WEC - 3 'Boring' Utilities I'm Buying Hand Over Fist

2024-01-17 07:00:00 ET

Summary

- I've avoided investing in utilities in the past, but not now.

- The best-in-breed utility companies now look compelling, as higher interest rates and investor focus on bonds have driven their valuations down to levels last seen nearly five years ago.

- Top-notch utilities offer solid growth prospects and reasonable dividend growth. I provide a list of three favorites.

This article was coproduced with Chuck Walston.

As a kid, I always loved playing Monopoly.

Did you know that with each roll of the dice, you have a 2.6% chance of landing on the Electric Company, a 2.8% chance of landing on Water Works, and a 5.4% chance of landing on either utility.

Owning utilities (in Monopoly) isn't sexy, either.

If you only own one utility property, the highest possible rent you get is $48. If you own both properties, you could earn as much as $120 each time.

With that being said, why am I recommending this boring sector now?

I've avoided utilities for several reasons.

At the top of that list was my perception that utilities were slow-growing businesses marked by at best moderate dividend growth rates.

The fact is that top-notch utilities not only have solid growth prospects but also offer reasonable dividend growth, and the current environment offers what I view as compelling valuations for the best-of-breed.

I'll use American Water Works CEO Susan Hardwick's comment during the last earnings call to sum up my perspective on this sector:

While utility stocks, including ours, have seen the impact on the short term of higher interest rates, history has shown that over medium- and longer-term horizons, the utility sector and certainly American Water has delivered compelling value to investors.

The bottom line is that higher interest rates and investors' focus on bonds has driven the valuations for many utility stocks to levels last seen nearly a half decade ago. Furthermore, there are several utilities with reasonable growth prospects.

First Up: American Water Works

American Water Works Company, Inc. ( AWK ) is the largest publicly traded water and wastewater utility in the U.S. The company has approximately 1.3 million customer connections, including those in their pipeline.

