PSCE - 3 Energy Macro Themes For 2023

Summary

- Oilfield services may outperform E&P.

- Small-cap oil equities should catch up with large-cap.

- The capital allocation may be shifting from onshore/short-cycle to offshore/long-cycle.

As we are bidding farewell to 2022, I wanted to share some high-level thoughts on the energy macro trends I expect to unfold in the new year.

Energy was the top performer in 2021-2022:

After two great years, many macro investment outlooks are skeptical that energy can crush the S&P 500 ( SPY ) for the third year in a row.

My view is that energy will still do well in 2023, even if not as great as in 2021-2022, but what I think is more important is that looking at the entire sector ( XLE ) masks some important differences in valuation and performance within the sector itself.

More than 40% of XLE is basically Exxon Mobil ( XOM ) and Chevron ( CVX ), the two integrated U.S. majors with market caps of $450B and $350B, respectively. Due to their size, XOM and CVX would naturally benefit the most from passive allocations to energy, but their risk profile and valuations are quite different from that of most other energy companies. As active investment is allegedly making a comeback, we should also look under the hood here and assess which areas of energy may be better positioned than others going into 2023.

I think that relative performance in the new year will follow three main themes.

Theme 1: Services may outperform E&P

The energy sector is a hodgepodge of exploration & production (or E&P) companies, downstream refiners, midstream operators, integrated majors and oilfield services (or OFS) providers. All these companies are indeed exposed to oil prices ( OIL ), but they don't quite share the same risks. OFS derives its revenues from selling services and equipment to E&P; from the latter's perspective this is a capital expenditure and a cash outflow. Excess services capacity can be detrimental to OFS but a boon for E&P and vice versa.

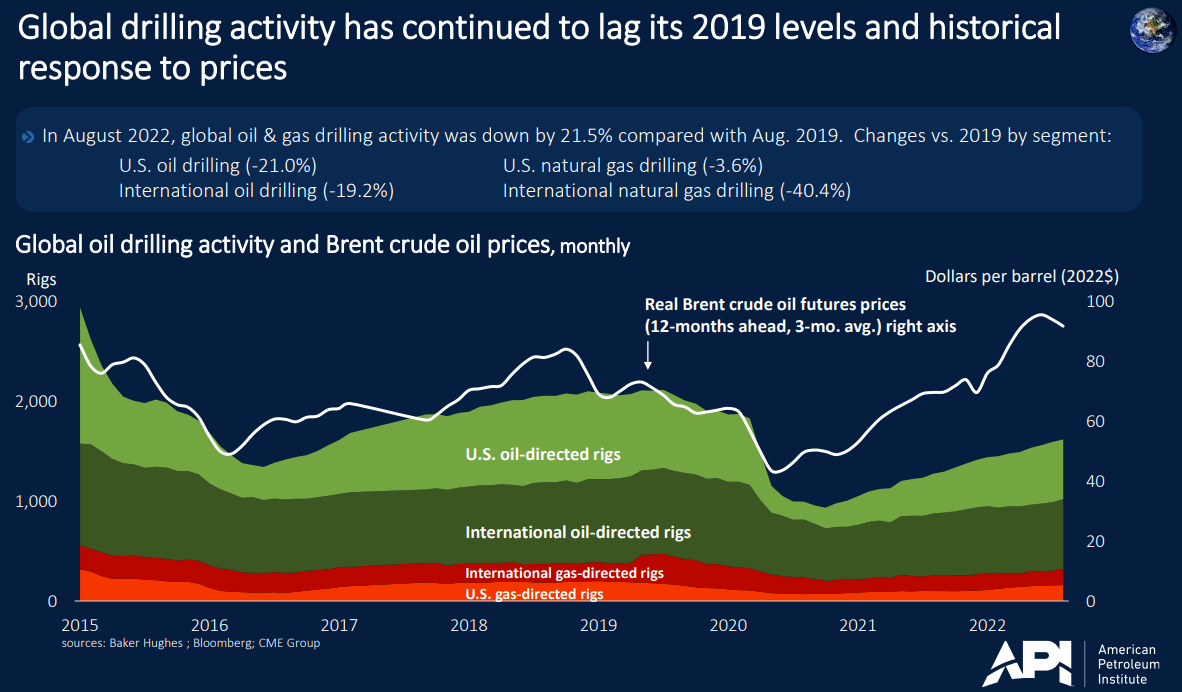

Generally, OFS trails E&P and peaks later in the cycle. Since capex comes from E&P, first the oil price environment has to be positive for E&P boards to authorize more capex. Then, we have further lags until exploration or development plans are made, and the work is put out for bid and eventually contracted to services providers. OFS revenue can easily lag behind E&P revenue by a couple of years.

