VGK - 3 Ideas For Value In A Market Where Value Is Hard To Find

2023-09-24 05:01:47 ET

Summary

- Gold remains a stable asset with solid gains, low volatility, and a history as a valid hedge.

- European shares still look cheap compared to the S&P 500, offering potential value.

- Investors may need to explore alternative strategies beyond a simple stock/bond portfolio for alpha.

Main Thesis & Background

The purpose of this article is to evaluate the broader market and to determine where some value may be hiding out. This is not specific to just equities, but rather a focus on all corners of global markets to determine where it makes sense to branch out to and/or move a little cash around. This thesis is useful to me personally because I see extended valuations in both the S&P 500 and the NASDAQ 100 - where the bulk of my net worth lies - as warning signs that a correction may be looming. As a result, I want to protect myself as best I can be staying diversified in the right way.

Of course, there are dozens of applicable hedges if one is looking to shift away from large-cap US equities. In this review I focus on three that have merit based on low volatility, valuation gaps, or strong growth potential. I will discuss the three that have caught my eye recently in detail below.

Gold Has Been Profitable & Steady

The first asset class I want to touch on is precious metals. In particular, I see merit to owning gold now and going forward in to 2024. This is because of its status as a safe haven - but that is true in most cycles. I also prefer it for two other reasons at this moment. The first is that it has been having a strong year, but recently the price has been trading in a narrow range. That tells me there has been strong underlying support, and also a nice basement floor price that should limit losses in the short-term at least:

Gold Spot Price (Seeking Alpha)

Beyond this price action in isolation, the second attribute that caught my eye is that volatility for gold has been declining. Throughout 2023 this has been a consistent theme and that is precisely the type of asset I am looking for as a stable rock holding in my portfolio:

Volatility ( GOLD ) (Yahoo Finance)

{kind=link}

As you can see, gold has been trading very passively for the second half of the year. While that can sometimes be viewed as a warning sign that more volatility is one the way, I think this trend will be tested for a little while longer. With central banks nearing the end of their rate hike cycles in both the US and EU, two major players in the precious metals space, I can't see gold's volatility spiking higher unless those central banks really catch investors off guard. That hasn't been the case in most of 2023, so I don't see why Q4 is going to be much different.

The bottom-line for me is that gold remains a stable asset and it is actually more stable right now than it has been in years past. With solid gains, low volatility, and history on its side as a valid hedge, I see a continued buy case for gold going forward.

**I have a position in the iShares Gold Trust ETF ( IAU ). Another popular option is SPDR Gold Shares ETF ( GLD ). A third fund for consideration that I have discussed positively in past reviews is the Sprott Physical Gold and Silver Trust ( CEF ). That fund is more diversified because it holds silver as well.

Euro-zone Stocks Look Cheap, Weak Currency Helps Outlook

The next topic for consideration is European shares. In particular, a diversified basket of large-cap Euro stocks, which are a good compliment to the S&P 500. I will be honest in saying this is a play I missed out on in 2023. I saw continued headwinds across the pond as a reason to focus more on North American shares (US and Canadian), but European markets caught me by surprise and have had a resounding comeback in 2023. This makes me a little late to the game, but that is spilled milk and under the bridge. Looking forward, we have to decide if these gains can continue regardless of what has happened in the past.

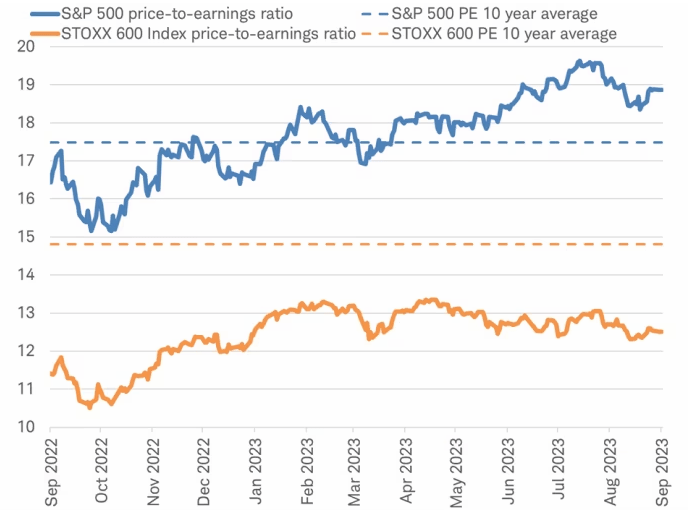

In this vein, I see a buy case still brewing. Relative to the S&P 500, the European shares still look very cheap. In addition, the STOXX 600 index is not only heavily discounted to the S&P 500 in terms of P/E, it is well below its own 10-year average (in terms of P/E). That shows there is still a lot of value under the surface, even with the rapid increase in share prices this calendar year:

Relative Valuations (S&P 500 vs. STOXX 600) (Charles Schwab)

{kind=link}

Of course, this isn't always a "good" thing. The low P/E multiple suggests investors expect weaker earnings compared to both history and the US. If that turns out to be correct, than don't expect the P/E spread to narrow in any significant way. Further, a weaker growth/weaker earnings environment is not going to drive the P/E higher for Euro stocks in isolation either. My point being that while there looks to be a lot of inherent value here, that can sometimes be misleading, so weigh any buy decision carefully.

