T - 3 High-Yield Dividend Stocks To Boost Your Income

2023-05-17 09:15:00 ET

Summary

- All three of these dividend stocks have dividend yields above 4%.

- The great thing about these dividend stocks is the fact that they offer high dividend yields at cheap valuations.

- A recession is imminent, as such, investors are looking for yield to increase their income.

The US economy is facing a potential recession in the coming months, so in the near term, yield is important. Retirees are especially impacted, as they live off yield, so looking for safe, reliable dividends are important.

In today's piece, we will look at three high-yield dividend stocks with yields above 4%. Not only do these stocks have a yield above 4%, but they also appear to be trading at a CHEAP valuation.

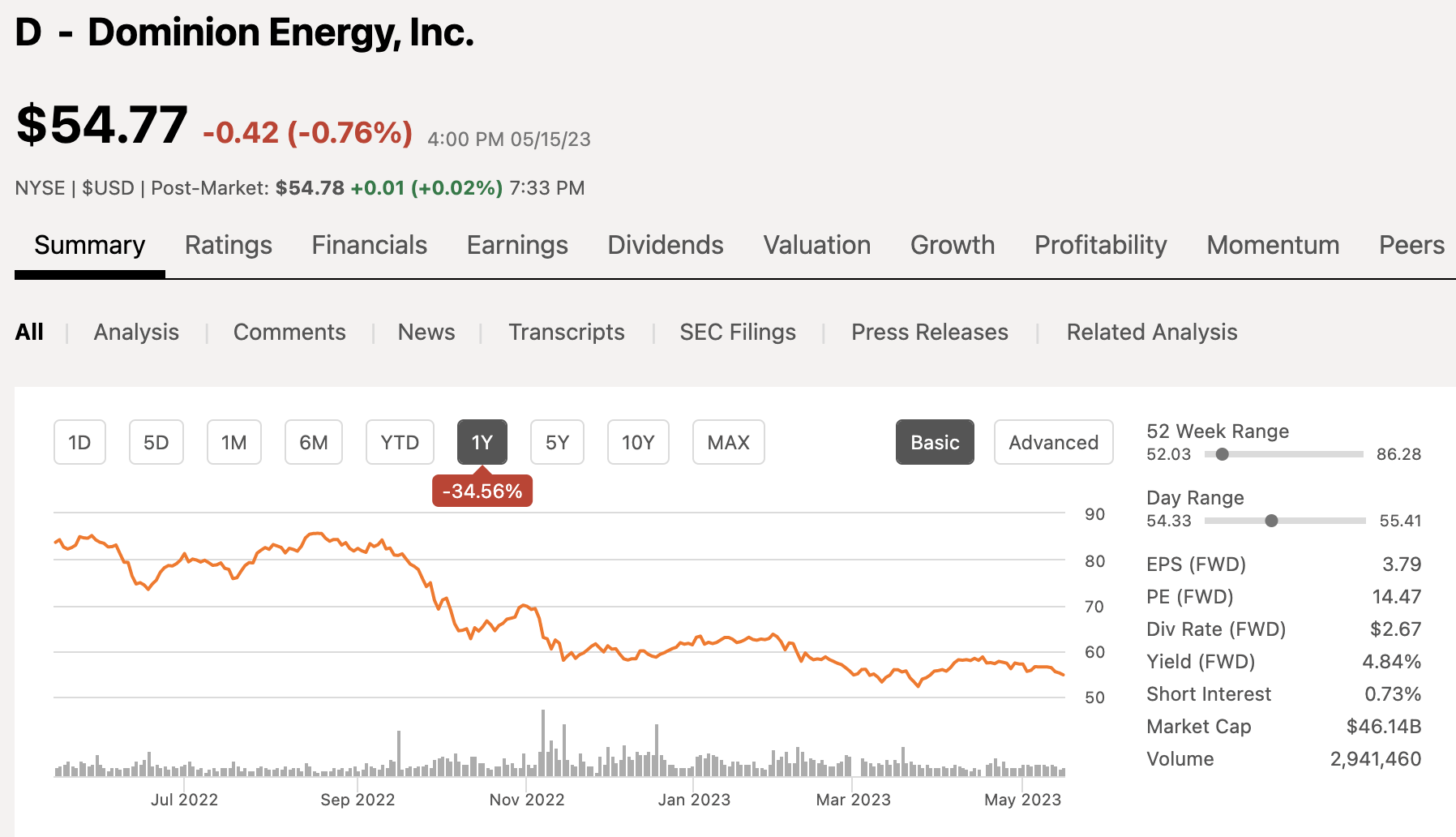

High-Yield Stock #1: Dominion Energy ( D )

Dominion Energy is an energy company that produces and distributes energy to nearly 7 million customers within the US. The company has a market cap of $46 billion and over the past 12 months, shares of D have fallen ~35%.

