REXR - 3 Cheap REITs That Could Return 25% Before My Birthday (In May)

2024-01-19 07:00:00 ET

Summary

- I'm planning a big birthday bash in May.

- And one way that I can celebrate is by investing in some cheap REITs.

- Let's hope that Mr. Market agrees with my picks.

I have a birthday in May.

The 10 th to be precise.

That’s just four months from now.

I’m already planning now because I want to celebrate by having a big birthday bash.

This weekend I dropped my car off at the Porsche shop and the dealership gave me this very cool loaner:

{kind=link}

That’s a 2023 Porsche Taycan (arctic blue) and it’s now on my wish list.

In case you didn’t know, I have a vice for nice cars.

I already own a Panamera and Boxster, and while most cars don’t appreciate (in value), I’ve found that high quality cars (purchased with a margin of safety) do.

So maybe, just maybe, Mr. Market can reward me on or before May 10 th …

How you may ask?

Keep reading…

An Experiment

As most know, I’m a real estate investment trust, or REIT, analyst, and I’ve been able to grow my nest egg by investing in quality stocks when they are trading at cheap prices.

Sounds simple, right?

Let’s start with quality.

Just like the Taycan, in order to understand quality, I always look under the hood…

Earnings history, Dividend history, Dividend safety, Balance Sheet, Management, Growth prospects.

All of these attributes are important when analyzing stocks…and if any of these less than favorable, I avoid them.

Why settle for a Volkswagen when you can own a Porsche?

Now, I know that answer…

Price.

So, what I want to own is a Porsche for the price of a Volkswagen.

How do you do that?

Keep reading…

3 of my Highest Conviction Picks

What else happens in May?

The Federal Reserve meets again on January 30th and will end with a policy statement on January 31st.

As of January 10th, interest rate traders assigned a 95% probability to the FOMC leaving the short-term federal funds rate unchanged at a target range of 5.25% to 5.50%, according to CME Group's FedWatch Tool .

We believe that the Fed could begin to decrease rates at the May meeting or perhaps as early as March. We’ve already seen what could happen when the word “pause” occurs.

{kind=link}

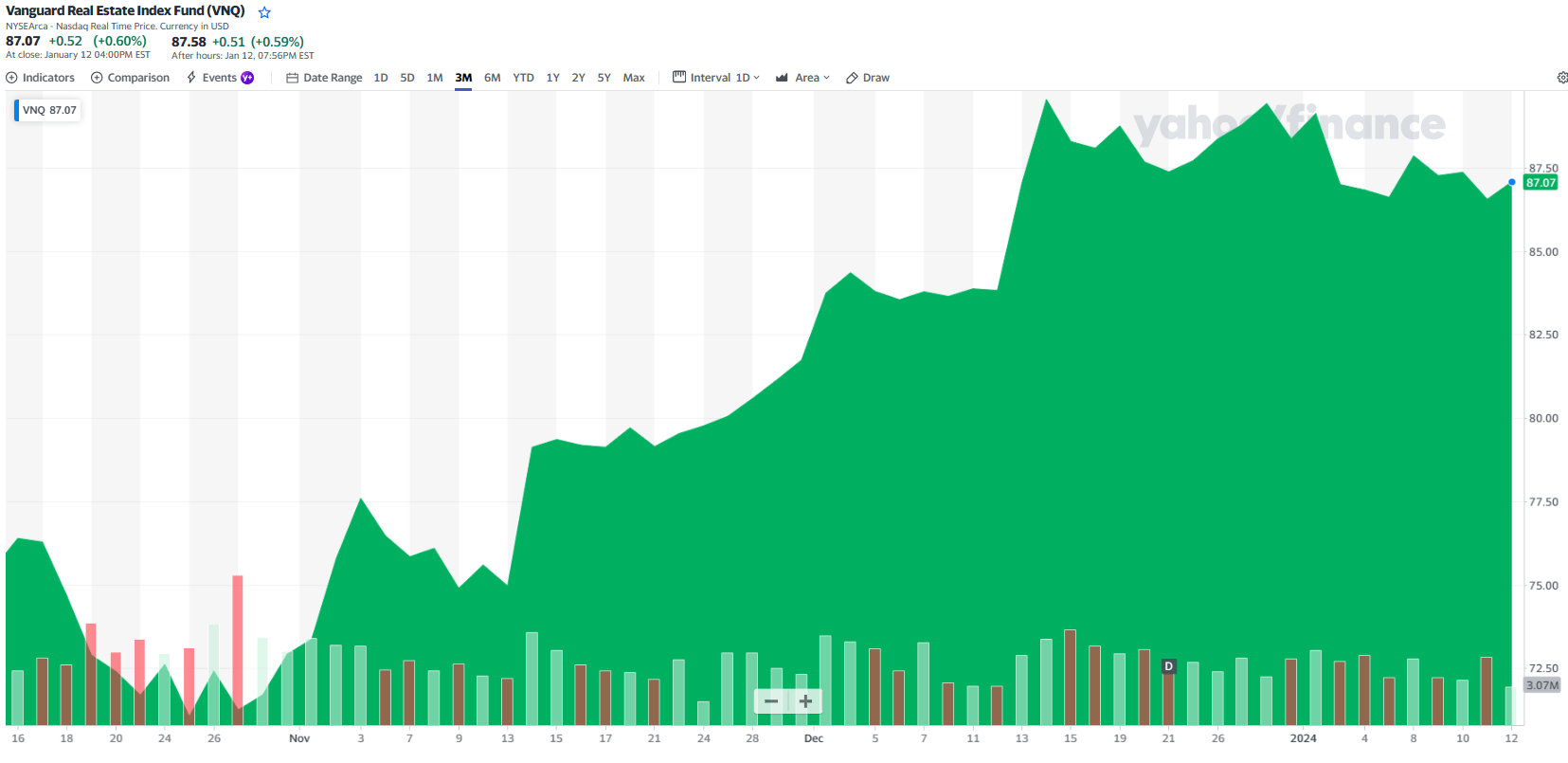

Looks good right?

