VERV - 3 Biotech Bull Cases To Consider In 2024 - And 2 Wildcard Recommendations

2023-12-29 14:12:19 ET

Summary

- The biotech sector is finishing 2023 on a high after a difficult couple of years, buoyed by Big Pharma M&A activity.

- The SPDR® S&P Biotech ETF has been soaring as a result of the M&A spree.

- Despite a challenging year, there have been some winners in the biotech sector - I have been fortunate to share a few successful tips with Seeking Alpha readers.

- In this post, I discuss three companies I believe are potential strong performers in 2024: Madrigal Pharmaceuticals, Intra-Cellular Therapies, and Ionis Pharmaceuticals.

- I also briefly discuss 2 "wildcard" companies that risk-on investors should add to their watchlists - Iovance, and Verve Therapeutics - and explain the investment proposition.

Investment Overview

The biotech sector of the stock market is finishing 2023 on a high after what has been a difficult couple of years.

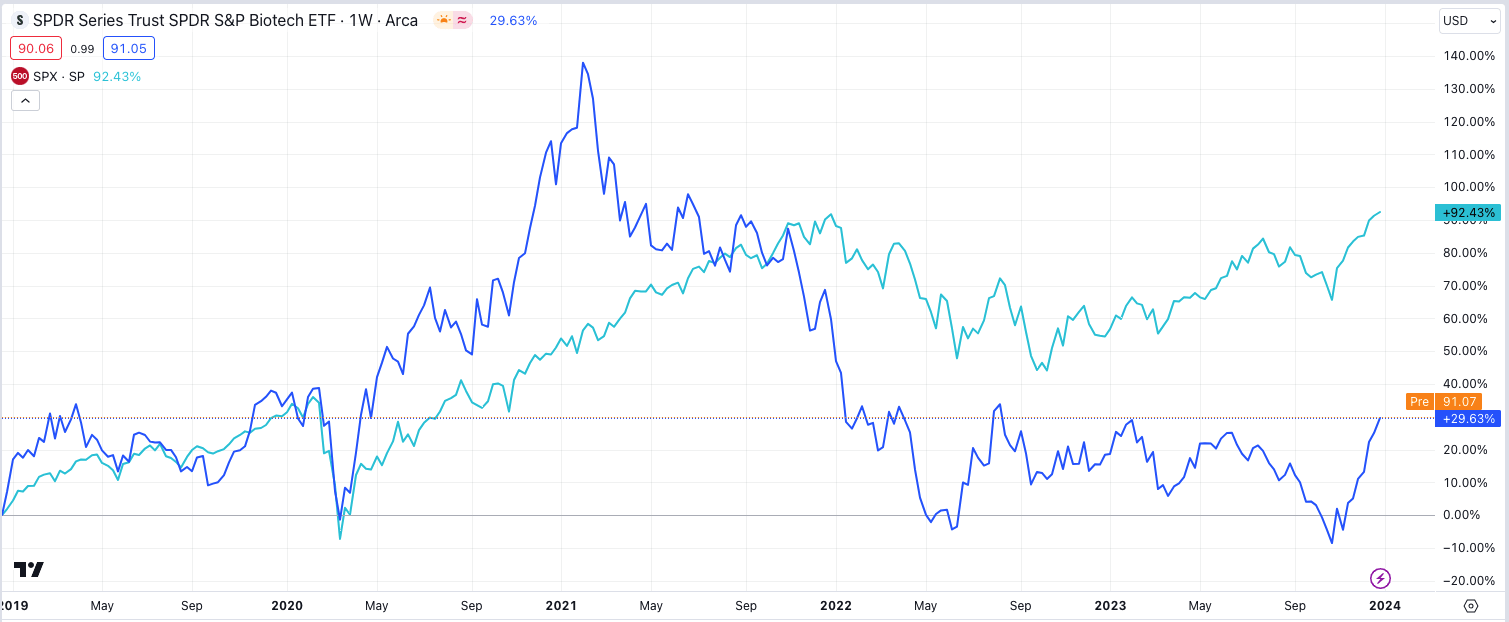

Buoyed by a Big Pharma M&A spree - the globally recognized Pharmas AbbVie ( ABBV ) and Bristol-Myers Squibb ( BMY ) have respectively spent a total of $18.8bn acquiring antibody drug conjugate ("ADC") specialist ImmunoGen ( IMGN ) and neuroscience pioneer Cerevel Therapeutics, and $18.1bn acquiring Karuna Therapeutics ( KRTX ) and its highly rated schizophrenia drug KARXT, and radiopharmaceuticals specialist RayzeBio ( RYZB ) - and the flagship SPDR® S&P Biotech ETF ( XBI ) has been soaring as result.

