O - 3 Monthly-Paying Bargains For My Grandson

2023-09-15 07:00:00 ET

Summary

- I'm investing in REITs for my grandson's future financial security.

- We highlight three dividend stocks that we believe are stable and have the potential for long-term growth.

- We emphasize the power of compounding and reinvesting dividends for maximizing investment returns.

Yup, everyone!

That’s right!

I’m talking about Asher again.

He’s nearing the year-and-a-half mark at this point, and man is he fun to interact with.

I know.

I know.

I’m his grandfather, not his parent.

So I don’t have to deal with the poopy diapers and inevitable toddler meltdowns.

Then again, I deserve that care-free status after dealing with my own kids’ (Asher’s mom, included) diapers and drama.

Five times over.

I’ve done my time and, technically, I'm still doing it considering how I’ve still got two kiddos in the house.

Though I will admit to enjoying some added ease now that they’re all driving themselves instead of relying on me for their busing needs.

For all of you parents and grandparents out there, I’m sure you understand what I mean.

No explanation necessary – including how I don’t resent my children for all the time, money, and effort they required.

Far, far from it.

“A parent’s love for their children can be one of the most genuine sources of unconditional love” that exists – “likely a bond that no other person could break.”

Part of this is biological, of course.

If we want our species to continue, we can’t just have kids.

We need to nurture them as well.

But there are so many more reasons than that why we want our children to not just survive… but thrive!

And the following three dividend picks can help make that happen.

3 Dividend Stocks for Everyone, in Fact

A point of clarification in case you don’t have kiddos or grandkiddos to think about…

These picks can still be of great benefit to you.

The REIT and BDC sectors usually are thanks to:

- Conservative business model

- Steady stock price growth

- Higher-than-average dividends and dividend growth.

Do some REITs and BDCs stumble, fall, and even fail?

Of course.

There's no perfect investment category out there any more than there’s a perfect investment.

We know that from the 2020 shutdowns.

And we’ve seen continuing weakness in a number of REITs three years after the shutdowns stopped.

But the majority of them are built and managed to last.

Considering the possibility of mergers and acquisitions – and the general uncertainty of life – I can’t tell you they’re going to be around in 50 years.

Or even in 2024.

But I did select the most stable, sturdy, and steady stocks around for Asher: The kind of companies with the kind of dividends that could and should accumulate year after year after year.

That’s why I titled the article “3 Dividend Stocks for My Grandson.”

Because if I invest in them for him now, they have an absolutely amazing chance of being worth a lot by the time he graduates from college.

And if he holds them until he retires?

Man, his golden years be shiny!

That is if he reinvests the dividends these REITs offer every time they pay out. (Or I do it for him.) That kind of compound appreciation can take you further and further the longer you stick with the plan.

2 Solid Dividend Reinvestment Success Stories

Dividend.com gave two great examples of how “long-term enrolling” in a dividend reinvestment plan, or DRIP, “can increase the value of an initial investment substantially.” And they’re real ones, not hypothetical.

Here’s the first:

“If you had $2,000 invested in Pepsi (PEP) in 1980, that would be worth more than $150,000 by the end of 2004. You would have started with 80 shares, but by reinvesting dividends, you’d now have 2,800 shares.”

Here’s the second:

“If you had $2,000 invested in Philip Morris in 1980, that would be worth just under $300,000 by the end of 2004. You would have started with 58 shares. Today, thanks to stock splits and reinvesting dividends, you now would have more than 4,300 shares.”

Shares that are all producing dividends. Don’t forget that.

Pepsi’s 24-year dividend results would pay for the $36,436 that Education Data Initiative says a student can expect to pay per year for college, “including books, supplies, and daily living expenses.”

Of course, that was as of June 25, 2023. And Asher won’t be in college until at least 2040. In which case, who knows how expensive things are going to get.

As the site adds: “The average cost of college has more than doubled in the 21st Century, with an annual growth rate of 2% over the past 10 years.”

Even so, that’s why you hold more than one REIT in your portfolio. One of the reasons, that is.

With all that established, let’s get to my three dividend stocks for Asher.

Realty Income ( O )

Realty Income is a real estate investment trust (“REIT”) that specializes in the acquisition and ownership of single-tenant, free-standing commercial properties.

