IND) losing 1.62% on the day. The S&P 500 (SP 500) was off a bit over 1.3% and the Dow Jones (DJI) fell nearly one percent. The higher beta parts of the market fared even worse with the small-cap Russell 2000 (RTY) falling 2.15.

!0-Year Treasury Yield (MarketWatch)

After moving up 74 bps in the third quarter, the yield on the 10-year Treasury is rapidly approaching the five percent mark. As I have written about a couple of times ( I , II ) over the past few months, it is feeling more and more like 2007 to this old investor.

Much like in 2007, we have a President who is flailing in the polls, the U.S. is involved in a potential conflagration in the Middle East, and an election lurks in the year ahead. Just like 2007, we have had a noticeable uptick in stress on the banking system with the second, third, and fourth-largest bank failures in U.S. history recorded in the first half of this year, headlined by the collapse of Silicon Valley Bank.

Average U.S. Home Prices (St. Louis Federal Reserve)

However, it is the real estate market that most reminds me of that infamous year just over a decade and a half ago. Easy credit in the 2000s stoked a huge rise in home prices leading into 2007 before they started to falter. Cheap money and sub-3% mortgage rates sparked an approximate 30% rise in the average U.S. home price of the pandemic this time around.

Mortgage News Daily

Just like in 2007, existing home sales are starting to increasingly be negatively impacted, as the 30-year mortgage rate just touched the eight percent level for the first time since 2000. Mortgage application volume also just hit its lowest level since 1995. Residential real estate investment has now contracted for nine straight quarters, the longest such streak since the housing market burst.

National Association of Realtors

Housing affordability (chart above) is in the toilet from a historical perspective. A $400,000 home with 20% down now costs $1,000 more a month on a conventional 30-year mortgage than it did two years ago, when mortgage rates were at three percent. The vice president of enterprise research at ICE was recently on CNBC stating to get back to " normal" housing affordability levels, average incomes would have to rise 55 percent or home prices would have to come down 35 percent.

Home prices have held up solidly up to this point, thanks largely to the lack of inventory as a result of so many homeowners having " golden handcuffs" of a low existing mortgage rate on their current property. Home foreclosures are up 34% from the same time a year ago, a figure that is likely to move higher in the months ahead. High mortgage rates are going to continue to be a considerable headwind to homebuilders, and it is one reason I have some out of the money, long-dated bear put spreads against the SPDR® S&P Homebuilders ETF ( XHB ) right now. Lower new home sales will also impact the ancillary industries that are driven by new homes being built. Think the likes of Home Depot ( HD ) , Williams-Sonoma ( WSM ), and Ethan Allen Interiors Inc. ( ETD ) .

The most likely path ahead is for average home prices to fall in the quarters ahead in the United States. Fortunately, this will not trigger a financial crisis like in 2007. There is simply too much equity in homes, as credit criteria were tightened considerably after the Great Financial Crisis. The days of low or no down payments and " liar loans" have been in the rearview mirror for more than a decade now.

However, as Mark Twain famously quipped " History doesn't repeat itself, but it does rhyme ." While the residential real estate market should weather the approaching storm, I am much less sanguine about the prospects for commercial real estate. A concern I first documented over the summer in an article entitled " Commercial Real Estate: The New Potential 'Subprime .'"

The environment around commercial real estate, or CRE, has deteriorated since I penned that piece three months ago. The delinquency rate on CRE loans secured by office buildings rose 139bps from August to 10.75% in September.

Morgan Stanley Research, Trepp

This truly is concerning, as interest rates continue to rise given how much CRE debt has to be rolled over in the coming years. Office building values have imploded in many major cities thanks to the virtual workforce exploding as a result of the pandemic and lockdowns. If an investor wants to keep track of how fast office and other CRE properties are being marked down in value, I advise you to follow this Twitter feed . It provides a smorgasbord of data points around an increasingly dire situation across the CRE universe.

