QQQ - 2023 Q1 GDP Sets Up 2nd Half Recession And 'Stagflation'

2023-04-27 13:30:13 ET

Summary

- Consumer spending kept GDP barely above zero at 1.1%.

- 2023 Q2 will likely print at half that or lower on a glidepath to recession.

- But the second half recession won't kill inflation; it likely will result in "stagflation."

- The Federal Reserve balance sheet is simply too big; inflation should continue notwithstanding higher rates (which we believe will be 6%).

2023Q1 GDP by Major Segment (The Stuyvesant Square Consultancy (from BEA data))

New York (April 27) - GDP for 2023Q1 printed at 1.1%, just half of the consensus estimate, but well in line with our estimate in our March jobs report.

As you can see from our exclusive chart of GDP by major category, GDP growth was led by PCE , Personal Consumption Expenditures, but offset by a serious decline of over 2% in GDI , Gross Domestic Investment. GCE , Government Consumption Expenditures, added another 81 bps to GDP. NEX, or Net Exports, increased a miniscule 11 bps.

The PCE price index, a measure of inflation, increased 4.2 percent, compared with an increase of 3.7 percent. Excluding food and energy prices, which is the Federal Reserve's preferred measure of inflation, the PCE price index increased 4.9 percent, compared with an increase of 4.4 percent.

Prognostication

Based on the current data, we believe the second quarter, 2023 Q2, GDP will print at or around 0.5%, leading the way into a mild to moderate recession starting in 2023 Q3.

We also believe, and have said repeatedly , going back to November, that the Fed's terminal rate will be at or near 6%.

But the continuing tide of inflation is likely to set up the miserable state we described with the portmanteau "stagflation," or "stagnation" and "inflation," simultaneously.

The principal problem of inflation is the same as it has been since it was being dismissed as "transitory" by Fed and Treasury officials: there is too much money in the economy.

