LNC - 3 Companies That Have 100%+ RoR Potential In Less Than 3 Years

2023-06-17 22:25:08 ET

Summary

- The article highlights three undervalued stocks that I believe are great buys in today's market: Teleperformance, Lincoln National, and Alexandria Real Estate.

- I look for companies with good credit ratings, solid fundamentals, good profitability, a good yield for the sector, and a significant conservative upside in case of reversal.

- These three companies offer a combination of undervaluation, quality, upside appeal, and likely growth, making them strong "BUYs" in the current market.

(Author's Note: This article was published on iREIT on Alpha in early June)

Dear subscribers,

I sometimes publish or write an article on a general list of good stocks that I consider to be currently good buys, and got a comment a few days ago that it had been some time since I actually provided an updated list of some of the better buys I see in the market today.

Well, that comment was entirely correct . It has been too long, and the time has come to give you an updated list of 3 great buys in today's market.

Different sectors, different countries, and different types of companies - but all of them are, as I see it, solid enough to invest in at a great upside.

In today's market there's plenty of safety and upside to be had if you know where to look - and even more if you don't have unfavorable FX exposure like I do.

So let's get going.

Undervalued Companies

So, when I look at companies, I generally look for a few common denominators, because undervaluation tends to look fairly similar across most sectors. It's an overreaction to company-specific challenges, real or perceived, that has pushed the share price well below levels that even realistic downturns could justify.

Beyond that, I want:

- Good credit rating, or equivalent credit safe.

- Solid fundamentals and good profitability. I do not invest in unprofitable businesses.

- A good yield for the sector.

- A significant conservative upside in the case of reversal, preferably coupled with market outperformance even if the company underperforms.

If I can find all of the above, then I'm in good shape, and I know my portfolio will be as well.

I use a number of tools and services for screening and also maintain my own lists and checks. I look at hundreds of companies across all continents, which then get boiled down to around 20-30 companies that I currently consider "attractive", by which I mean the more attractive ones currently available on the market.

From those 30, I then sometimes pick 3 to cover - and I pick 1-3 on a continual basis to invest in both my private and my corporate/commercial portfolio.

That, in the coarsest description, is my "process".

So, here are 5 companies that currently stand out to me in a non-trivial manner as undervalued, above-quality businesses.

1. Teleperformance ( OTCPK:TLPFY )

Yeah, I'll keep harping on this company quite a bit until I am sure that everyone has at least heard of it. It represents a significant investment allocation for me over the course of the past 1-2 months. I love this absolutely contrarian type of investing that this company and businesses like it allow me to do.

Teleperformance is, simply put, one of the most undervalued businesses in the entire communications sector. It's not a market leader, but it's a marker outperformed , significantly outperforming the profitability of most companies in its relevant sector.

The company provides what the market calls "outsourced customer experience management services" - this is a fancier way of saying that the company essentially is a call center operator. It offers care solutions, technical support, acquisition services, digital solutions, analytics, and specialized services aside from its core segments, such as Visa management, debt collection services, interpreting and translation services, and back-office services.

The company employs over 400,000 people across the world.

Teleperformance IR (Teleperformance IR)

It's by far the #1 leader in outsourcing for customer and citizen experience. Over 50% of the company's workforce works from home. The company employs people from 91 countries, works in over 300 languages for nearly 1,200 clients ranging from megacorps to smaller businesses, and they operate in over 170 markets.

The company, at current yield levels, has over 2.5% yield paid out on an annual basis. That this does not excite you in a communications business is perfectly understandable.