{kind=link}

As we can see above, after reaching its high water mark value of $166 in February 2021, when the success of Moderna ( MRNA ) and Pfizer ( PFE ) / BioNTech's ( BNTX ) messenger-RNA COVID vaccines put the entire sector heavily in credit, investors subsequently began pulling money out of early stage biotech as a spate of big money IPOs, rising interest rates, out of control inflation and concerns about cash burn versus successful drug approvals gave investors the jitters.

The XBI hit a low of ~$65 in June 2022 - down >60% in less than 18 months, and despite some early promise in 2023, was trading at the same value at the end of October this year. Clearly, the market seemed to have fallen out of love with biotech.

With the global economy beginning to find its feet again post pandemic, and with several new areas of research yielding some impressive results both in the clinic and in the real world setting - from PARP inhibitors, ADCs, Protein Degraders, and radiotherapeutics in oncology, to IL-17 inhibitors and Sphingosine-1-phosphate receptor modulators in immunology / anti-inflammatory, to the miraculous GLP-1 agonist drug class in weight loss diabetes, arguably, the biotech sector looks as investable today as at any time in the past few years, and while the COVID era surge in XBI's valuation never looked sustainable, many of the new drug classes underpinning its recent rise look set to stick around for many years, if not decades.

Despite a tricky year in 2023, I have been able to tease out some winners and share bullish recommendations with Seeking Alpha readers that have resulted in some good gains.

Some notable examples would be a call on BridgeBio ( BBIO ) in February - shares are up >250% since that bullish note - backing Rocket Pharmaceuticals ( RCKT ) in the same month - shares have risen >60% since - a vote for Ascendis Pharma in April, which would have returned 75% if backed - a bullish note on Eyepoint Pharmaceuticals in May - shares have risen >285% since - support for buying Ideaya stock in August, with the stock price rising >40% post-publication, and bullish notes on ophthalmology specialist Belite Bio ( BLTE ), autoimmune-focused cell therapy developer Cabaletta Bio ( CABA ), and protein degradation specialist Arvinas ( ARVN ), preceding gains of 54%, 23%, and 95%, respectively.

Naturally, not every call I have made has been a success - cell therapy stocks I have backed have mostly tanked amid a savage bear market in that field of research, whilst some stocks I tipped to fall have posted notable gains - Harmony Bio ( HRMY ), Cerevel Therapeutics ( CERE ), and most recently, TG Therapeutics ( TGTX ) being good examples.

When investing in biotech, or any other sector of the stock market, I like to take the optimist's view that you "either win, or you learn," and therefore, armed with another year's worth of experience, detailed due diligence, and good calls and bad, I am going to use the remainder of this post to highlight three companies I believe can have a strong year in terms of share price performance in 2024, and 2 "wildcard" companies that may either deliver skyrocketing gains, or eye-watering losses next year. So, without further ado, I'll begin with my three more "solid" bull cases.

Madrigal Pharmaceuticals - A Straightforward Early Win In 2024?

Big Pharma and the biotech industry has been attempting to secure approval to market and sell a drug targeting nonalcoholic steatohepatitis ("NASH"), without success to date. The field has been characterized by high profile late-stage study failures, and plummeting stock prices, as the FDA's criteria approval, shown below, remains stringent:

- Resolution of steatohepatitis on overall histopathological reading and no worsening of liver fibrosis;

- Or

- Improvement in liver fibrosis greater than or equal to one stage and no worsening of steatohepatitis;

- Or

- Both resolution of steatohepatitis and improvement in fibrosis.