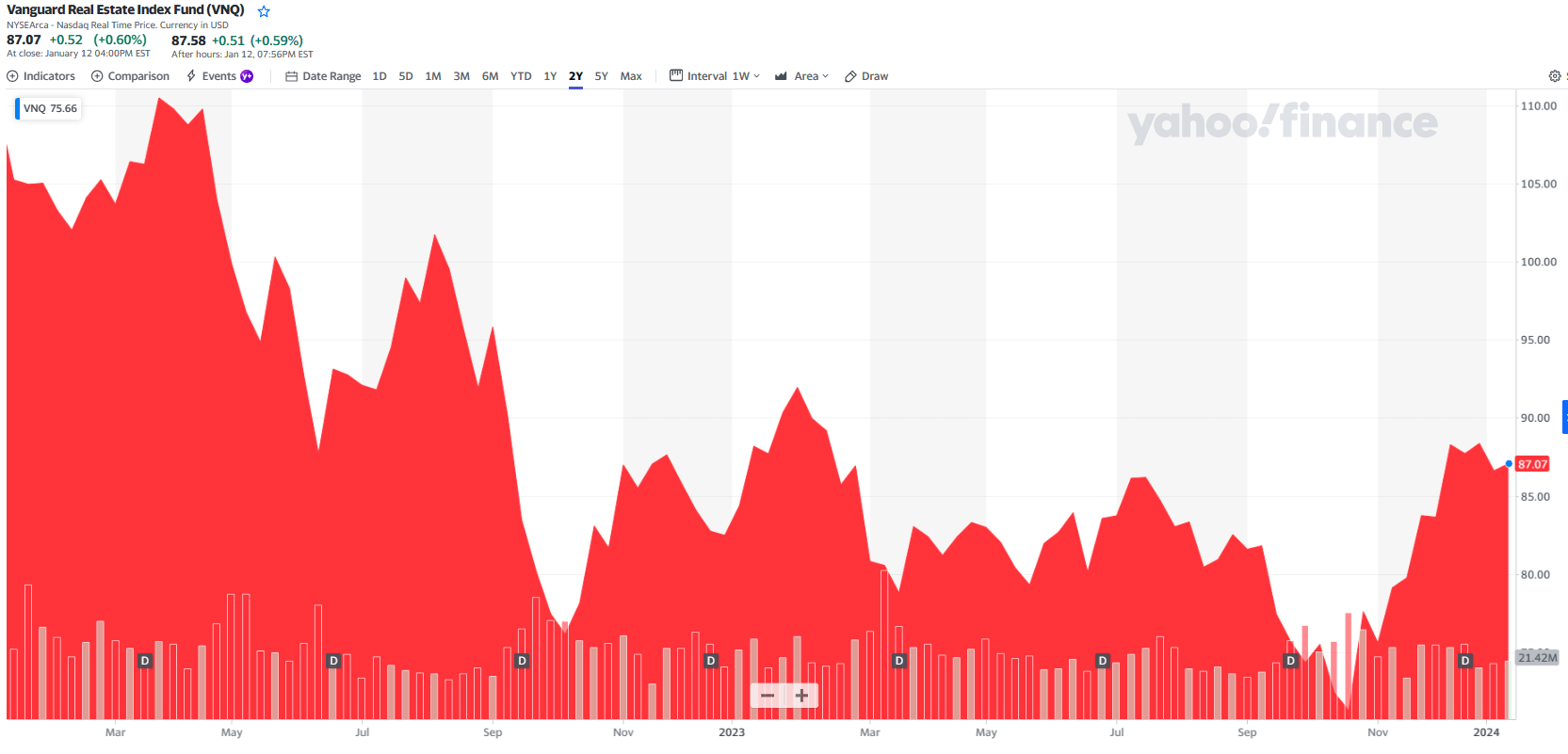

But wait, let’s look at the 2-year chart:

{kind=link}

Now that’s just a broad-brush exercise in which I used the Vanguard Real Estate ETF ( VNQ ) as the benchmark.

And we all know that you can’t paint all REITs by the same brush…

In my view, the highest quality REITs with the best balance sheets will perform better over the next few months and quarters.

When rates do fall, they won’t drop rapidly, and many of the lower quality REITs will continue to struggle.

I believe the winners will be the so-called blue chips and that’s precisely what I’m buying.

So, without further ado, let’s sing Happy Birthday to Me!

Four Corners Property Trust, Inc. ( FCPT )

FCPT began as a subsidiary of Darden Restaurants in 2015 and was formed to acquire, own, and lease restaurants and other food-related properties on a net basis.

In late 2015, FCPT was spun-off and received an 100% equity interest in 418 restaurants operated by Darden, primarily under the brands Olive Garden and LongHorn Steakhouse.

FCPT is now an independent net lease REIT that specializes in the acquisition and management of restaurants, and to a lesser extent other retail properties, primarily consisting of auto service and medical retail.

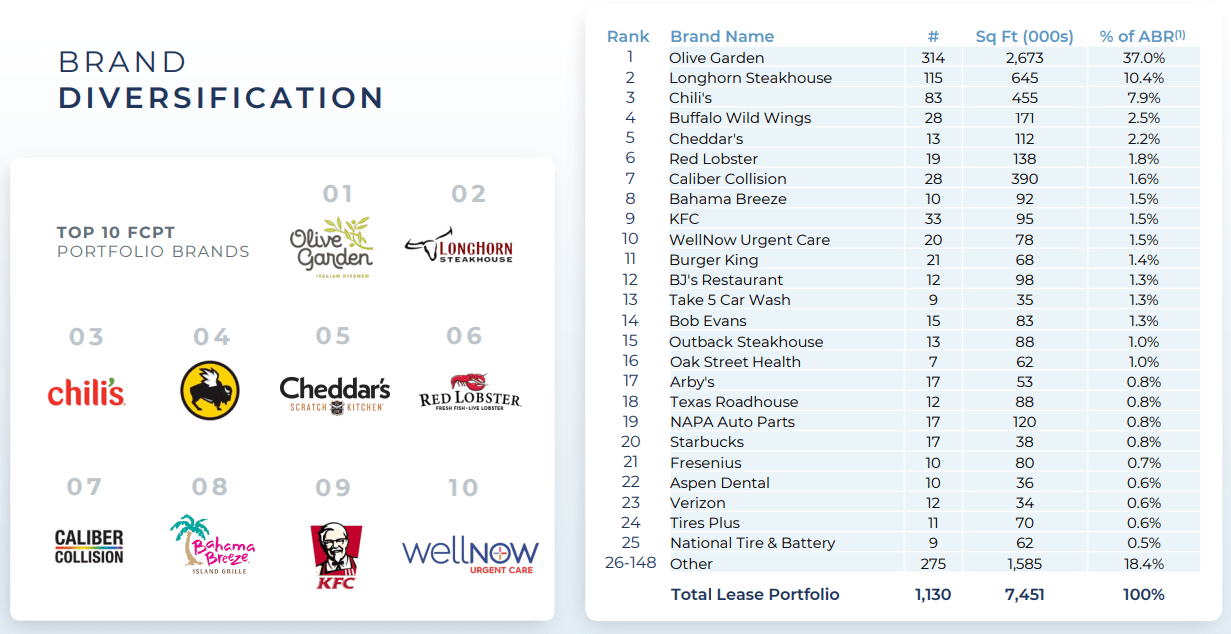

As of its most recent update , FCPT’s portfolio was comprised of 1,106 commercial properties operating under 148 brands across 47 states.

