MEUSW - 23andMe Holding: At Risk Of Becoming Irrelevant

2023-03-29 13:26:31 ET

Summary

- 23andMe is known around the world for its ancestry DNA genetic testing service.

- The company's pivot into therapeutics seems attractive.

- But the company saw revenue decrease from $441 million in 2019 to $272 in 2022.

- What's the value of having loads of DNA data without the people's medical records and other relevant data points?

- Genotyping also seems inferior to whole genomic sequencing, particularly in rare disease detection.

Introduction

23andMe Holding ( ME ) is a company that became very famous in 2006 when it launched its ancestry DNA genetic testing service. The service entails that after the customer provides a saliva sample, 23andMe uses genotyping to analyze the DNA and provide interesting insights.

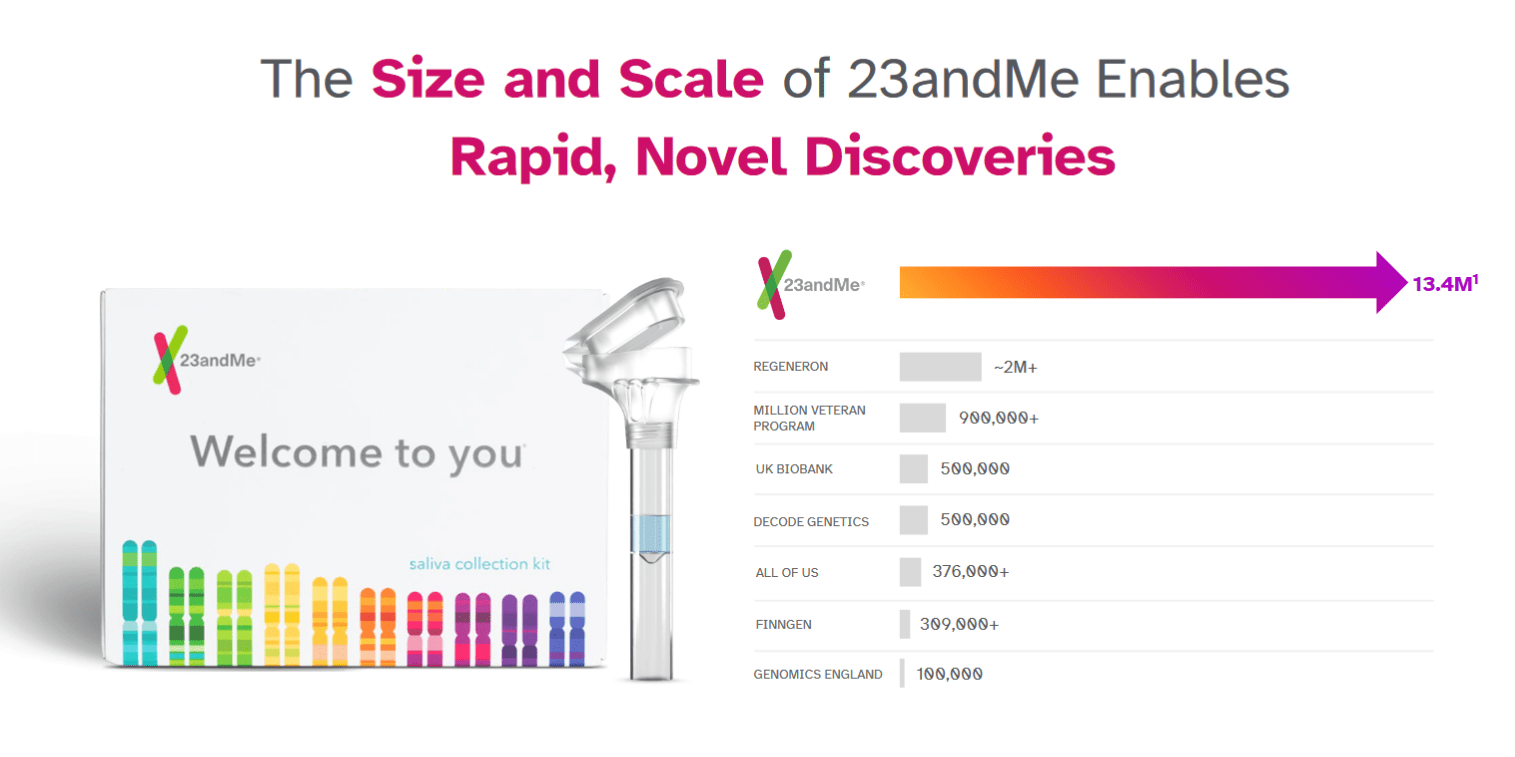

The company's goal is "Revolutionizing the Diagnosis, Prevention and Treatment of Human Disease"; with a database of 13.4 million individuals who undertook genotype tests, 23andMe is the biggest in the genome space.