Madrigal Pharmaceuticals ( MDGL ) looks set to win the so-called "NASH Dash" in 2024 however, with a Prescription Drug User fee Act ("PDUFA") - when the FDA announces whether it has approved or rejected a drug's New Drug Application ("NDA") - arriving on March 14th.

After Madrigal released compelling Phase 2 study results for its NASH candidate Resmetirom - a proprietary, liver-directed, selective thyroid hormone receptor-ß, or THR-ß, agonist administered as a once-daily oral pill - in 2018, shares in the company rose >$280 per share. What followed was a 3-year wait for Phase 3 MAESTRO-NASH data, however, which saw the market lose faith, and Madrigal stock fall to ~$70 per share.

In late December 2022, however, Madrigal finally released positive data from the study, sending its stock price skyrocketing to >$300 per share. Management discusses the data as follows in Madrigals' Q3 quarterly report / 10Q submission:

The subpart H portion of the study enrolled more than 1,000 patients with biopsy-proven NASH (with the majority having significant liver fibrosis (F2/F3)), randomized 1:1:1 to receive once-daily resmetirom 80 mg, resmetirom 100 mg, or placebo.

After 52 weeks of treatment, a second liver biopsy is performed. The dual primary surrogate endpoints on biopsy are NASH resolution with ?2-point reduction in NAS (NAFLD Activity Score), and with no worsening of fibrosis OR a 1-point decrease in fibrosis with no worsening of NAS. Achievement of either primary endpoint is considered a successful trial outcome.

In December 2022, we reported topline results from the subpart H portion of the study: resmetirom achieved both primary endpoints with both daily oral doses, 80 mg and 100 mg, relative to placebo.

It has taken another year for Madrigal to prepare its NDA for the FDA and have it accepted, but the successful Phase 3 seems to imply there are few obstacles preventing the FDA from granting resmetirom approval in March. The agency has indicated that it will not convene an Advisory Committee to discuss the application, which could be interpreted as a sign it believes Madrigal's data to be strong enough to support an approval.

If it were approved, resmetirom would be the sole approved drug in a market some analysts believe would support a peak revenue figure of ~$2.5bn, whilst others are more cautious, suggesting peak sales may only reach ~$1bn. Madrigal's current market cap is $4.6bn, with shares trading ~$230 per share.

There are competitive threats - Viking Therapeutics ( VKTX ) is developing a NASH drug with a similar mechanism of action to resmetirom that some observers believe has best-in-class potential, while Eli Lilly (LLY) and Novo Nordisk's ( NVO ) miracle weight loss drugs Wegovy and Zepbound could yet win approvals in NASH.

Given the historic nature of a NASH approval, Madrigal's first-mover advantage, and the drug's ability to be used in conjunction with Wegovy / Zepbound as an adjunctive therapy, however, my feeling is a 50% rise in market cap valuation would not necessarily flatter Madrigal, if resmetirom is approved in March, based on the higher end of analysts peak revenue expectations.

Intra-Cellular Therapies - De-risked CNS Play Attracting M&A Interest

If Bristol-Myers Squibb was prepared to pay $14bn for Karuna Therapeutics, whose schizophrenia candidate is not yet FDA-approved, with its PDUFA date arriving next September, and AbbVie prepared to pay $8.7bn for Cerevel, a CNS specialist with no commercially approved assets, then what does that say about the valuation of Intra-Cellular Therapies, Inc. ( ITCI )?

Intra-Cellular secured approval for Caplyta, whose mechanism of action is based on a combination of antagonism of serotonin 5-HT 2A receptors, and postsynaptic antagonism of dopamine D 2 receptors, in schizophrenia all the way back in 2019, and Caplyta was approved to treat bipolar disorder in 2021.

The drug earned revenues of $126m in Q3 2023, up 75% year-on-year, with prescriptions increasing 71% year-on-year. Across the first nine months of 2023, Intra-Cellular earned $331m of revenues, although the company recorded a net loss of $(125m). The forecast for 2024 is for revenues of $460 - $470m, with SG&A expenses of $405m - $420m, and &D expense of $185 - $200m.

