PRNDY - 3 Consumer Staple Picks For A Potential 2023 Earnings Recession

Summary

- Fear of a 2023 earnings recession grows. According to Morgan Stanley’s chief equity strategist and many Wall Street analysts, stocks may experience some of their worst performance since 2008.

- For investors concerned about market performance in 2023, there may be an opportunity to buy defensive stocks to protect your portfolio if the markets retract.

- YTD, many of the unloved sectors of 2022, like Communications, Tech, and Discretionary, have rebounded sharply, and defensive sectors have sold off.

- The recent rally has been sparked by past peak inflation, investor sentiment, and speculation that Fed hikes will be reduced. The demand for essentials like food and beverages makes consumer staples an opportunity to prepare for market swings and a decline in 2023 earnings.

- The three consumer staples stocks featured here are intended to put your money to work. Their fundamentals, attractive valuations, and solid earnings are driving catalysts in outperforming inflationary levels and stand to benefit from an earnings recession based on our quant ratings.

Preparing for an earnings recession?

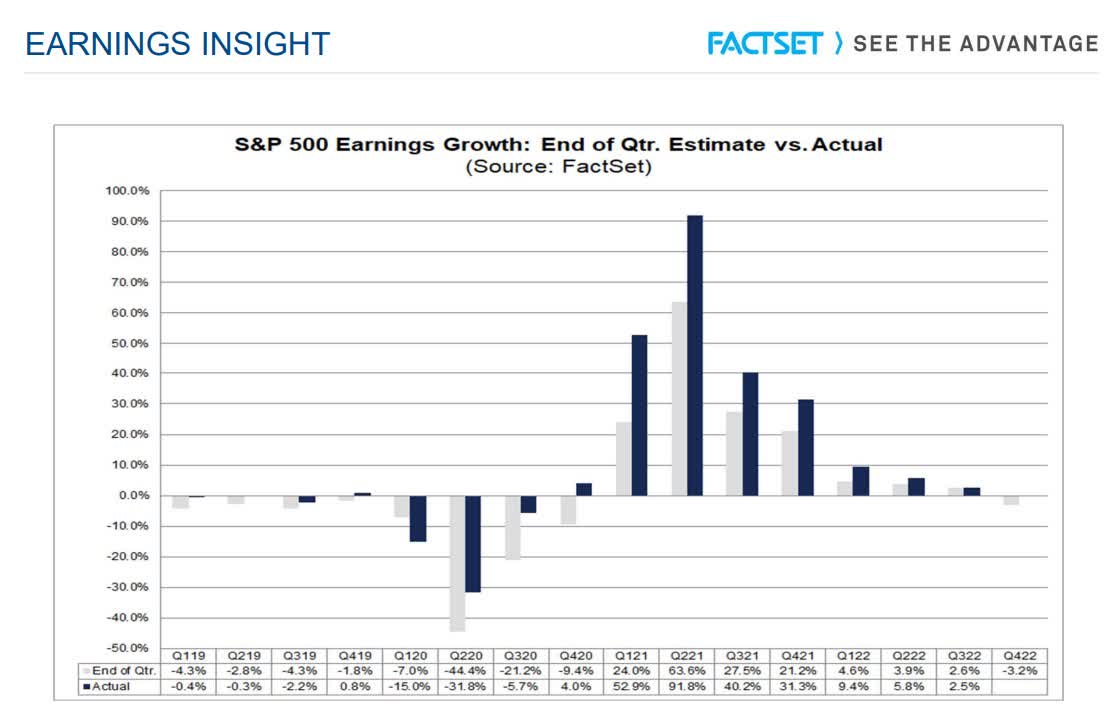

According to a January 13th FactSet Earnings Insights , the fourth quarter of 2022 is expected to have its first year-over-year decline since Q3 of 2020 (-5.7%). The estimated S&P 500 earnings decline increased by 0.7%, from -3.2% to -3.9%. This shows that the 29 companies that reported actual Q4 2022 earnings through January 13 have exceeded estimates by 7.7%, and EPS surprises closer to their five-year averages.

