QQQ - 2024: Where Hopes For A 'Soft Landing' Go To Die

2023-12-04 11:30:49 ET

Summary

- Equities had one of their best months in years during November, as interest rates dropped dramatically during the month while inflation fears ebbed.

- Will a much-anticipated "soft landing" occur in 2024 powering stocks higher, or are falling rates just one of many signs that a recession is right around the corner?

- That is the $64,000 question for investors as we head into a new year.

- Unfortunately, for the key reasons highlighted in this article, a recession and a corresponding bear market in equities likely lies ahead in 2024.

- Are investors being too complacent, or is my pessimistic economic view heading into 2024 off base? A discussion follows below.

I predict future happiness for Americans, if they can prevent the government from wasting the labors of the people under the pretense of taking care of them ."? Thomas Jefferson.

December started on a high note Friday, with the Dow (DJI) gaining nearly 300 points and the S&P 500 (SP500) rising .6% on the day. What were perceived as "dovish" comments from Fed Chairman Powell, and the growing belief that the Federal Reserve will start to cut rates as soon as March of next year, ignited a broad-based rise in most assets, with gold hitting an-all time high, and Bitcoin (BTC-USD) rallying. The dollar continued to slide, and the yield on the two-year Treasury (US2Y) fell 12bps to 4.56% while the 10-Year Treasury (US10Y) fell in a similar fashion to end the week at 4.2%.

S&P Weekly Performance By Sector (Seeking Alpha)

For the week, Real Estate was the best performing of the 11 sectors in the S&P, nine of which were up. Materials, Financials and Industrials all gained over two percent on the week, while Energy and Communication Services were the only sectors in the red.

Trading Friday followed a huge rebound in the markets in November. Both the Dow and S&P 500 gained nearly nine percent on the month, their best monthly performance since July of 2022. The NASDAQ (COMP.IND) rose nearly 11% on the month.

The main trigger for the big rally in equities was the collapse in yields and interest rates during the month, which followed a series of better-than-expected readings on inflation. After touching five percent for the first time since July of 2007 at the end of October, the yield on the 10-Year Treasury has fallen dramatically over the past five weeks. This has touched off a huge rally across most markets.

10-Year Treasury Yield (Market Watch)

The $64,000 question for investors is if the big decline in rates due to falling inflation and the Fed achieving a " soft landing" or because the economy is slipping into a recession? If the former scenario plays outs, equities could well have further upside from here. If the latter occurs, equities probably will see a " bear market" in 2024 as happens during most recessions. Unfortunately, my view is that a recession is more than a 50/50 probability and my portfolio is positioned accordingly.

There are many reasons for this belief. Here are three key tenets forming this view.

Economic Growth Is Slowing

It is hard to believe the U.S. could be on the cusp of a recession when the country experienced 5.2% GDP growth in the third quarter. However, a good portion of growth in 2023 has come from deficit spending via the Federal Government. In its recently closed fiscal year, the federal government's deficit was nearly eight percent of GDP. Given federal government spending totals almost one quarter of the nation's GDP these days, one could make the argument that most of the just over two percent growth (2.4%) projected for 2023 has been the direct results of this largess. Unfortunately, that level of deficit spending is unsustainable, with the national debt to GDP ratio already at its highest levels since WWII.

Capital Economics, Congressional Budget Office

Economies can also turn quickly. The last time GDP growth clocked in at five percent or better was in the fourth quarter of 2021. This was followed by two quarters of economic contraction in the first half of 2022.

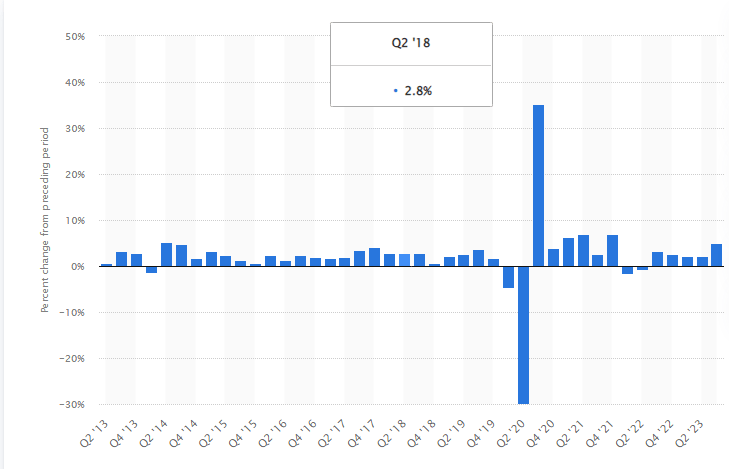

U.S. GDP Growth By Quarter (Statista)

