ODFL - 3 Awesome Dividend Growth Stocks To Buy During A Bear Market

2023-03-14 06:00:00 ET

Summary

- Markets are in turmoil. Hence, in this article, we start with a discussion of the risks facing investors and why I believe in attractive buying opportunities this year.

- While I understand that investors often opt for higher-yielding investments, I will explain why investments in low-yielding dividend-growth stocks come with benefits.

- I present three of my favorite dividend growth picks that, I believe, make terrific investments during bear markets.

Introduction

As an investor, maintaining a well-diversified portfolio is crucial for minimizing risk and maximizing returns. With this in mind, I have created several model portfolios in addition to my personal dividend growth portfolio, which constitutes 90% of my net worth. In this article, I will share three of my top low-yield dividend growth stock picks that have consistently performed well in bull markets and are poised for long-term success.

While the current market environment may seem challenging, savvy investors can capitalize on the current downturn by strategically adding high-quality stocks to their portfolios. The three companies I will be discussing in this article offer exceptional value and are ideal for investors looking to buy on weakness. These stocks boast a track record of high and consistent dividend growth, low payout ratios, and strong competitive advantages. Furthermore, they have the potential to outperform the market over the long term.

So, let's get to it!

The Tricky Macro Environment

Why I believe in a volatile low-3,000 to mid-4,000 points longer-term trading range.

Last week, I wrote a lengthy piece covering my thoughts on the economy, the market, and (related) Federal Reserve.

To give you the condensed version of my article, I believe in a prolonged and volatile sideways trend because of headwinds that are hard to overcome. Right now, the Fed is fighting persistent inflation caused by energy inflation, which worked its way through the economy, high wage inflation, supply chain issues, high food prices, red-hot rent inflation, and other issues.

While some of these problems have faded, the economy is now dealing with elevated core inflation, which is a bad sign, as inflation is now almost everywhere.

Bloomberg

Even worse, prior to the issues facing SVB Financial Group ( SIVB ), inflation expectations were rising again.

Twitter (@passedpawn)

Meanwhile, economic growth is slowing, as the yield curve is now indicating a high certainty of a recession over the next 12 months.

The chart below shows the 10-year vs. 3-month yield curve (the Fed's favorite recession indicator), except that it goes back to 1968. The shaded areas display recessions. Historically speaking, we're now in territory that more or less guarantees a recession to occur within 12 months.

Credit Suisse

Yet, the Fed needs to be hawkish. It cannot give in and let inflation win. Even if the Fed were to do an emergency rate cut in a situation where the banking situation gets out of hand, it would have to quickly return to hiking again.

Why?

Because government interest rate payments are rising and are expected to remain high as roughly 40% of the government debt matures within 12 months . This translates to $8 trillion. One year ago, it cost $64 billion to finance this debt load. Currently, it's $400 billion. Imagine what that number could be a few months from now. The Fed needs to put an end to inflation in order for rates to remain low on a long-term basis. Everything else would be too dangerous for government finances.

Nasdaq

Moreover, investors have alternatives. Short-term government bonds are yielding more than 4.5%. Ongoing banking issues help to push money into safe investments.

While I am not a huge market bear - especially not a perma-bear - I expect that stocks have more downside. It looked like I was wrong earlier this year. Now, the downtrend is back.

Needless to say, my long-only portfolio is suffering a bit. However, I haven't lost a second of sleep. If there's anything that keeps me up at night, it's figuring out which stocks I want to buy!

That's why I wrote this article and so many others.

As soon as the stock market gets close to 3,500 points, I will be an aggressive buyer, putting some of that 10% (of my net worth) cash to work.