{kind=link}

Historically, utility companies are often steady as you go, slow growing companies. Dominion operates within a regulated industry and operates within 16 states, but its primary operations are within Virginia.

The stock is down roughly 35%, what happened?

Rising interest rates is what happened. These rising rates have really put heavy pressure on higher yielding stocks, especially utility companies like Dominion. Higher interest rates have increased interest rates among a multitude of different products, such as T-Bills and High-Yield Savings Accounts, which makes the higher yield space more competitive.

Rising interest rates from the Federal Reserve, have forced utility companies to pass on rate hikes to customers, but the speed of the rate hikes have been so fast that the companies have been unable to pass all these hikes onto the customers.

In addition, during the company’s Q1 earnings release, management presented a pretty dismal outlook for Q2, which came in well below analyst expectations. This also added additional pressure to shares of D.

So as you can see, there are some notable headwinds for Dominion, so shares certainly did not fall without reason. However, it appears (fingers crossed) that we are nearing the end of this Fed rate hike cycle, which will benefit a company like Dominion. They can continue to increase rates slowly without seeing interest rates rise faster. Also, if we fall into a recession, what better company to own than a utility company. People need to keep their utilities on regardless of the economic backdrop.

Given all of this, shares of Dominion are trading at a solid valuation, making the downside risk limited. One way I like to screen for cheap stocks is by comparing their current dividend yield to their 5-year average. After all, when a stock price falls, it dividend yield goes higher.

Dominion shares have a 5-year dividend yield of 4.2% and right now they sport a dividend yield of 4.8%.