Some of the brands FCPT’s properties operate under include Olive Garden, LongHorn Steakhouse, Chili’s, Red Lobster, Outback Steakhouse, Arby’s and Burger King. Additionally, some of their non-restaurant brands include Caliber Collision, WellNow Urgent Care, NAPA auto parts, and Aspen Dental.

Olive Garden is by far FCPT’s largest tenant and makes up 37.0% of their annualized base rent (“ABR”). LongHorn and Chili’s are their second and third largest tenants and make up 10.4% and 7.9% of FCPT’s ABR, respectively.

At the end of the third quarter, FCPT’s portfolio was 99.8% occupied with 4.8x tenant EBITDAR coverage and had an average lease term remaining of 8 years.

{kind=link}

While FCPT is primarily known for its restaurant properties, the net lease REIT has been expanding into other e-commerce resistant industries such as the auto industry and medical retail.

FCPT targets auto service properties that do not rely heavily on the combustion engine, such as tire service and collision repair which will stay relevant as electric vehicle adoption increases. Their Auto Industry portfolio consists of 138 leases and made up 9% of their ABR.

FCPT’s looks for medical retail properties that specialize in urgent care, dental, veterinary, and outpatient services. Their portfolio of medical retail properties consists of 84 leases and made up 7% of FCPT’s ABR.

{kind=link}

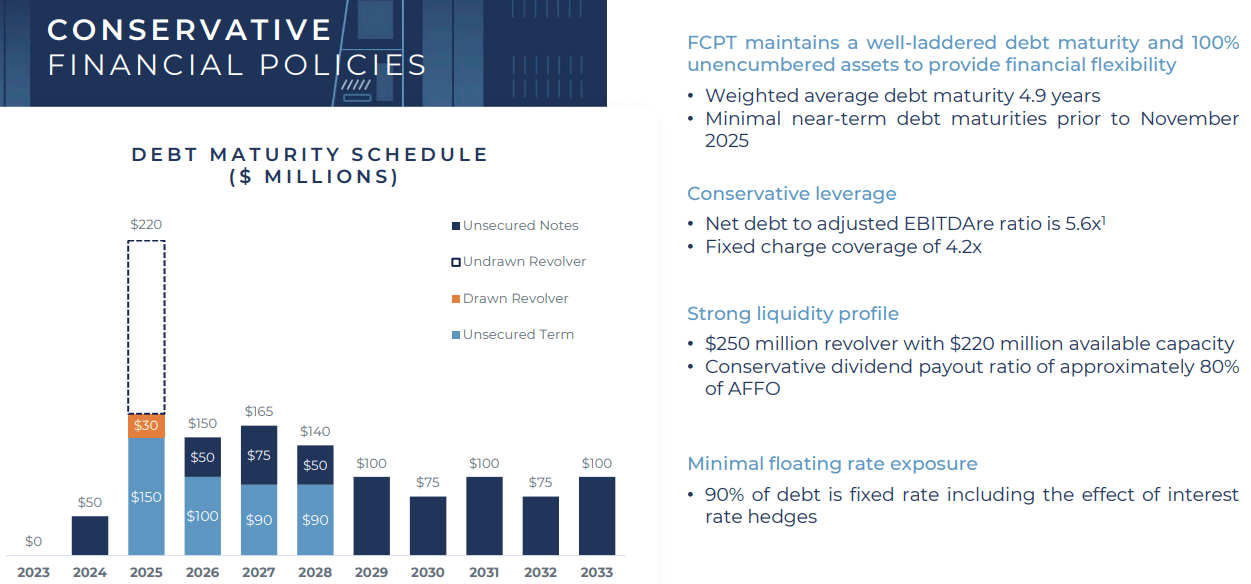

The net lease REIT has an investment-grade balance sheet with a Baa3 credit rating from Moody’s and solid debt metrics including a net debt to adjusted EBITDAre of 5.6x, a long-term debt to capital ratio of 42.17%, and a fixed charge coverage ratio of 4.2x.

Additionally, 100% of their ABR is unencumbered, 90% of their debt is set to a fixed rate, and their debt has a W.A. term to maturity of 4.9 years.