{kind=link}

Several analysts anticipate a weaker year for earnings in 2023. Morgan Stanley Chief Equity Strategist Mike Wilson thinks the market hasn’t fully priced in the magnitude of earnings contractions for Q1 of 2023. He believes Americans are in store for the largest earnings surprise since 2008, which includes contributing factors like

-

High inflation compared to recent historical averages (over the past 10 years, averaged ~2%.) versus 2022, which experienced an annual inflation rate of 8%.

-

The increased cost of labor exacerbated by…

-

Tight labor market - The Jolts Report does not reflect actual openings, and many companies forget to remove postings or keep them open.

As a result of the factor affecting bullet point #3, the figures for the latest job openings tend to be inflated, as even the figures for layoffs are skewed by approximately six weeks. And although job openings are abundant compared to the number of job seekers, employees are demanding more compensation than employers are willing to pay, given the cost of living adjustments and experiences post-COVID. These factors can affect earnings, so it's imperative to find companies that can easily pass price increases to consumers.

Consumer Staples is relatively inelastic, meaning regardless of economic conditions, they tend to be less volatile, and demand remains the same regardless of price. As we’ve experienced over the last couple of years – especially regarding food – when the price of a good or service increases, consumers’ buying habits stay about the same. When the price goes down, consumers’ buying habits also remain unchanged. It’s important to identify companies that are inelastic. Sin stocks like alcohol and tobacco tend to offer recession resiliency, as people embrace or enjoy “sin products” in good times and bad. With an earnings recession likely, the ability to maintain margins can benefit shareholders. So let’s cheers to three beverage companies offering strong fundamentals in consumer staples capitalizing on the surge in prices.

Top Recession-Resilient Stocks

To end 2022, consumer staple stocks were among the third best performing, as showcased in the chart below, offering essential products like food, beverage, and hygiene. Considered necessity products, the sector will likely remain resilient during a recession, which is anticipated for 2023.

S&P 500 Sectors Performance (thru 12/27/22) (Standard & Poor's, Yardeni Research)

Although the Consumer Staples sector ( XLP ) is down 2.59% YTD, it reflects a rotation from investors into the sectors that underperformed in 2022. The reality is that Consumer Staple companies have shown as costs for products and services continue to increase, the sector is successfully pushing costs onto consumers without a significant drop-off in sales and revenues. For example, we’ve seen this occur with eggs, poultry, and many other items. Let’s toast to the new year and three consumer staples for a 2023 earnings recession.

1. Coca-Cola FEMSA, S.A.B. de C.V. ( KOF )

-

Market Capitalization: $14.88B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 1/22/23): 14 out of 193

-

Quant Industry Ranking (as of 1/22/23): 2 out of 17

Coca-Cola FEMSA is a Mexico-city-based bottler, producer, and distributor of Coca-Cola trademark beverages. I have personally visited this facility, which is a very impressive bottling operation. As the world knows, Coca-Cola is a popular soft drink, and household staple, the beverage not only comes at an affordable price but the stock is also discounted and has bullish momentum.

Coca-Cola Stock Valuation & Momentum

Significantly outperforming its sector median peers quarterly, KOF is on a longer-term uptrend. Shares are trading above the 10- and 200-day moving average, showcasing a remarkable +4,691% difference to the sector for its six-month price performance.

KOF Stock Momentum Grade (SA Premium)

Over the last year, the stock is +33%, trading near its 52-week high of $72.99 per share. The stock comes at a solid valuation amid rising food costs and continued demand for the popular drink. Possessing a B- overall valuation grade, the stock not only maintains a 17.61x forward P/E, a near -15% difference to the sector, but the company also has a forward PEG ratio, -34.45% difference to the sector, an indication this stock is undervalued. Trading at $70.81 per share, KOF is capturing the rise in food prices, and its overall metrics have seen improvements since the pandemic. You can also see EPS figures have improved with growth and profitability.