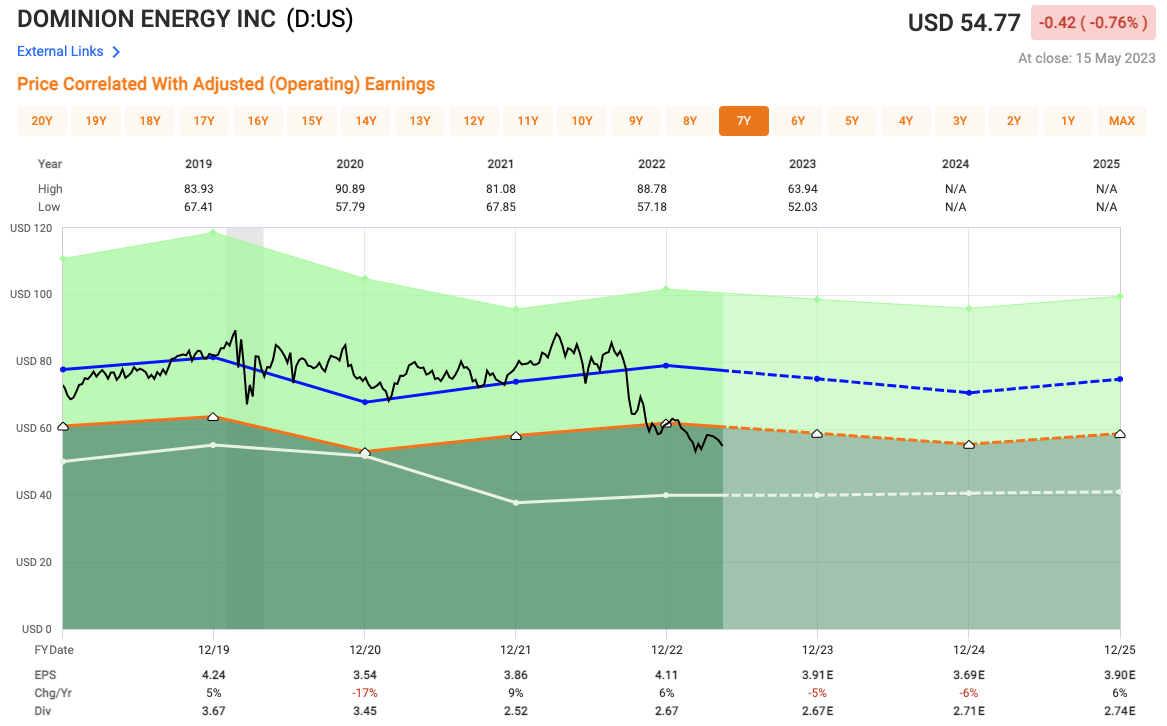

In terms of valuation though, look at just how low of an earnings multiple shares of D are trading at. Analysts are looking for 2023 EPS of $3.91, which equates to an earnings multiple of just 14.1x. Over the past five years, shares of D have traded at an average multiple of 19.2x. That is more than a 25% difference. The last time shares of D traded at a multiple that low was 2011.

