INTC - 3 Dividend Stocks To Buy When 98% Of CEOs Predict A Recession In 2023

Summary

- The consensus is clear: 2023 will be a recession.

- But the numbers don't necessarily suggest this.

- Here's how to invest when everyone predicts a recession.

The inevitable never happens. It is the unexpected always - John Keynes

Written by Sam Kovacs

Introduction

News only serves us insofar as it provokes forward looking questions.

As I was looking through Seeking Alpha's trending news, a headline caught my attention:

98% of CEOs predict recession in 2023 - Conference Board - Seeking Alpha

The article gives a little more detail. Below is the TL;DR:

- Dana Peterson, chief economist at conference board, performed a survey which concludes that 98% of CEOs expect a recession in 12 to 18 months.

- That is up from earlier this year when 95% expected a recession.

- Peterson expects the downturn to be swift and shallow, with housing being hit and services next.

How does one use this news item, and ask a series of questions which will lead to the answers we need to make it actionable?

Is a recession inevitable?

Does the news matter?

One could argue that it does, as CEOs supposedly have the best foresight on their business and industries state of affairs.

One could also argue that it doesn't, calling a recession in 2023 has become quite a mainstream proposition. All news outlets have an article telling you the 2023 recession is inevitable:

- Bloomberg says that the " Forecast for US Recession Within Year Hits 100% ".

- The Wall Street Journal writes that " Economists Think They Can See Recession Coming—for a Change ".

- Finally, the FT, shares our opinion: Economists see recession coming, so maybe it’s not ".

You see, economists get it wrong, a lot.

In fact, the consensus view of economists has not predicted a single recession since records have been kept in 1970.

Not one. Zero. Nada. Zilch.

As the FT author concludes:

Still, when the consensus is so strong, anchored by economists whose recession forecasting record is so poor, it is hard not to think of that quote from Keynes. The unexpected is a constant in markets and the economy, which suggests we should at least entertain the possibility that a recession is not inevitable.

Goldman Sachs ( GS ), have a piece of the puzzle, but they're looking at the wrong aspects.

In a recent Bloomberg article , it was reported that Goldman Sachs strategists viewed stock markets as " not yet reflect the risk of a US recession ."

Well let's stop and think about this for a second.

The "market" is supposed to be this "forward thinking entity" which reflects market participants collective expectation of the future. The puzzle of why markets seem to be predictive lies in the fact that the average view of a large number of participants seems to consistently outperform the opinions of a few experts.

Of course there are times where the collective thought overshoots or undershoots, or even becomes reactionary, but over time, it does quite a good job.

A quote, often misattributed to Mark Twain says that " it's not what you don't know that gets you killed, it's what you know for sure, that just ain't so '.

Right now, economists, CEOs, the media, and probably some of your favorite SA authors, are dead convinced that there is going to be a recession.

And they might be right. But markets are currently pricing that if there even is a recession, it could be short lived and shallow, which is what most expect.

If our protagonists are being overly negative, we might even expect no recession at all.

There's a good ol' joke about having an economist friend who predicted 12 of the last 2 recessions.

So to answer: is a recession inevitable? No.

Does someone saying (or even multiple "someones" saying) a recession is looming matter? No.

But we certainly shouldn't ignore that a recession is possible.

More like the 90s than the 80s

This inflation bout has been compared largely to the inflationary period of the early 80s, when in fact there are many similarities with the early 90s.

Many assume that the Fed will have to act like it did under Volcker in the 80s by inducing a recession through aggressive rate increases. But if supply side inflation subsides, which it very well could do in 2023, then such extreme measures could be avoided.

I talked more about this idea in an article titled " What if the 2022 bear market is already over? " which I wrote in late October as the rally was underway.

But if a recession is less likely than is believed by the consensus, and the fallout in case of a recession is milder than consensus, then the market is fading certain parts of the market beyond reason.

The market does this time and time again.

Remember when the market faded energy? Some of you reading this probably thought it would have been crazy to build overweight energy positions in 2020-21.

I remember a comment on a Chevron ( CVX ) article of ours where a member told us that if we wanted to protect our capital we should "stay away from oil".

CVX MAD Chart (Dividend Freedom Tribe)

{kind=link}

Of course, the stock returned 113% since then compared to the S&P 500s low double digit increase.

This is because the collective view was vulgarizing the idea that the energy transition was killing oil and gas. The data didn't back this up.

Then in early 2021, the market was fading defense stocks because "The Biden administration would slash the defense budget".

We wrote a note to the members of the Dividend Freedom Tribe, explaining that because the geopolitical threats of China, Russia, and North Korea remained elevated, Biden's preferences had very little to do with what the defense budget would be.

Here the market made the classic mistake of judging political decisions based on preferences, rather than on constraints. Constraints always determine the action.

