JNJ - 2seventy bio: Nothing Properly Explains The Low Valuation

2023-06-21 16:58:52 ET

Summary

- 2seventy bio, Inc. was spun off from bluebird bio, Inc., and has one product in the market making decent revenue.

- They have a good cash position, a decent if early stage pipeline, and strong collaborations.

- Thus, their currently low market cap does not make sense.

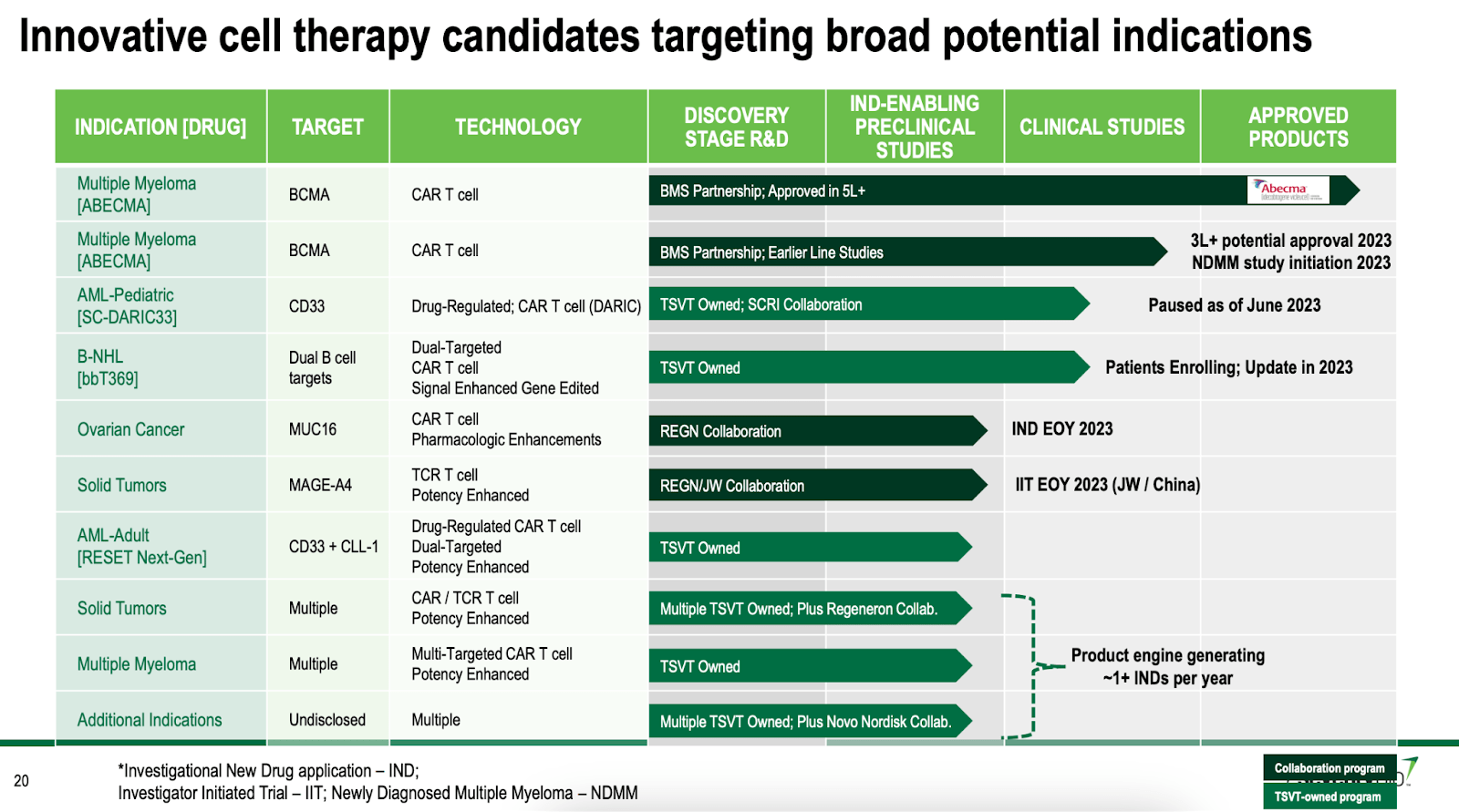

2seventy bio, Inc. ( TSVT ), spun off from bluebird bio, Inc. ( BLUE ), is a developer of T-cell therapies targeting cancer. It has one approved product called ABECMA® (idecabtagene vicleucel), the first approved CAR T therapy for multiple myeloma, which is generating considerable revenue, and its pipeline looks like this:

{kind=link}

ABECMA was approved in 2021. It is the first cell-based gene therapy for adults with multiple myeloma “who have not responded to, or whose disease has returned after, at least four prior lines (different types) of therapy.” According to the National Cancer Institute , there are approximately 32000 new myeloma patients in the U.S. (2020 figures, incidence rate). As the FDA describes it, “Abecma is a B-cell maturation antigen ((BCMA))-directed genetically modified autologous chimeric antigen receptor ((CAR)) T-cell therapy.” The treatment is autologous, using the patient’s own T-cells.

Efficacy and safety data of ABCEMA, as described by the FDA, is as follows:

The safety and efficacy of Abecma were established in a multicenter study of 127 patients with relapsed myeloma (myeloma that returns after completion of treatment) and refractory myeloma (myeloma that does not respond to treatment), who received at least three prior antimyeloma lines of therapy. About 88% of patients in the study group had received four or more prior lines of antimyeloma therapy. Overall, 72% of patients partially or completely responded to the treatment. Of those studied, 28% of patients showed complete response—or disappearance of all signs of multiple myeloma—to Abecma, and 65% of this group remained in complete response to the treatment for at least 12 months.

Treatment with Abecma has the potential to cause severe side effects. The label carries a boxed warning for, cytokine release syndrome ((CRS)), hemophagocytic lymphohistiocytosis/macrophage activation syndrome (HLH/MAS), neurologic toxicity, and prolonged cytopenia, all of which can be fatal or life-threatening. CRS and HLH/MAS are systemic responses to the activation and proliferation of CAR-T cells causing high fever and flu-like symptoms, and prolonged cytopenia is a drop in the number of a certain blood cell type for an extended period of time. The most common side effects of Abecma include CRS, infections, fatigue, musculoskeletal pain, and a weakened immune system. Side effects from treatment usually appear within the first one to two weeks after treatment, but some side effects may occur later. Patients with multiple myeloma should consult with their health care professionals to determine whether Abecma is an appropriate treatment for them.

Because of the risk of CRS and neurologic toxicities, Abecma is being approved with a risk evaluation and mitigation strategy which includes elements to assure safe use. The FDA is requiring that hospitals and their associated clinics that dispense Abecma be specially certified and staff involved in the prescribing, dispensing or administering of Abecma are trained to recognize and manage CRS and nervous system toxicities and other side effects of Abecma. Also, patients must be informed of the potential serious side effects and of the importance of promptly returning to the treatment site if side effects develop after receiving Abecma.

TSVT developed ABECMA in partnership with Celgene Corporation, presently a Bristol-Myers Squibb Company (BMY) unit. They have 50/50 U.S. rights in the partnership. In 2020, the product made $297mn top line revenue, and this year, it is expected to make $470-570mn in revenue. According to their presentation , the product has a peak U.S. revenue estimate of $2-3bn.

Currently, ABECMA is being studied for earlier lines of MM patients, including NDMM or newly diagnosed MM patients. In 2023, they plan to get U.S. approval for 3rd line disease. The KarMMa-3 trial which supports an NDA in this indication met its primary endpoint. This year, the plan is to initiate the KarMMa-9 study for NDMM patients.

In the KarMMa-3 trial, the following data was seen:

A total of 386 patients underwent randomization: 254 to ide-cel and 132 to a standard regimen. A total of 66% of the patients had triple-class–refractory disease, and 95% had daratumumab-refractory disease. At a median follow-up of 18.6 months, the median progression-free survival was 13.3 months in the ide-cel group, as compared with 4.4 months in the standard-regimen group (hazard ratio for disease progression or death, 0.49; 95% confidence interval, 0.38 to 0.65; P<0.001). A response occurred in 71% of the patients in the ide-cel group and in 42% of those in the standard-regimen group (P<0.001); a complete response occurred in 39% and 5%, respectively. Data on overall survival were immature. Adverse events of grade 3 or 4 occurred in 93% of the patients in the ide-cel group and in 75% of those in the standard-regimen group. Among the 225 patients who received ide-cel, cytokine release syndrome occurred in 88%, with 5% having an event of grade 3 or higher, and investigator-identified neurotoxic effects occurred in 15%, with 3% having an event of grade 3 or higher.