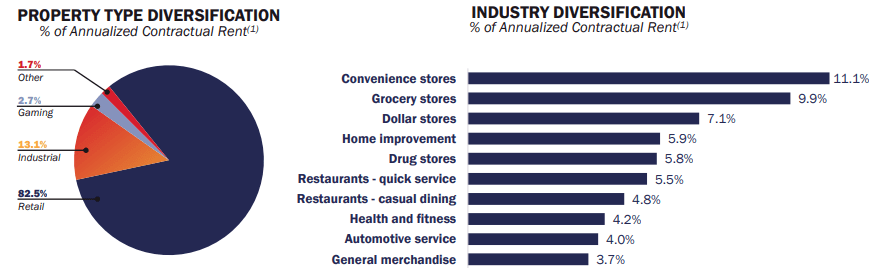

They typically acquire properties through sale-leaseback transactions and lease out their properties on a long-term, triple-net basis. The company primarily invests in retail properties, which makes up 82.5% of their annual rent, but they also invest in industrial and gaming properties, which makes up 13.1% and 2.7% of their annual rent, respectively.

They target properties in industries that are insulated from the threat of e-commerce such as grocery stores, pharmacies, and convenience stores and are well diversified by tenant, with their top tenant (Dollar General) only making up 3.8% of their annual rent.

Realty Income’s portfolio consists of 13,118 commercial properties covering approximately 255.5 million square feet of leasable space with properties located in all 50 states, the U.K., Italy, Spain, and Ireland.

Their properties are leased to roughly 1,300 tenants that operate in 85 different industries and as of the end of the second quarter their portfolio had a weighted average remaining lease term of approximately 9.6 years and an occupancy rate of 99.0%.