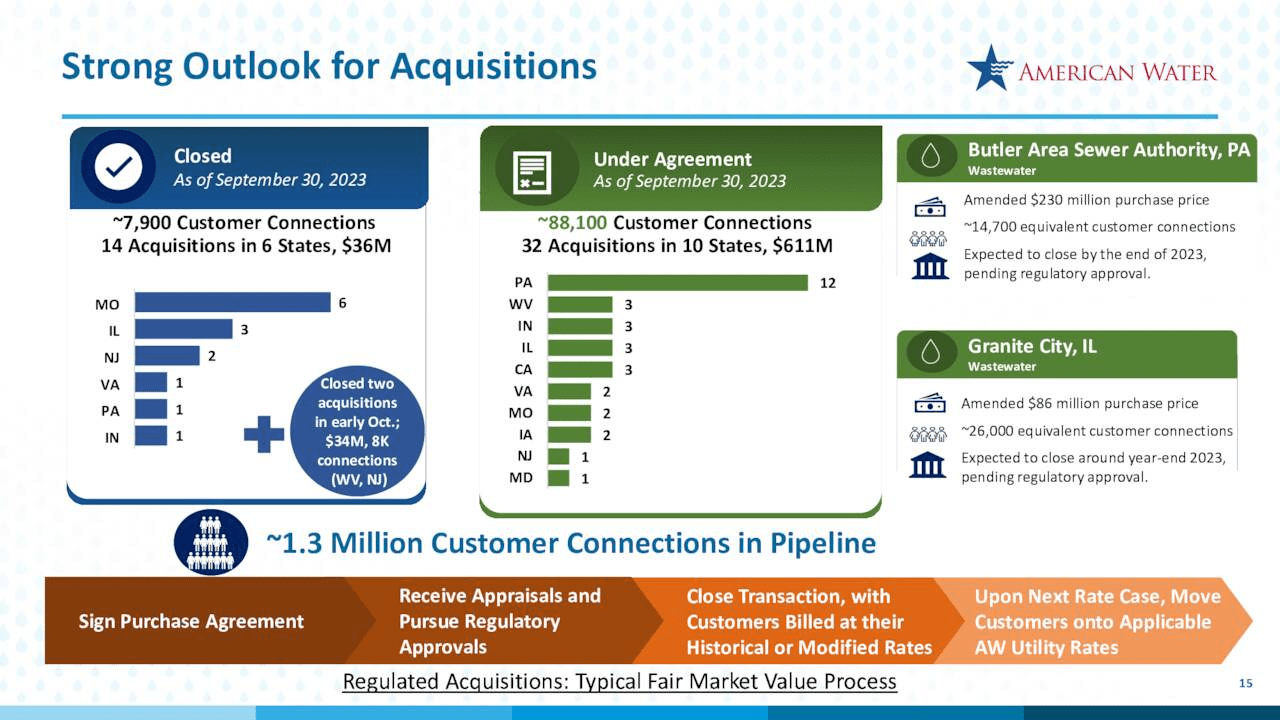

Last quarter, AWK completed four acquisitions. That brought the firm's total acquisitions year-to-date to fourteen. Those deals added about 7,900 new customer connections.

American Water has an additional 32 acquisitions in 10 states under agreement. Collectively, those deals will cost $611 million and add approximately 88,100 customer connections.

