PLYM - 3 High Conviction REITs For Early 2024

2024-01-05 17:14:48 ET

Summary

- Plymouth Industrial REIT, Inc. has strong fundamental momentum and potential for further upside due to industry and macro trends in its favor.

- Simon Property Group, Inc. has a low FFO multiple but its real estate business is showing growth potential disguised by the drag from its cyclical operating retailers.

- EPR Properties may experience a reversal in its momentum as its price movement is not supported by fundamental strength and it faces significant tenant risk.

2023 was a year of big moves. The stocks that outperformed really outperformed, while others got left in the dust. Moves of this magnitude often come from one of two sources:

- Momentum resulting in overvaluation

- Underlying fundamental driver.

In the first category we would expect a bit of mean reversion, while the second is a recipe for further upside. Today we will be examining two stocks on which we are strongly bullish as their fundamental momentum has exceeded their stock rallies, and one potential short that was driven too high by momentum.

Plymouth Industrial REIT, Inc. ( PLYM ) – industry and macro trends shifting in its favor

Plymouth is up 23% in the last year.

{kind=link}

Despite the gains, PLYM is still trading at just under 13X funds from operations, or FFO, compared to the industrial real estate investment trust, or REIT, average of 19.4X. It has long been market consensus that PLYM should trade at a discounted multiple because of its higher leverage and inland markets.

However, four factors suggest PLYM’s multiple should be significantly closer to the sector average.

- PLYM’s markets evaded the new supply

- Construction is abating

- Macro trends look to increase demand in PLYM’s markets

- Reduced debt levels warrant higher multiple.

Construction deliveries were quite high in 2023 for industrial as developers want to get in on the sector’s rapid growth. However, new starts have been stifled by tighter lending standards and higher cost of capital, which is resulting in deliveries dropping in 2024 and further dropping in 2025.

Yardi Matrix

In brief, supply growth is moderating.

The properties delivered and those still in planning are concentrated in select submarkets.

Yardi Matrix

These are not PLYM markets.

{kind=link}

By evading the supply, PLYM’s markets remained tight with high occupancy. This is providing PLYM with the power to raise rents substantially.

In fact, PLYM just announced its 4 th quarter leasing: 5.6 million square feet at cash rent 21% higher than expiring rent. This brought same store occupancy up to 98.6% which is above what is traditionally considered full occupancy.

The Wall Steet Journal reports that:

“The average warehouse vacancy rate across the U.S. jumped to 5.2% in the fourth quarter of 2023 from 4.6% the previous quarter and 3.1% a year earlier.”

So, PLYM’s occupancy is up while the sector is losing occupancy.

Going forward, I anticipate demand to continue to increase for PLYM’s markets relative to other industrial REIT markets, as shipping is down while domestic manufacturing is kicking into high gear.

Yardi Matrix reports:

“The ports of Los Angeles and Long Beach, for example, handled 17% fewer containers through October than they had through the same period last year.”

Lower port activity hurts demand for coastal logistics facilities. This demand is moving inland to PLYM territory. Yardi Matrix continues:

“The other factor behind port activity normalizing this year is the nearshoring and reshoring of manufacturing. Manufacturers want to avoid the kind of disruptions seen in 2020 and 2021, and are increasingly looking to move operations to North America.”

Finally, PLYM is using profitable, low cap rate dispositions to significantly lower its debt levels

{kind=link}

Increasing demand, evading markets with new supply, and lower debt all suggest PLYM’s multiple should be higher than it has been in the past. I think its multiple will move significantly closer to that of the sector which implies material upside.

Simon Property Group, Inc. ( SPG )

SPG returned 23% in the last year, handily beating the REIT index.

{kind=link}

This took its FFO multiple from high single digits to 11.5X.

{kind=link}

Year-over-year FFO growth was okay, but not nearly enough to keep up with the price movement.

So, while 11.5X is still quite a low multiple, SPG is less cheap relative to the index than it was.

However, those who are just looking at the headline FFO number are missing the bigger picture story of what is going on underneath.

SPG is primarily a real estate company, but they also get significant earnings from ownership of operating retailers.

The real estate revenue is much more reliable and would tend to trade at a higher multiple, while the operating revenues are more cyclical in nature and would tend to trade at a lower multiple.

FFO had, in prior periods, been propped up by unusually strong earnings from the cyclical operating businesses. These retail revenues have since moderated, which has been a drag on FFO and masked the growth in the real estate business.

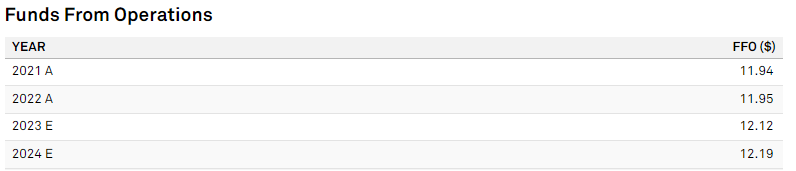

Here are the FFO numbers of recent years and consensus for 2024.