{kind=link}

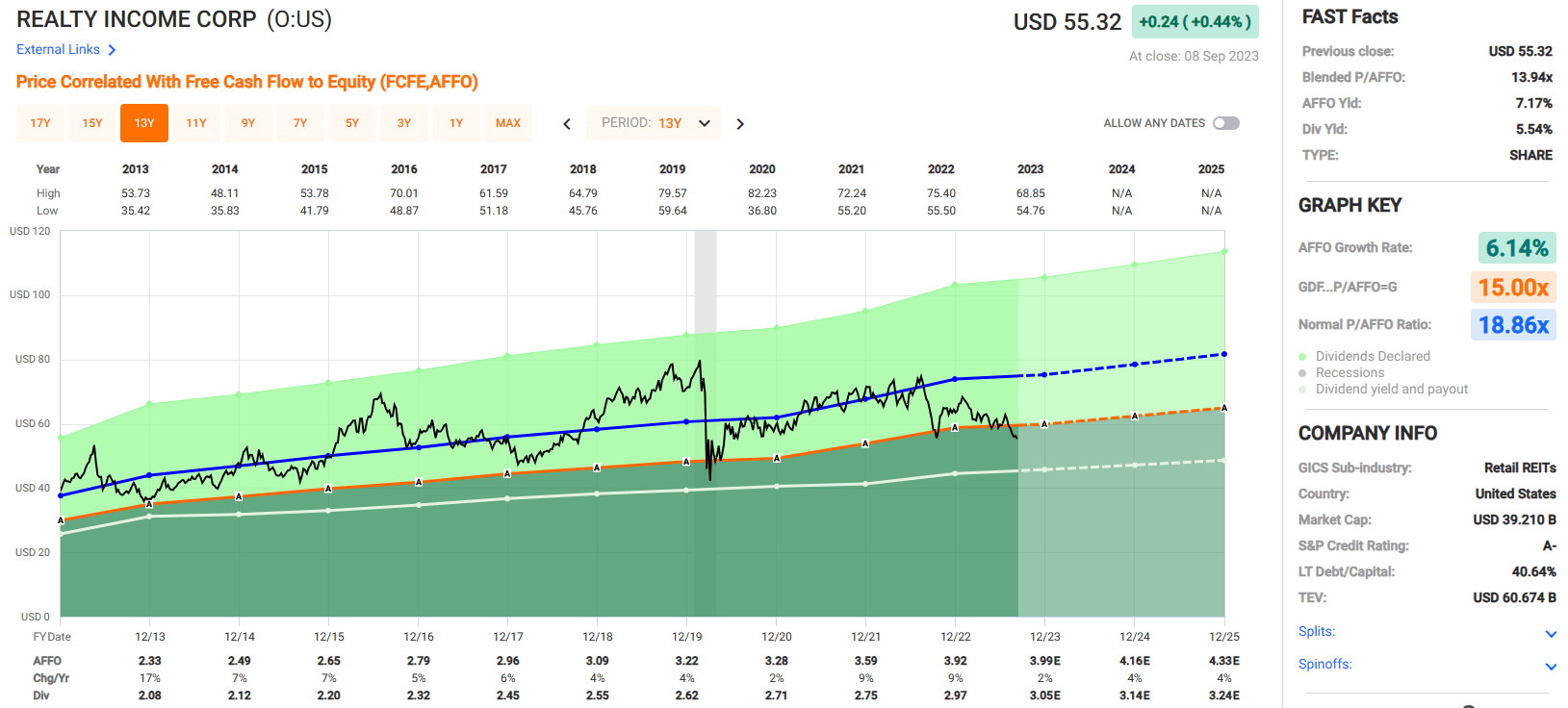

Realty Income pays a monthly dividend that's supported by the diverse stream of rent checks they receive from more than 13,000 properties and their investment-grade balance sheet.

They have an A- credit rating from S&P Global, a net debt to pro forma adjusted EBITDAre ratio of 5.3x and a fixed charge coverage ratio of 4.6x.

Realty Income has paid 638 consecutive monthly dividends since its formation in 1969 and has increased their dividend for 29 consecutive years and 121 times since their initial public offering in 1994.

O - IR

Realty Income has been extremely consistent and reliable as it has produced positive adjusted funds from operations (“AFFO”) growth in 26 out of the last 27 years and has delivered a median AFFO growth rate of 5% since 1996.

Their steady growth in earnings has supported their dividend, which has a compound annual growth rate of 4.4% since 1994.

Between their monthly distributions and stock appreciation they have delivered compound annual total returns of 14.2% with half the volatility of the broader market with a beta of 0.5 since their public listing in 1994.

Realty Income pays a 5.54% dividend yield that's secure with an AFFO payout ratio of 75.69% and trades at a P/AFFO of 13.94x, which is a significant discount compared to their 10-year average AFFO multiple of 18.86x.

We rate Realty Income a Buy.

{kind=link}

Main Street Capital ( MAIN )

MAIN is an internally managed business development company (“BDC”) that specializes in providing equity and long-term debt capital to lower middle market businesses which are companies that typically have annual revenues ranging between $10 million and $150 million.

MAIN also provides private loans and debt capital to middle market businesses which are generally larger than their lower middle market portfolio companies. MAIN’s portfolio investments support recapitalizations, management buyouts, growth financing, and the acquisition of businesses that operate in multiple industries.

They generate interest income from their debt investments in lower middle market and middle market companies and they receive dividend income and capital gains from their equity investments in lower middle market companies.

MAIN is based in Houston, Texas, and has provided flexible financing solutions since its formation in 2007 and currently has more than $6.7 billion of investment capital under management.