KOF Stock Growth & Profitability

KOF maintains strong financials and momentum that has allowed it to expand across Latin American countries, highlighted by strong financials and the latest earnings results. With an EPS of $1.04 beating by $0.16 and revenue of $2.86B beating by $128.31M, a near 20% increase year-over-year, Mexico’s largest coke bottling firm continues to outperform. Q3 volumes are up 12.1% compared to Q3 2019, and gross profit increased by 16.4%.

“Driven by our affordability capabilities and relentless point of sale execution, we continue gaining share across markets and categories…with slight inflationary pressures, we continue leveraging initiatives to drive single-serve mixed growth. We remain on track to reach our ambitious single-served mix for the year that more than 65% of our volume growth coming from single-serviced presentation,” John Santa Maria , Coca-Cola FEMSA Chief Executive Officer.

In addition to strong financial performance, KOF boasts a solid dividend scorecard , which includes a 3.91% forward dividend yield and 18 years of consecutive dividend payments.

KOF Stock Profitability Grade (SA Premium)

With increasing prices, excellent EBIT margins as highlighted above, and cash from operations at $1.57B, Coca-Cola FEMSA is on solid footing to capitalize on the tailwinds supported by an inelastic industry. When you factor in that the Biden Administration recently announced restoring relations between the U.S. and Venezuela , as highlighted by SA contributor Ian Bezek, this may be a major opportunity for KOF, whose analysts believe this stock is a strong buy, given the five FY1 Up revisions in the last 90 days. But if you’re not sold on this beverage, perhaps you’ll toast to my next two.

2. Heineken N.V. ( HEINY )

-

Market Capitalization: $56.72B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 1/22/23): 12 out of 193

-

Quant Industry Ranking (as of 1/22/23): 1 out of 8

Global beer brewer Heineken N.V. is a well-known seller of beer and cider, offering products to retailers, bars, and chains around the globe. Founded in 1864, the Amsterdam, Netherlands-based company is currently ranked #1 in its industry according to our quant ratings and #12 out of 193 in its sector. Their facility in Amsterdam offers a great tour of the factor and beer tasting experience. I can state first hand the quality of the beer at the plant is excellent, and it is a fun experience.

HEINY Stock Valuation & Momentum

This particular Consumer Staples stock has not experienced a pullback this year, as the sector has. Although the company’s D+ valuation is not ideal, Heineken stands to remain resilient with pricing power to offset the inflationary increases, given its industry, and as people drink beer, whether their financial situation is good or bad. Despite an overall D+ grade, HEINY’s PEG ((TTM)) is an A+, showcasing a 0.07x ratio, nearly a -90% difference to the sector, and its momentum is strong.

HEINY Stock Momentum Grade (SA Premium)

HEINY shares remain on an upwards-sloping 200-day moving average. YTD, the stock is +5% and, as showcased in the below momentum grades, outperforms its sector median peers’ quarterly. Despite shares of Heineken down nearly 12% over the last year, Deutsche Bank stated , "We believe the recent de-rating of Heineken relative to both brewing peers and European Staples leaves Heineken undervalued with the shares trading at a CY23 P/E of 16.6x (a 20% discount to European Staples) and offering an FCF yield of c. 5.0%." RBC is also bullish on brewers, citing price growth and improved operational performance. This upgrade to Heineken , along with its solid growth and tremendous profitability, indicates why this stock is a solid pick coming into the new year.

Heineken Stock Growth & Profitability

After flexing its pricing power that showcased consumers unwilling to cut out beer despite price increases, Heineken’s earnings showed a 37% increase through June 2022, plus an increase of 20.6% in operating profits. CEO Dolf van der Brink said,

“We benefited from the recovery in Asia Pacific and the on-trade in Europe as consumers returned to the bars, with demand resilient until now despite mounting inflationary pressures on consumers' disposable income. Our actions on pricing, revenue management, and productivity offset significant inflationary pressures in our cost base. As a result, operating profit is now firmly ahead of 2019.”