{kind=link}

That appears to be fairly anemic growth and is likely why SPG is trading at such a low multiple.

I posit that the low growth rate is a temporary phenomenon largely due to normalization from the abnormally high earnings in the operating retail.

This can be measured by looking at the real estate revenue.

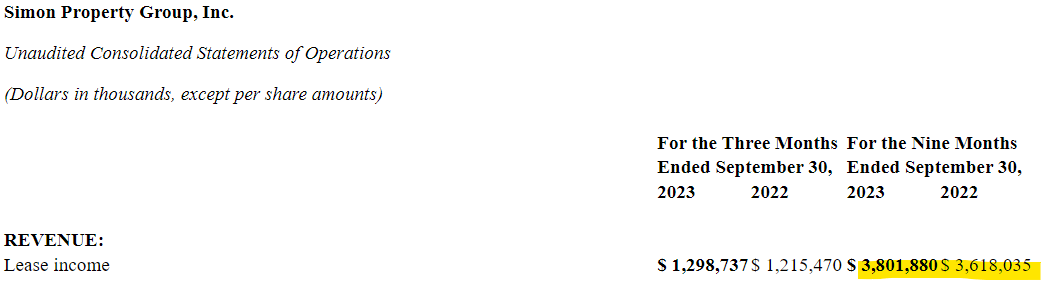

{kind=link}

That is 5% growth in lease income.

In the most recent quarter, occupancy was up 70 basis points to 95.2% and base minimum rent was up 2.9%. Domestic property NOI increased 4.2%.

I think SPG has a significantly higher growth rate than is showing up in the numbers.

Think of it as a person walking an undisciplined dog along a sidewalk. Sometimes the dog will run out in front of the owner, and other times the dog will get distracted and lag behind.

In the short term, the location of the dog is greatly impacted by the noise of the dog’s erratic behavior. In the long term, however, the human is consistently moving in the same direction which will ultimately dictate where they move.

- The retail revenues are the dog, sometimes surging, sometimes lagging

- Real estate lease revenues are the human. Consistently moving forward.

Essentially, the 1% FFO growth rate is inclusive of the noise, which over this particular measurement period happened to be a negative factor.

If we remove the noise, I think FFO/share growth is closer to 4%-5% annually. That warrants a multiple significantly higher than 11.5X.

Short/sell thesis: EPR Properties ( EPR ) momentum “risk on” trade likely to reverse

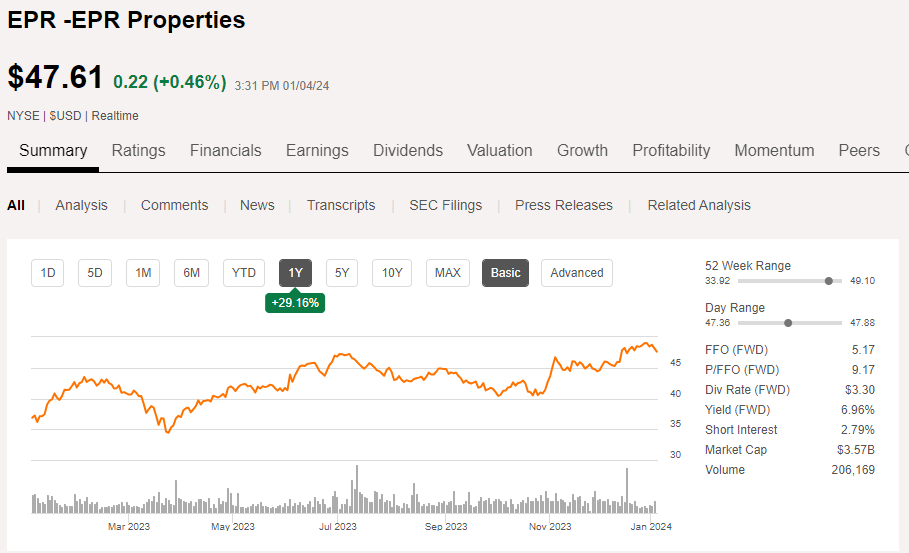

Like the other REITs discussed above, EPR had a great 2023, with the stock trading up nearly 30%.

{kind=link}

Unlike the other companies, the price movement was not driven by fundamental strength.

Movie theaters are still struggling, and EPR is forecasted to lose FFO/share going forward.

{kind=link}

The tenant risk is significant, and at current pricing I don’t think investors are getting enough of a discount to account for the risk.

So why is EPR trading up so much?