This data can be summarized below for easier reading:

Efficacy

| Parameter |

| Ide-cel Group |

| Standard-Regimen Group |

| mPFS (months) |

| 13.3 |

| 4.4 |

| Hazard ratio |

| 0.49 |

| - |

| Response rate (%) |

| 71 |

| 42 |

| Complete response (%) |

| 39 |

| 5 |

Safety

| Adverse Events |

| Ide-cel Group |

| Standard-Regimen Group |

| Grade 3 or 4 adverse events |

| 93 |

| 75 |

| Cytokine release syndrome (Grade 3 or higher) |

| 5 |

| - |

| Investigator-identified neurotoxic effects (Grade 3 or higher) |

| 3 |

| - |

KarMMa-3 is the first randomized phase 3 trial that directly compares a CAR T therapy with standard therapies in 3L RRMM. OS data was mature at the time of reporting, and was blinded. The company filed a BLA based on this data, and received a PDUFA date of December 16, 2023.

There are 4000 patients in the late line setting in which it is currently approved. There are 12,000 patients in the 3rd line setting where it is seeking approval next. There are another 5000 patients in the 2L setting. This is the scope for revenue improvement in the coming years for ABECMA. In 2 years since approval, and with just 4000 patients, it is projecting over half a billion dollars in U.S. revenues. If it gets approved for 3L in 2024, then by 2026, one could reasonably expect ABECMA to bring in an extra $1.5bn in U.S. revenues. Of course, the math is not so straightforward, but these are very good tidings for ABECMA.

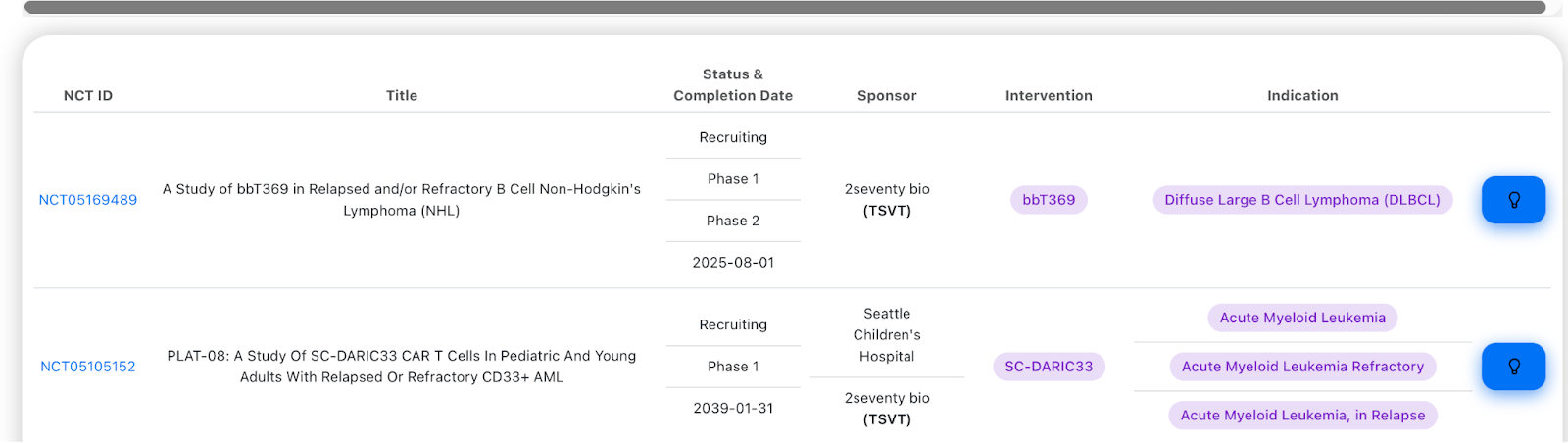

The rest of TSVT’s pipeline is really very early stage. It consists of two clinical assets, a CD33 targeting subcutaneously administered molecule called DARIC33 for AML-Pediatric, whose trial is currently paused; and a dual B Cell targeting molecule called bbT369 which is enrolling patients in an NHL trial.