Rising delinquency rates, increasing write-offs and fast falling property values have me increasingly worried about the regional banking system. Regional banks hold approximately 30% of CRE loans and originate some 70% of them. As noted previously, we have already seen three high profile regional banks fail earlier in the year. My bet is more will follow, and it is why I have built an out of the money, long-dated bear put position against the SPDR® S&P Regional Banking ETF ( KRE ) .

The good news is the major banks have less concentration and exposure to CRE loans. Their balance sheets are also in much better shape with higher reserves than going into the Great Financial Crisis. Third quarter results from the likes of JPMorgan Chase & Co. ( JPM ) confirm the sound footing they currently enjoy.

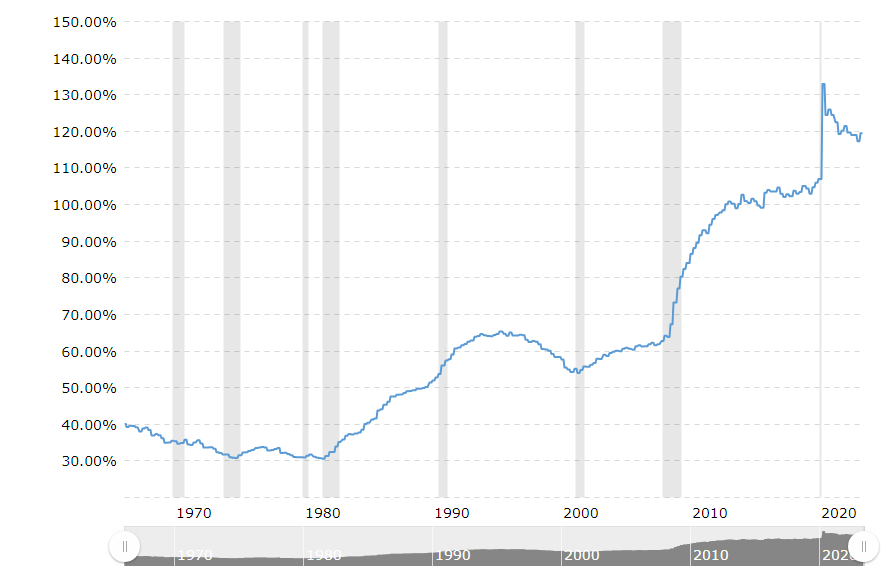

U.S. National Debt Compared to GDP (Macrotrends)

{kind=link}

Unfortunately, I cannot say the same thing about the federal government, which bailed out major financial institutions during the last financial crisis. As can be seen from the chart above, the U.S. debt to GDP level ratio has exploded since the Great Financial Crisis and now stands a bit over 120%, levels only seen during WWII in the country's history.

{kind=link}

In addition, interest rates were lower in 2007. At the close of that year, the Fed Funds rate stood a tad over four percent and was just under three percent in March 2008. The Fed Funds rate currently stands solidly over five percent. To finance the current national debt of over $33 trillion at the current Fed Funds rate would cost north of $1.7 trillion annually, for anyone who needs a scary thought heading into Halloween.

I don't foresee as dire of a situation as the one that led to the Great Financial Crisis, mostly because CRE is a smaller market than residential real estate. However, I put the odds of avoiding a recession in 2024 given these headwinds and debt loads at these interest rate levels as very low.

Therefore, 50% of my current portfolio is in short-term treasuries which yield 5.5%, nearly two percent above the current level of inflation measured by the CPI. It is a good return and one that I noted earlier this week was likely to outperform the overall market in the quarters ahead.

Finally, two pieces of advice to investors inclined to believe Federal Reserve and Treasury officials as well as the financial pundits that litter the financial media airwaves about the likely economic scenario in front of us being a "s oft landing ." The first is these are the same institutions that assured the country in 2007 that the subprime crisis was " contained" and problems in the housing market would not bleed over to the larger economy or the markets. The second piece of wisdom is to always remember that five of the most dangerous words in the English language are " It is different this time ."

Sometimes I have these premonitions and I don't forget them, so I will be prepared when they happen. "? Isabel Allende.

For further details see:

2007 Deja Vu