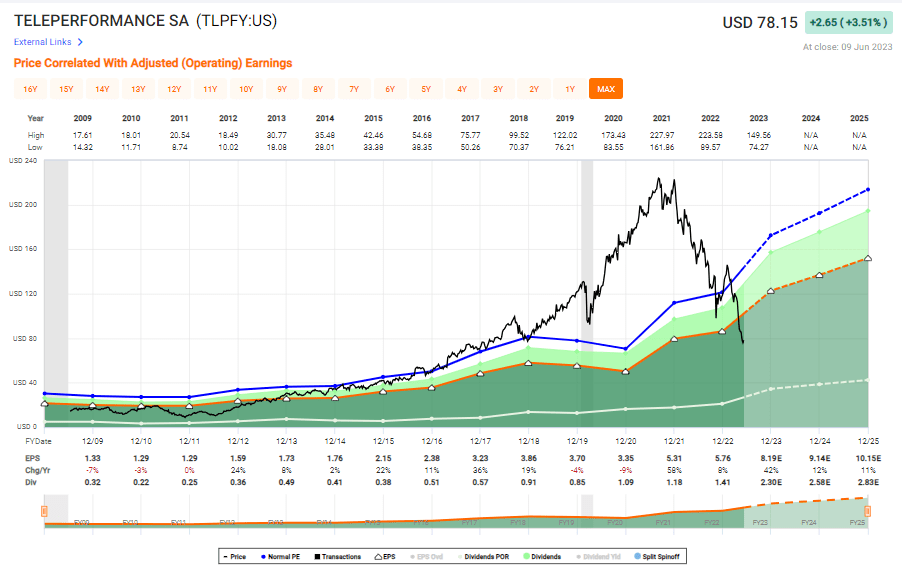

What should excite you is the company's record of profitability over time, illustrated well in this fashion.

{kind=link}

Teleperformance valuation (F.A.S.T Graphs)

Teleperformance averages EPS growth in the 12-14% per year, and there is zero indication that its growth going forward is in any way slowing down. In fact, the company recently added more capabilities to its portfolio through the purchase of Majorel, part of why the stock is down.

Teleperformance is a BBB-rated company with a market cap of around €9B, though it has been far higher. I would never buy the company above its 20-year average, but it's currently trading at 11.45x - less than half of its historical premium. And there is, as I see it, no justifiable reason for this extreme of a drop.

Teleperformance has a high analyst accuracy when it comes to forecasts, and forecasted at 15x P/E, this company has the potential to RoR triple digits. That's on a 15x P/e when it would generate 34% per year based on a 2025E of €10.15/share adjusted EPS, and a yield that's twice the current level.

If we consider premiums valid, which we should - at least 18-22x, for the long term given a forecasted growth rate of almost 20% per year until 2025E, then we find potential RoR of over 200% at 22x P/E normalized from today's share price. And I want to point out to you, that the company traded at PEs of 30-40x only a few short years ago.

The potential upside here just in the case of fair-value is superb - and the company's services and demands aren't going anywhere. The company has low debt, less than 36% to capital, and I expect it to massively outperform.

Current S&P Global analyst targets? 16 analysts between €146 to €380, a massive spread, ending at an average target of €295, with 12 out of 16 analysts at a "BUY". I add my voice to that choir and say that Teleperformance is a massive "BUY" with a PT of at least €250/share long-term.

That's number 1.

I own over 1% of both my portfolios in Teleperformance.

2. Lincoln National ( LNC )

Lincoln National has been a hell of a ride, and there's nothing to say it's over yet. In my private portfolio, I went in too early - and I'm in the red still. In my commercial portfolio, I've fared a lot better, and at a $23/share price, I'm in good shape to see good returns here already.

But this is nothing compared to what the company could deliver when, or if it normalizes.

Many people that follow LNC forget that the company is a:

- Well-run, conservative business.

- BBB+ rated

- While it has seen decline, no fundamental long-term danger seems likely at this time.

The company seems to have found its bottom at the $20/share level, at least for the time being. From here on out, it's a question of how quickly it can recover investor confidence.

I would consider it fair with respect to my own background, skills, and proven track record to be fairly knowledgeable when it comes to insurance businesses.

Whenever a company in this sector holds a fair bit of risk on its balance sheet, there are always assumptions for how this risk is calculated and how this impacts it from a capital perspective. This is why, no matter how great the company is, I never go above a 4-5% holding size - not even in world-class companies like Allianz ( OTCPK:ALIZY ) and Munich RE ( OTCPK:MURGY ). That's the first thing, and this applies to LNC as well.