{kind=link}

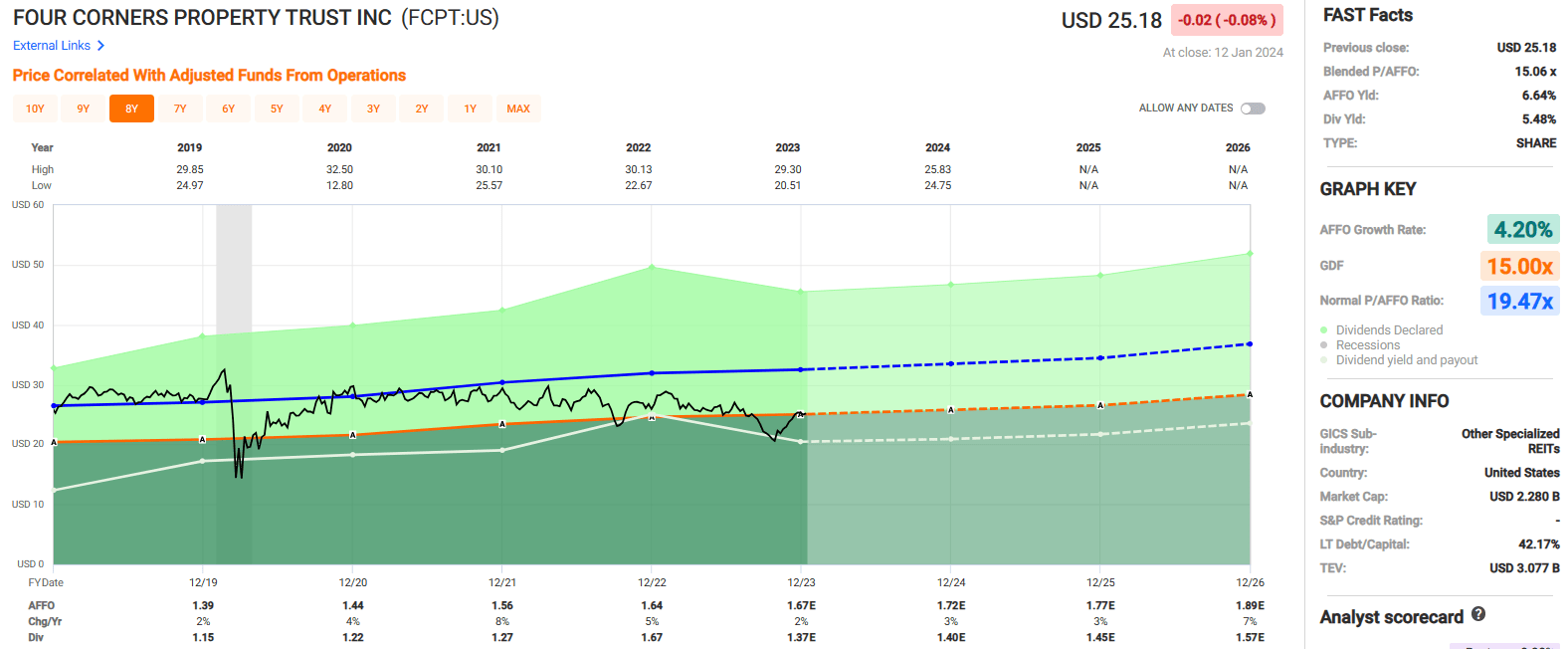

Since 2019, FCPT has had an average adjusted funds from operations, or AFFO, growth rate of 4.20% and a compound dividend growth rate of 10.60%.

Analysts expect AFFO per share to increase by 3% in both 2024 and 2025, and then increase by 7% in 2026.

The stock pays a 5.48% dividend yield that is well covered with an AFFO payout ratio of 81.74% and trades at a P/AFFO of 15.06x, compared to its average AFFO multiple of 19.47x.

{kind=link}

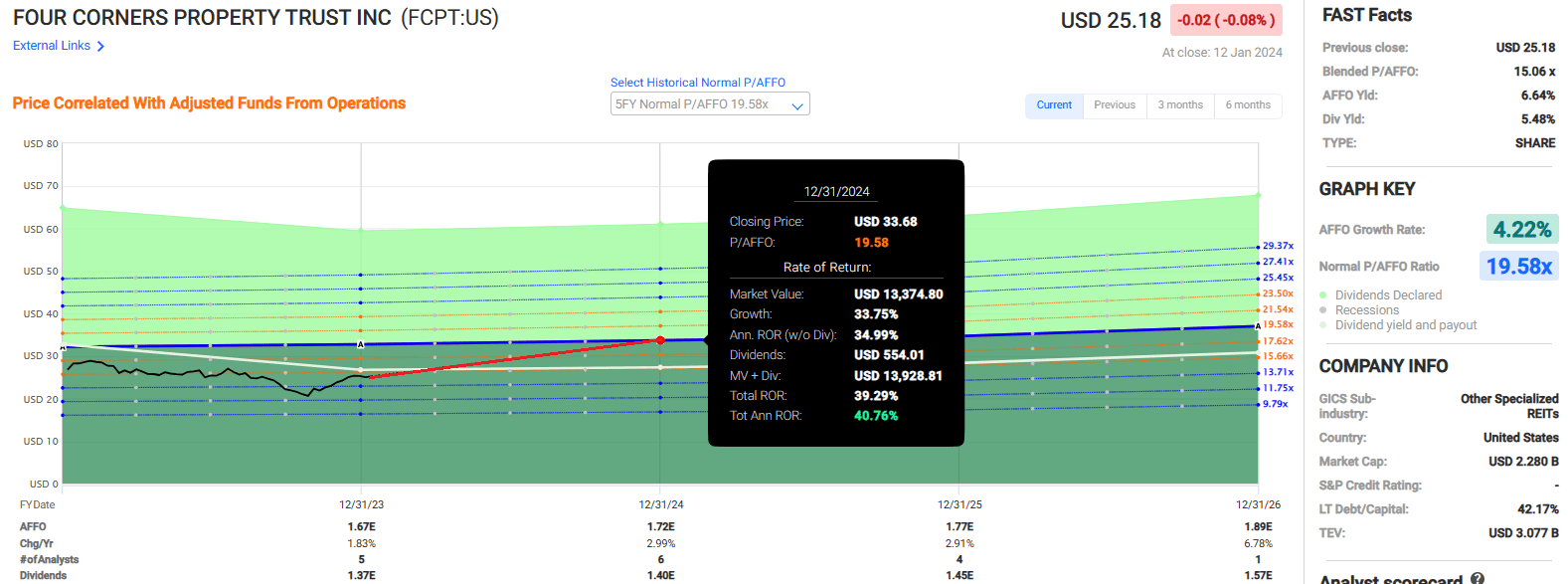

If FCPT can trade back up to its 5-year normal AFFO multiple of 19.58x by the end of 2024, it would result in total annual rate of return of 40.76%.

We rate Four Corners Property Trust a Hold.

{kind=link}

Alexandria Real Estate Equities, Inc. ( ARE )

ARE is a life science REIT that has been sold off with the rest of the office sector but is significantly different than a traditional office REIT.

Alexandria pioneered the life science real estate niche and is the clear leader in the space. It has a 75.1 million SF asset base in North America consisting of 41.5 million SF of operating properties and 33.6 million SF of properties undergoing construction, in development, or allocated for future development.

ARE specializes in the development and management of life science laboratories which are used by leading pharmaceutical, bio-technology, and other healthcare related companies such as Bristol-Myers, Moderna, and Merck as well as top academic institutions including Harvard University, New York University, and Massachusetts Institute of Technology.

The main point is that many of the tasks done in ARE’s lab space are regulated and cannot be done from home or over Zoom. Some sceptics may point to cell phone data, but I don’t ever see a day when scientists at Eli Lily are mixing up chemicals for Cymbalta in their kitchen, regardless of what the cell phone data may or may not imply.