In 2021 the company reverse-merged with SPAC to become publicly listed; in this article, I will analyze the company and elaborate on why I do not see 23andMe as a very attractive stock.

Scale

{kind=link}

23andMe is not the only player in the genome space. What 23andMe does is map out a small part of the genome and say something about ancestry and health.

While 23andMe has the biggest genome dataset in the world, I am questioning whether having this scale is really that beneficial.

You see 23andMe has been around for a long time, yet consumer services still makes up 80% of the revenue, and research services just 20%. The share of research services is increasing, which is a positive narrative in the company.

The company has seen revenue decrease from $441 million in 2019 to $272 in 2022 - which also includes the major Lemonaid acquisition, which obviously grows revenues.

These figures do not show the traction I would expect from a business in genomics.

Problem #1

What's the point of having loads of DNA data if you don't have the people's medical records and other relevant data points?

I think that the genome alone is not enough. You want to collect a lot of data besides the genome: companies like GeneDx ( WGS ) and Tempus are going further on the analytics mountain. By having lots of clinical data with disease progression and biomarkers from blood tests: you start to map the effects of the genome on health, disease, and other things much more effectively.

{kind=link}

This is a flaw in their business model, and the recent telehealth acquisition is set to expand the company's offering. The company wants to provide telehealth, lab tests, and other services to drive long-term engagement. It acquired the telehealth company Lemonaid in November 2021. The goal is to build a telehealth platform around genetic data - using genetic data to provide better telehealth services.

I don't view these strategic decisions as coincidental but as well-intended decisions to strengthen the customer proposition.

{kind=link}

In an interview with Dave Lee, ARK Analyst Brett Winton answered why Teladoc ( TDOC ) is attractive as an investment in the genome revolution:

"If you are in the front-end of the patient tunnel then you can begin to deliver people a patient experience -- from that exposure to those patients and begin to improve that experience." ~Brett Winton

It is this front end that 23andMe is missing. People use the service one time to check up on their genome for ancestry insights and health recommendations. And that's it.