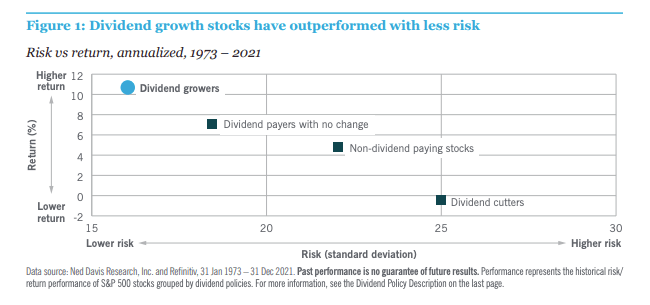

Why Dividend Growth Makes Sense

There are often tremendous benefits hidden behind a disappointingly low yield.

Whenever I discuss stocks with very low yields, at least a few people get upset, asking me how I dare to call these stocks dividend stocks.

Personally, I'm not bothered by it, as I understand people's frustration. Especially at a time of high inflation, investors feel like they need to get something back from their investments. Something tangible. And after all, that's why we all buy dividend stocks, right?

For example, a stock with a 0.40% dividend yield will give you $40 in annual pre-tax dividends for every $10,000 invested in the stock. $40 doesn't get you very far in today's economy.

However, that's not the main point when buying dividend growth stocks. There are some compelling reasons to include low-yielding dividend growth in one's portfolio.

Note that some of these reasons are interrelated.

-

Potential for (outperforming) capital appreciation : High-dividend growth stocks tend to have a strong track record of generating long-term capital appreciation. By investing in companies that are expected to grow their earnings and cash flows over time, investors may see their investments increase in value over time, in addition to receiving dividends. Moreover, these companies often come with lower volatility.

{kind=link}

Nuveen

-

Lower payout ratios : Low payout ratios suggest that companies have more room to reinvest earnings in their businesses or pay down debt, which can help support long-term growth prospects. This also protects investors against dividend cuts during recessions. However, on the flip side, yields are low, which means these stocks aren't part of a typical investors' income stream.

-

Diversification : Investing in low-yielding high-dividend growth stocks can provide diversification benefits to an investor's portfolio. High-yield stocks are often concentrated in certain mature industries like utilities, energy, finance, and industrials. There is nothing wrong with that, but in some cases, investors benefit from diversifying into faster-growth sectors - even if it means lowering the average portfolio yield.

-

Potential for dividend growth : Low payout ratios and high (potential) business growth could mean that the yield-on-cost after buying quickly rises.

-

Attractive valuations : In a bear market, valuations tend to be lower, which can create buying opportunities for investors. By purchasing low-yielding high-dividend growth stocks with low payout ratios at a discount, investors may be able to capture long-term growth potential and generate income at a relatively attractive price.

Needless to say, the last point is only valid when markets are weakening, which is why I am writing this article with the market being close to 20% below its all-time high.

So, with that said, let's get to the picks!

3 Of My Favorite Low-Yield Dividend Growth Stocks

Stocks that come with fast growth, high moats, and expected outperformance.

Let's start with a stock that I have covered just once in the past.