The prior energy bull cycle ended in 2014, as rapid productivity gains in U.S. shale led to global overcapacity, which has taken years to work through. While E&P was predictably able to offset some of the impacts of lower oil prices by reducing capex, the downturn was detrimental for OFS ( XES ):

The broad energy sector has already exceeded its prior 2014 top, but oilfield services still have a lot of ground to cover.

The prolonged OFS decline has, however, also positioned the services sector for future outperformance. During the lean years, much capacity was lost due to bankruptcies, idle equipment that is no longer economic to bring online, or laid off personnel that has permanently left the industry. That is why, when E&P spend finally started increasing in the last year, the services sector couldn't immediately meet the demand. The shortage of workers, rigs and other equipment is driving "oilfield services inflation" which now prominently features in many earnings calls.

For some time in 2021, the prevalent sentiment was perhaps that OFS would never come back because the "capital discipline" endorsed by E&P would preclude signification capacity expansions. According to this narrative, E&P would produce their existing reserves and then liquidate themselves. Indeed, the capex response to oil prices is still muted in historical comparison:

{kind=link}

However, much changed in 2022 with the Russia-Ukraine war, and energy security has started displacing the ESG narrative, particularly so in Europe:

Offshore Engineer

Much of the "capital discipline" was probably limited to U.S. shale anyway (see Theme 3), as national oil companies (or NOCs) had already announced ambitious expansion plans. Majors' capex including XOM, CVX and Shell ( SHEL ) also seems to have bottomed in 2021:

Now that capex has finally lifted off, and compounded with the "supply chain" issues plaguing the general economy, the narrative has quickly switched from OFS being a price taker to unprecedented services inflation:

Oil Services Cost to Increase 15.9%... And This is NOT TRANSITORY!

Schlumberger ( SLB ) and Halliburton ( HAL ), the largest OFS firms, have been very bullish during their 2022 earnings calls, seeing a multi-year growth cycle, led by international markets and offshore - and so have many smaller firms, despite the macro recessionary fears. By all indications, the industry seems to feel that a 2023 recessionary drop in oil prices will be temporary, so long-cycle projects which will drive much of the OFS growth won't be as impacted.

Some repricing signs

In the last couple of months, there are some modest signs that OFS is indeed beginning to outperform XLE:

I expect this trend to strengthen in 2023, and I don't think it is too late to buy into the OFS space. Here is, for example, the XOM/SLB price ratio; high values mean that XOM is relatively expensive and vice versa:

Coming off the prior bull cycle, SLB was valued quite generously. The ratio peaked around March 2020 when the lockdown-driven production shutdowns really forced "capitulation" in OFS. The ratio has come down a bit in the last couple months but is still above the historical averages.

Theme 2: Small-cap is undervalued relative to large-cap

While energy ( XOP ) has regained a lot of ground, small-cap energy stocks ( PSCE ) have been left behind:

Here is also a comparison I generated using SA's stock screener function:

{kind=link}

I included U.S. and Canadian tickers flagged as oil and gas drilling, equipment or services, exploration and production or integrated oil and gas. I further required positive TTM revenue and EBITDA. The screen yielded 216 tickers, which I ranked into quintiles by market cap.

While there is some movement among the bottom quintiles, I think all four metrics show that the top quintile is relatively overvalued. For example, price to book ratios average 3.3x in the top quintile compared to 1.2x in the bottom quintile.

What explains the difference in valuation?

There are good reasons why the market is willing to pay higher multiples for integrated majors such as XOM or CVX compared to bottom quintile companies, with scale and diversification likely topping the list. After all, even in March 2020, there was little doubt these mega companies would survive the crisis. Passive allocations to the energy sector likely push up the multiples for the largest companies too.