My own M.O. in the case of an investment like this, or like Unum ( UNM ) - more on that in a second - is that my position, lest there are significant and fundamental dangers to the underlying business, is kept and given time to recover and outperform. I have not identified significant or fundamental long-term dangers to LNC's finances or balance sheet.

For Unum, the closest similar company, it was a trip starting at below $20/share, to where is now trades at over $45.5/share. My rating on Unum is a "HOLD" today, but I can tell you, as I've said before, that I made an absolute fortune on that investment due to the exact same strategy I'm employing here with LNC. Also, my theses and stances can be traced here on Seeking Alpha.

There is a general lack of understanding for insurance businesses here on Seeking Alpha. This is not surprising, because insurance businesses are not easily-understood entities. They are often compared to banks, but this is not relevant. Insurance companies are far less vulnerable to risks faced by banks, because they match liabilities and assets far better, making "runs" on the companies is unlikely - and even impossible. Sudden liquidity needs for insurers, especially in P&C, w hich is most exposed due to their climate/natural disaster exposures , are in turn matched with reinsurance protection.

Any sort of insurance liquidity crunch , even though finance is being punished, in this sector is extremely unlikely, as I see it. You can't compare asset/liability matching in the two industries.

Higher interest rates mean higher reinvestments in bond portfolios and as long as they can sit out those losses, which they typically can because there is no scenario where an immediate need for capital in the business is apparent, there really isn't an issue. Also - insurance bond portfolios tend to be much shorter durations than banks on average.

So - my suggestion would be to focus on the longer term - as I do.

And longer term, current forecasts call for LNC to be able to make $7/share worth of adjusted EPS this year, and around $9.4/share in 2025E. Based on previous normalized P/E, and only putting the company at a 9x P/E to that result, gives us an upside of 70% per year, or 285% RoR , implying a share price of above $80/share.

Triple-digit RoR is possible with as low as a 4.5-5x P/E normalized - and if you don't believe that a BBB+ rated insurer with excellent management will manage that then...well, I guess we'll wait and see what happens. But I am heavily invested in LNC, and happily adding more.

That's number 2.

I own over 1% of both my portfolios in Lincoln National.

3. Alexandria Real Estate ( ARE )

I thought long and hard about which company to make number 3 - there were a number of options possible. In the end, I elected to go for Alexandria Real Estate. It's not the highest upside that's possible, but it couples a severely undervalued company and sector with a good safety of BBB+, a good yield of 4%, and that triple-digit upside that I spoke of.

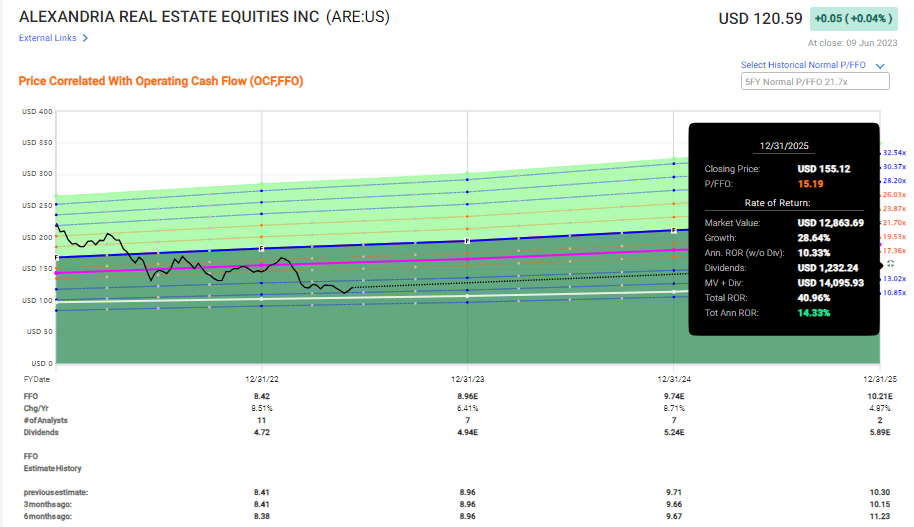

Even on the basis of a 15x P/E upside on FFO, Alexandria, with a market cap of over $20B, will outperform the average with a 14.3% annualized RoR, or 41% until 2025E.