{kind=link}

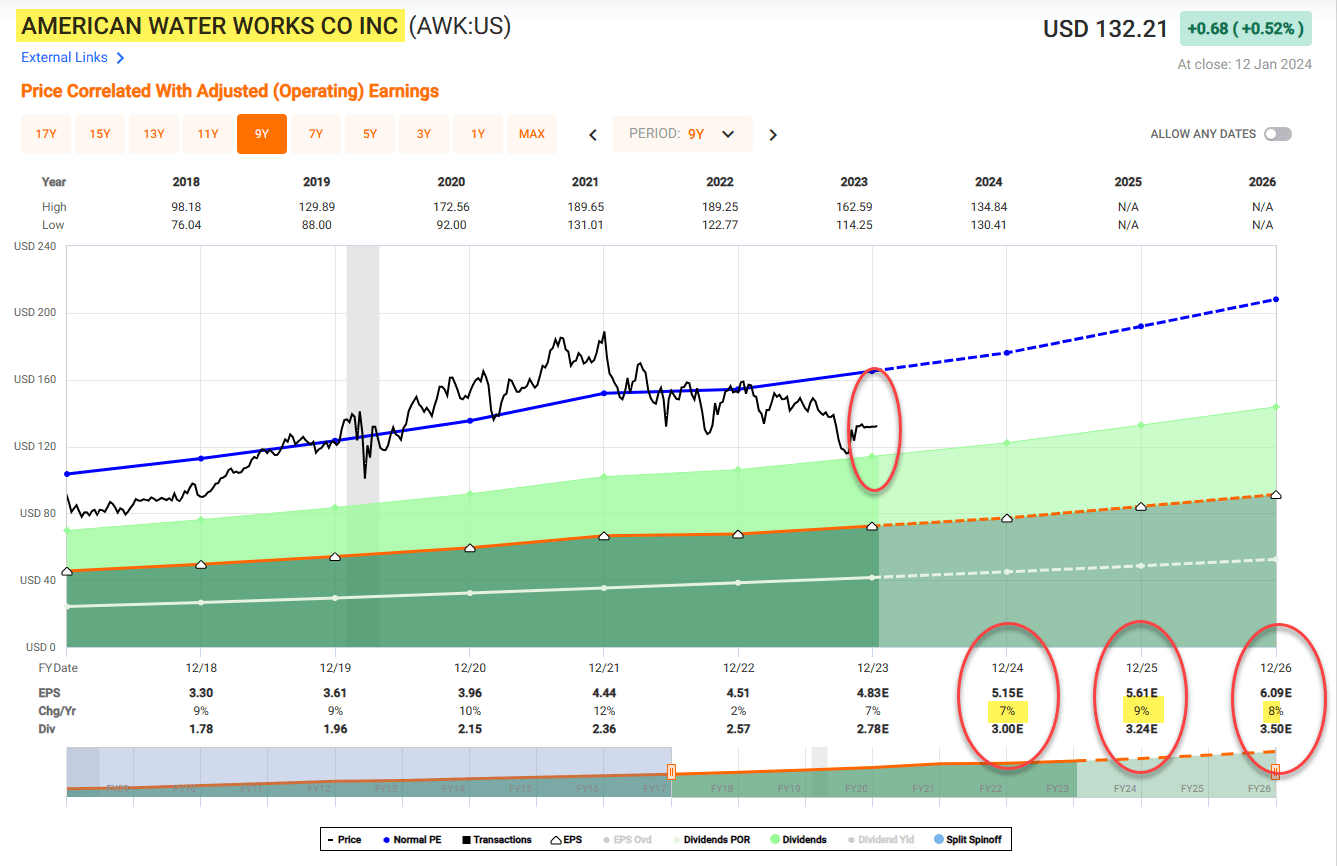

For 2024, management guides for weather-normalized EPS in a range of $5.10 to $5.20. That would constitute around 8% growth over the company's weather-normalized 2023 EPS guidance.

AWS projects a long-term EPS CAGR in a range of 7% to 9% and targets a long-term dividend growth rate in a 7% to 9% range.

Like the other utilities I'm highlighting, AWK's share price has been pounded over the last twelve months. However, the stock provided a total return over the last decade of nearly 287%, handily beating the S&P 500's (SP500) total return of about 216% in that time frame.

And AWK outperformed while providing a dividend that's grown at a near 10% pace over the last five years. With a current yield of 2.14% and a payout ratio of 56.54%, the dividend is safe and likely to grow at a relatively robust pace in the foreseeable future.

AKW's debt is rated A by S&P 500 and Baa1 by Moody's.

{kind=link}

WEC Energy Group

The largest Midwest utility, WEC Energy Group, Inc. ( WEC ) is a 98%-regulated energy company with 4.7 million utility customers. While nearly two-thirds of the firm's customers are in Wisconsin, WEC's operations also serve Illinois (17% of customers), Minnesota (5%), and Michigan (5%).

Through its subsidiaries Wisconsin Public Service, We Energies, Peoples Gas, North Shore Gas, Michigan Gas Utilities, Minnesota Energy Resources, and Upper Michigan Energy Resources, WEC delivers natural gas and generates and distributes electricity.

Approximately 75% of WEC's revenue stems from electricity generation and distribution and 22% from natural gas distribution. Through WEC's We Power, the company also builds, and owns electric generating plants.

Almost 75% of WEC's earnings are generated from constructive Wisconsin and Federal Energy Regulatory Commission regulation, while the remainder of its revenues are from its renewable energy business.