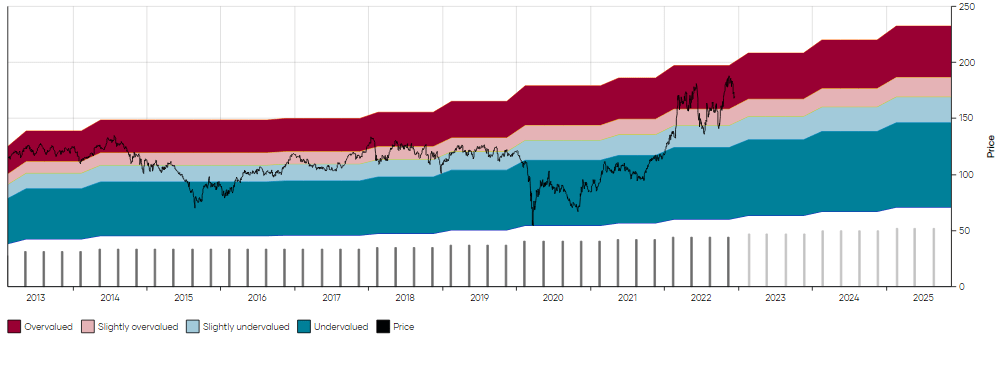

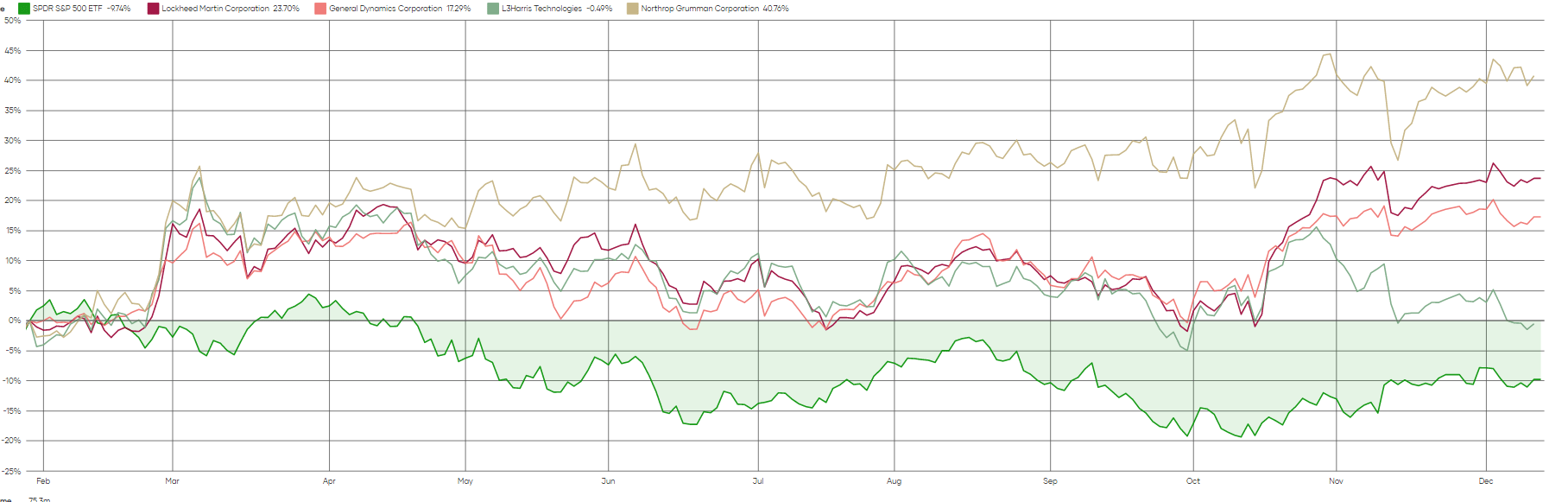

So we suggested investors initiate positions in beaten down defense stocks, such as Lockheed Martin ( LMT ), Northrop Grumman ( NOC ), L3Harris ( LHX ), and General Dynamics ( GD ).

SPY vs Defense Stocks (Dividend Freedom Tribe)

{kind=link}

As you can see in the chart above, all have beaten the S&P 500, with 3 stocks having done extremely well.

Of course, it now seems obvious that the defense budget won't be significantly cut, and in fact, it is likely we'll see an 8% increase in the defense budget in 2023.

But at the time, the market took a vulgarized idea "Democrats don't like defense", and punished stocks without looking beyond that.

When the consensus acts on a shallow belief, it is often wrong. It is these instances we want to identify.

Why did I say this is more like the early 90s than the 80s?

Inflation coming from demand or supply?

So here is the current situation:

Everyone is expecting the Fed's consecutive interest rate hikes to eventually kill the economy, à la Volcker.