Last month, the company posted phase 1 data from the DARIC33 trial. Data from two patients provided were as follows:

Preclinical studies predicted that DARIC33 dimerization, activation and expansion would occur at rapamycin trough levels in the range of ~1.5-3 ng/ml, well below the trough levels associated with immune suppression. Such levels were not achieved in the initial patient; however, after adjusting rapamycin monitoring and dosing algorithm, these levels were attained in the next two patients. As anticipated, attainment of such levels was associated with DARIC33 dimerization, activation, engagement of antigen and elicitation of CD33 expressing leukemic cell cytotoxicity. Of the two patients who achieved target rapamycin trough levels, the first one had extramedullary leukemia, and in this patient, we were able to infiltrate, activate and expand DARIC33 cells within an extramedullary leukemic infiltrate in the skin, resulting in hemorrhagic necrosis of this infiltrate. In the second patient, we saw DARIC33 expansion in the peripheral blood, peaking nine days after DARIC33 infusion, where 6.1% of the total lymphocytes were DARIC33 cells. The expansion of DARIC33 was associated with a significant transient reduction in the CD33 leukemic burden in the blood. Taken together, we believe this indicates at this very low cell dose that we can dose rapamycin to target levels resulting in the activation and expansion of DARICC33 cells which can then traffic to, engage, and kill leukemia cells.

However, last week, the study was paused after one of these patients died. The cause of this “Grade 5 SAE” is under investigation.

The other asset, bbT369, is in a phase 1 trial. Here’s the data from our Tickerbay tool:

{kind=link}

They only have preclinical data for this asset.

Financials

TSVT has a market cap of $512mn and a cash balance of $341mn. Last quarter, ABECMA made $118mn in total US revenue, and TSVT made $41.6mn. A collaboration with Novo Nordisk triggered $15mn in milestone revenue after the partnered asset delivered proof of concept data in an in-vivo gene editing hemophilia A program. More on their revenues :

-

2seventy bio and BMY share equally in all profits and losses related to development, manufacturing, and commercialization of Abecma in the U.S. 2seventy reported collaborative arrangement revenue of $23.0 million for the three months ended March 31, 2023, and share of collaboration loss of $5.4 million for the three months ended March 31, 2022.

-

Abecma was cash-flow positive in the first quarter and the Company expects the Abecma collaboration to be cash flow positive throughout 2023 and to generate between $200 and $300 million of operating income for 2seventy bio during the 2024-2025 period, based on management’s current operating plans.

They also raised $117mn through equity financing.

Research and development expenses were $68.2 million for the three months ended March 31, 2023, while Selling, general and administrative expenses were $20.7 million. Given their incoming revenue from ABECMA, their upcoming approval, and their cash balance, TSVT has a very long cash runway.

The company has multiple collaborations with big pharma like BMY, Regeneron and Novo Nordisk. The company is heavily owned by institutions, and key holders are Kynam Capital, BlackRock and State Street. Insiders, however, are regularly selling stock , and almost never buying.

Bottom Line

There is much to like in 2seventy bio, Inc. They have a very good cash runway, strong incoming revenue, upcoming catalysts, major collabs, and they are have a low market cap - which would have been a good thing, except one wonders why the market is valuing them at less than or not much more than the sum of their cash balance and their expected revenue this year. One reason could be Johnson & Johnson's (JNJ) CARVYKTI, approved for 5th line MM last year, which will eat into ABECMA's market.

However, I do not think this is the only reason; neither did the patient death and trial pause pool down the stock so much. 2seventy bio, Inc. stock has been falling for a long time now. There is something else amiss, and I am not sure what it might be. But the low valuation is both a worry and an opportunity.

For further details see:

2seventy bio: Nothing Properly Explains The Low Valuation