However, I believe this value is a definitive opportunity for a couple reasons. One, Euro stocks have a higher concentration of Consumer (especially luxury goods) and Industrial holdings than their S&P 500 counterparts. This makes the sector more reliant on trade and exports than the U.S. (and other countries). A trend that is helping to boost my confidence in those sectors is the decline in the Euro. The currency has been in decline that last few months quite consistently:

Euro's Price (in USD) (Bloomberg)

{kind=link}

While some might argue this isn't "good" either, my premise is this is a positive for exporters and retailers that sell goods to the public overseas. Again, luxury exporters and other manufacturers are now able to compete more aggressively with their peers because their currency is worth less - meaning consumers outside the Euro-zone can buy more goods with the same amount of their own local currency. This could provide a much needed boost to the demand side of the equation, and help European corporates perform reasonably well heading in to the end of the year.

**Two good options for large-cap European shares are the SPDR Euro STOXX 500 ( FEZ ) and the Vanguard FTSE Europe ETF ( VGK ). I may initiate a position in one or both of these funds in the next 72 hours.

Domestic Small-Caps Haven't Kept Up

Looking closer to home for the third place of value is small-cap US stocks. This is a more risk-on play - so unlike good or even large-cap Euro corporates - readers should approach this idea more cautiously. It may not be for everyone, so I want to be upfront about that from the get-go. However, for those who see the opportunity for diversification and potential growth, small-caps are an interesting play here.

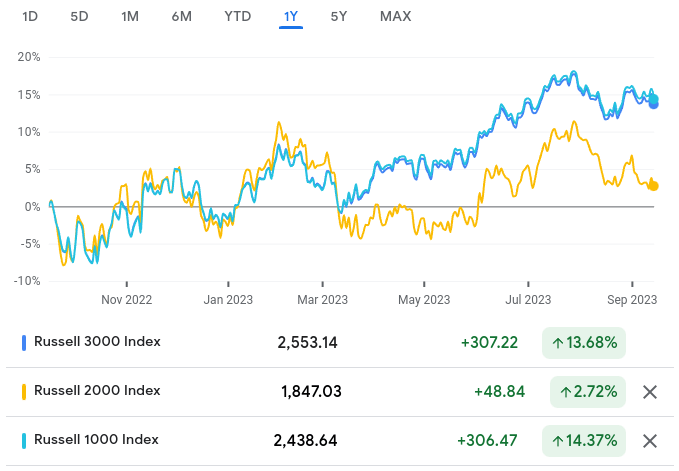

The primary reason has to do with relative performance. If we look at the Russell 3000 - an index that captures the "entire" US stock market - we see a solid year in 2023. However, the gains between the large-caps in the Russell 1000 index, compared to the small-caps in the Russell 2000 index (the two indices combine to make the Russell 3000), we see a tale of divergence:

1-Year Performance (Google Finance)

{kind=link}

This got me thinking - how unusual is this spread and could it reverse in the months ahead?

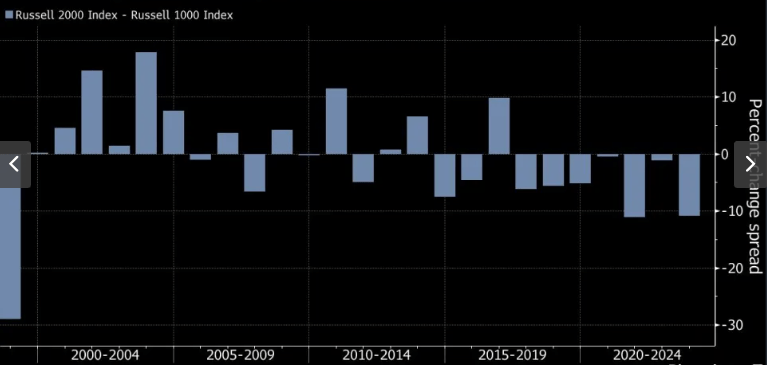

To gauge the likelihood of this, I went back to history. It is true that large-caps have tended to out-performance, especially in the last decade. But even with that understanding, this year's spread is quite wide. In fact,

Annual Performance of Russell 2000 Index (less Russell 1000) (FactSet)

{kind=link}

This is not an automatic buy signal. As I'm sure my followers know, trends like this can continue for a long time. But the subject of this piece was value - and small-caps seem to be registering plenty of value in terms of relative performance against their large-cap peers at the moment. This has piqued my interested to say the least.