Zoetis Inc. ( ZTS ) - Veterinarian Healthcare Growth

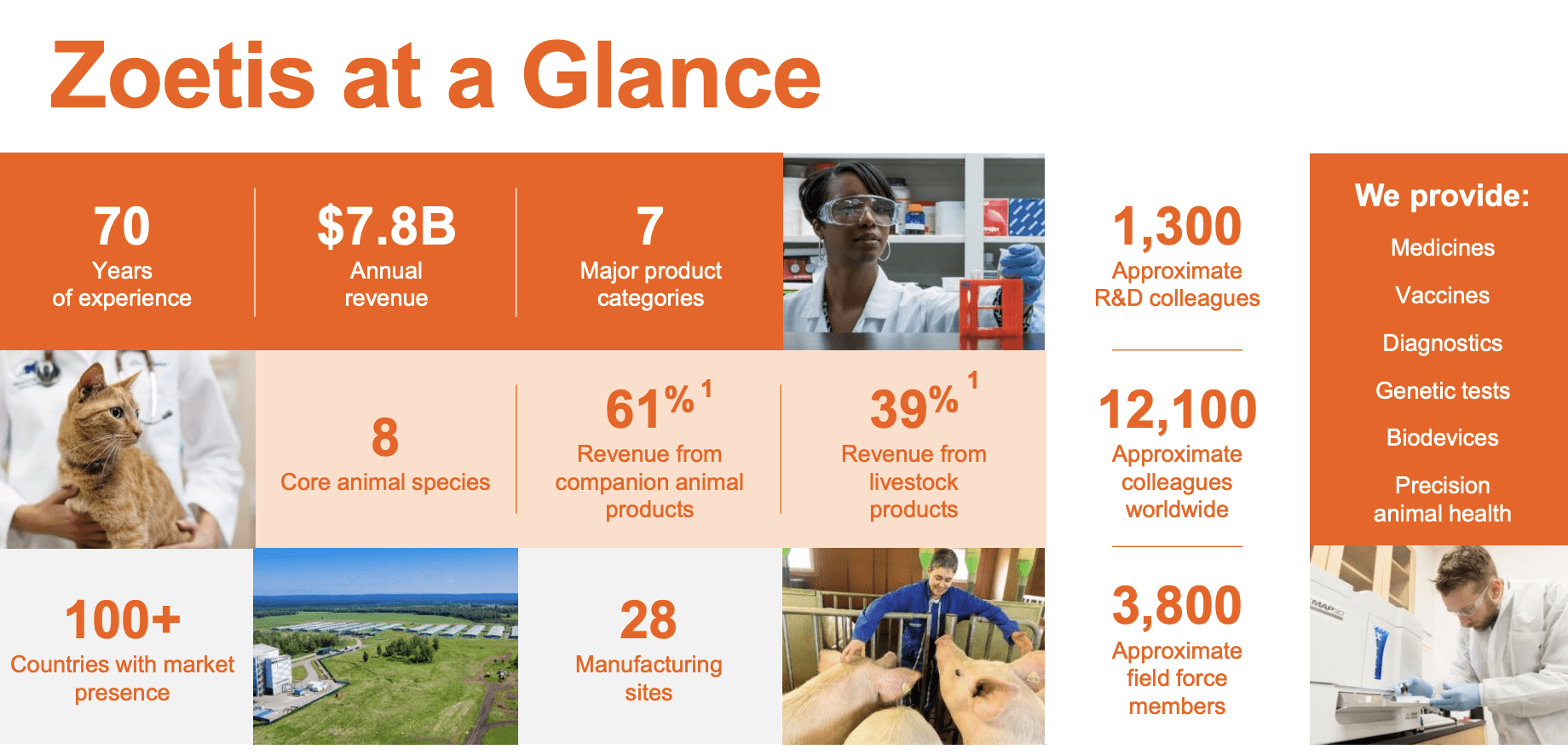

The first time I covered Zoetis was in January of this year. Zoetis is a Pfizer ( PFE ) spin-off that is the global leader in animal health, focusing on the discovery, development, manufacturing, and commercialization of medicines, vaccines, diagnostics, and related services.

The company generates roughly 40% of its sales from livestock, which is a fast-growing industry with a need for better healthcare (as proven by the ongoing bird flu). 60% of sales are generated in companion animal products, which target cats, dogs, and other animals.

{kind=link}

Zoetis Inc.

The company is the market leader in companion animals, cattle, fish, swine, North America, Latin America, Asia, and in niche markets like anti-infectives.

Roughly half of its sales are generated in the United States.

As I wrote in January:

[...], while livestock healthcare demand is somewhat cyclical due to consumer spending on proteins, the company does benefit from anti-cyclical spending on pets, which grew by almost 4% in the Great Financial Crisis of 2009, according to CEO Kristin Peck . So, overall, ZTS does have a very resilient business model.

It also benefits from these key trends:

- More people buy pets.

- People spend more time with pets.

- People are more willing to spend money on pet health.

- Innovation is driving market growth (new possibilities in health).

- Global protein production is rising (livestock demand).

- Protein production needs higher efficiency.

- Sustainable food production is key.