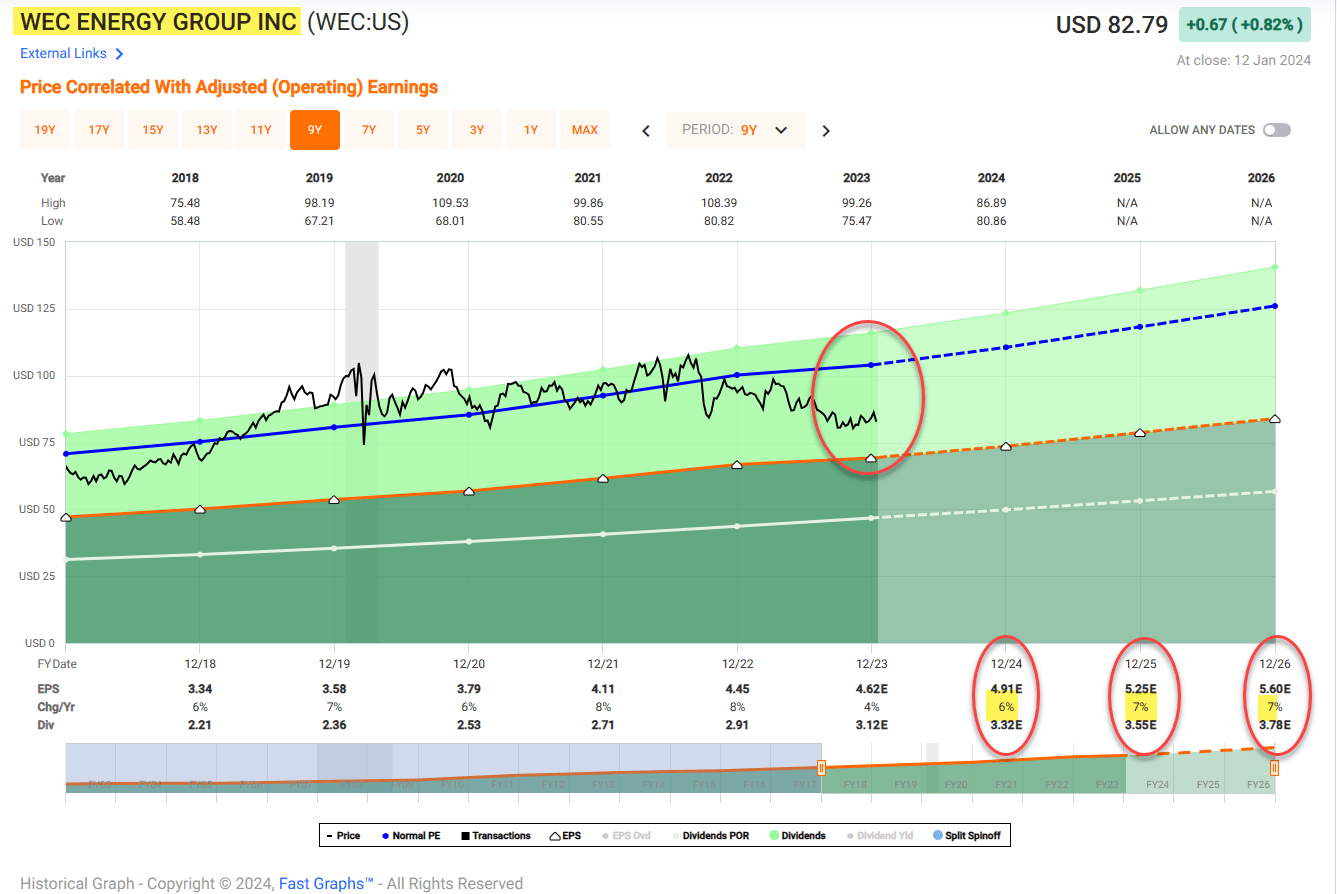

Management guides for annual earnings growth in a range of 6.5% to 7% through 2028. It should be noted here that the company has a sterling record of meeting and oftentimes beating its earnings guidance.

A good deal of that growth will come from what has been described as a "massive data center expansion" in Wisconsin. Last March, Microsoft ( MSFT ) revealed a plan to build a $1 billion data center in Mount Pleasant, Wisconsin. That was followed in November by Microsoft's announcement that it would increase the investment in the Mount Pleasant site markedly.

The first data center alone represents over 1,000 MW's of electricity load, or over 10% of the WEC's current load in the state.

The company recently increased its capital investment plan to $23.4 billion, up 17% from its previous plan.

WEC projects annual electricity demand growth in a range of 4.5% to 5% from 2026 through 2028, largely based on the data center developments.

WEC has $6.8 billion in capex targeted for new solar, battery storage, and wind generation projects. In total, they should add 3.8 gigawatts of additional generation capacity.

The company is also moving to shutter 1,400 MW of coal powered plants and to retire its less-efficient natural gas generation facilities.

WEC has a current yield of 4.03%, a payout ratio of nearly 71%, and a 5-year dividend growth rate of 7.14%.

WEC's debt is rated BBB+ by S&P and Fitch and Baa1 by Moody's.