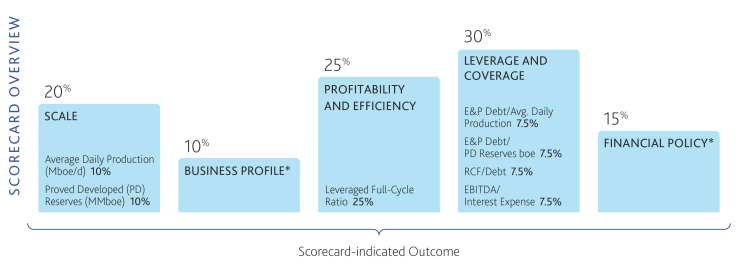

On the other hand, many small-cap companies have been addressing their debt issues, which in a number of cases has also forced these companies to enter into unfavorable hedges. The way credit markets think about borrower risk also inherently penalizes smaller companies; much of the credit rating determinations are based on scale (production, reserves size) and diversification (operating in multiple basins):

{kind=link}

Consequently, it is harder for small-caps to earn investment grade ratings; this pushes up their debt yields and also affects negatively the equity too.

What does this mean about 2023?

During 2022 much progress was made on debt repayments and many small-caps are now practically debt-free. These companies can hedge less, allowing for more upside exposure. They are also going to be insulated from rising interest rates and corporate credit spreads. As 2023 earnings start to roll out, these improvements should start getting noticed by analysts, resulting in gradual re-rating.

Of course, not every small-cap will be a winner. Some companies still have high credit risk or long-term profitability issues. However, profitable small-caps with clean balance sheets should do well. Given how wide the relative discount to large-caps is right now, I expect the small-cap group to outperform XOM and CVX on a relative basis too.

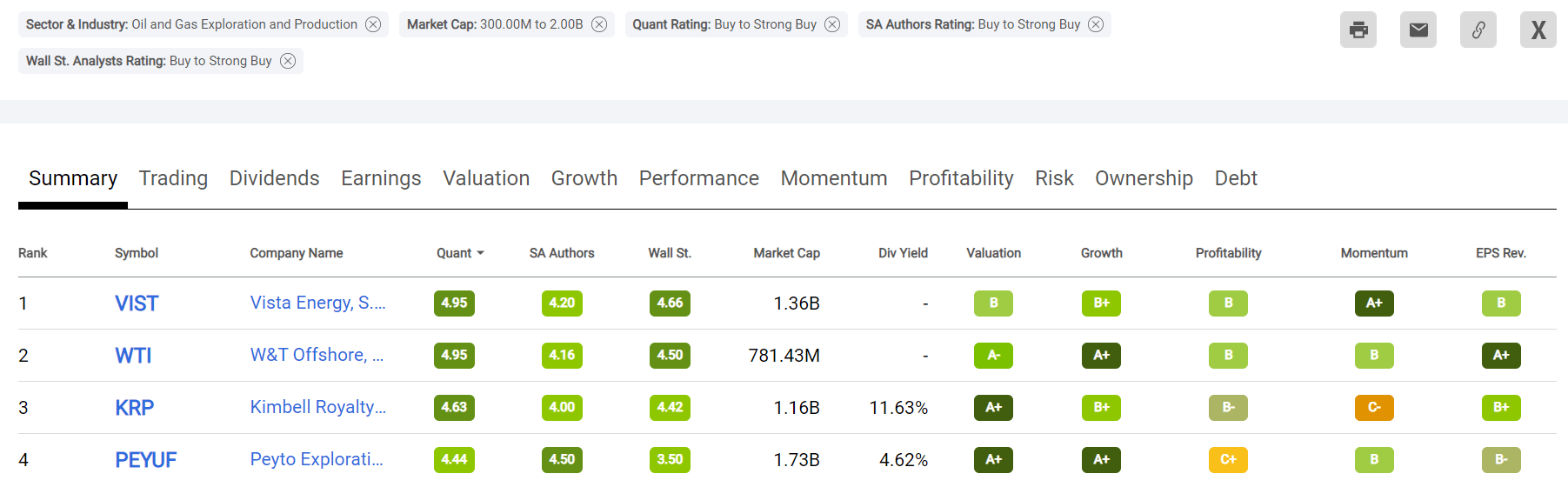

Here is a quick screen for small-cap E&Ps with favorable recommendations from SA and Wall Street analysts:

{kind=link}

Of these companies, I personally like W&T Offshore ( WTI ) - see Theme 3 too.