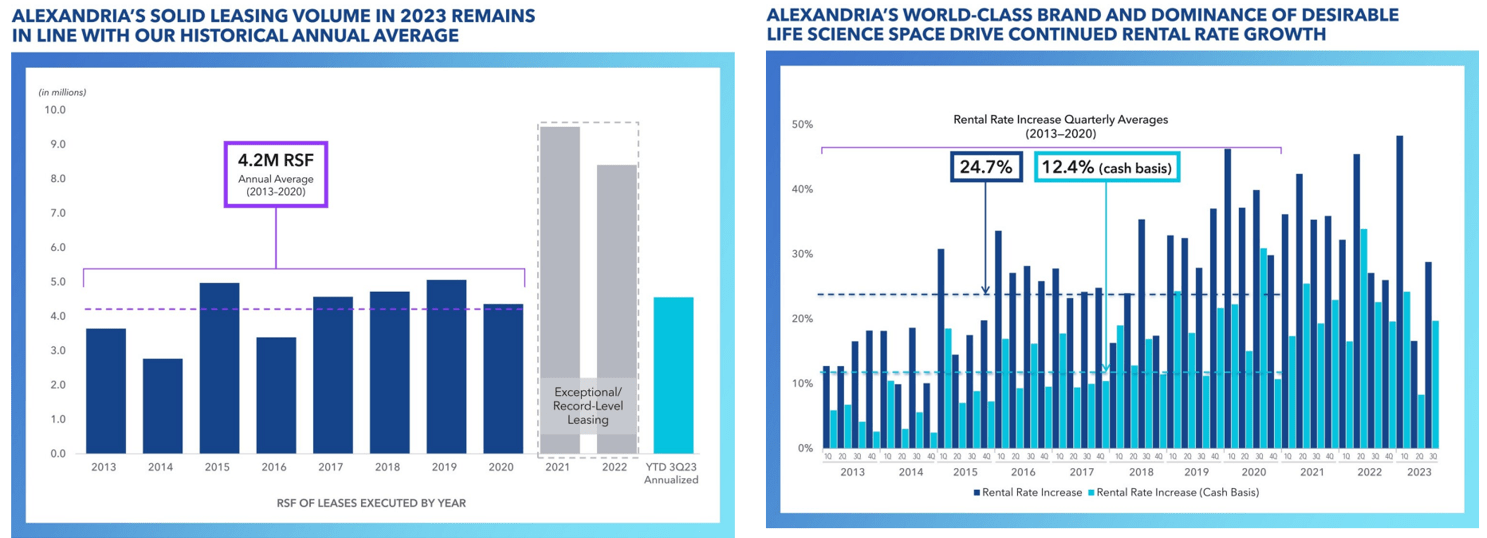

But don’t take my word for it, Alexandria’s third quarter results showed solid leasing volume of 867,582 SF with a W.A. lease term of 13 years and a reported rental rate increase of 28.8% or 19.7% on a cash basis. These numbers are not indicative of a REIT struggling with occupancy.

ARE’s year-to-date 3Q23 annualized leasing volume of 4.2 million SF is in line with their average leasing volume from 2013 to 2020 and their 3Q23 rental rate increases exceeded their average over that same period.

{kind=link}

ARE is a blue-chip REIT with a BBB+ credit rating and excellent debt metrics, including a net debt plus preferred stock to Adj EBITDA of 5.4x, a long-term debt to capital ratio of 39.05%, and a fixed charge coverage ratio of 4.8x. Additionally, 99.0% of their debt is fixed rate.

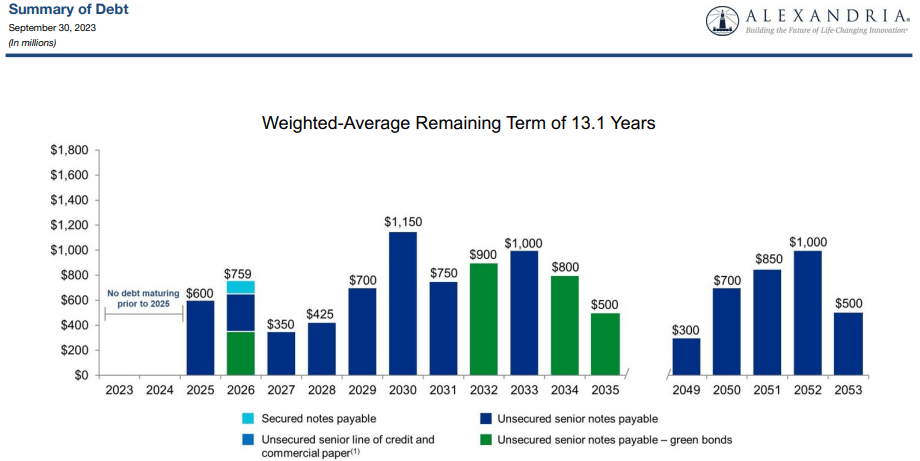

The life science REIT has one of the best debt maturity profiles in the industry with a W.A. term to maturity of 13.1 years, a W.A. interest rate of 3.70%, an enormous amount of liquidity of $5.9 billion (as of 3Q23), and no debt maturities before 2025.

{kind=link}

I don’t see Alexandria facing the same headwind from the work-from-home movement as traditional office REITs, yet its stock price has declined by almost 19% over the past year, even after the significant rally in November and December.