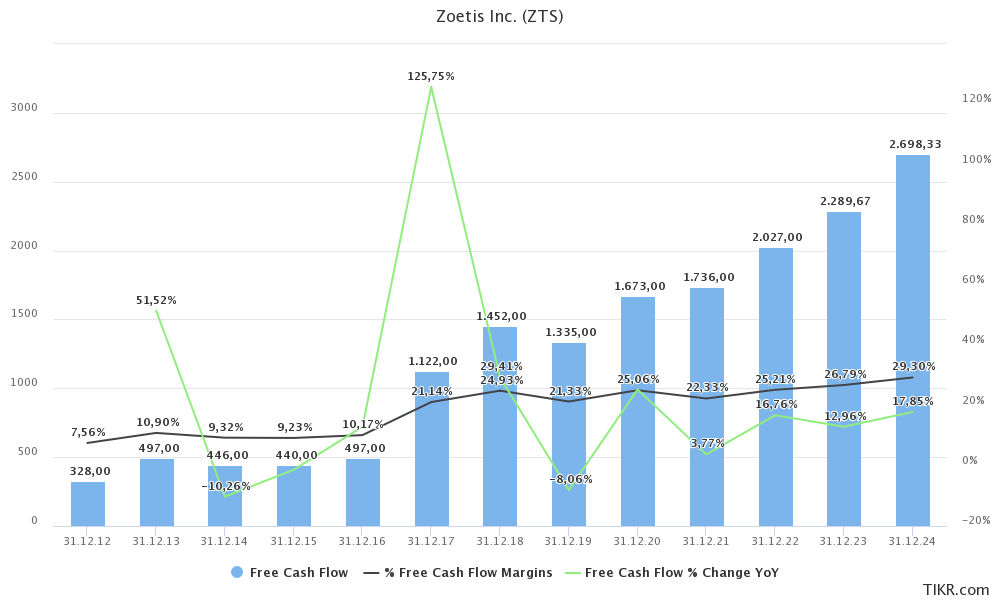

Moreover, the company is highly efficient and growing free cash flow by 19.2% per year in the 2012-2024E period. This outperforms EBITDA growth by 610 basis points. As the graph below shows, free cash flow has benefited from an FCF margin expansion from less than 8% to almost 30% in 2024E.

{kind=link}

TIKR.com

The company has a Baa1 credit rating and a net leverage ratio of less than 0.6x EBITDA. Hence, I have little doubt that the company will be A-rated in the not-too-distant future.