{kind=link}

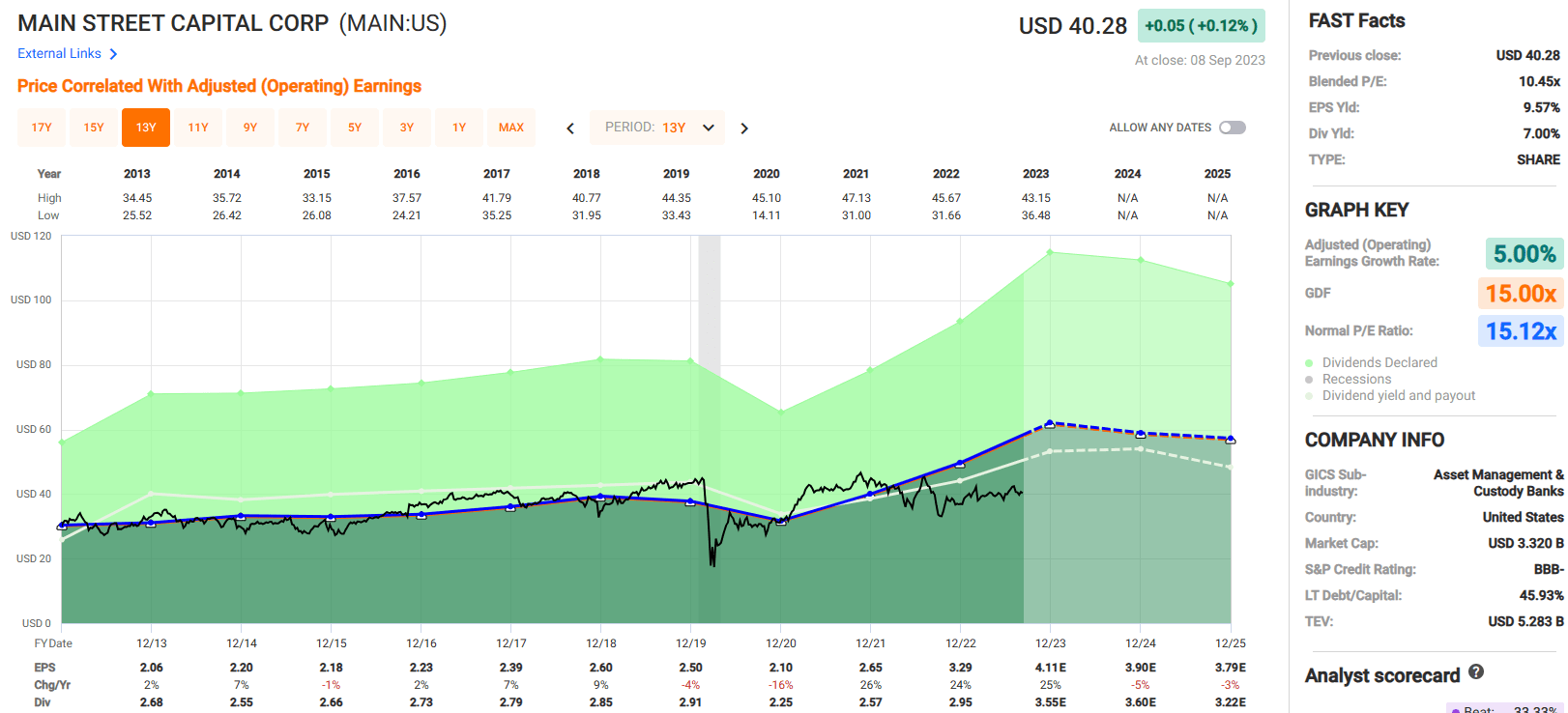

MAIN is one of the most highly regarded BDC’s and is well known for the monthly dividends they have paid since 2008.

MAIN has not increased its dividend every year, but their monthly dividend has never been decreased and has been increased by a total of 114% since their IPO when they paid a 2007 fourth quarter dividend of $0.33 per share ($1.32 annualized) compared to declared dividends of $0.705 per share ($2.82 annualized) for the fourth quarter of 2023.

In addition to their regular dividend, MAIN frequently pays supplemental dividends as shown below and has paid or declared $5.165 in supplemental dividends since their IPO.

Cumulative dividends paid or declared, including both their regular and supplemental dividend, from their IPO date until the end of 2023 totals $38.54 per share, compared with MAIN’s IPO price of $15.00 per share.

In addition to their growing dividend, MAIN has been able to increase its net asset value (“NAV”) by $14.84 per share, or 115%, since 2007 as their equity investments provides MAIN with growth opportunities including fair value appreciation, dividend income, and realized gains.

Since their IPO, MAIN’s cumulative net realized gains from its lower middle market portfolio investments total $77.3 million and the company has $449.3 million, or $5.54 per share, of cumulative net unrealized appreciation as of June 30, 2023.

MAIN - IR

MAIN pays a 7.00% dividend yield that's covered by their adjusted operating earnings with a 2022 year-end dividend payout ratio of 89.51%.

Analysts expect MAIN’s earnings per share to increase from $3.29 in 2022, to $4.11 in 2023 for a projected increase of 25% and for MAIN’s dividend to increase from $2.95 in 2022 to $3.55 per share in 2023, for a projected increase of 20.34%.

If these estimates are on the mark it would put MAIN’s 2023 dividend payout ratio at 86.37% based on their adjusted operating earnings.

Since 2013, MAIN has averaged an adjusted operating earnings growth rate of 5.00% and an average dividend growth rate of 6.99%. The stock is currently trading at a steep discount with a P/E ratio of 10.45x compared to their 10-year average P/E ratio of 15.12x.

We rate Main Street Capital a Buy.

{kind=link}

Agree Realty ( ADC )

Agree Realty is a net-lease REIT that specializes in free-standing commercial retail properties. Their portfolio consists of more than 2,000 properties covering roughly 41.7 million square feet of gross leasable space and are located in 49 states across the U.S.