{kind=link}

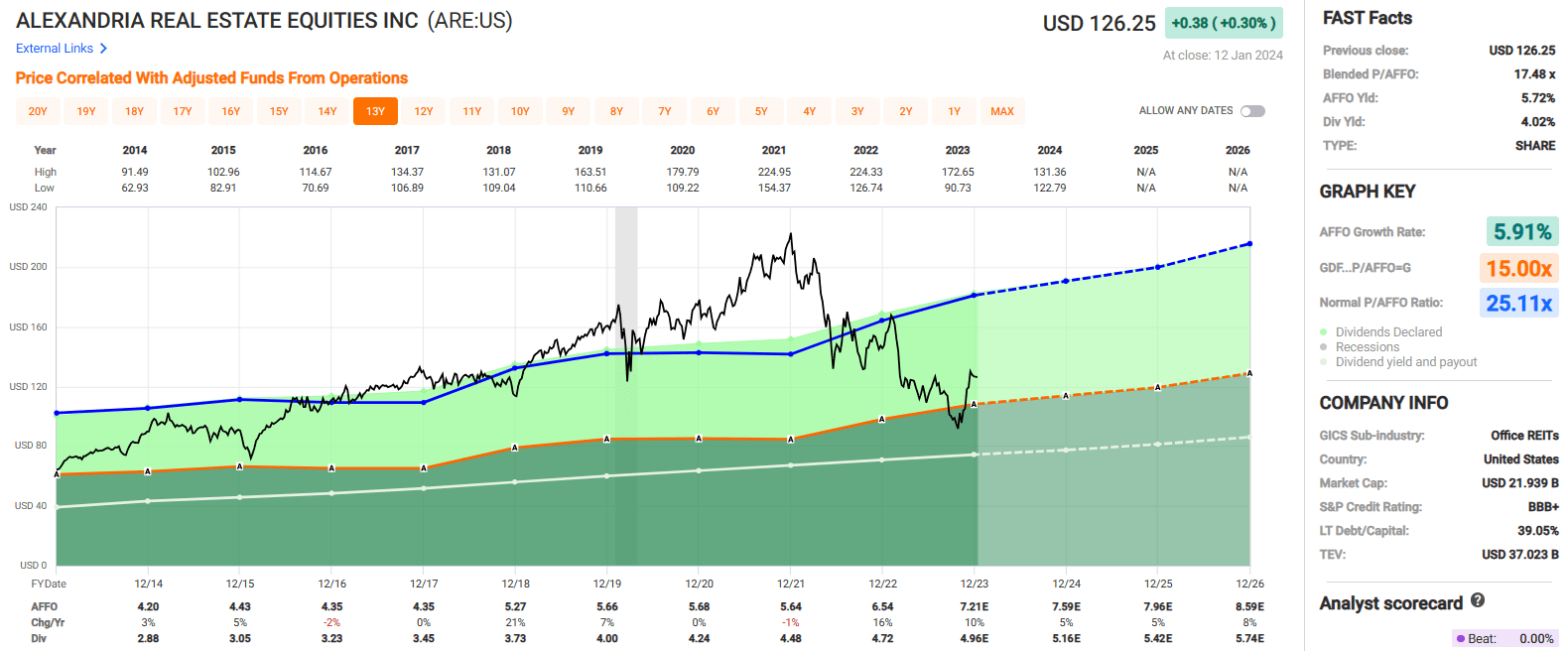

Since 2014, ARE has had an average AFFO growth rate of 5.91% and an average dividend growth rate of 6.64%. Analysts are projecting AFFO per share growth of 5% in both 2024 and 2025, and then for AFFO to increase by 8% in 2026.

The stock pays a 4.02% dividend yield that is well covered, with an AFFO payout ratio of 68.79%. It trades at a P/AFFO of 17.48x, compared to its 10-year average AFFO multiple of 25.11x.

While the stock has rebounded from its October lows, it is still trading at a discount compared to its average multiple and compared to its estimated net asset value of $144.36 per share.

{kind=link}

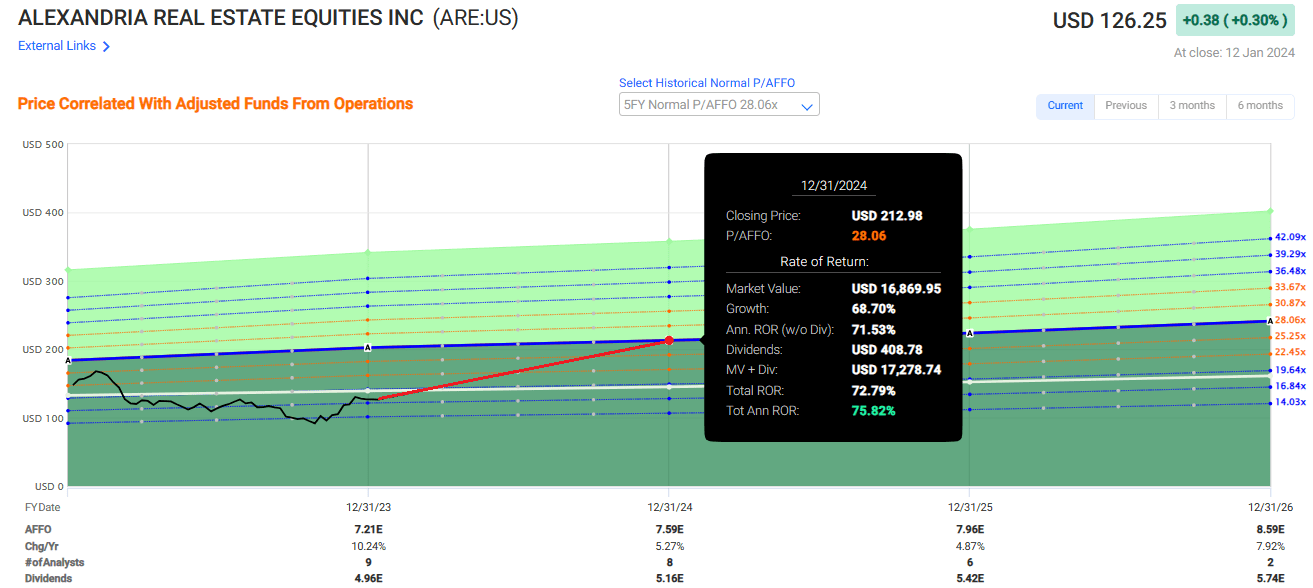

If ARE can trade back up to its 5-year normal AFFO multiple of 28.06x by the end of 2024, it would result in total annual rate of return of 75.82%.

We rate Alexandria Real Estate a Strong Buy.

{kind=link}

Rexford Industrial Realty, Inc. ( REXR )

REXR is an industrial REIT with a market cap of approximately $11.45 billion and a 45.8 million SF portfolio comprised of 373 industrial properties exclusively located throughout infill Southern California (“SoCal”).