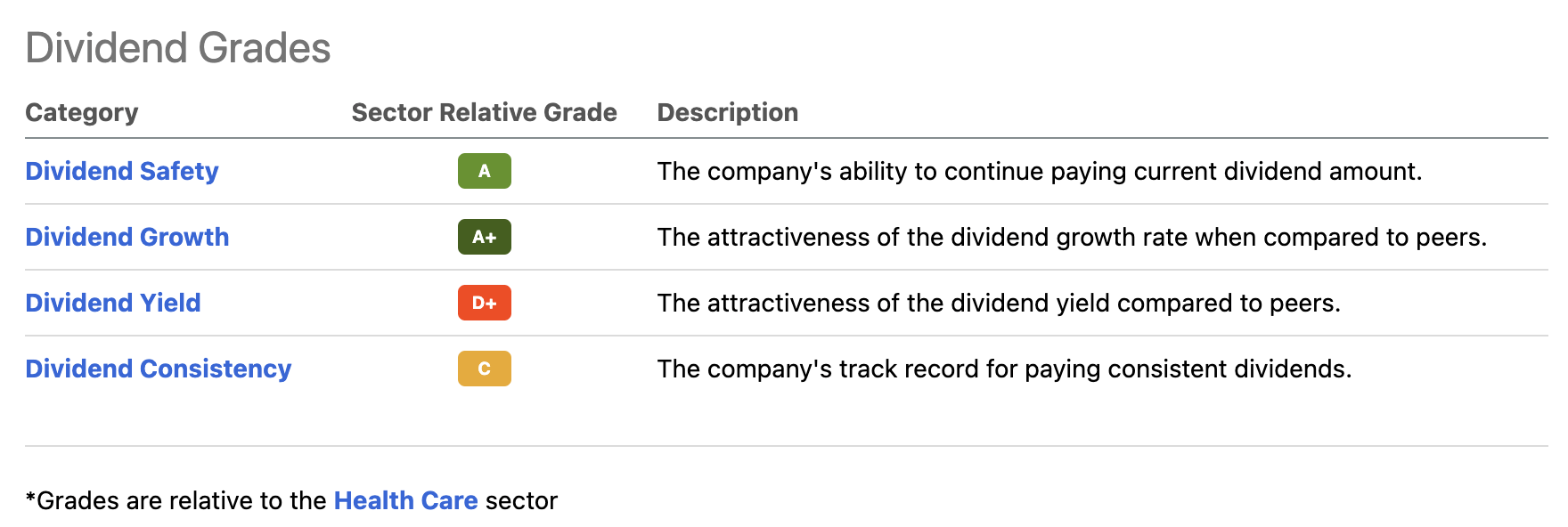

Looking at the company's dividend scorecard, we see an A+ for growth and a D+ for its yield.

{kind=link}

Seeking Alpha

The company started to pay a dividend in 2013. Over the past five years, dividend growth has averaged 25.1% per year. Over the past three years, that number is still 25.0%.

On December 8, 2022, ZTS announced a 15.4% hike.

Its payout ratio is 28%. The stock yields 0.9%.

Over the past five years, ZTS shares have returned close to 100%, beating the market by roughly 50 points.

The company is trading at 21x NTM EBITDA, which is well above the sector median of 13x NTM EBITDA.

Investors interested in healthcare dividend growth might enjoy putting ZTS on their watchlist. I think it's a great buy on bigger dips/corrections.

Danaher Corp. ( DHR ) - Healthcare Supply Growth

Danaher is one of the reasons why I'm glued to my screen.

I bought this company last year to expand my healthcare exposure, and to add some more dividend growth firepower to my portfolio.

Earlier this month, I wrote an article dedicated to the company's dividend growth capabilities and the perfect mix of outperforming returns and low volatility this company has provided for its investors in the past.

Danaher is a Washington D.C.-based healthcare supplier focused on diagnostics, biotechnology, and life sciences. It also has environmental and applied solutions, which will be spun off later this year.

{kind=link}

Danaher Inc.

The company benefits from a strong brand reputation, a diverse product portfolio, and high R&D spending, keeping it able to supply the most advanced healthcare supplier in the industry - with its peer Thermo Fisher ( TMO ).

Thanks to these benefits, the company has strong pricing power and a broad customer base consisting of anti-cyclical healthcare and related companies.

Danaher is not a buyback company. It spends most of its cash on M&A. In 2020, it bought General Electric's ( GE ) life sciences division in a massive $21.4 billion deal. Occasionally, the company spins off non-core assets. For example, in 2016, it spun off Fortive ( FTV ), which covered the company's industrial technology back then.

In 2019, it spun off Envista Holdings ( NVST ), a dental-focused healthcare supplier.

With that said, the company's dividend yield is just 0.5%. However, dividend growth over the past ten years has averaged 27% per year. Over the past five years, dividend growth has averaged 12.3% per year. The company has a payout ratio of just 10%.

Even more important, its business model has provided investors with steady outperformance.

As I wrote in the aforementioned article:

The good news is that Danaher continued to be a terrific source of wealth. When looking at the numbers below (January 1988 - February 2023), we see that DHR has returned 20.3% per year. This performance has remained consistent. Over the past ten years, the stock has returned 20.3% per year. Over the past three and five years, the return has remained close to 20%.

Portfolio Visualize

Moreover, the company has done this with subdued volatility. Over the past five years, the annualized standard deviation was 23.8%. That's slightly more than 500 basis points above the market's standard deviation. That might sound lit a lot. However, that's not the case. We're comparing a single company to a well-diversified basket of 500 stocks.