{kind=link}

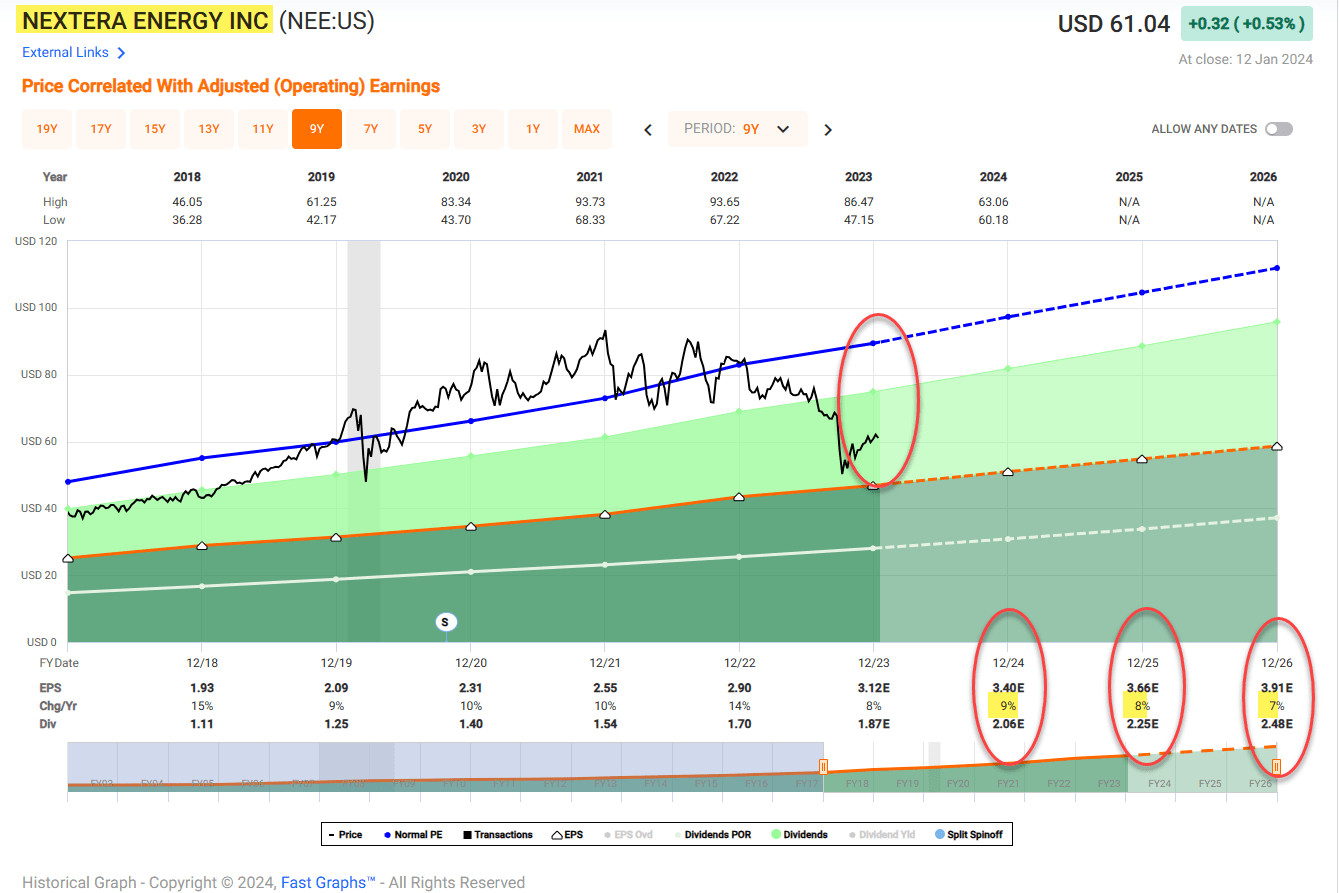

NextEra Energy: Higher Risk, Higher Reward?

With a market cap of $125 billion, NextEra Energy, Inc. ( NEE ) is the largest utility in the U.S.