Problem #2

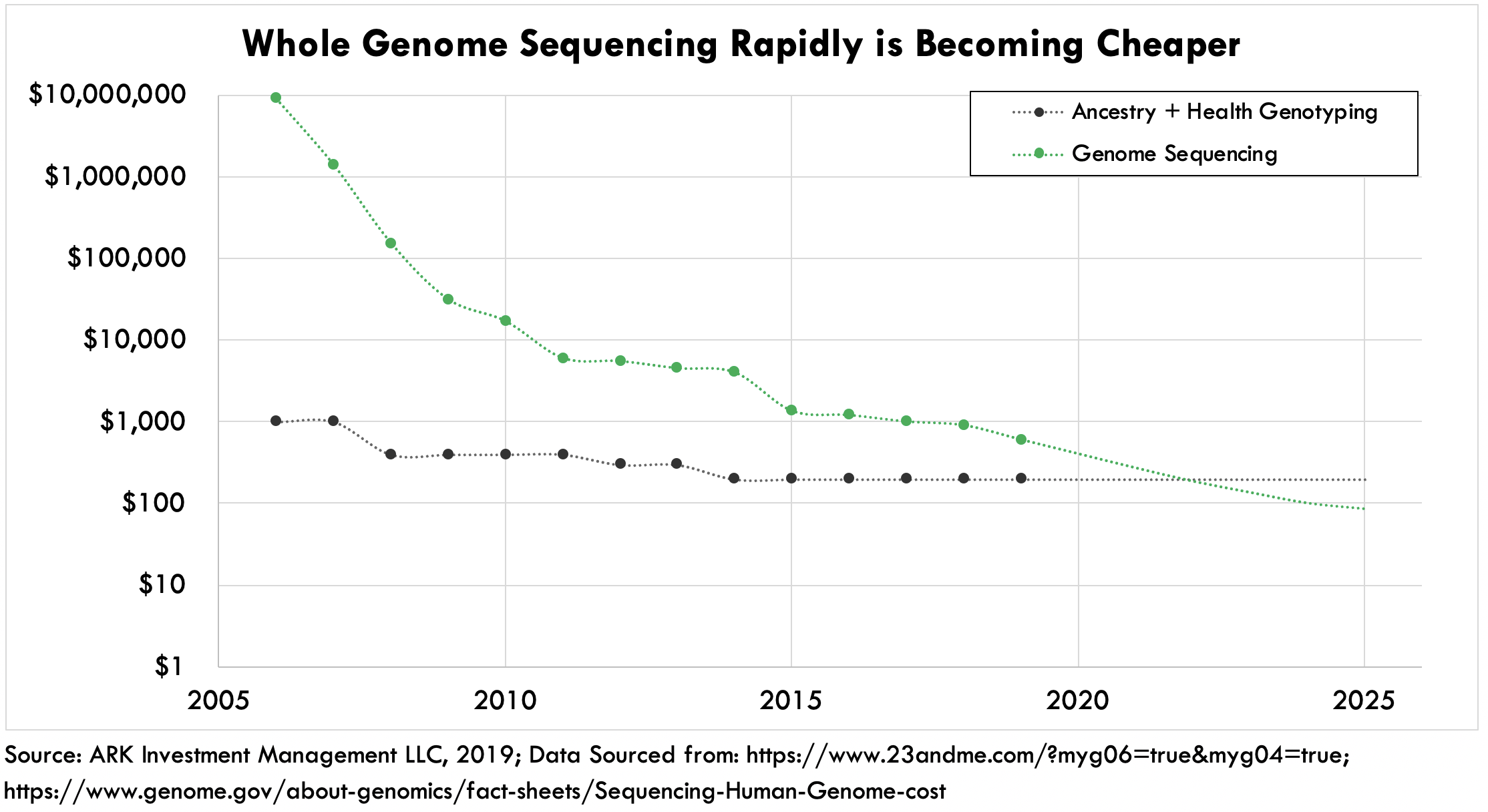

As whole genome and whole exome sequencing become cheaper, ancestry/health genotyping is set to become more and more irrelevant. ARK Invest published an interesting paper with some very noteworthy facts.

First, you can see that whole genome sequencing is getting closer to the price of genotyping.