{kind=link}

Earlier this month, I added some shares using dividend proceeds from other investments. However, I am planning on buying somewhat aggressively if the market weakens further. While I am to maintain a somewhat decent average portfolio yield, I decided to make DHR a core holding of my portfolio.

The company is currently trading at 19.4x forward EBITDA. That's a fair valuation. However, given my view on the market, I think we get an even better entry.

FINVIZ

Number three is another stock I want to add very badly.

Old Dominion Freight Line ( ODFL ) - High Transportation Growth

I own three railroad stocks, as I am a big believer in buying investments that are critical to a nation's supply chain.

Initially, I decided to avoid trucking companies. Unlike railroads, trucking companies have smaller moats. Starting a trucking company isn't extremely hard. At least not compared to operating a railroad.

That said, operating a trucking company efficiently is hard. Once companies have figured out how to do that, they can grow exponentially, taking market share for smaller players.

That's what ODFL has done for decades.

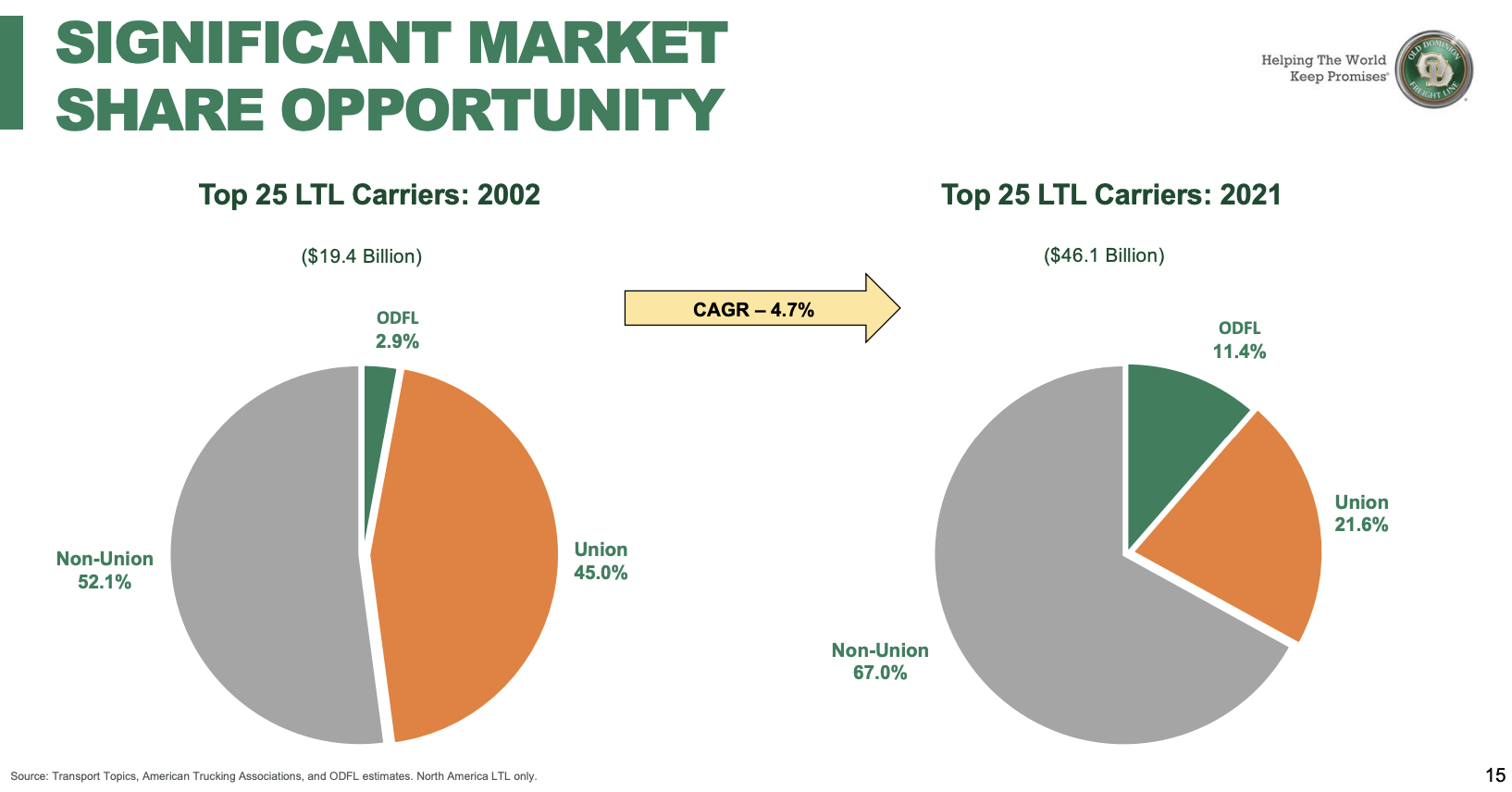

ODFL is an LTL transportation company. LTL means less-than-truckload, which covers the transportation of smaller loads, often from multiple customers at the same time.

In this industry, the company has expanded its market share from less than 3% in 2002 to more than 11% in 2021.

{kind=link}

Old Dominion Freight Lines

The best thing is that the company has done it with little M&A. It was almost entirely organic.

As I wrote in a recent article :

Between 2014 and 2025E, the annual compounding revenue growth rate is 9.3%. This excludes the strong post-Great Financial Crisis years. However, it includes the 2015 manufacturing recession and the 2020 pandemic.

Thanks to higher margins, EBITDA has grown by 14.0% per year during this period. Needless to say, few companies can compete with these growth rates.

Management has figured out how to be successful. Its wide network of distribution centers and high customer satisfaction come with strong pricing power. In 4Q22, the company saw a 9.1% contraction in tonnage per day. Revenue per shipment, however, increased by 8.1%. This excludes fuel surcharges.