NEE is not only America's largest electric utility, it also owns NextEra Energy Resources ("NEER"), the world's largest generator of wind and sun energy and a world leader in battery storage.

NextEra's electricity generation costs are considerably lower than its peers. That advantage resulted in the company posting a compound adjusted EPS growth rate of 9.8% since 2012. In contrast, most peers increase the bottom line at low-single-digit percentages.

NEE operates in two segments: NEER, which generates about 35% of the firm's revenue, and the company's Florida Power & Light ("FPL").

NEER is at the forefront of the move to develop wind generation. Early on, the company secured premier locations in the U.S. along with 20-year contracts with price escalator clauses.

Of NextEra's 70 gigawatts ("GW") of power generation, 34 GW are from renewable energy. Of those, 23 GW consist of wind power and 6 GW of solar power, making the company a global leader among electric utilities for power generation from those sources.

NextEra's FPL segment generates about 65% of earnings from utility operations in Florida, a state experiencing steady energy demand from population growth. The utility also benefits from industry-leading constructive regulation in Florida.

Although NEE has had a strong year, with adjusted earnings per share up 10.8% through the first three quarters, and management guides for annual earnings growth at the upper end of the long-term target of 6% to 8%, the stock is trading at levels seldom seen since 2019.

{kind=link}

NextEra is down more than 28% over the last twelve months. This is largely due to developments related to NextEra Energy Partners, LP ( NEP ), a subsidiary of NEE.

NEP relies on debt to fund its business model, and higher rates now present a stiff headwind.

Last September, NEP lowered its growth forecast for limited partner distributions. NEP now guides for annual distribution growth in a range of 5%-8% through at least 2026, along with a target growth rate of 6%. Management had previously projected annual growth of 12%-15% over that time frame.

That announcement led to NEP stock plummeting from over $48 per share to $21 in less than two weeks. NextEra's shares also swooned, from over $68 in late September to about $49 in the first week of October.

In an effort to right the ship, last month, NEP priced a private offering of $750 million in unsecured notes at 7.25%. The proceeds from that transaction will be used to repay 4.25% senior notes due in July and September 2024 along with debt from the firm's revolving credit facility.

The company is also selling assets in a dual effort to transition to a pure-play renewable energy producer and to raise additional funds. In November, it sold STX Midstream to Kinder Morgan ( KMI ) in a $1.8 billion deal.

These developments provide NEP with the funds needed to buy out its CEPF through 2025 and pay down some of its credit facility debt.

