LQD - 3 Investment-Grade Bond Trends Impacting LQD

2023-08-03 07:10:17 ET

Summary

- Federal Reserve rate hikes have led to higher interest rates across fixed-income markets.

- The exact impact varies according to the sub-asset class.

- A look as to how rates have impacted investment-grade corporate bonds, specifically, follows.

Federal Reserve hikes have led to higher interest rates across fixed-income markets, and to higher dividends for most bond funds. Specifics vary, with some fixed-income sub-asset classes seeing stronger dividend growth, higher spreads, and lower capital losses than others. I thought to focus on investment-grade bonds for this article, due to the strong credit quality and competitive yield of these securities.

Investment-grade corporate bonds currently sport moderately higher interest rates than average, and very slightly higher spreads too. Term premia is negative, as the yield curve is inverted, on expectations of sizable rate cuts next year. In my opinion, under current conditions, focusing on higher-yielding, shorter-term bonds is best.

I'll be focusing on the iShares iBoxx $ Investment Grade Corporate Bond ETF ( LQD ) for the rest of this article, but everything here should apply to most investment-grade bond funds in roughly equal measure.

LQD - Quick Overview

LQD is an investment-grade corporate bond index ETF, tracking the Markit iBoxx USD Liquid Investment Grade Index , an index of these same securities. It is a relatively simple index, investing in all relevant securities meeting a basic set of liquidity, maturity, issuer, and credit quality criteria. It excludes issuers from developing countries, as well as floating rate securities.

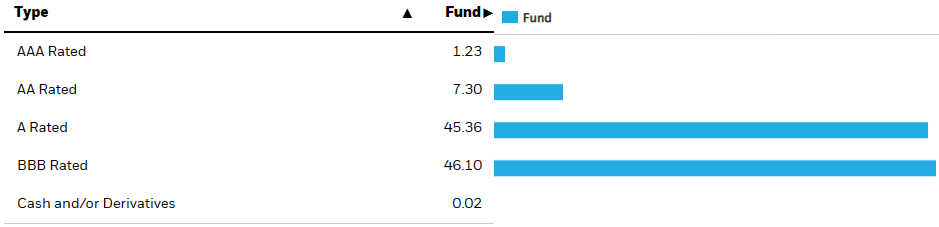

LQD's underlying index is quite broad, resulting in an incredibly well-diversified fund. LQD invests in 2630 securities, from most relevant industry segments. Credit quality is above-average, with most of the fund's underlying holdings sporting A-BBB ratings.

{kind=link}

LQD is the largest investment-grade corporate bond ETF in the market, and provides investors with broad-based exposure to the same. Due to this, I'll be using the fund as a stand-in for its asset class moving forward.

Investment-Grade Corporate Bond Trends

Higher Interest Rates

Interest rates rose through all of 2022, and most of 2023, as the Federal Reserve hiked rates to combat surging inflation. Federal Reserve funds rate rose from effectively zero in early 2022, to 5.00% - 5.25% as of today, an aggressive, fast-paced set of rate hikes. Fed officials expect one or two more hikes this year, stability for the rest of the year, and cuts in late 2024.

Higher Federal Reserve rates led to higher interest rates on almost all newly-issued bonds, including those bought by LQD.

As the interest rate on (some of) LQD's underlying holdings increases, so does the fund's generation of income, ultimately resulting in higher dividends for the fund and its shareholders.

LQD's dividend yield also increased, from around 2.25% in early 2022, to around 3.50% as of today.

Go through the figures above, and you'll see that LQD's yield increased by less than interest rates rose. This is because it takes quite a bit of time for higher interest rates to lead to higher dividends for bond funds. Funds must generally wait for their older, lower-yielding bonds to mature to buy newer, higher-yielding bonds, and funds must then wait for these newer bonds to start paying interest before distributing the proceeds to shareholders. The process is proceeding at good pace, but could take years to play out.

Higher interest rates boost LQD's yield, benefiting the fund and its investors.

Very Slightly Wider Spreads

LQD focuses on A-rated and BBB-rated corporate bonds, which trade with spreads to safer securities of comparable maturities (treasuries and some mortgage-backed securities). Spreads vary, depending on economic conditions and investor sentiment. Spreads have risen these past few years, and are currently slightly higher than historical averages.