Moreover, the company has an operating ratio of just 71.2%, which is absolutely phenomenal. Most Class I railroads have operating ratios close to 60%. None of ODFL's competitors comes anywhere close to that number.

This allows the company to use high growth to invest in its business and further improve its footprint in North America.

For example, $300 million of its 2022 CapEx was invested in real estate projects to further improve the company's service center network, which allowed the company to achieve a 99% on-time service rate and a cargo claims ratio of just 0.1%.

With that said, the company has a 0.5% dividend yield. However, its payout ratio is below 10% and the five-year average annual dividend growth rate is 35.3%. On February 1, the company hiked its dividend by 33.3%.

Thanks to these qualities, the company has returned close to 250% over the past five years, beating the market by 200 points.

Currently, the company is trading at 18x forward EBITDA. That valuation is fair. However, ODFL has the habit of selling off during recessions.

The stock is currently just 9% below its all-time high. While I am risking missing yet another upswing in the future, I'm waiting for another drop of at least 10% before I jump in.

With all of that said, here's my takeaway.

Takeaway

Markets are in turmoil again. Banking headlines are causing anxiety, and the Fed is somewhere between further hiking to fight inflation and pivoting to calm investors' nerves, which is a dangerous game in light of sticky inflation and ongoing economic growth slowing.

While it's hard to say where this market may be headed, I believe there's a high chance we get the opportunity to buy some high-quality dividend growth stocks at attractive prices.

Hence, in this article, I started by explaining why this situation is so tricky, and why I believe that we're in for a prolonged period of high volatility.

In the second part of this article, I explained why it makes sense to buy (some) companies with low yields and high dividend growth.

I presented three of my favorite low-yield high-growth picks. In the weeks ahead, we'll discuss more opportunities, as this is just a small part of my watchlist.

Other than that, I will be patiently monitoring the market, hunting for opportunities to add some of these beauties to my portfolio.

For further details see:

3 Awesome Dividend Growth Stocks To Buy During A Bear Market