Granted, this makes Intra-Cellular an unprofitable company, although if we exclude R&D expense, the company is EBITDA positive, and that R&D money is being well spent, used to develop lumateperone, the underlying ingredient in Caplyta, in the indication of Major Depressive Disorder. There are 2 Phase 3 studies ongoing in MDD, and Intra-Cellular expects to report results in "the first and second quarters of 2024, respectively."

Lumateperone's prior data in depression has been stellar , and analysts believe Caplyta could eventually generate peak sales of >$4bn per annum. If that were the case, using a rule of thumb valuation metric that a commercial stage pharma typically trades at 3-5x sales, it's clear that Intra-Cellular's valuation could climb significantly if its lead drug wins approval in MDD - a large and lucrative market.

There is a downside to consider - Intra-Cellular's share price, which is up 20% in the past month, may be artificially inflated by acquisition rumors, although should those rumors prove true, the company would surely fetch a double-digit billion valuation, implying a ~40% upside opportunity, and even if they do not prove true, the MDD data readouts arriving next quarter are potentially major upside catalysts, provided they are positive.

It is not hard to see a company like Biogen ( BIIB ), which failed to secure approval in MDD for its Sage Therapeutics ( SAGE )-partnered Zuralonone this year, making a substantial bid for Intra-Cellular, although as things stand, the company is doing an excellent job for shareholders even without the M&A speculation, and 2024 is likely to feature further revenue growth, and perhaps a supplementary new drug approval in MDD.

Ionis - A Gem In The Oligonucleotide Space With Big Pharma Backing

Back in September, in a note for Seeking Alpha, I gave Ionis Pharmaceuticals, Inc. ( IONS ) a "Buy" recommendation and the stock price has since gained by 25%. I wrote that the company:

remains a pioneering drug developer with a unique focus on antisense technology, which has produced 4 commercially approved drugs - QALSODY, SPINRAZA, TEGSEDI and WAYLIVRA - indicated for superoxide dismutase 1 amyotrophic lateral sclerosis ("SOD1-ALS"), spinal muscular atrophy, polyneuropathy caused by transthyretin amyloidosis with polyneuropathy ("ATTRv-PN"), and genetically confirmed familial chylomicronemia syndrome ("FCS") respectively.

Ionis unique approach to drug development is based on "antisense medicines" that target RNA, the "intermediary that conveys genetic information from a gene to the protein synthesis machinery in the cell". It is comparable to the RNA-interference approaches pioneered by Alnylam Pharmaceuticals ( ALNY ), and Arrowhead Pharmaceuticals ( ARWR ), but while Alnylam's market cap valuation is $24bn, and the company is heavily loss-making, with 5 approved drugs, Ionis' market cap is just $7bn, and Arrowhead, whose market cap is $3.4bn, has never commercialized a drug and is unlikely to do so in 2024.

Ionis therefore emerges as the logical stock to back in this field. The company has ambitious plans for growth, both through revenues earned from drugs it commercializes itself, and through milestone payments to it by its multiple Big Pharma partners, including AstraZeneca ( AZN ), Biogen, GSK ( GSK ), Novartis ( NVS ), and Roche ( RHHBY ). According to Ionis' 2022 annual report :

We have the potential to earn more than $23 billion in future milestone payments, licensing fees and other payments from our current partnerships. In addition, we are eligible to receive up to mid-20 percent royalties under our partnerships.

Not everything is perfect in relation to Ionis - the company is loss-making. Ionis' revenues - mainly derived from royalties, license fees and milestone payments from its Big Pharma partners, have declined since 2019, falling from $1.1bn, to $729m, then $811m, then $587m in 2022. After earning revenues of >$270m in 2018 and 2019, net losses have been $(444m), $(29m), and $(270m).

Nevertheless, the company has a compelling range of pipeline opportunities - Eplontersen, co-developed with AstraZeneca, was approved under the brand name Wainua for the treatment of polyneuropathy of hereditary transthyretin-mediated amyloidosis, also known as hATTR-PN or ATTRv-PN, on December 22nd. AstraZeneca will pay Ionis up to $485 million in development and approval milestones, plus up to $2.9 billion in sales-relates milestones, and the drug has been forecast to earn >$1bn in peak sales by analysts.