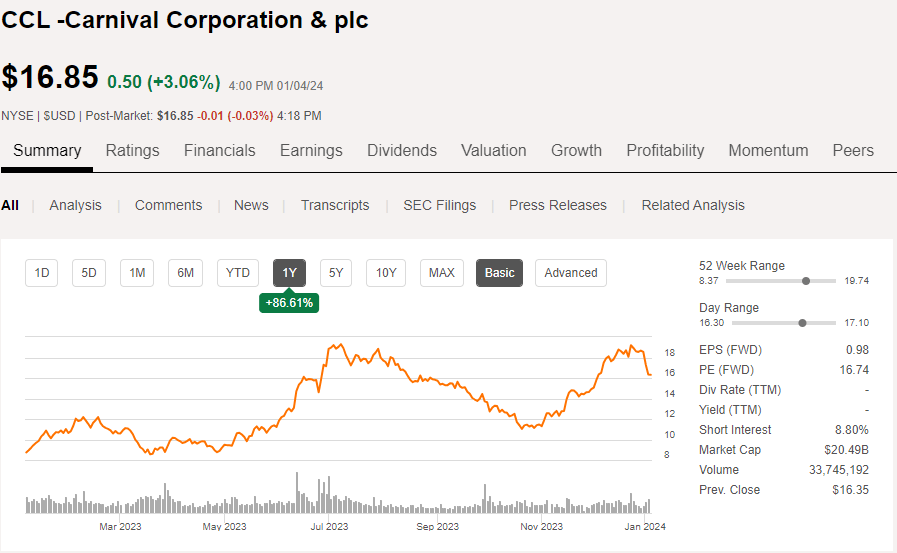

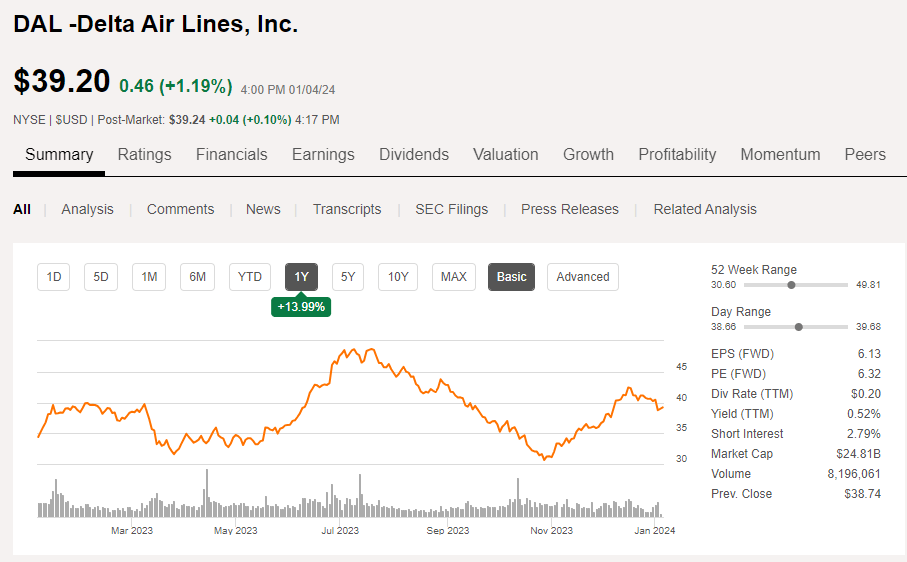

Asset correlations have increased in recent years, and 2023 was particularly correlated. Certain stocks were considered to fit certain categories, and those categories tended to trade up or down together.

EPR, as a high-risk entity, was lumped in with the basket of extremely risky investments. This group would trade up or down substantially on any given day depending on whether the market was feeling “risk-on” or “risk-off.”

The group consists largely of airlines, cruises, and crypto along with other high risk assets like theaters and hotels.

{kind=link}

{kind=link}

The idea is that these names have high betas such that they would be expected to outperform in a good market year.

Well, 2023 proved to be a strong year. The economy went from an expected recession to a soft landing, and the Fed went from hawkish to now looking like cuts in 2024.

Each of these events made the market happy, which played well for the high beta “risk on” stocks.

I suppose it worked as a speculative trade, but eventually the fundamental value of these companies will matter.

My hunch is that the whole group will underperform in 2024, but I don’t know enough about airlines or cruises to state that with any confidence.

Real estate, however, is something I am more familiar with valuing, and I have not seen any fundamental changes in EPR that justify the kind of price move it has had.

Fundamental troubles could manifest in a variety of ways:

- Tenant failure

- Rent rolldowns

- Vacancy upon leases expiring

- Dividend cut to fund capex of redevelopments.

I don’t think EPR is a bad company, but given the challenges inherent in their property sectors I think it will be tough. Its FFO multiple is only slightly lower than that of triple net peers that are in strong sectors like retail and industrial.

The quality delta is greater than the valuation delta. At its current multiple, I don’t think EPR investors are getting sufficiently compensated for the excess risk.

Wrapping it up

I’m optimistic for 2024. Real estate fundamentals are positioned well broadly with most sectors experiencing net operating income growth and construction activity moderating across the board. The properties already standing will have less competition as a result, which should lead to growth.

I believe the three ideas discussed above are well positioned heading into 2024.

For further details see:

3 High Conviction REITs For Early 2024