PYPL - 3 Dividend Growth Stocks To Buy In January 2023

Summary

- Dividend growth stocks can contribute significantly to increasing your additional income in the form of dividends year over year.

- In this article I will present 3 companies that I currently consider to be attractive, particularly due to their strong competitive advantages and current valuation.

- Each company has shown a relatively high Average Dividend Growth Rate over the past 5 years and has a relatively low Payout Ratio.

Investment Thesis

Dividend growth companies are important for the long-term success of your investment portfolio, since they can contribute significantly to increasing the dividends that you receive from the companies you are invested in.

Building an investment portfolio that, on the one hand, offers an attractive Dividend Yield and, on the other, provides you with Dividend Growth, helps you to be more independent from price fluctuations on the stock market. At the same time, such an investment portfolio can provide you with an enormous amount of extra income, especially when investing with a long investment-horizon.

Before I present the three Dividend Growth companies that I’ve selected for today’s article, I would like to mention the pillars of my investment approach ; when building an investment portfolio, I aim to reach a balanced mix between the following factors:

- Relatively high Average Dividend Yield of the companies

- Relatively high Average Dividend Growth Rate

- Attractiveness in terms of risk and reward

- Companies with strong competitive advantages that provide an economic moat

- Companies with strong financials

- Companies with a relatively high brand value

- Consumer familiarity with the products of these companies

- Attractive Valuation of the companies

- Aiming to achieve a relatively high Yield on Cost when having a long investment horizon

- Risk diversification across sectors and industries.

In today’s article, however, the focus will be only on dividend growth companies. The three dividend growth companies that I have selected for you and which I consider to be particularly attractive to buy this month, share the following characteristics:

- Low risk of insolvency

- Strong competitive advantages (such as a strong brand image)

- High economic moat

- Attractive Valuation

- Relatively high Dividend Growth Rate over the past 5 Years

- Relatively high expected Dividend Growth Rate for the following years

- Relatively low Payout Ratio.

From my point of view, fulfilling these characteristics makes the companies attractive dividend growth picks.

The 3 companies I have selected for you:

Bank of America

When I analyze and select companies for you that I consider to be worth investing in, I put a lot of emphasis on making sure that each one has strong competitive advantages and a wide economic moat, so as to help you not lose money as an investor. One of these companies that ticks all of these boxes is Bank of America.