What I view opportunistically about this is that small-caps may be pricing in some of that negative economic news that large-caps (especially in Tech) seem to be ignoring. This could limit downside if we do get bad news ahead, and could also set the stage for plenty of upside if what has been priced in (bad news) does not occur. That offers a fairly straightforward risk-reward proposition that I find favorable.

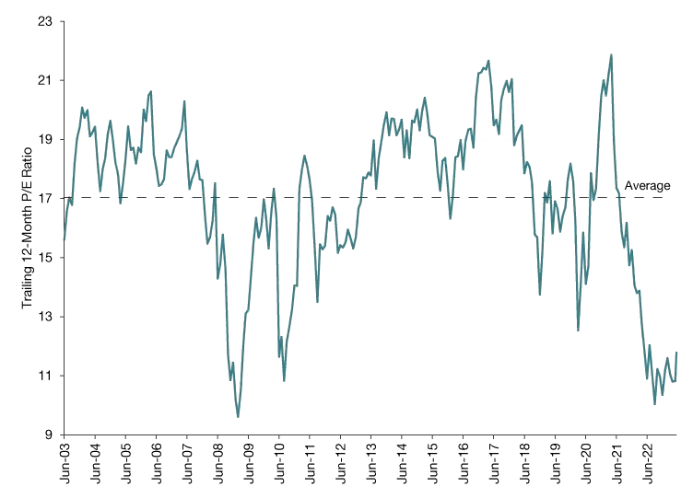

And it isn't just in relative terms that small-caps look cheap. By their own standard they are offering investors a substantial discount to historical norms if they bought in now:

Russell 2000 Index (Trailing 12 Month P/E) (Lord Abbett)

{kind=link}

Given the point of this review was to find "value", I don't see how I could have left small-caps off the list. This presents a classic value-oriented play at the moment.

Beyond just valuations and relative cheapness, readers may find small-caps fit the bill for another reason. This is diversification. That may sound obvious, since small-caps would naturally be different than large-caps. But it isn't just in terms of size. The sector compositions vary greatly between the two and that means small-caps can help round out a portfolio (like mine) that is large-cap heavy and, thus, Tech-heavy:

Sector Breakdown Comparison (Fidelity)

This strikes me as a win-win in terms of rounding out my portfolio and prepping for some upside. For this reason I am definitely looking to branch in to some small-cap exposure in the near term.

**There are numerous ways to play US small-caps. Two popular ETFs include the iShares Core S&P Small-Cap ETF ( IJR ) and the Vanguard Small-Cap Index Fund ETF Shares ( VB ). I may initiate a position in either in the next 72 hours.

Bottom Line

The US equity market has proved resilient and I will remain long my core index holdings going forward. However, I think the valuation backstory and the potential for a Fed "higher for longer" environment means it is time to look elsewhere for value too. In this review I have touched on three reasonable ways to do just that.

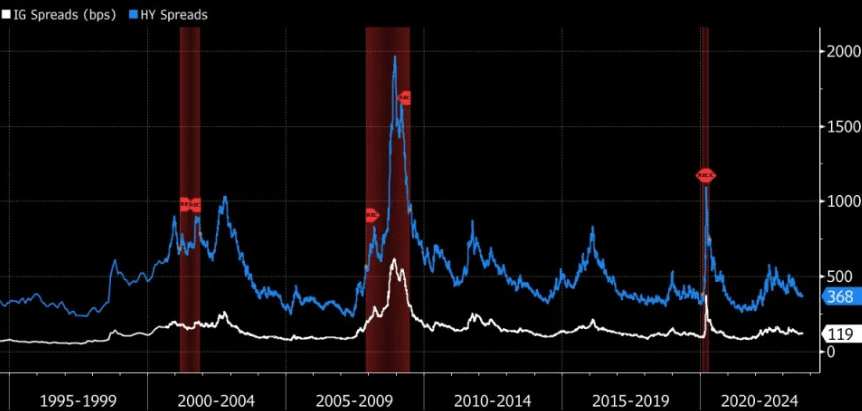

I believe this is an important discussion because the days of just diversifying with bonds are no more. Bonds have had a rough year and a half and, despite the losses in most fixed-rate sectors, spreads are not indicating value there:

Corporate IG and HY Spreads (US) (S&P Global)

{kind=link}

The thing I am trying to convey here is investors may have to get a bit more creative than a simple stock/bond portfolio if they want "alpha". The sectors I touched on in this review could do just that under the right circumstances, and I am willing to take a bit of a gamble on it going forward. Hopefully this review gives my followers some food for thought as we wrap up another interesting year in both the global economic and political markets.

For further details see:

3 Ideas For Value In A Market Where Value Is Hard To Find