{kind=link}

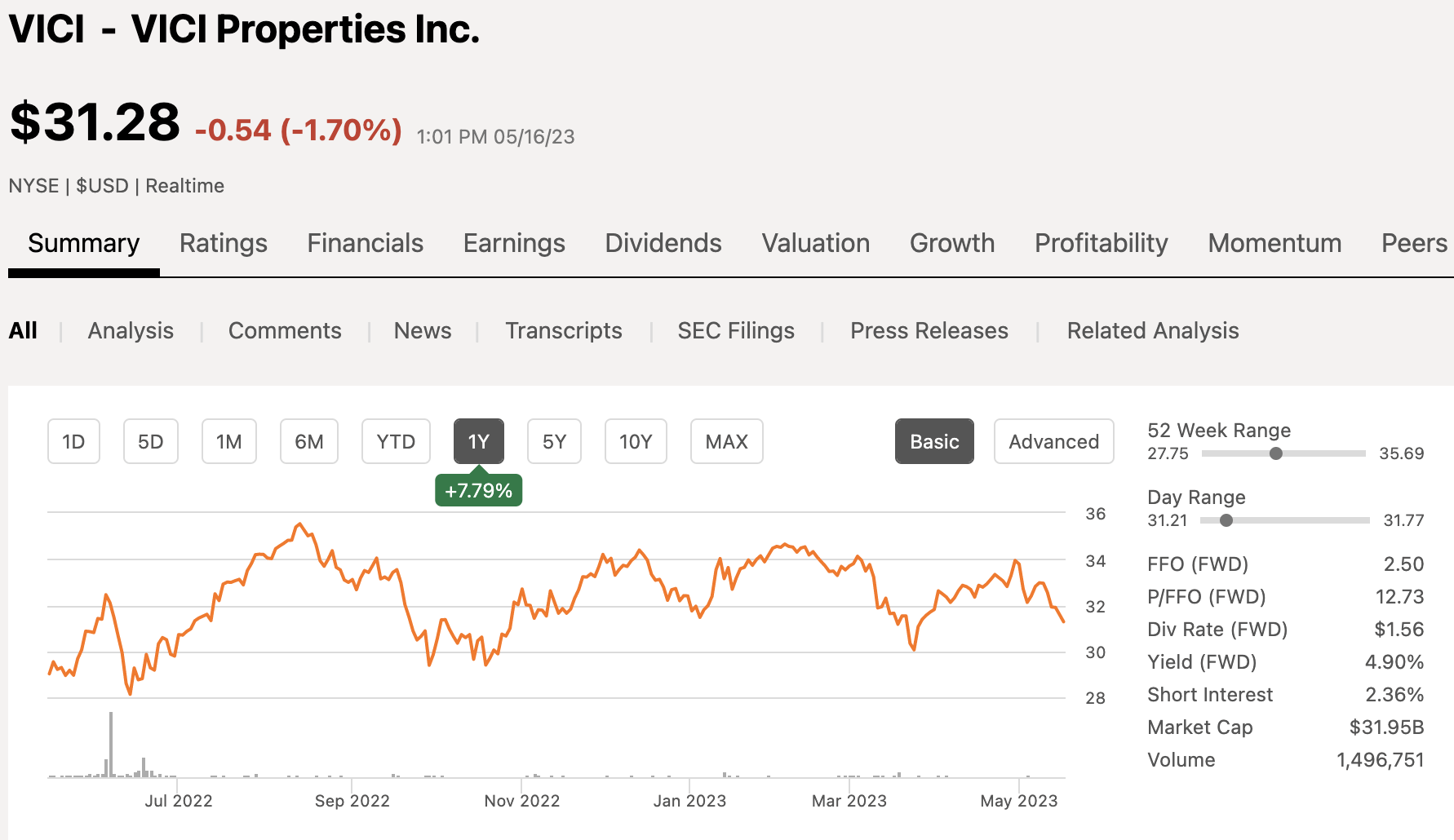

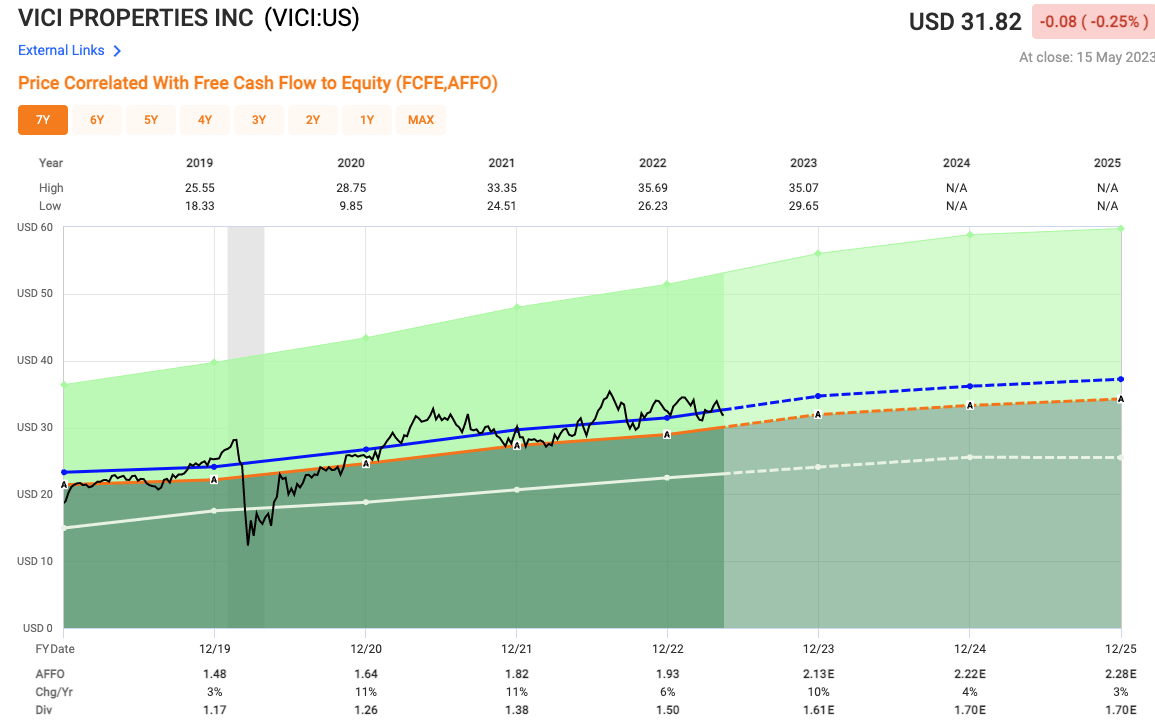

High-Yield Stock #2: VICI Properties ( VICI )