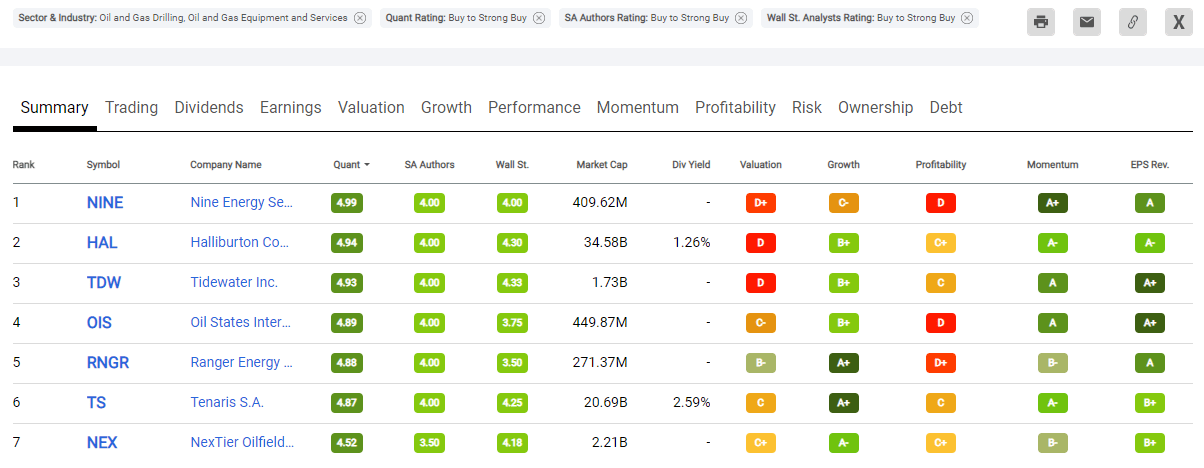

Another similar screen for OFS players:

{kind=link}

Of this list, I like Oil States International ( OIS ) - see also Theme 3 - and Tidewater ( TDW ). I personally prefer SLB to HAL, as SLB has more international and less North American exposure. I think Nine Energy ( NINE ) is also interesting but is trading too much like a meme stock for my preference.

Theme 3: Long-cycle over short-cycle

U.S. shale has been the "pivotal" global producer for quite a while. Its "short-cycle" profile has allowed it to ramp up or down faster in response to demand compared to long-cycle investments. However, there are signs that shale's role may diminish in the future; negative assessments of shale's prospects now frequently make headlines :

{kind=link}

While predictions of shale's demise appear exaggerated; ultimately, shale is also a depletable resource; the more we produce, the less is left to produce in the future and that additional production will also come at higher cost because E&P companies have picked up the lowest hanging fruit first.

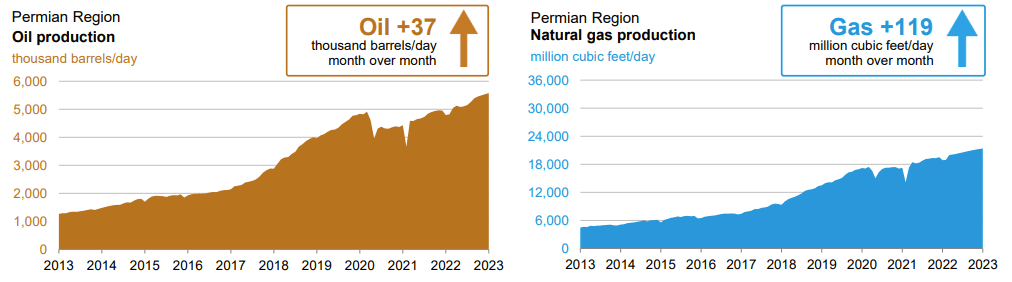

The Permian is still eking out growth and is pulling aggregate U.S. numbers:

{kind=link}

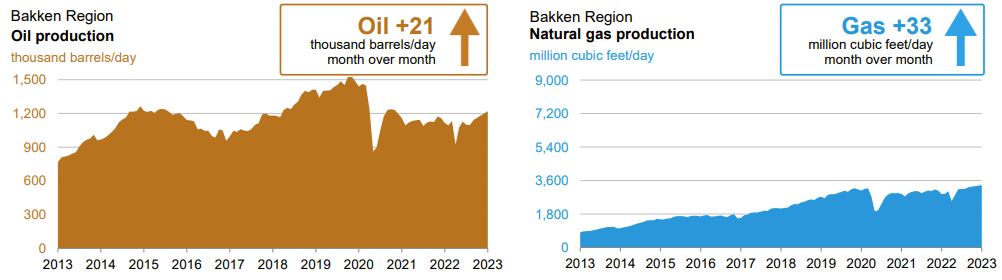

However, more mature basins such as the Bakken are behind their prime:

{kind=link}

Drilling productivity is also down although most of the gains in 2020-2021 were likely due to cannibalization of drilled-but-uncompleted (or DUC) wells:

API, EIA

As the pivotal role of U.S. shale is reduced, the confidence in long-cycle investments with longer payback periods will improve. Schlumberger CEO Olivier Le Peuch:

The macro environment we are facing is quite unique. It's a confluence and unprecedented low spare capacity, 8 years of underinvestment in international basins and a call for energy security that is creating a double sourcing of both oil and gas parts of the international basins. So, when you put that together, it trades not only a short cycle impulse on production enhancements to respond to that energy security, but also reinforce the need for expanding oil capacity, accelerating gas development and the entire set of international basis both offshore and onshore benefit from it, right, as we see. So, we have seen an inflection in the sentiment of our customers, both our national company, international oil company and international independent, to respond to that call and turning and accelerating the investments and rotating their investment internationally visibly.

Much of the international growth will be offshore too, both from deep and shallow water. Mr. Le Peuch for Q3:

Internationally, all areas grew and the pace of growth increased to 13% sequentially and 26% year-over-year. Activity and revenue trends confirm the onset of another phase in the global growth cycle, one that will be increasingly driven by the international and the offshore markets.