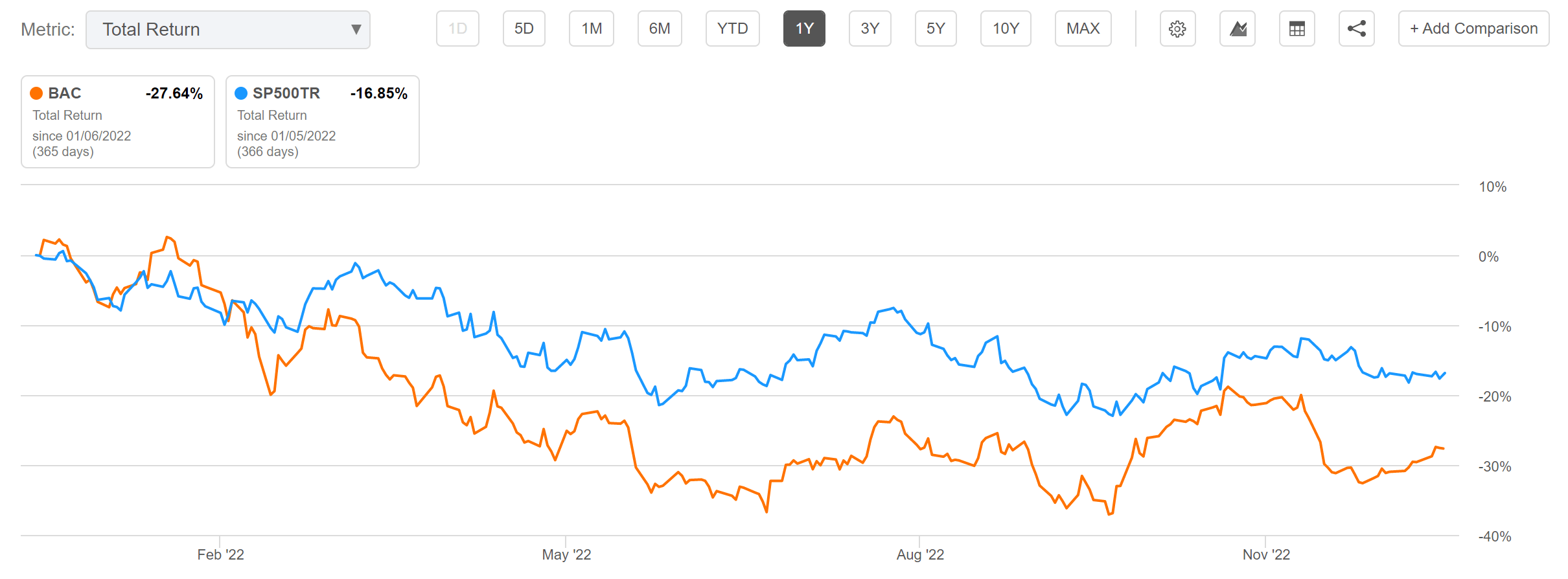

However, within the past 12 months, the U.S. bank has shown a Total Return which is significantly lower than the one of the S&P 500: while the S&P 500 has shown a Total Return of -16.85%, Bank of America has produced one of -27.64% over the same period (see the graphic below).

{kind=link}

Bank of America’s weak performance over the past 12 months has contributed to the fact that I currently consider it to be attractive in terms of Valuation: the bank has a P/E [FWD] Ratio of 10.83. The current valuation is 11.68% below its 5 Year Average P/E [FWD] Ratio (12.27), indicating that it is undervalued at this moment in time.

Bank of America’s Dividend Growth Rate [CAGR] over the past 3 years is 9.22% and its Dividend Growth Rate [CAGR] over the past 5 years is even higher (17.14%). Both Growth Rates are significantly above the one of competitors such as Wells Fargo (NYSE: WFC ) (3 Year Dividend Growth Rate [CAGR] of -16.95% and 5 Year Dividend Growth Rate [CAGR] of -6.51%), Citigroup (NYSE: C ) (2.04% and 16.27%) and JPMorgan (NYSE: JPM ) (5.57% and 13.54%). These are strong indicators that Bank of America is an excellent pick for investors seeking Dividend Growth.

However, you should take into account that it currently has a Dividend Yield [FWD] of 2.58%, which is below its competitors Wells Fargo (Dividend Yield [FWD] of 2.83%), Citigroup (4.36%) and JPMorgan (2.96%). So, in the case that you are looking for a U.S. bank that can already provide you with a higher Dividend Income, you should instead take a closer look at one of the mentioned competitors.

Furthermore, Bank of America has a relatively low Payout Ratio of only 26.90%. The Payout Ratio is an important metric that I look at when analyzing companies, mainly to filter out the ones that are able to pay a sustainable dividend and for which I consider the risk of a dividend cut to be low. Bank of America’s low Payout Ratio provides us with additional evidence that the bank should be able to continue raising its dividend in the years ahead.

Visa

I believe that Visa is an excellent choice in terms of risk/reward and I still see plenty of growth potential in the years to come. Visa’s high EBIT Margin of 67.42% is a clear indicator of the company's outstanding competitive position as well as its strong competitive advantages.

Given the company's current valuation, I currently see an attractive entry point for buying the stock: Visa's P/E [FWD] Ratio is 25.80, which is 20.36% below its Average P/E Ratio over the last 5 years (32.40), highlighting that the company is undervalued at this moment in time.

In addition to the above, and when comparing to Mastercard (NYSE: MA ), Visa seems to be the slightly more attractive choice in terms of Valuation: Mastercard currently has a P/E [FWD] Ratio of 34.62, which is significantly higher than Visa’s Valuation. When comparing Visa to PayPal (NASDAQ: PYPL ), I come to the same conclusion: with a P/E [FWD] Ratio of 35.94, PayPal’s Valuation is significantly higher. Furthermore, Visa has shown a higher Revenue Growth Rate [FWD] than its rival (13.84% compared to 12.28%).

Moreover, Visa currently has a Free Cash Flow [TTM] of 4.06%. I consider this Free Cash Flow Rate to be very attractive, especially when considering that the company has shown an Average Free Cash Flow Per Share Growth Rate [FWD] of 16.78% over the past 5 years.