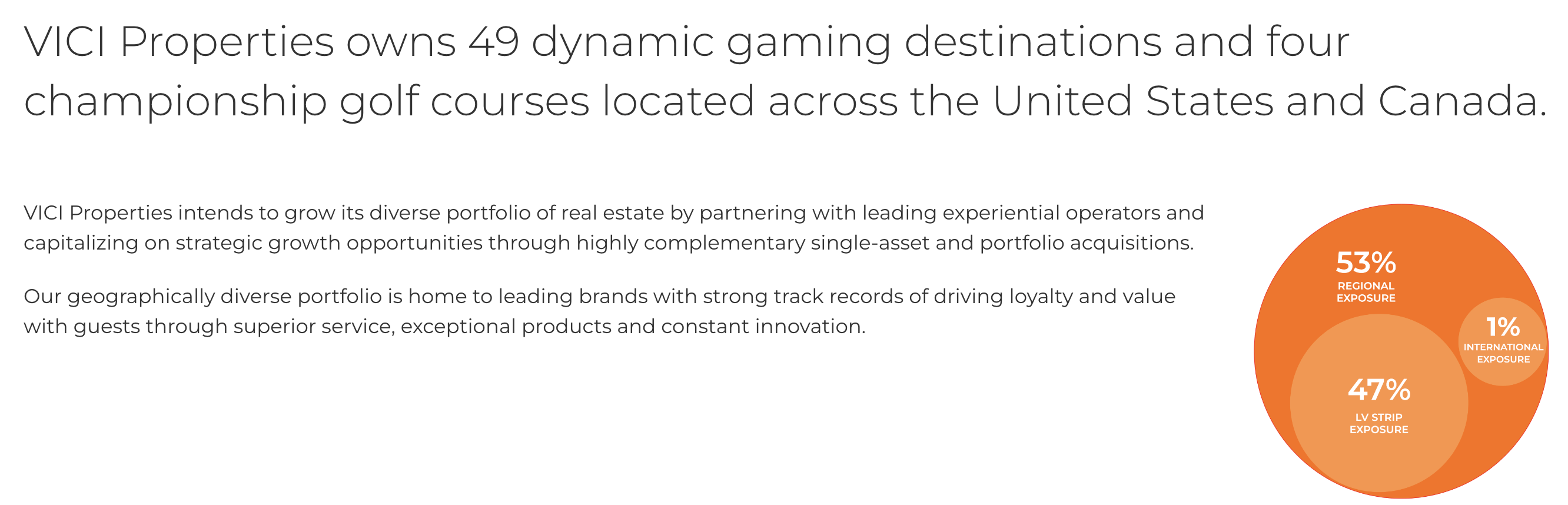

VICI is a REIT operating in the gaming and hospitality REIT, owning some of the best properties along the Las Vegas strip, and elsewhere across the US. The company has a market cap of $32 billion and over the past 12 months, shares of VICI have climbed 8%.

{kind=link}

VICI is known for being the largest landlord on the Las Vegas strip, owning properties such as:

- Caesars Palace

- MGM Grand

- The Venetian

- New York New York

- Mandalay Bay

In totality, the REIT owns 49 properties with 47% exposure to the LV strip.

{kind=link}

Owning great properties is just one piece of the puzzle, but you also have to have great operators, which is exactly what VICI has. VICI was in rare territory during the global pandemic as they were able to collect 100% of their rent, during a time when we saw REITs collecting 50% or less, even high-quality REITs like Realty Income ( O ).

Remember, even if we dip into a recession and operators see less activity at their casinos, although VICI wants their operators to always do well, they are more worried about collecting a rent check.

VICI currently offers a high dividend yield of 4.7%, and over the past two years, investors have also enjoyed dividend hikes of 8.3% and 9.1%, which is an added bonus to an already high dividend yield.

VICI has only been public since 2018, so investors are still working on what the proper valuation should be based on results, but the company continues to grow and expand at a nice clip.

Analysts are looking for VICI to generate AFFO of $2.13 in 2023, which would be a 10% increase over 2022. This equates to a P/AFFO of 14.9x and since going public the REIT has traded closer to 16.3x. The drop in the multiple is not due to stock price drop, as we saw at the start the stock is up 8% over the past 12 months, so this tells you how their AFFO has been growing steadily over the years.