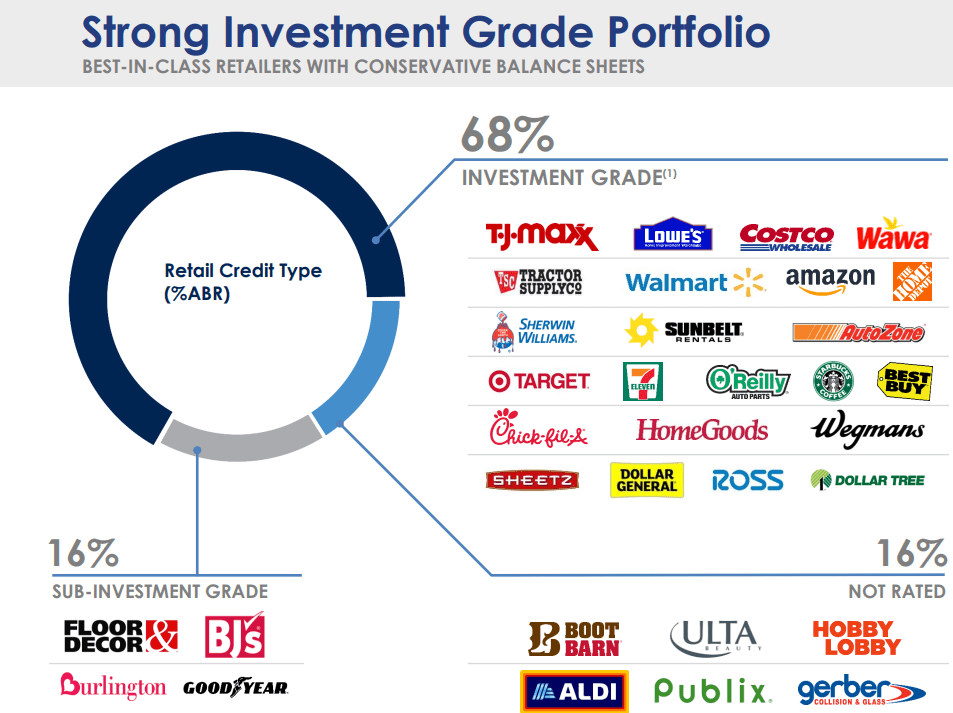

ADC leases its properties to a strong list of tenants including Lowe’s, Amazon, Target, Chick-fil-A, Tractor Supply, and Walmart. In terms of tenant credit quality, Agree Realty is among the top of its net-lease peers with approximately 68% of their annualized base rent (“ABR”) generated from tenants with an investment-grade credit rating.

They target properties used in industries that are e-commerce resistant and as a percentage of ABR their largest three retail sectors are grocery stores at 10.1%, home improvement at 8.9%, and tire and auto service at 8.7%.

ADC’s net-lease portfolio had a weighted average lease term of approximately 8.6 years and was 99.7% leased as of the end of the second quarter. In addition to their traditional net-leased properties, ADC has a portfolio of ground leases that consists of 210 leases covering 5.7 million square feet across 34 states.

As of the end of the second quarter ADC’s ground lease portfolio was fully occupied, had a weighted average remaining lease term of roughly 10.9 years, and represented 11.9% of their ABR.