Meanwhile, Ionis is developing 3 wholly owned candidates in Olezarsen, Donidalorsen, and Ulefnersen. Olezersen is targeting severely elevated triglycerides ("TGS"), which breaks down into 2 indications, Familial chylomicronemia syndrome ("FCS") and Severe hypertriglyceridemia (SHTG) - a potential blockbuster opportunity, and donidalorsen, indicated for Hereditary angioedema ((HAE)), could earn peak revenues of ~$500m, it has been speculated.

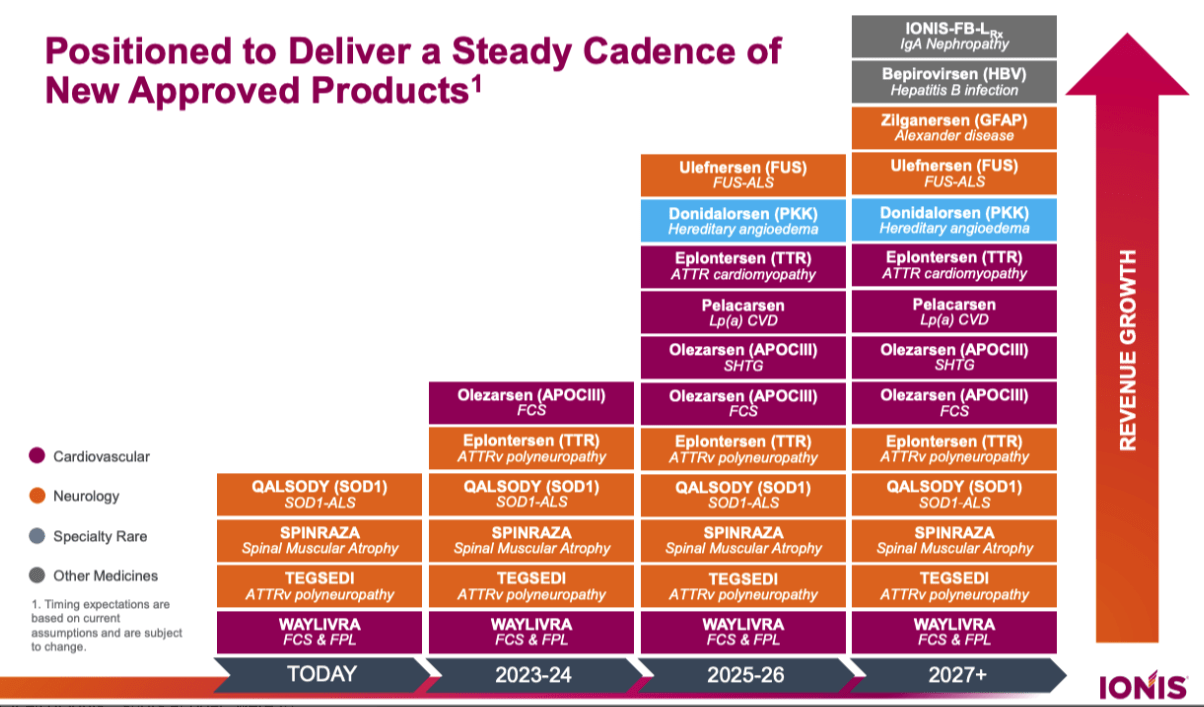

In short, Ionis' ability to churn out approvable drug candidate, guide them through the clinical study and FDA approval process, and earn handsome revenues for itself and its partners, plus substantial milestone payments, is unmatched by almost any other Pharma that I can think of, and as such, I do not think a double digit billion market cap would flatter Ionis, which could target $3bn in annual revenues by 2030, based on its detailed plans for drug launches as shown below in a recent investor presentation:

Ionis portfolio expansion plans (investor presentation)

{kind=link}

Ionis may have earned revenues of just $463m in the first three quarters of this year, versus operating expenses of $732m, but the company retains >$2bn in cash, allaying any financial concerns, and with so many data readouts and approval shots to come, as shown below, the future for this unique company, and its valuation, still looks very bright, in my view.

Ionis pipeline overview (Ionis Q3 earnings presentation)

{kind=link}

2 Wildcard Picks For 2024 - Solid Tumor Cell Therapy Pioneer Iovance, In-Vivo Gene Therapy Play Verve Therapeutics

To conclude this post on "Stock to Watch" in 2024, I will briefly single out two companies that represent "wildcard" picks for 2024.