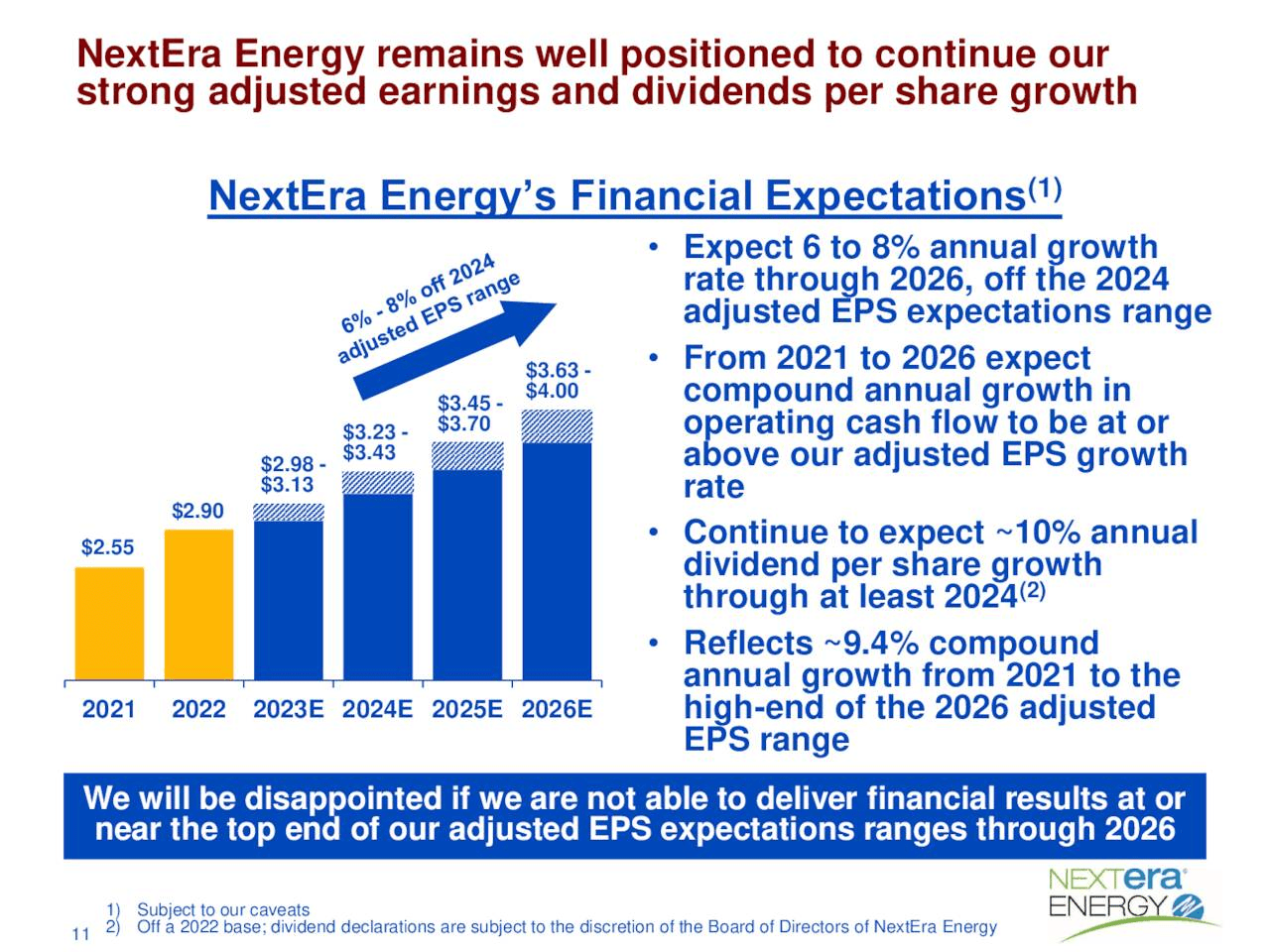

NextEra Energy has increased its dividend at a double-digit annual rate for 29 consecutive years. With a current yield of 3.06%, and a payout ratio just below 58%, management guides for dividend growth of 10% through at least 2024.

The company also forecasts earnings to increase in a range of 6% to 8% a year through 2026.

With a backlog of 21 gigawatts, a good deal of the firm's growth is assured.

NextEra's debt is rated A- by S&P, Baa by Moody's, and A by Fitch.

{kind=link}

Summation

Utilities are monopolies in the areas they serve; however, to raise rates and to move ahead on many development projects requires the approval of the government. Each of the highlighted companies operates in a constructive regulatory environment.

While this business model often leads to slow growth, it also means investments in utilities tend to be quite safe.

Each of the listed companies stands out among their peers.

NextEra has built one of the largest clean energy companies in the world. The company has also grown its earnings per share at a 9% CAGR for a decade, which is three times faster than its rivals.

American Water Works is the largest publicly traded water and wastewater utility in the U.S. Over the last ten years, AWK's stock has outperformed the total returns of the S&P 500 by a wide margin (the same holds true for NEE).

While WEC Energy Group is not on par with the first two in terms of its size versus peers, the growth catalyst from Microsoft's data center expansion should drive revenue for the foreseeable future.

Each of the highlighted companies has investment grade debt and has a history of strong growth and dividend payments. The three are also trading at valuations near the lowest levels since 2019.

I rate each of the companies as a BUY.

I am not invested in any utilities, but I intend to initiate a position in each of the companies reviewed in this article after the market opens on Tuesday.

Author's note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

3 'Boring' Utilities I'm Buying Hand Over Fist