{kind=link}

Alexandria Real Estate Upside (F.A.S.T graphs)

ARE is neither the highest-yielding nor the lowest-trading Office REIT in terms of multiples, FFO, or otherwise. Boston Properties ( BXP ), Highwoods ( HIW ), and Kilroy ( KRC ) which are all BBB-rated or above are all at significantly higher yields, at significantly lower valuations, and upsides that are comparable to this one. I own all of them - so if you want a higher upside, and know that you want someone with skin in the game on them, well, I own all of those as well, and I'm bullish on them.

Unlike other Office REITs, Alexandria focuses on a subsection of properties and developments which by many investors are considered to be higher quality overall compared to what else is available. ARE is one of the highest-rated REITs out there.

Alexandria has offered, despite its lower yield compared to the current sector average, one of the best total shareholder returns in the entire REIT sector. Since its original IPO in the late '90s, the company has delivered shareholder returns of above 1,500%, which is not only better than Walmart ( WMT ), it's better than Buffett's Berkshire ( BRK.B ), and being a better investor or capital allocator than Buffett is not an easy claim to make - but if you had invested in ARE, you could technically have said so, given that you outperformed.

It's also wrong to call ARE a strict "Office REIT". Yes, they have offices, but their properties are far more specialized, offering mission-critical qualities and assets that their tenants cannot be without or "work-from-home" in.

Instead of calling ARE an office REIT, we might want to call it a "Healthcare/Pharma REIT", which is somewhat weird, but also more accurate.

Alexandria Real Estate IR (Alexandria Real Estate IR)

Alexandria has also seen a near-zero rent collection impairment and occupancy issues, making it a shining beacon in this sector - also in terms of tenants and ABR.

ARE IR (ARE IR)

You know how investors say that "next time the market crashes, I'm going to invest so much in quality companies".

Well, the market is crashing - and most of the investors I speak to seem to be caught between seeing where the market "ends up", i.e. market timing, or running and hiding to keep from seeing their portfolio fall. Some of the people I know have gone to 80% cash-in-deposit accounts, which is the same as watching 6-11% of your purchasing power disappear due to inflation.

ARE has superb upside even in the case of a near-bearish case. However, I view Alexandria as likely to significantly outperform over time, not just 13-14% per year, but delivering that triple-digit RoR until 2025E, which it would at around 20x P/FFO or slightly above, depending on growth.

S&P Global targets for Alexandria come in between $140 on the low side and $190 on the high side. Out of 9 analysts, all 9 are at "BUY" or "Outperform" in terms of targets, with an average PT of $166/share. My own price target mirrors this very closely, at around $165/share.

There isn't a single perspective or argument that I can see, that you can make a valid argument that this company will not produce positive returns going forward. It would take something massively detrimental, something truly cataclysmic to change this company from a "BUY" to something else at this point.

There is, simply put, too much safety included in this company at this time. The discount is high - higher than it has been in close to a decade here.

That is why I am adding to my own position of ARE, lowering my cost basis, and improving my yield.

Wrapping up

These are the current 3 companies that I consider to have a combination of undervaluation, quality, upside appeal, and likely growth to make them some of my strongest "BUYs" here. They're not the entirety of my "BUYs" at this time, but they are companies that I myself have been adding to over the past 2 weeks, and have frequently bought shares in as they have dropped/declined.

So when someone is asking me, what he/she should be buying - I would say to take a look at these three companies and see if any of them meet your requirements or pique your interest.

Because if you're anything resembling a valuation-conscious investor, then they should at the very least interest you.

Questions?

Let me know!

For further details see:

3 Companies That Have 100%+ RoR Potential In Less Than 3 Years