{kind=link}

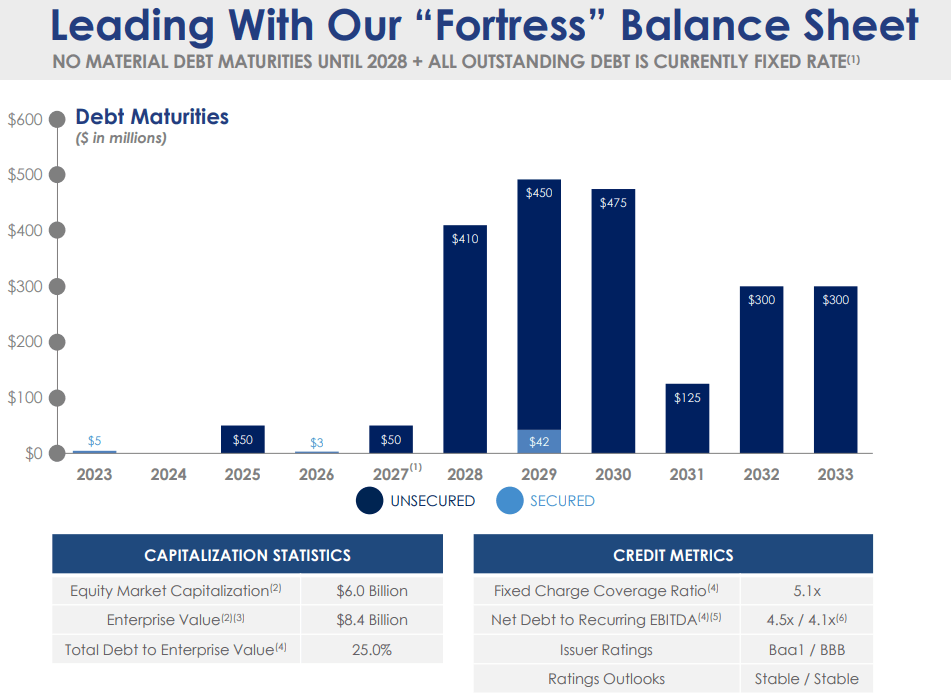

ADC is investment-grade with a BBB credit rating from S&P Global and has impressive debt metrics including a net debt to EBITDA of 4.5x, a total debt to equity ratio of 43.5%, and an EBITDA to interest expense ratio of 5.93x.

All of ADC’s debt is fixed rate and they have roughly $1.3 billion of liquidity, minimal debt maturities in 2023, and no significant debt maturities until 2028.

{kind=link}

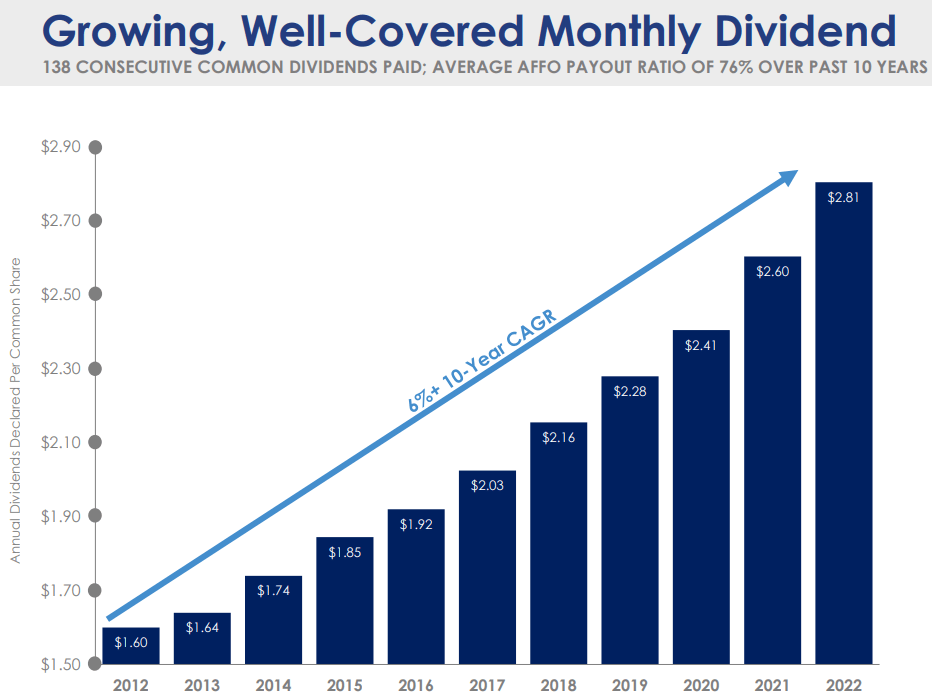

In 2021 ADC changed its dividend policy from a quarterly to a monthly distribution. Before the change, they paid 107 consecutive quarterly dividends (1994 to 2020) and have paid 31 consecutive monthly dividends since the change was made.

They have raised the dividend each year since 2013 and have delivered a compound annual dividend growth rate of approximately 6% since 2012. Additionally, they have consistently maintained a conservative payout ratio, with an average AFFO payout ratio of 76% over the past 10 years.