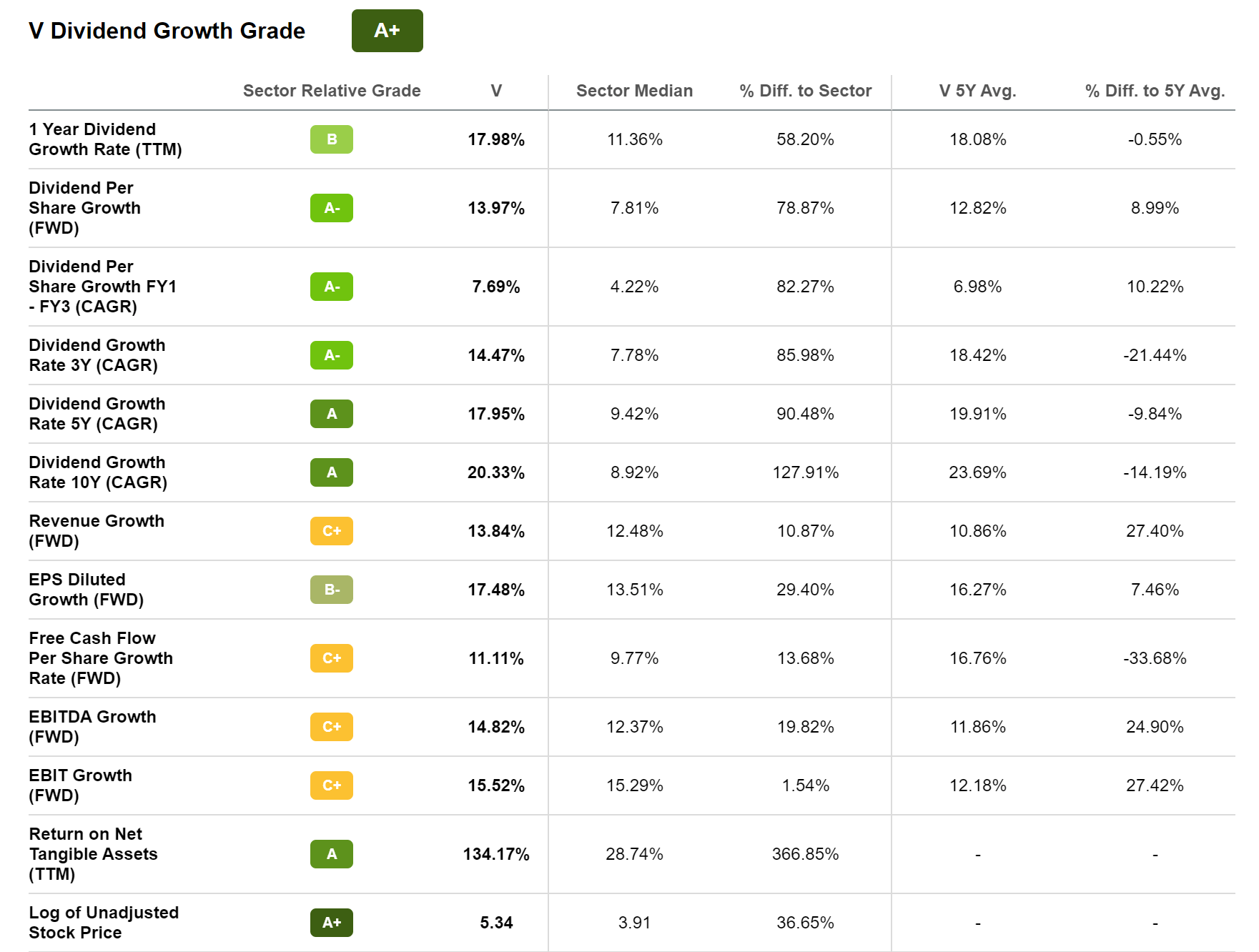

It can also be highlighted that Visa has shown a Dividend Growth Rate [CAGR] of 20.33% over the last 10 years, which reinforces my opinion to select it as one of my favorite dividend growth companies to invest in this month.

Below you can find the Seeking Alpha Dividend Grade results for Visa, which also support my investment thesis that the company is an excellent pick for dividend growth investors.

{kind=link}

Johnson & Johnson

I admit that you cannot expect exceptionally high Dividend Growth Rates from Johnson & Johnson in the coming years. Nevertheless, I have still included it in this month's list of dividend growth companies you should invest in. In the following, I will discuss the reasons for doing so:

First, the company will help you to protect your investment portfolio. In my opinion, it is important to have companies that ensure your portfolio will not lose too much of its value in times of a stock market crash. Johnson & Johnson is a company that can help with this: it has a low 24M Beta of 0.24 and, in addition to that, has enormous financial strength (Aaa credit rating by Moody’s).