{kind=link}

The Atlanta Fed's GDPNow has already quickly ratcheted down their forecast of Q4 GDP growth, as can be seen below. The Conference Board's latest projection for U.S. GDP growth in 2024 is just .8%. The Organization for Economic Cooperation and Development recently lowered their forecast for both global and U.S. growth in 2024. They project 2.4% growth in the United States for 2023, which they now see slowing to just 1.5% in 2024.

Atlanta Fed's GDPNow

Default And Delinquency Rates Are Rising Rapidly

The health of the American consumer is deteriorating. Full-time jobs have declined over the past few months. Headline number have been kept positive by a surge in part-time positions, as a record 8.4 million Americans are now working at least two jobs to make ends meet. Nearly two thirds of the nation believes the U.S. is on the wrong track , according to recent polls.

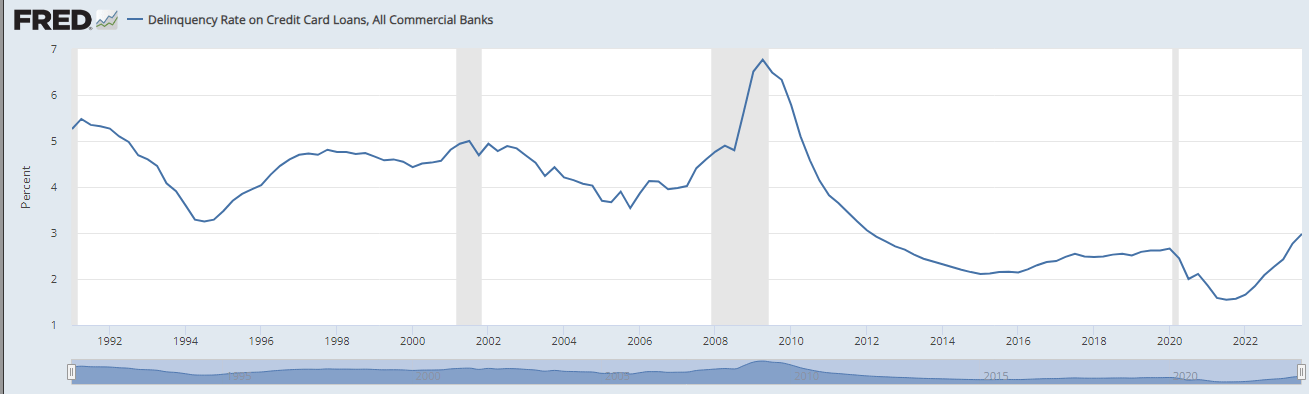

U.S. Credit Card Delinquency Rates (St. Louis Federal Reserve)

{kind=link}

Credit card delinquency rates are at the highest levels in more than a decade and continue to rise even as Americans now have a record $1.08 trillion in credit card revolving balances. Auto loan defaults also just hit a 29-year high even as student loan payments for nearly 40 million Americans just restarted in October, after more than three-year taxpayer funded hiatus.

Trepp, Morgan Stanley Research

However, it is the rising delinquency rates in the commercial real estate sector that should give investors the most pause, given some $540 billion in CRE debt needs to be refinanced at much higher rates in 2024. This could have grave consequences for the regional banking system as well as overall credit availability, given regional banks originate some 70% of CRE loans and hold 30% of CRE debt.

In what is becoming almost a weekly occurrence now, another major property owner went belly up last week. This time it was a European entity called Signa, which is the co-owner of New York's famed Chrysler building. The company had assets of upwards of $25 billion as of the end of 2022. It filed for insolvency in Vienna on Wednesday.

Trepp

As can be seen from the chart above, delinquency rates across all categories of CRE have risen. In November, the delinquency rate for office real estate debt pushed through the six percent level, up from just 1.7% just 12 months ago. Delinquency rates for hotel debt also cross over the five percent threshold for the first time this cycle as well.

Too Many Potential Economic Failure Points

The flagging consumer should be enough to put the economy into a recession at some point in 2024, given they drive nearly 70% of economic activity. If the consumer manages to keep spending at current rates, the unfolding CRE debacle could tip the economy into contraction, given what soaring delinquency rates and defaults will do to the regional banking system.