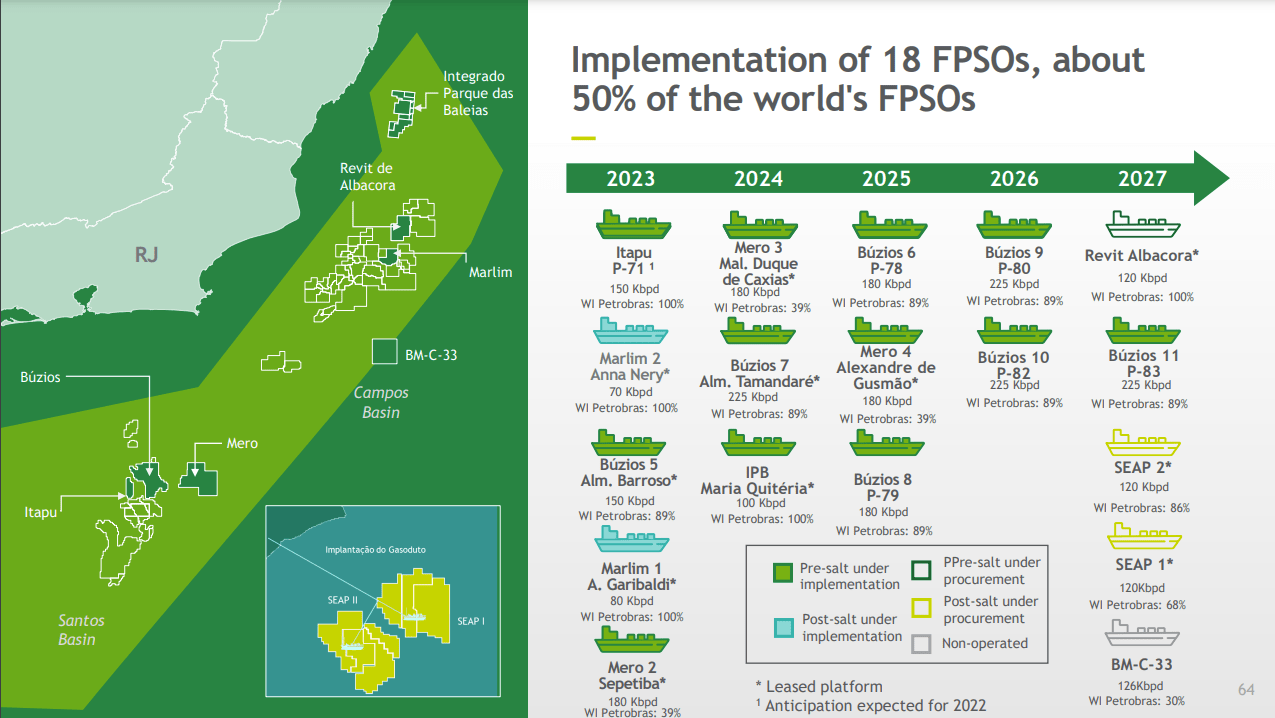

Brazil's NOC Petrobras ( PBR ):

Petrobras hikes five-year spending plan to $78B but Lula team may review

Petrobras is planning to deploy 18 floating production storage and offloading (or FPSO) units over the next 5 years:

{kind=link}

{kind=link}

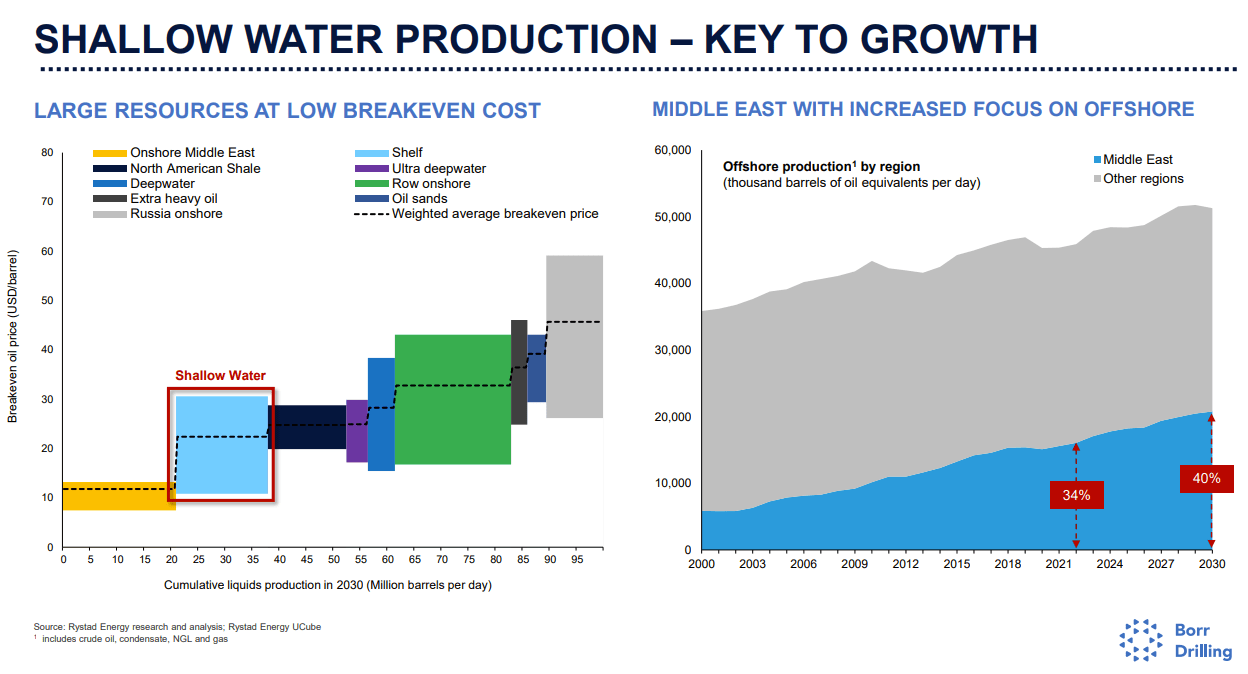

Borr Drilling ( BORR ), a jackup driller, expects increased shallow water activity over the next several years, particularly in the Middle East:

{kind=link}

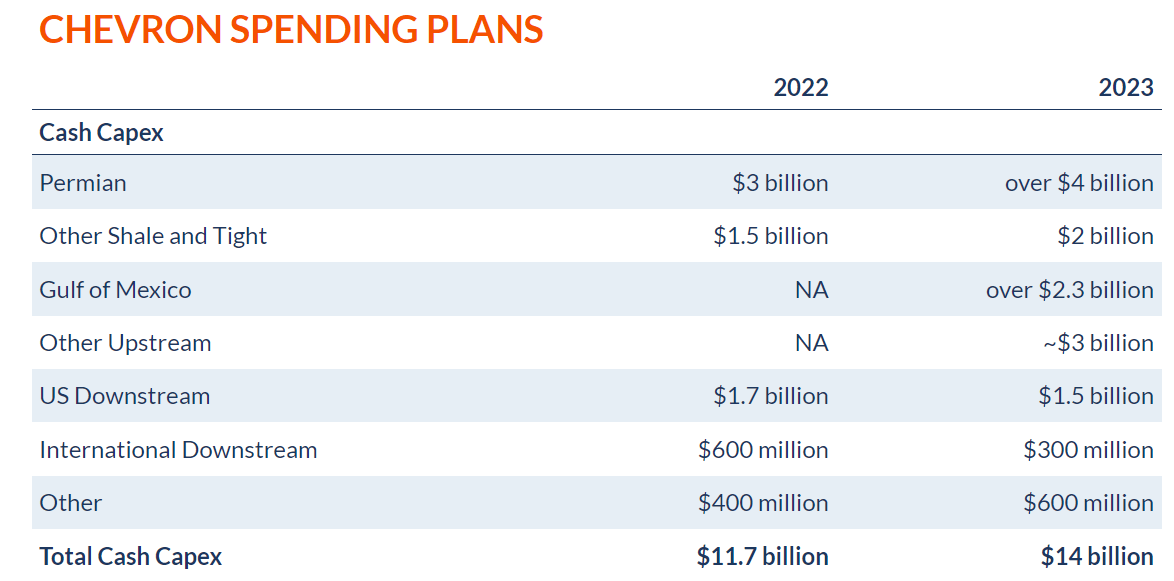

Finally, Chevron itself is also allocating more to the Gulf of Mexico in 2023:

{kind=link}

The Permian is also getting a boost, but the allocation to "other shale" is not increasing significantly.

Some ideas

Much of the future offshore activity will be run by NOCs, which frequently aren't directly investable, or even if they are as PBR, they won't be a pure play on the investment theme.

What unifies NOCs, though, is that they are all heavily reliant on U.S.-listed oilfield services providers to carry out their expansion plans. That is why I think the better way to capitalize on the offshore revival is through services providers. Here are a few ideas I have written about before:

SLB, a mega-cap, but still with some runway left:

Schlumberger: Even If OPEC+ Fills The Supply Gap, SLB Still Wins

Oil States International, a small-cap OFS player with exposure to deepwater:

Oil States International: Benefit From The Deepwater Revival

BORR, a shallow-water driller with exposure to the Middle East:

Borr Drilling: What To Make Of The Refinancing Mess

From E&P with offshore exposure, I like two small U.S. Gulf of Mexico players:

W&T Offshore: Even The Bonds Are Undervalued - Buy

Talos Energy Stock: The EnVen Acquisition Should Pay Off

Both W&T Offshore ( WTI ) and Talos Energy ( TALO ) are deeply discounted and have significant reserves, so are somewhat insulated from the rising production costs that are experienced by U.S. shale. The U.S. Gulf of Mexico producers also pretty much sell their production at the headline benchmarks ( CL1:COM ), in contrast, say to Canadian oil sands producers, which also have long-lived assets but sell their production at huge discounts.

Conclusion

I have outlined three broad themes that I think will affect relative performance within the energy sector in 2023. Overall, I am optimistic about how the sector will do as a whole, but I think some areas will do better than others due to lower starting valuations and closer alignment with the capital allocation trends we see in the industry.

For further details see:

3 Energy Macro Themes For 2023