{kind=link}

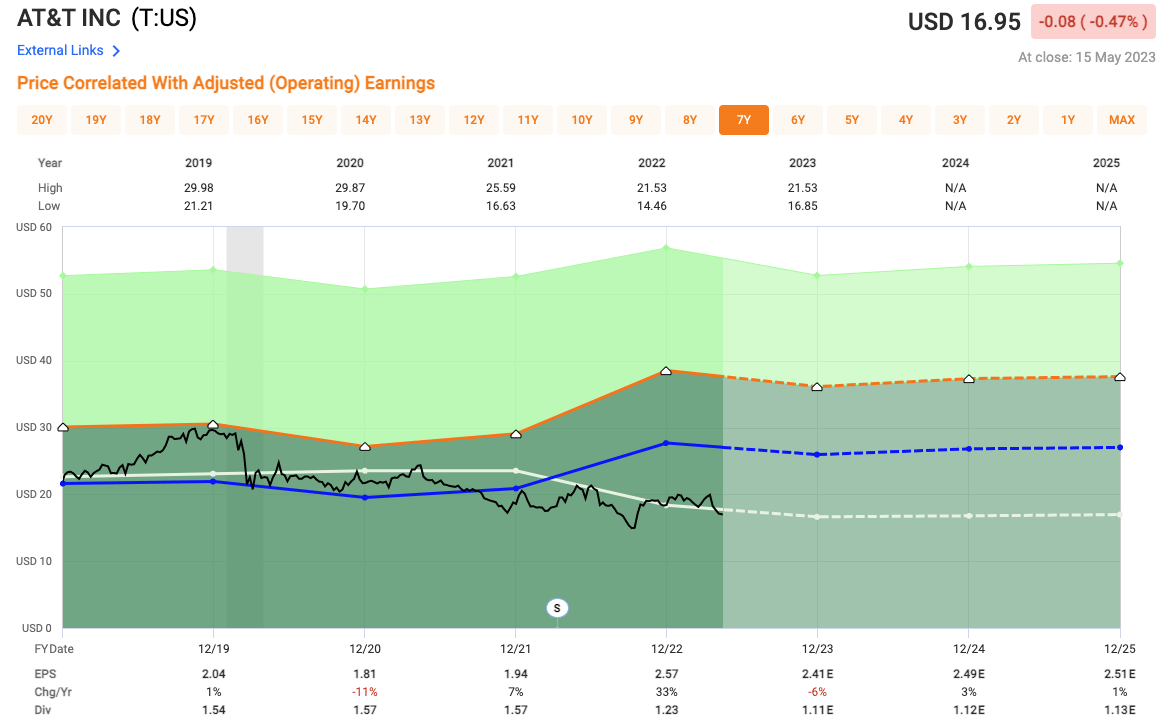

High-Yield Stock #3: AT&T ( T )

This final stock could be a little controversial, as it is a company I have vowed to stay away from for quite some time. AT&T is a stock I sold around $30 years back, and I am very thankful I did.