Only, the numbers don't suggest this so much.

As you know, what is currently driving markets is inflation, and the Fed's reaction to inflation.

If this time around is more like the 80s, it would be because inflation is primarily demand driven, and this demand driven inflation is persistent.

Market participants are now convinced that inflation is mostly demand driven. In 2021 when we warned that all the helicopter money would lead to demand driven inflation, most said "no, no, it is all supply driven".

{kind=link}

But I believe that most of the demand driven inflation is behind us. "One-off" inflation contributors like travel and hotels, which increased following reopenings, as they were coming off a low base, and were fueled by pent-up savings. They have now been receding, as pent-up savings are drying up, and we're comparing to a higher base.

Wage growth is the one which can lead to demand-led feedback loops, but given the crunch that retailers like Target ( TGT ) and VF Corp ( VFC ) have reported in discretionary segments, we're seeing more of a reshuffling of budgets (dominated by essential household expenses), which should have an overall neutral impact on a balanced basket of goods (inflation in certain areas compensated by deflation in others).

And supply driven inflation seems to have peaked and is now coming down. The pandemic initiated supply-chain issues were exacerbated by war in Ukraine. They are now receding.

This is why it is now expected that inflation hits 3% by the end of next year, a level at which it would no longer be a problem.

Getting there will hurt consumers, but unlike the 80s, and like the 90s, it is mostly white collar jobs which will be targeted. The job cuts at Twitter ( TWTR ), Amazon ( AMZN ) and Meta ( META ) signal this.

On the other hand, restaurants and factories are still short of workers.

This means that an economy-wide crisis is unlikely. Whether Twitter marketing staff will pick up a job at a restaurant remains to be seen, but what it means is that the most fragile part of US consumers will likely not be affected.

Blue collar jobs outnumber white collar jobs 4 to 1.

This all looks very much like the early 90s.

Most are not looking at it this way. This creates opportunities.

Opportunity 1: Stable businesses with a discretionary kicker

There are businesses which are viewed as purely discretionary or cyclical, although they in fact have a strong staples or secular segment as well.

Such stocks are great for the current environment, as they provide a natural hedge. If a recession shows up, they can see it through with their stable business backdrop. If we skirt the recession, they enjoy the upside from a mean-reversion of discretionary stocks.

Two stocks, which are unjustifiably undervalued come to mind.

Target which is viewed as a discretionary stock, despite 50% of its business coming from food & beverage and household essentials.

The declines in its discretionary segments have been offset by increases in staple segments.

TGT Segments (Dividend Freedom Tribe)

{kind=link}

This is allowing TGT to hold up a lot better than the market is pricing, with the stock down significantly, and now yielding 2.9%., which is its 10 year median yield, and I believe, slightly undervalues the stock.

TGT MAD Chart (Dividend Freedom Tribe)

{kind=link}

As I said in a note to Dividend Freedom Tribe members this week:

As management moves to cut another $2-3bn in costs over the next couple of years, and the company consolidates the explosive growth they generated since 2019 (going from an $80bn in sales business to a $100bn business), I expect the company to maintain a platform which will support a healthy dividend and more growth to come.