{kind=link}

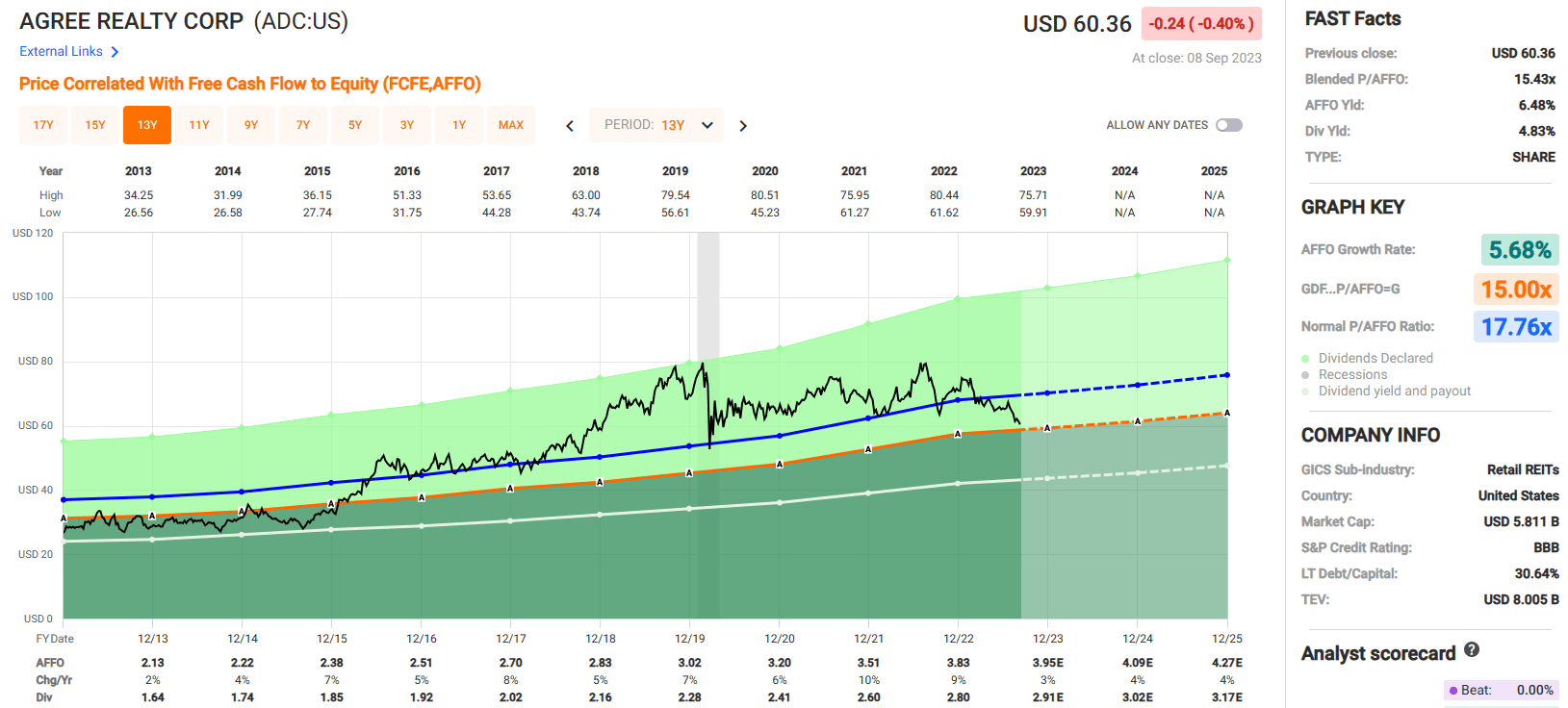

Agree Realty pays a 4.83% dividend yield that's secure with a 2022 year-end AFFO payout ratio of 73.24% and a 2023 estimated AFFO payout ratio of 73.67%.

Since 2013 ADC has had an average AFFO growth rate of 5.68% and analysts expect AFFO per share growth of 3% in 2023 and then AFFO growth of 4% in both 2024 and 2025.

ADC has a portfolio of high-quality properties leased to high-quality tenants and the stock is trading at a discount. Currently the stock trades at a P/AFFO of 15.43x, which compares favorably to their 10-year average AFFO multiple of 17.76x.

We rate Agree Realty a Buy.

{kind=link}

In Summary

As you can tell, I enjoy writing about my grandson, Asher.

Hopefully he will love REITs and BDCs as much as me when he gets older.

One thing is for sure, he will love the dividends.

By the time he's in college, I'm sure that he will grasp the power of compounding too.

Given the discounts that we're seeing now, the potential for price appreciation is almost certain.

As always, thank you for reading and commenting.

Happy SWAN investing!

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

3 Monthly-Paying Bargains For My Grandson