Data by YCharts

I'm not actually sure why the above occurred, but investors shifting into t-bills and other high-quality, short-term assets seem likeliest. When t-bills yielded 0%, risk-averse investors bought investment-grade corporate bonds, seeking at least a bit of income. When t-bills yielded 5.0%, risk-averse investors bought t-bills, and ignored investment markets. The shift meant lower demand for investment-grade corporate bonds, leading to wider spreads.

Higher spreads benefit LQD and its investors, and make the fund a more attractive choice relative to peers. Do bear in mind, spreads are only marginally higher, so the overall impact is quite small, if positive.

Negative Term Premia / Inverted Yield Curve

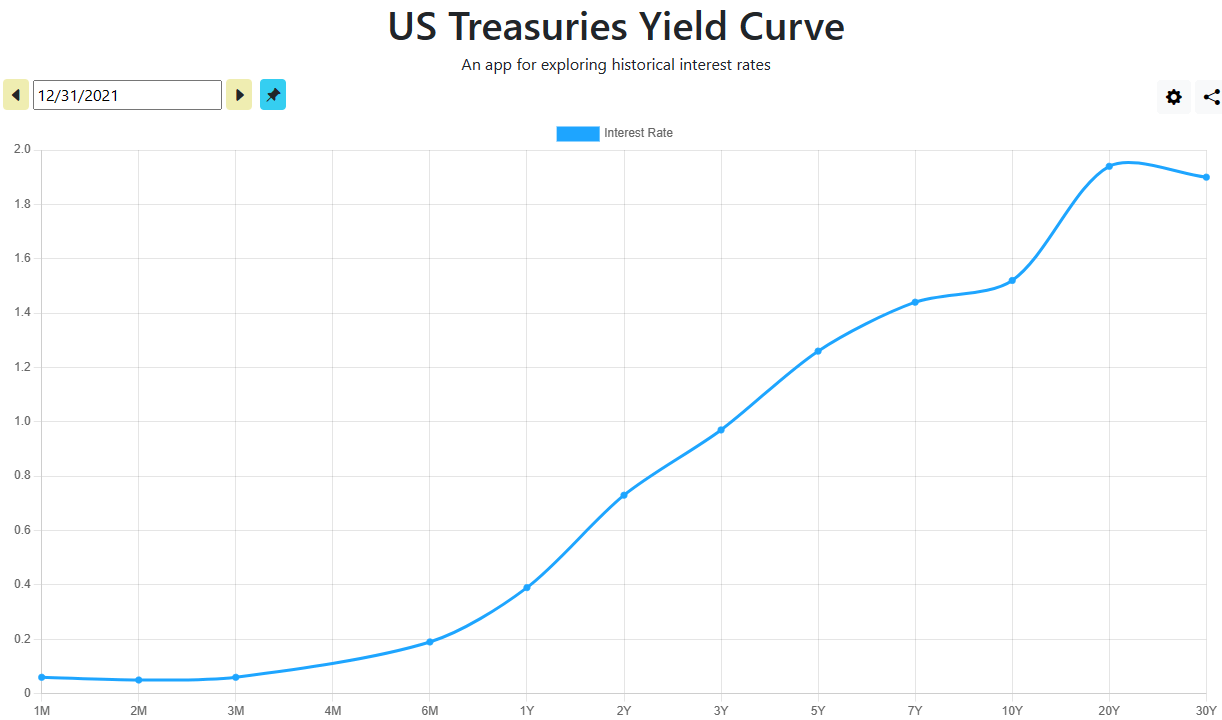

In the vast majority of cases, long-term bonds have higher interest rates than comparable short-term bonds, to compensate investors for increased interest rate risk, and for locking-up their cash for longer periods of time. As an example, a quick look at U.S. treasury curves in early 2022, before recent Fed hikes.

{kind=link}

As can be seen above, longer-term treasuries tended to have higher interest rates than shorter-term treasuries, as one would expect.