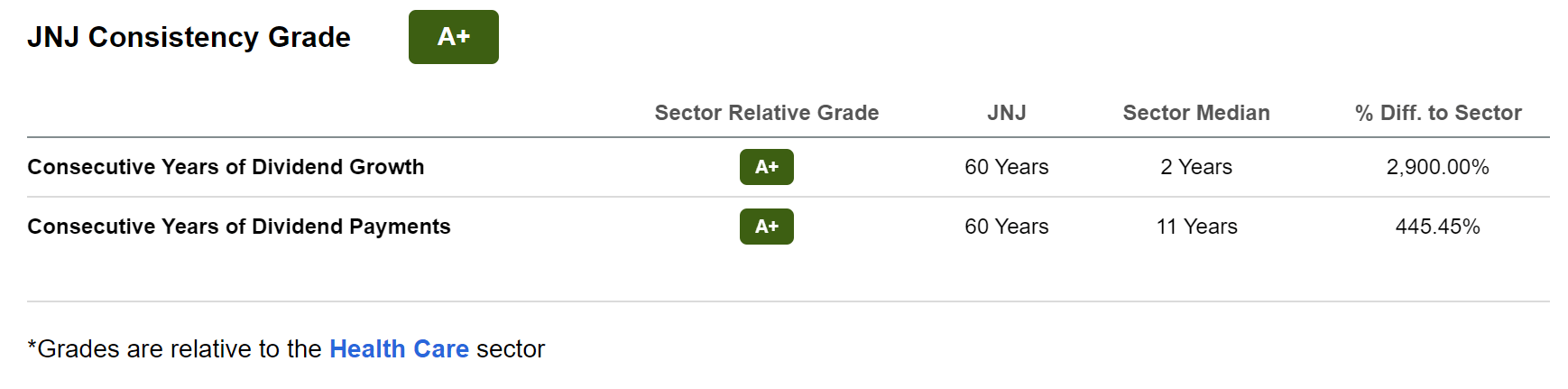

Second, I am confident that the company will succeed in raising its Dividend year after year in the coming years and even in the coming decade. The company has shown a Dividend Growth Rate of 6.03% [CAGR] over the past 5 years, and, in addition to that, has shown 60 Consecutive Years of Dividend Growth.

Third, it can be highlighted that Johnson & Johnson’s Payout Ratio of 44.06% is slightly lower than its competitors such as Eli Lilly and Company (NYSE: LLY ) (Payout Ratio of 45.44%) and Novo Nordisk A/S ( NVO ) (45.31%) and significantly lower than AstraZeneca (NASDAQ: AZN ) (83.45%). However, it is true that Pfizer’s (NYSE: PFE ) Payout Ratio is even lower (24.39%) than Johnson & Johnson’s.

Johnson & Johnson’s low Payout Ratio once again strengthens my theory that the company can serve to hedge your investment portfolio, since the low Payout Ratio suggests that the probability of a dividend cut is low. A dividend cut could cause the stock price to decrease significantly. The opposite is true for Johnson & Johnson: the company’s low Payout Ratio leaves plenty of room for future dividend enhancements from which you can benefit as an investor when investing with a long time-horizon.

Fourth, Johnson & Johnson’s current Valuation is attractive: the company has a P/E [FWD] Ratio of 22.69, which is 12.47% below the Sector Median (25.92). From my point of view, however, the company should be rated with a premium when compared to its competitors: this should particularly be the case because of Johnson & Johnson’s broad product diversification and its enormous financial strength.

Below you can find the Seeking Alpha Consistency Grade for Johnson & Johnson which again confirms that the company is an excellent pick for dividend income as well as dividend growth investors.

{kind=link}

Conclusion

When building an investment portfolio that aims to help you generate some extra income, it is important to not only focus on the Dividend Yield but also the selection of dividend growth stocks, as this can contribute to significantly raise the dividend that you can receive year over year from the companies you invest in.

In my opinion, achieving a balance between an attractive Dividend Yield and a relatively high Dividend Growth Rate is very important to the long-term success of an individual investment portfolio.

In this article I have shown three dividend growth companies that I currently consider to be attractive: all of them have strong competitive advantages, have shown a relatively high Dividend Growth Rate in the past and all currently have an attractive Valuation, offering investors an attractive entry point for investing and to benefit from the companies’ constantly growing dividends.

I look forward to hearing your opinion on my selection of these three dividend growth stocks and to hearing which are your favorite dividend growth stocks to invest in this month!

For further details see:

3 Dividend Growth Stocks To Buy In January 2023