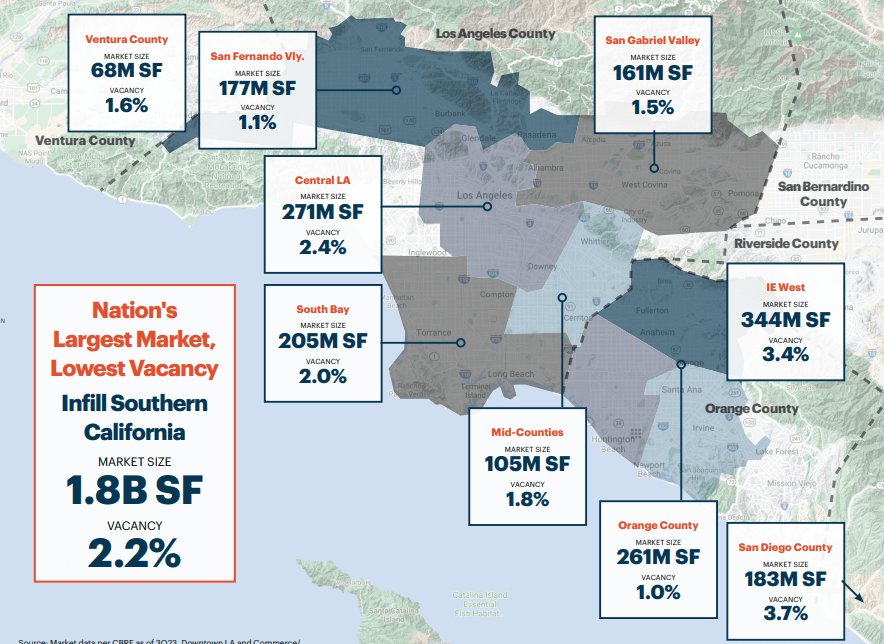

The industrial REIT specializes in acquiring, redeveloping, and managing properties in SoCal, which is the fourth largest industrial market in the world and the highest demand / lowest supply market in the United States.

SoCal is such an attractive market given the size of the economy and the limited supply of land for development. The region is surrounded by natural barriers and the supply of developable land is further constrained by overly burdensome state regulations.

Given the scarcity of supply and vast demand in SoCal, Rexford considers its portfolio irreplaceable and mission-critical for commerce in the region.

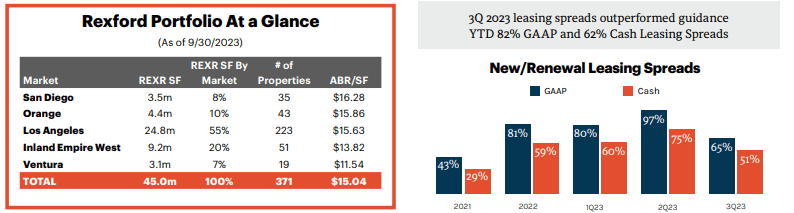

Within SoCal, REXR’s markets include San Diego, Orange, Los Angeles, Inland Empire West, and Ventura. Los Angeles is their largest market with 223 properties covering 24.8 million SF, which represents 55% of the portfolio’s total square footage.

At the end of 3Q23, REXR reported comparable rental rates increased by 64.8% on a GAAP basis and 51.4% on a cash basis, when compared to the prior rents paid.

Additionally, REXR reported a 97.8% average same property portfolio occupancy as of 3Q23.

{kind=link}

Put simply, REXR attempts to dominate the SoCal market with their laser focus on the region.

Instead of spreading their resources and capital across multiple states or countries, they focus exclusively on the top industrial market in the U.S. Or put another way, instead of trying to be a jack of all trades they attempt to become the master of one.

{kind=link}

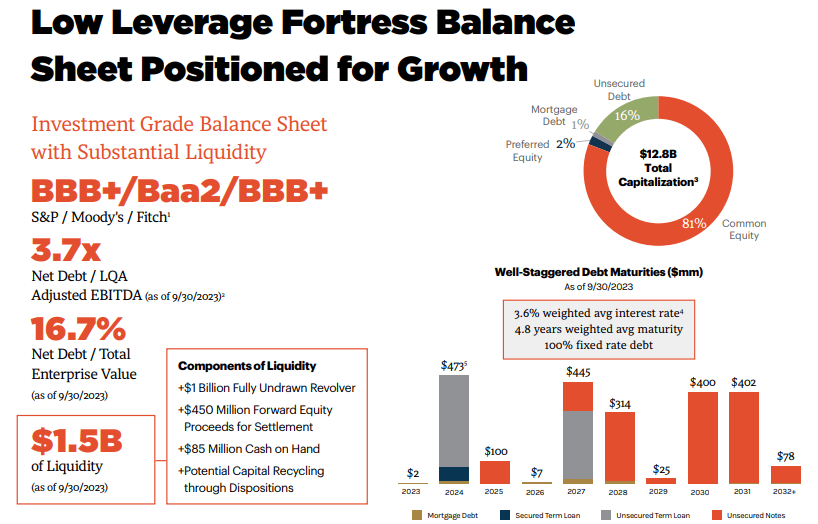

Rexford Industrial has a BBB+ credit rating and a fortress-like balance sheet with a net debt to Adj EBITDA of 3.7x, a long-term debt to capital ratio of 24.23%, and an EBITDA to interest expense ratio of 7.92x.

All of their debt is fixed rate and carries a weighted average interest rate of 3.6% with a weighted average term to maturity of 4.8 years.

At the end of the third quarter , the industrial REIT had $1.5 billion of liquidity and no material debt maturities until 2026, inclusive of their 2024 extension options.

{kind=link}

Since 2016, Rexford Industrial has been a growth machine, with only 1 year of negative growth (2019) and a blended average AFFO growth rate of almost 15% since that time.

Over the next several years AFFO growth is expected to accelerate with AFFO per share projected to increase by 16% in 2024 and then increase by 21% in 2025.

In addition to its impressive AFFO growth, REXR has an average dividend growth rate of 14.87% over the past 8 years.