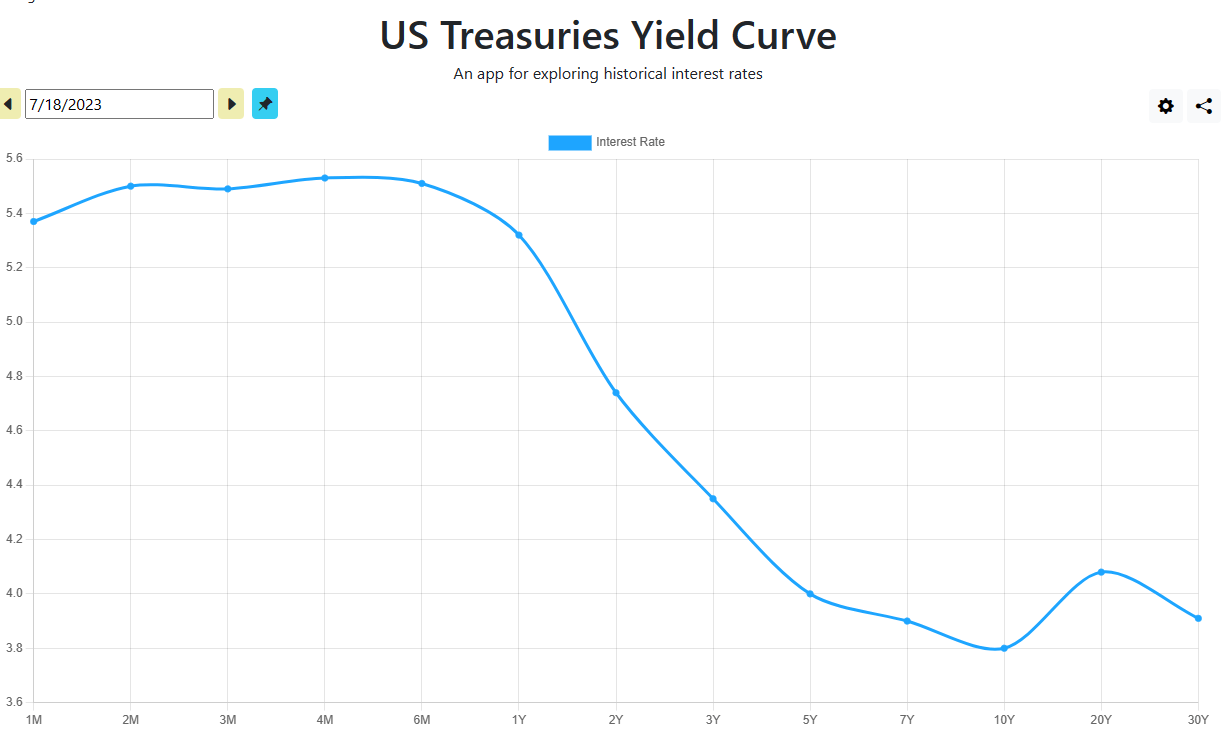

Although the above is generally true, there are exceptions, and we are currently living through one. Right now, longer-term treasuries tend to yield less than shorter-term treasuries, with some slight exceptions.

{kind=link}

The above has a relatively simple explanation: inflation is plummeting, so investors expect rate cuts in the coming years, and are pricing treasuries accordingly. Sure, 10Y treasury yields are less than a t-bill right now , but that is unlikely to be the case for the next ten years, or so investors believe.

An inverted yield curve means that longer-term securities yield comparatively less, making them less attractive investment opportunities. LQD focuses on longer-term securities relative to most other bond index ETFs, so is negatively impacted by these trends.

Fund Filings - Chart by author

On a more positive note, LQD's securities would almost certainly see higher capital gains if interest rates were to plummet. With inflation plummeting, rates could easily follow next year. Do bear in mind that markets expect a few rate cuts next year, and that securities are priced accordingly. LQD is unlikely to see any gains if rates slightly decrease next year, although much will depend on how sentiment develops.

In my opinion, as markets are already pricing-in several rate cuts next year, expecting bonds to increase in price next year seems misguided, and risky. It could happen, but only if rate cuts come higher than expected, or if markets expect that to be the case. Would not bet on this, even though at least some rate cuts seem exceedingly likely.

Conclusion

Investment-grade corporate bonds currently sport moderately higher interest rates than average, and very slightly higher spreads too. Term premia is negative, as the yield curve is inverted, on expectations of sizable rate cuts next year.

In my opinion, under current conditions, focusing on higher-yielding, shorter-term bonds is best. LQD focuses on longer-term securities, so I am not investing in the fund at the present time.

For further details see:

3 Investment-Grade Bond Trends Impacting LQD