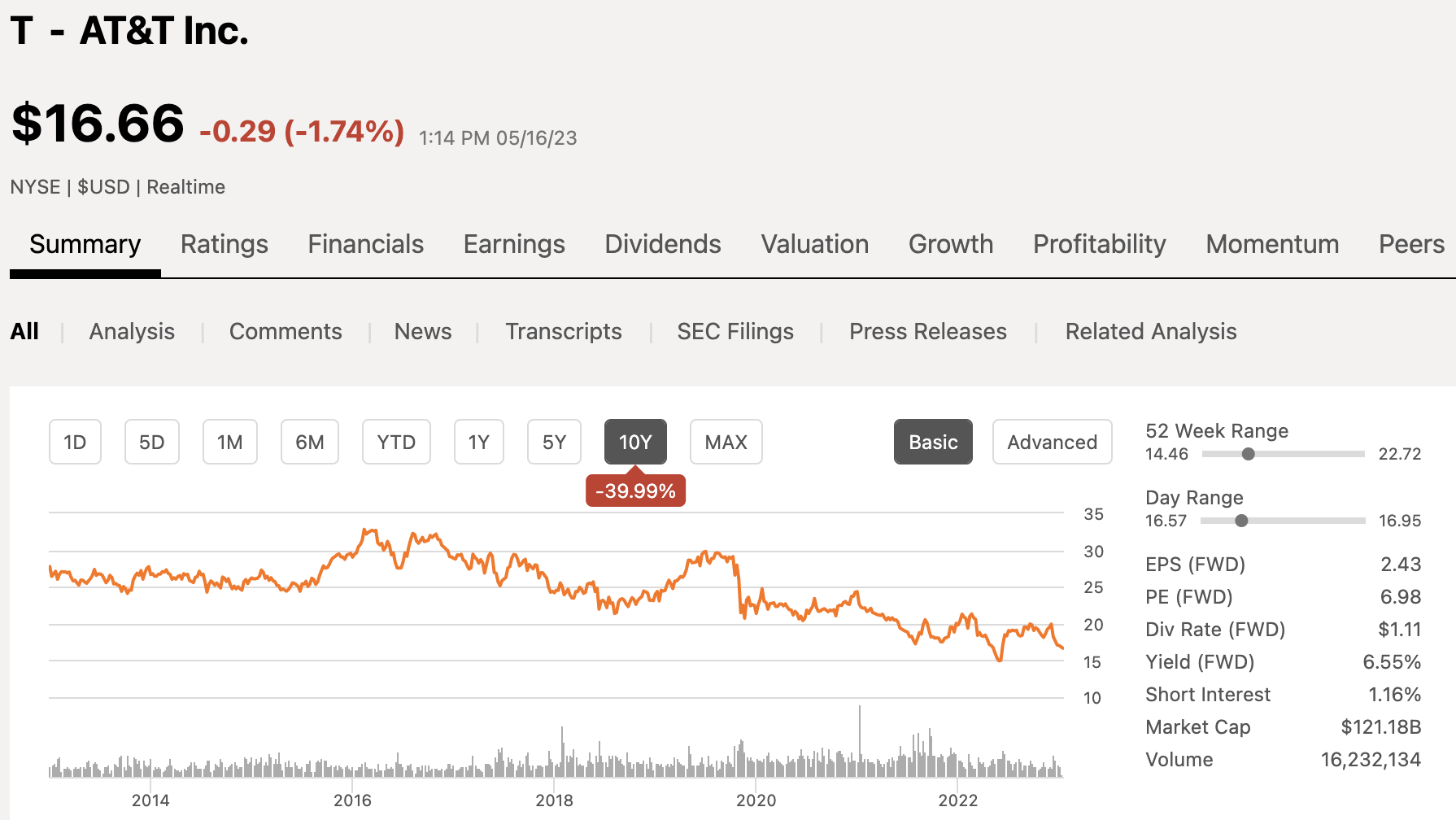

Today the stock trades closer to $17 and they have steadily fallen for much of the past decade. Over the past 10 years, shares of T have fallen 40%, while the S&P 500 has climbed nearly 150%, making it more of a lost decade for AT&T.

{kind=link}

The company has consistently gotten in its own way and try to take the company in directions they dividend need to. T shareholders have seen:

- Bad acquisition after bad acquisition

- Ballooning debt

- Poor management execution

The tone at the top and decisions from management were extremely poor. The current CEO, John Stankey, took over the CEO position in July 2020 and has since overseen the sales of a third of AT&T’s stake in Directv for $16.25 billion, which was an acquisition the company made years back for $67 billion, including debt.

In addition, Mr. Stankey has also oversaw the spinoff of WarnerMedia to Discovery Inc last year for $43 billion cash plus $59 billion in Discovery stock. AT&T paid $85 billion for WarnerMedia in 2018.

Mr. Stankey isn’t new blood to the company, which is something I didn't like when he was picked as the new CEO, but what I do like so far is that he is trying to make up for some of the past mistakes made by management by returning AT&T to its Telecom roots all while bringing down the MOUNTAIN of debt the company has incurred.

Debt is still my biggest concern, but management expects to generate $16 billion in FCF on the year , which will help pay the big dividend and help pay down debt. Total debt amounted to over $160 billion in recent years, but with the recent sales and spinoffs, they have been able to bring that down to $136 billion. Still a big number but PROGRESS nonetheless.

Management has a goal to hit net debt to EBITDA of 2.5x by 2025. Right now they are closer to 4x, so still plenty of progress to be made, but again moving towards a leaner more efficient company.

In terms of the dividend, AT&T shareholders earn a yield of 6.3%. The dividend has been a hot topic because last year AT&T slashed their dividend by nearly 50%, and yet you are still earning more than a 6% yield, which tells you just how under pressure AT&T shares have been.

The question I get a lot as it pertains to AT&T’s high dividend is whether it is a safe. Very valid question, especially considering the company paid out $2.1 billion in dividends in Q1 and only generated FCF of $1 billion, which means the company had to dip into cash reserves for the dividend. Not something dividend investors ever want to see. However, as I stated earlier, management expects the company to generate $16 billion in FCF, which would make up for the short falling in Q1.

Now for valuation. Analysts are looking for 2023 EPS of $2.41 which equates to an earnings multiple of just 7x compared to their 5-year average of 10.7x.

{kind=link}

AT&T still has plenty to work out, which is why it is likely the most risky of the three high-yield stocks we looked at today, but the valuation is quite intriguing at these levels if you believe in the turnaround story.

Investor Takeaway

Interest rates are high across the board, and with uncertainty in the economy in the near-term, investors are looking for quality yield. Equities have plenty of competition right now, given the higher interest rates, with less risk options like T-Bills and High-Yield Savings Accounts, but if you are looking for high-yield stocks, definitely take a closer look at these three.

COMMENT BELOW: Which of these three high-yield dividend stocks would you be MOST comfortable buying right now?

Disclosure: This article is intended to provide information to interested parties. I have no knowledge of your individual goals as an investor, and I ask that you complete your own due diligence before purchasing any stocks mentioned or recommended.

For further details see:

3 High-Yield Dividend Stocks To Boost Your Income