Iovance Biotherapeutics, Inc. ( IOVA ) stock has had a roller-coaster year in 2023, falling to low of $3 per share in mid-October, before staging a sudden bull run up to >$8 per share at the time of writing. The company is close to securing an historic approval for a ex-vivo cell therapy targeting a solid tumor cancer, in this case melanoma - a feat which has never been achieved before.

Lifileucel in Advanced Melanoma is under review with the FDA and the PDUFA date is set for February 24th, 2024. The date has already been delayed by 3 months due to "insufficient resources" at the agency, but if approved, analysts believe the drug can earn revenues of >$700m, and perhaps even top $1bn.

The data is relatively strong, with a 36% objective response rate ("ORR"), and 36-month duration of response, although doubts around durability of the therapy persist, as the ORR fell slightly in a later data release, which weighs down Iovance's valuation. If an approval is secured in February, however, Iovance, whose current market cap is just over $2bn, could realize a substantial share price gain, thanks to the validation of a full FDA approval, potential blockbuster revenue opportunity, and quite possibly make Iovance an M&A target for Big Pharma.

And finally, as a fan of biotech and an avid biotech stock watcher, it is hard not to root for Verve Therapeutics, Inc. ( VERV ) and its efforts to develop an in-vivo gene therapy to treat cardiovascular disease. Ex-Vivo cell therapies have garnered multiple approvals in hematological cancers, and generated blockbuster revenues for Pharma's such as Gilead Sciences ( GILD ) and Bristol-Myers Squibb, whilst Iovance looks set to potentially open up the solid tumor market.

Ex-vivo cell therapies involve painful preconditioning regimes for patients as cells are harvested, and are associated with some significant safety concerns, as engineering cells ex-vivo could lead to "off-target" activity which can trigger unwanted and potentially dangerous cell mutations. In vivo therapies, administered via intravenous infusion or even subcutaneously, may represent a faster, safer, and more potent treatment alternative in time, although delivery issues mean no in-vivo therapy has ever secured a commercial approval.

Verve Therapeutics is partnering with the world's most valuable Pharma company, Eli Lilly, to develop 2 in-vivo cell therapy programs directed against cardiovascular disease, using base editing technology developed by Beam Therapeutics ( BEAM ).

Beam sold the rights to Verve's programs to Lilly, and this initially looked to be a wise decision , as the market sold off Verve stock when one patient out of six in a phase 1 study experienced a myocardial infarction (Grade 3) the day after treatment.

The adverse safety event - while serious and demanding that Verve and Lilly proceed with the utmost care - may be unrelated to the therapy, which in fact returned some promising data - according to a press release :

The two patients treated with 0.45 mg/kg of VERVE-101 had a time-averaged blood PCSK9 protein reduction of 59% and 84%. The patient treated with 0.6 mg/kg of VERVE-101 had a time-averaged blood PCSK9 protein reduction of 47%.

The two patients treated with 0.45 mg/kg of VERVE-101 had a time-averaged LDL-C reduction of 39% and 48%. The patient treated with 0.6 mg/kg of VERVE-101 had a time-averaged LDL-C reduction of 55%. In this single participant in the highest dose cohort, the 55% reduction in LDL-C was durable out to 180 days, with follow-up ongoing.

The fact that Verve's in-vivo therapy reached its target - thanks to pioneering lipid nanoparticle ("LNP") delivery technology (similar to the deliver technology in mRNA COVID vaccines) - and was able to trigger a positive effect in the form of a reduction of LDL-C, a form of bad cholesterol, is a genuinely exciting development. Providing the safety elements of the study can be managed adequately, Verve and Lilly may be on the verge of a major breakthrough in gene therapy that could trigger a seismic shift in the way patients are treated for cardiovascular disease, and a major improvement on current standards of care.

The FDA recently lifted its clinical hold on studies of Verve's candidates in the U.S., which will potentially speed up progress in this exciting field of development.

For further details see:

3 Biotech Bull Cases To Consider In 2024 - And 2 Wildcard Recommendations