{kind=link}

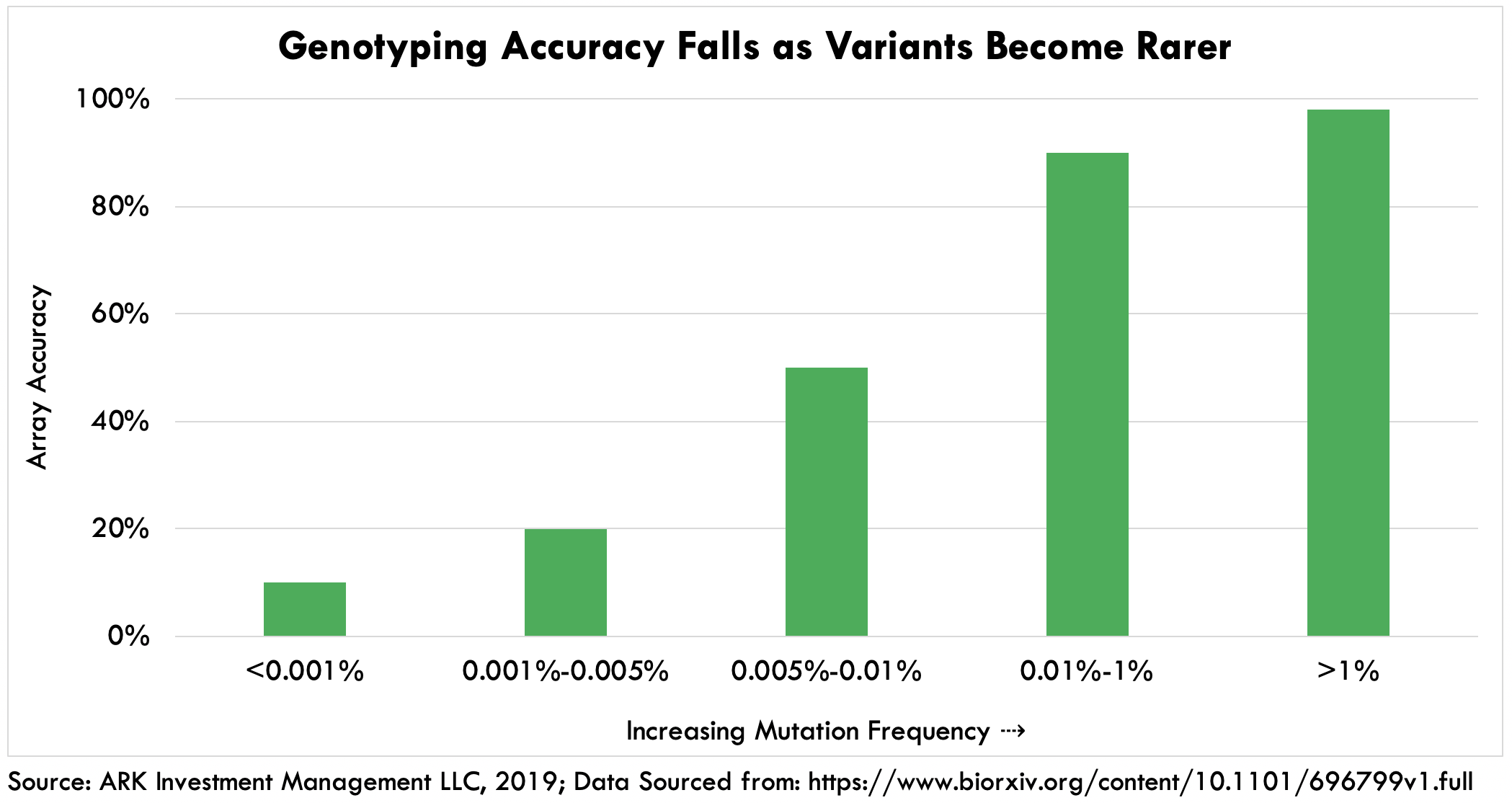

Second, genotyping struggles with accurately detecting rare diseases - and you say, who cares? But research has shown that medically important diseases tend to be exactly those rare diseases. It seems that genotyping is just simply inferior to whole exome and genomic sequencing.

{kind=link}

Very fundamentally, the data shows something intuitively very logical. By sequencing only a tiny portion of the genome, you will lose significant information, which will drive down the accuracies of many tests. Recently , research has shown that the junk/noncoding DNA - DNA that was told to have no purpose - does have a purpose, particularly in gene activity. I note genotyping only covers a fraction of the coding DNA and does not cover the noncoding DNA. Whole exome sequencing covers all the coding DNA while whole genome sequencing covers all the DNA.

Companies focusing on the whole exome and genome are significantly better positioned to become big in the genome revolution.

In my view, 23andMe is fundamentally flawed. While it has scale - it does not benefit from any significant scale benefits.

You see, the scale alone doesn't get you anywhere. You have to turn scale into sustainable competitive advantages - something many ex-SPAC companies in the stock market struggle with.

A Positive

The company's pivot into biotech/therapeutics by developing molecules that seem very attractive from its vast genome database can be very lucrative.

While this is not my core expertise, I view this part of the business as one that can potentially justify the higher stock valuation. Of course, the returns of biotech investment are skewed and require years to occur; it is an all-or-nothing story.

As the company succeeds, I can imagine more and more biotechs wanting to partner with 23andMe to develop very valuable molecules.

Valuation

The company sells at 2.23 EV/Revenues with a market cap of around $1 billion and an enterprise value of $675 million. According to analyst estimates, Quest Diagnostics ( DGX ) and Hims & Hers Health ( HIMS ) sell at similar forward revenue multiples. Still, those companies are set to be EBITDA and net income profitable in the next twelve months, according to consensus analyst estimates.

Quest Diagnostics is very profitable, generating significant cash flows the company can reallocate. At the same time, Hims & Hers Health is just turning profitable but has grown and is set to grow in the high multi-digits in the coming years. So I view these companies as excellent, which is why they acquire high valuations.

I find that a very hefty valuation for 23andMe which has seen: little growth over the past years, a lot of headwinds facing it, and whose operating income was -$314 million in the last trailing twelve months.

Takeaway

23andMe has entered telehealth to reach the front in the patient funnel. 23andMe is big in genotyping, while whole genome sequencing seems better positioned. This does not bode well for 23andMe. 23andMe's valuation is quite expensive for a company with such tiny growth: I conclude with a sell rating, as I think there are significantly more attractive companies on the market.

For further details see:

23andMe Holding: At Risk Of Becoming Irrelevant