HEINY Profitability Grade (SA Premium)

With organic net revenue growth of 24.3% and volume growth as a result of expansion throughout the Americas, Heineken’s portfolio and customer base continues to grow. Heineken 0.0 is now the #1 nonalcohol beer in Brazil, Mexico, and the U.S., and digital sales exhibited exponential growth, with more than 6x from 2021, and Vietnam as the fastest growing. With healthy cash from operations and 25 million Heineken’s served daily across 192 countries, consider adding this staple to your fridge and portfolio.

3. Pernod Ricard SA ( PRNDY )

-

Market Capitalization: $54.05B

-

Quant Rating: Strong Buy

-

Quant Sector Ranking (as of 1/22/23): 11 out of 193

-

Quant Industry Ranking (as of 1/22/23): 1 out of 10

Suppose soda or beer isn't your thing, or you consider your pallet more refined. In that case, Paris, France producer and seller of wines and spirits, Pernod Ricard SA offers whisky, vodka, tequila, gin, rum, and an assortment of liqueur and bitters. As with our previous beverage stock, this “sin stock” will likely remain resilient whether we experience a 2023 recession or not; people drink in good and bad times. YTD, the stock is up 7.74%. Like Heineken, PRNDY’s valuation is not ideal and requires some prudence when investing at its current price point of $41.69 per share, which is near its 52-week high of $45.04.

PRNDY Stock Valuation & Momentum

With a D valuation grade , PRNDY has undemanding PEG ratios with more than a -25% difference from its sector median peers, coupled with solid growth and profitability metrics to indicate potential upside in the new year. JP Research also wrote an article titled Pernod Ricard: Quality Spirits Company Trading At An Undemanding Valuation. Momentum remains strong, offering an overall B+ grade, with quarterly price performance outperforming its sector peers. PRNDY has outperformed its sector peers for the six-month period by 1,666%.

PRNDY Momentum Grade (SA Premium)

In addition to PRNDY’s outstanding global performance, it offers a portfolio of premium alcohol brands and consecutive top-and-bottom-line earnings beats.

PRNDY Stock Growth & Profitability

With diversified offerings, PRNDY products have experienced strong growth and record operation margins of €28.3 (USD ~$31B) with an expansion of 80 basis points or 52 basis points on an organic basis. Additionally, Pernod’s specialty brand portfolio doubled post-pandemic. With record cash generation, the company has its highest-ever free cash flow at €1.8 billion (USD ~$2B) and net debt-to-EBITDA ratio at 2.4%.

“We are investing in the future growth of our business with increased strategic investments and all these results allow us to accelerate the returns to our shareholders with a strong dividend growth of plus 32% versus last year. And the announcement of a new share buyback program of roughly €500 million to €700 million for this fiscal year.”

PRNDY Stock Profitability Grade (SA Premium)

Despite inflation taking a toll on many stocks, alcoholic beverages are a popular necessity for many consumers, and given the increased volumes these beverages are produced, Pernod continues to expand. Not only did it increase its minority stake in Sovereign Brands , but Pernod also acquired a majority stake in Código 1530 tequila , an indication that investors may want to consider taking a shot of this stock, as well as my other quant-rated strong buys.

Cheers to 3 Top Beverage Stocks in the face of a Potential Earnings Recession

While an official recession in 2022 was never declared, surging inflation and the Fed’s hawkish stance are projected by many strategists and economists to push the economy into a recession in 2023. In preparing for a slowdown, as we’re already experiencing, consumer staples offer the necessary products that can serve as a defense during periods of downturn, offering recession-resilient qualities for a portfolio.

The three recommendations, KOF, PRNDY, and HEINY are all quant-rated strong buys and possess great outlooks and collective characteristics, with tailwinds for continued profitability, momentum, and growth. Where economists and analysts are predicting an earnings recession in the first part of 2023, key strategist Mike Wilson believes the markets will bottom in early 2023 but also predicts that the S&P 500 will rebound to 3900 in the second half of the year. To endure the volatility and potentially capitalize, consider using Seeking Alpha's 'Ratings Screener' tool to help you find defensive stocks that achieve diversification into desired sectors you like, including Top Consumer Staple Stocks .

For further details see:

3 Consumer Staple Picks For A Potential 2023 Earnings Recession