Then we have the stagnant housing market, where existing home sales look like they will hit their lowest levels since 1992. Manufacturing is also in a funk as well. Friday, the November ISM Manufacturing PMI came in unchanged at 46.7, falling short of the 47.6 consensus. It was the 13th straight month that this index was in contractionary territory.

{kind=link}

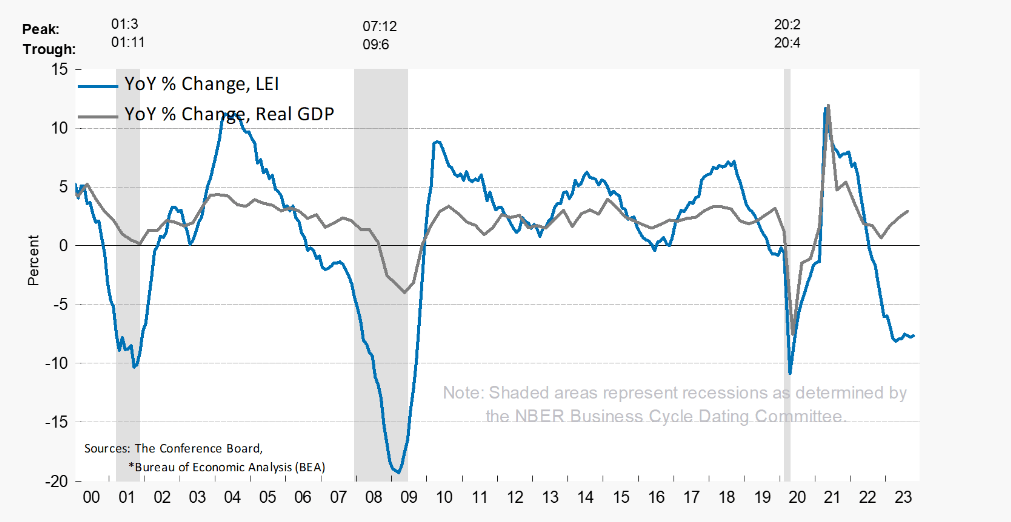

All these negatives are key reasons the Leading Economic Indicators have fallen for 19 straight months now. This is their longest losing streak since their 22 months of decline into the Bear Stearns bankruptcy in the first half of 2008.

Portfolio Allocation

Given this pessimistic view on the economy and equities, my portfolio is positioned very conservatively. Roughly half my funds are in short term treasuries. In November, as my three-month T-bills cashed out, I moved these proceeds into six and 12-month treasuries as the window for getting five percent yields on these instruments seems to be fast closing as the yield curve starts to become less inverted.

Most of the rest of my portfolio is in covered call holdings around stocks with solid balance sheets and reasonable valuations, like Exelixis ( EXEL ). This provides some downside protection and good return potential even in a sideways market. Approximately three percent of my portfolio is in long-dated, significantly out of the money bear put spread positions against the SPDR® S&P 500 ETF Trust ( SPY ) and the Invesco QQQ Trust ETF ( QQQ ). The last of these were executed on Friday. They will provide massive profits, if, and only if, the market has a 20% decline from current trading levels.

{kind=link}

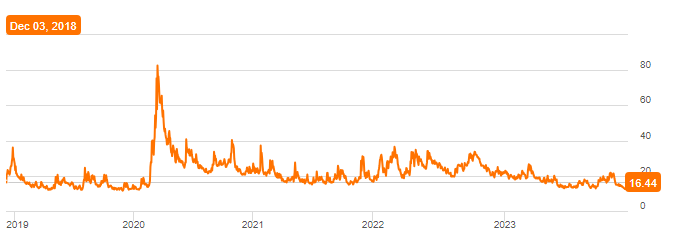

The S&P VIX Index ( VIX ) is signaling complete complacency by investors and at/near its lowest level of the past half-decade. These bear put spreads are simply good and cheap portfolio insurance should a recession and bear market occur in 2024, both scenarios I continue to believe are more likely than not in the year ahead.

Sometimes I wonder whether the world is being run by smart people who are putting us on or by imbeciles who really mean it ."? Laurence J. Peter, The Peter Principle.

For further details see:

2024: Where Hopes For A 'Soft Landing' Go To Die