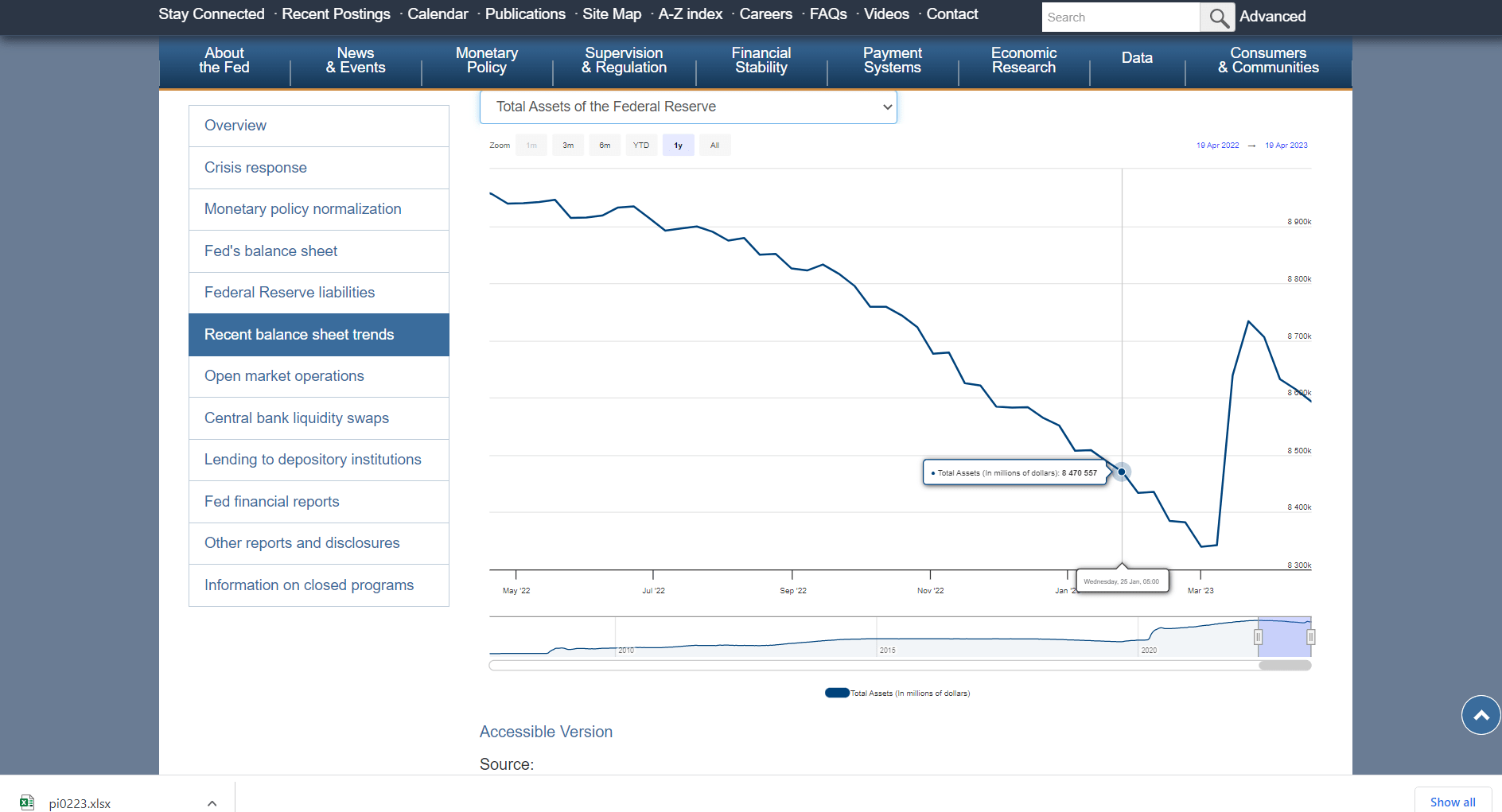

Federal Reserve Balance Sheet (SOURCE: Federal Reserve)

{kind=link}

While the Fed had been gradually "burning off" assets it acquired during the pandemic (far too slowly, in our view), it was forced to drastically reverse course because of the Silicon Valley Bank regional bank crisis, as illustrated above. We're back to where we were in November, when PCE inflation (ex-food and energy) was 4.8%. (New data is set for release tomorrow.)

Grey Swans

Debt Ceiling

We predict government will suffer a "shutdown" of non-essential services that will be more in the nature of an annoyance than actual pain. National parks and monuments may be shut down at the height of the summer school vacations, but Social Security checks and Food Stamps will still go out.

The U.S. should not default on its debt because there is sufficient cash rolling in to cover debt service, but the politics requires that canard to be proffered in the debate. What likely will happen is that the debt ceiling will be raised, but spending will increase above the 1% limit Speaker McCarthy has set; probably in the range of 2.5% to 3.5%.

But the spending-increase GOP will have a galvanizing issue for its base for the 2024 elections to increase its majority in the House and win control of the Senate.

Regional Conflicts

The Ukraine War will continue in stalemate so long as the United States funds President Zelenksy's plans. Risks of it getting worse are inevitable.

Taiwan elections scheduled for January should be observed very closely by American media. China will be pouring lots of resources into support for the Kuomintang , the opposition party that supports ties with China, so a great deal is at risk. In the meantime, China will continue to threaten and prod, just as Russia did with its "exercises" that we warned about almost two years ago to the day.

Investment Thesis

This is a very unsettling time. While we don't expect the regional banking troubles to spread, we do expect recession. Older and retired investors might wish to keep their savings "safe" with maybe 70% of their portfolio in two-year Treasuries (US2Y), to be held to maturity, with the balance in Gold and the Blue Chip equities and bonds of consumer brands, including those in developing markets. Younger investors should stick to the S&P index (SP500), in equities, but up their investments in two-year Treasuries to as much as 50% with a view to holding them to maturity. Once the post-recession economy settles out after the two years, investors can decide whether to roll over the Treasuries or step back into the equities markets with their cash.

___________________________

Note: Our commentaries most often tend to be event-driven. They are mostly written from a public policy, economic, or political/geopolitical perspective. Some are written from a management consulting perspective for companies that we believe to be under-performing and include strategies that we would recommend were the companies our clients. Others discuss new management strategies we believe will fail. This approach lends special value to contrarian investors to uncover potential opportunities in companies that are otherwise in a downturn. (Opinions here with respect to whether to buy, sell, or hold such companies, however, assume the company will not change its current practices).

For further details see:

2023 Q1 GDP Sets Up 2nd Half Recession And 'Stagflation'