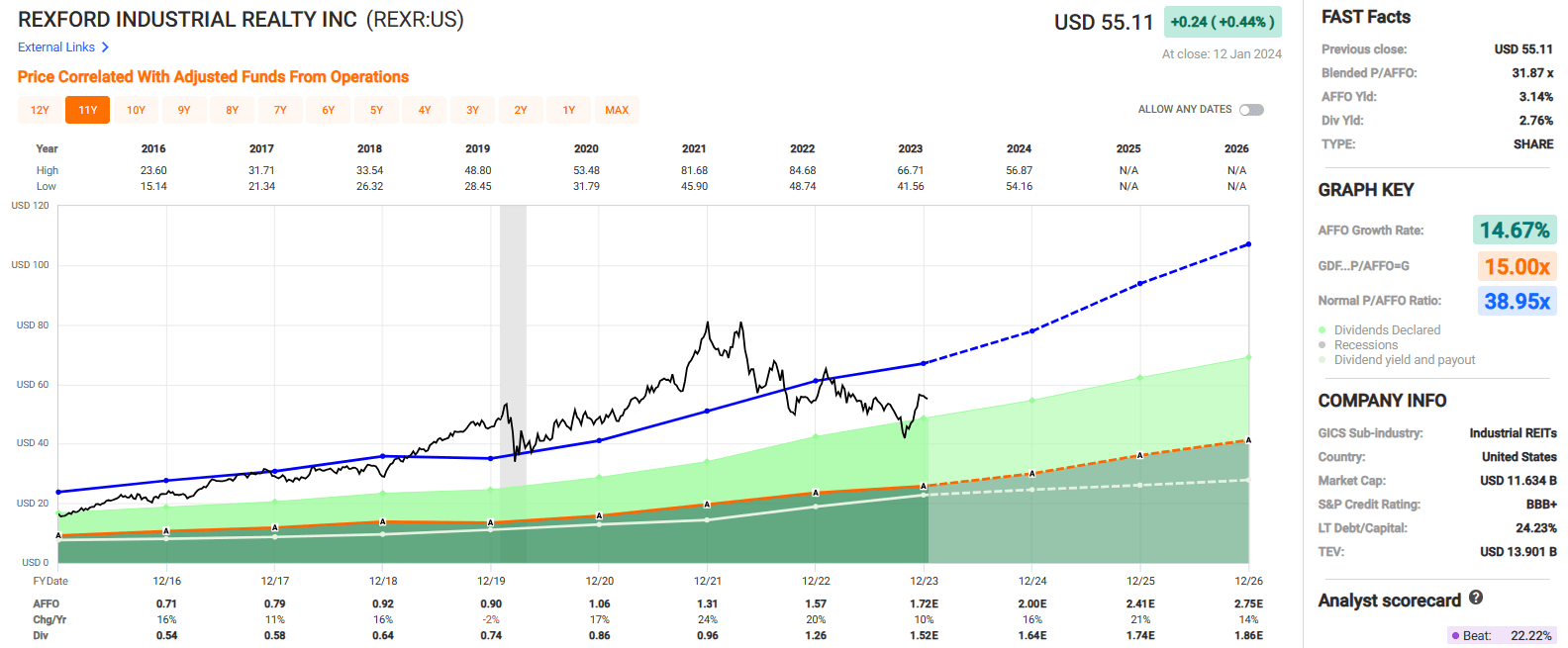

Currently the stock pays a 2.76% dividend yield and trades for a P/AFFO of 31.87x, compared to its average AFFO multiple of 38.95x.

{kind=link}

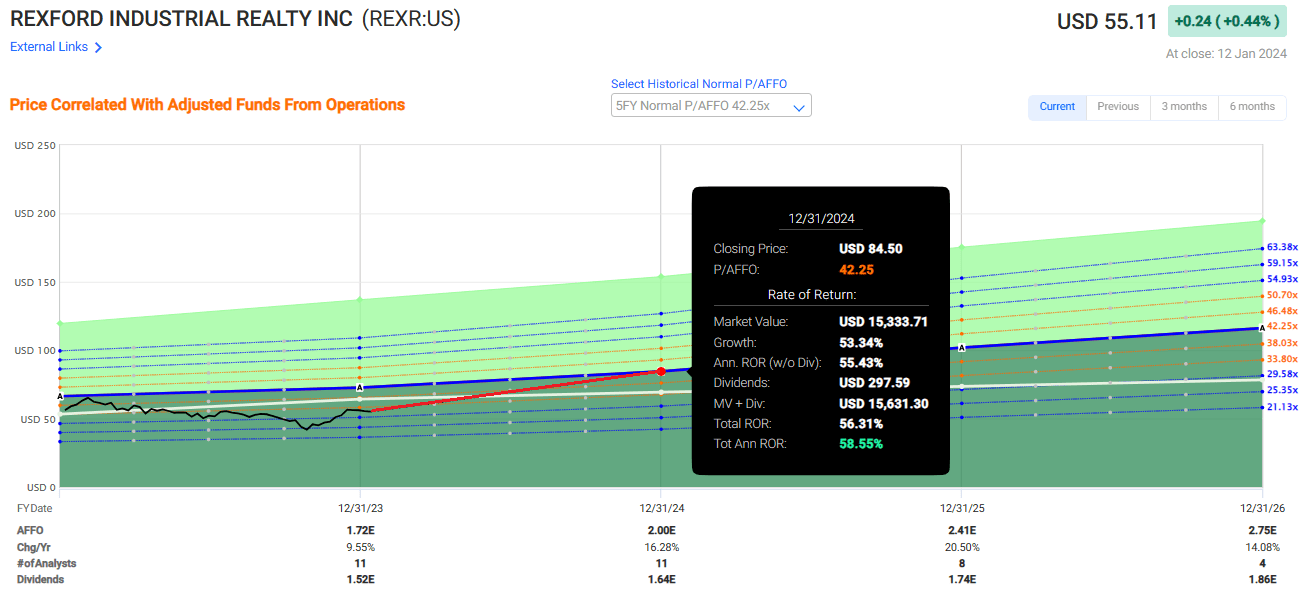

If REXR can trade back up to its 5-year normal AFFO multiple of 42.25x by the end of 2024 it would result in total annual rate of return of 58.55%

We rate Rexford Industrial a Strong Buy.

{kind=link}

In Closing

I own two out of three of these REITs referenced above.

(REXR -1.5% and ARE +8.3%)

I plan to purchase FCPT this week.

I know that it's optimistic to think all three REITs could return 25% on or before my birthday...

However, it's possible...

And whether it's May, June, July, August, or September...

I like the odds that I see.

Just for kicks, I created a portfolio called Brad's Birthday Picks:

Sharesight

It's seeded with $100,000 of "Monopoly" money, and I'll check back in on May 10th to see if these three picks performed above or below expectations.

And now it's time to get back behind the wheel of my loaner car.

Just remember, before you buy anything, always check under the hood!

Happy SWAN Investing!

For further details see:

3 Cheap REITs That Could Return 25% Before My Birthday (In May)