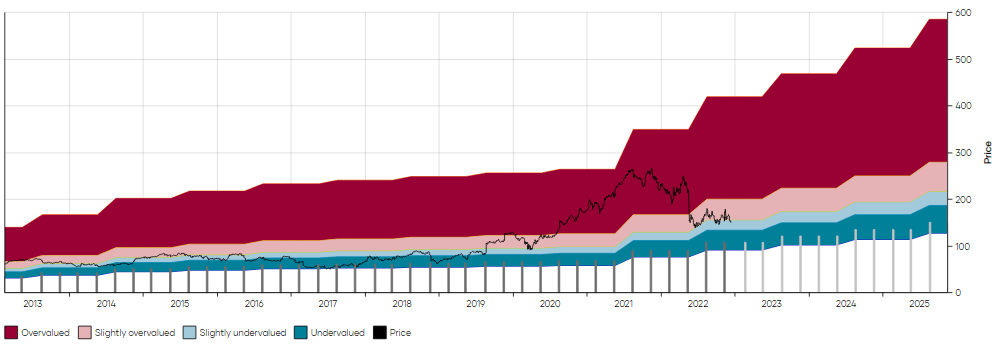

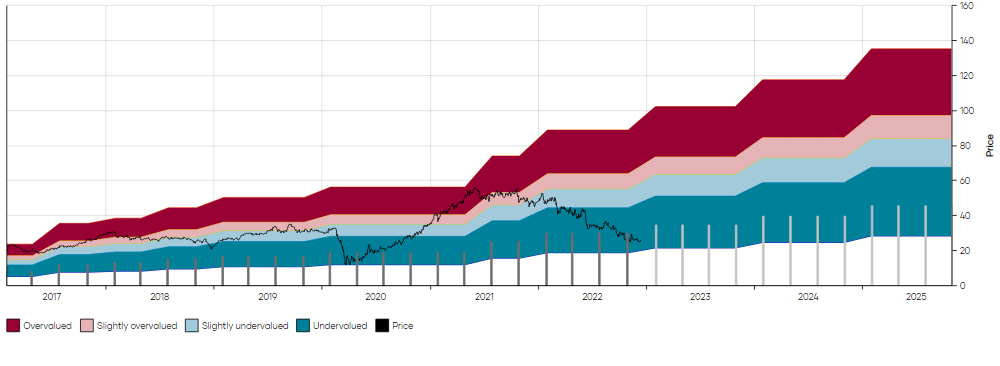

The second such stock is Intel ( INTC ), which is being judged ONLY on its current consumer oriented business, which it is true has lost a lot of market share to AMD. But looking at INTC this way ignores the massive role that the company will play in becoming the most prominent foundry in the US;

This is a theme which I highlighted in an article I called the " $1 Trillion Dollar Opportunity ":

The pandemic supply-chain shock exposed a problem that had been mounting for years. The U.S. share of global chip manufacturing has declined to 12% from 37% in 1990. South Korea and Taiwan, notably, have spent years actively investing in their own chip manufacturing, creating an uneven playing field for U.S. chip makers that harms our economy and global competitiveness.

The U.S. will invariably pass its bill to support fabrication domestically.

Intel will get new fabs.

In the current environment in which relying on Taiwan semiconductors is a TOTAL liability because of the geopolitical risks in the region, the west can only invest in its own supply capacity.

Intel will be the biggest recipient, and this will start to become obvious to markets in 23 and 24. By 2030, people will be saying, "imagine if we bought Intel below $30?".

Don't imagine, buy it now and get a 5% yield.

INTC MAD Chart (Dividend Freedom Tribe)

{kind=link}

Opportunity 2: Unjustified bearishness on consumer strength.

As explained earlier, it is not the most fragile portion of the economy which will be the most impacted by job cuts and a possible recession in 2023. It is white collar workers.

So investors who are preparing for an apocalypse in auto loan payments, mortgage payments, or credit card payments, are not going to get it.

They are projecting the 2008-2009 recession onto the current market, and it simply will not work out this way.

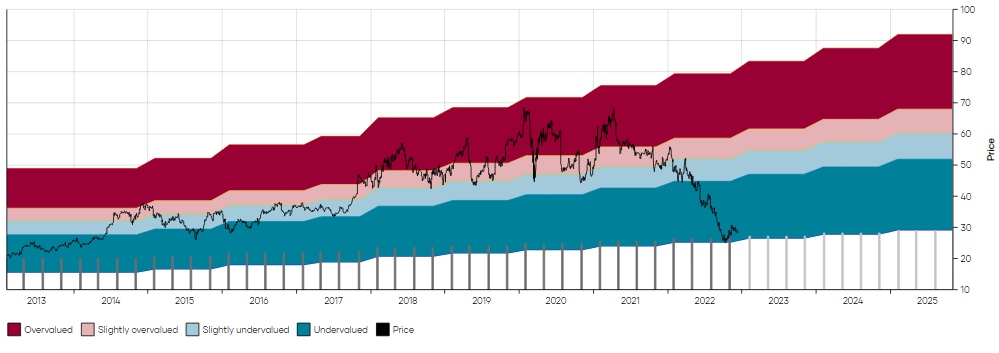

One stock, Ally Financial ( ALLY ), has been butchered by the market this year because of "consumer caution", to borrow words of analysts which have been downgrading the stock.

Results missed analyst expectations because of higher costs on the existing batch of loans, but analysts outlook clash with the reality that management are noticing. As was said in the last earnings call:

Similar to last quarter, and consistent with what we have been guiding, we saw strong loan growth across the company and in particular, within auto finance. We certainly recognize the tightening environment but consumer credit underwriting is a core capability of our company, and we believe we are generating some of the most attractive, risk-adjusted loans in the history of Ally.

ALLY currently yields 4.66%.

ALLY MAD Chart (Dividend Freedom Tribe)

{kind=link}

The market is overdramatizing the risks. This makes for a brilliant entry into the stock at the current price.

Conclusion

Don't pay too much attention to the pundits in the news. They have a headline for every piece of data.

Don't pay too much attention to economists. They have a recession for every piece of data.

Focus on the numbers. On the common sense, and make investment decisions which bake in a margin of safety.

For further details see:

3 Dividend Stocks To Buy When 98% Of CEOs Predict A Recession In 2023