BNL - 3 Net Lease REITs That May Not Be Around A Year From Now

2023-06-22 07:00:00 ET

Summary

- Given the wide discounts today in REIT-dom, I believe it’s a perfect storm for M&A activities, especially within the Net Lease sector.

- I would not be surprised to see Broadstone Net Lease, Alpine Net Lease, or Spirit Realty being sold to either public or private REITs.

- Agree Realty, Realty Income, and W.P. Carey have terrific platforms in which they can use their scale and cost of capital advantages to generate solid accretion and long-term shareholder value.

This article was published at iREIT® on Alpha on Monday, June 19, 2023.

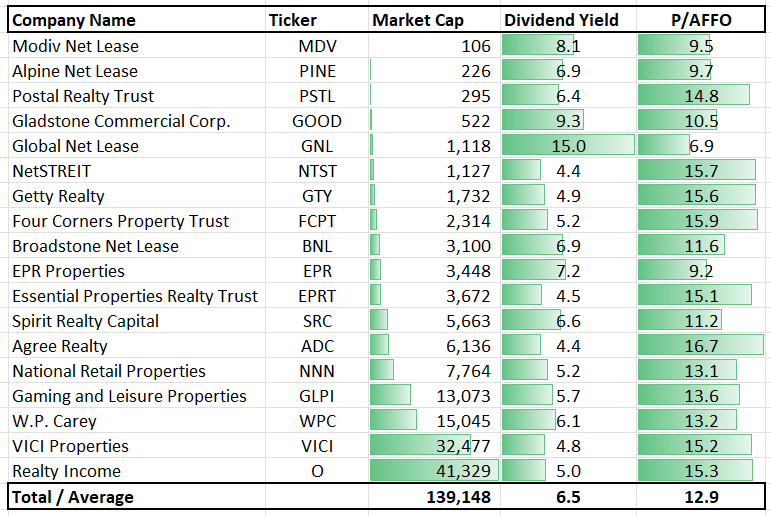

The net lease real estate investment trust ("REIT") sector has grown to become one of the largest categories. Including gaming REITs, the sector boasts 17 companies with a combined market capitalization of just under $140 Billion. The average dividend for the sector is 6.5% and the average P/AFFO (adjusted funds from operations) multiple is 12.9x.

{kind=link}

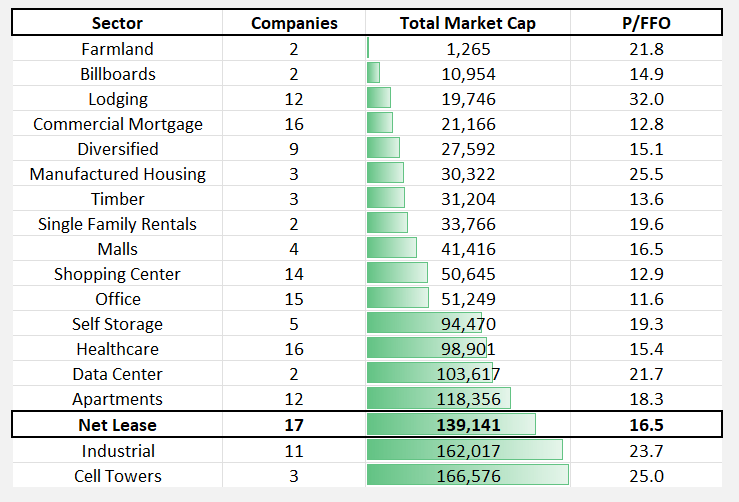

To put that into perspective, the Net Lease REIT sector is almost as large as the Industrial sector ($162 Billion) and the Cell Tower sector ($166 Billion). The Net Lease sector is also larger than the Mall ($41.4 Billion) and Shopping Center ($50.6 Billion) sectors combined.

{kind=link}

When I began writing on Seeking Alpha in 2010 there were just a handful of Net Lease REITs, namely Realty Income Corporation ( O ), NNN REIT, Inc. ( NNN ), W.P. Carey Inc. ( WPC ), Agree Realty Corporation ( ADC ), and EPR Properties ( EPR ).

{kind=link}

A few days ago, I wrote an article in which I highlighted several recent M&A announcements, including:

- Ready Capital Corp. ( RC ) announced a merger with Broadmark Realty Capital (BRMK, TMCXU ).

- Extra Space Storage ( EXR ) agreed to buy Life Storage ( LSI ).

- Regency Centers ( REG ) announced the acquisition of Urstadt Biddle Properties ( UBA , UBP ).

So this means that the number of mREITs (mortgage REITs), self-storage REITs, and shopping centers REITs will decrease by one in each sector, and Net Lease REITs are the largest sector, based on the number of constituents:

iREIT®

With that in mind, I want to put on my M&A hat and examine three REITs that could become prime-time takeover targets. Before I begin, I'll remind you that these picks are simply ideas, and I would never recommend buying (or selling) a stock based purely on M&A rumors.

Broadstone Net Lease, Inc. ( BNL )

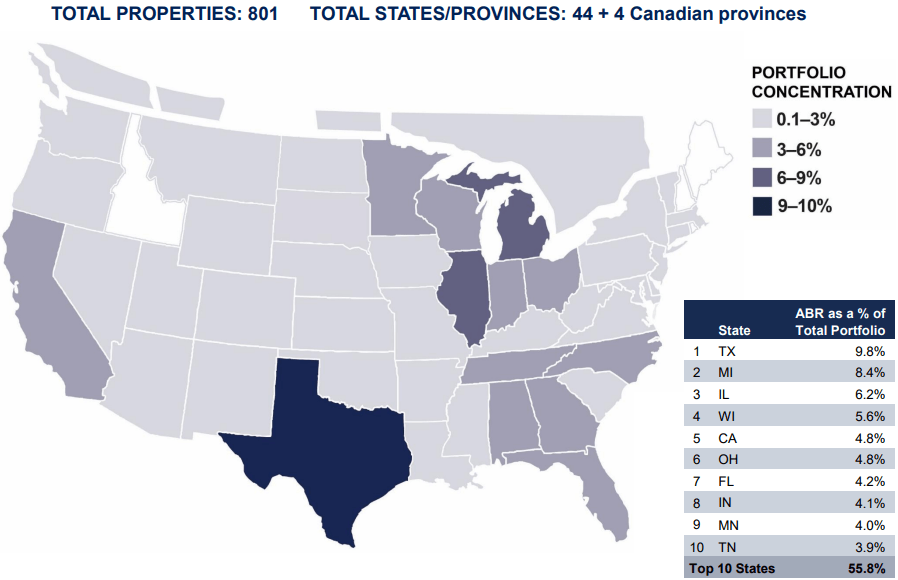

Broadstone Net Lease acquires and manages single-tenant properties that are net-leased on a long-term basis. They have a diversified portfolio consisting of 801 properties located in 44 U.S. states and 4 provinces in Canada. Along with their geographical diversity, they own multiple property types including industrial, healthcare, restaurant, office, and retail properties.

Industrial properties make up 52% of their annualized base rent ("ABR"), healthcare makes up 17%, restaurants make up 13%, retail makes up 12%, and office makes up 6% of their ABR.

BNL has 221 tenants that operate across 54 industries and a weighted average lease term ("WALT") of 10.8 years. 15.6% of their tenants are investment-grade rated, and their portfolio has a 99.4% occupancy rate.

{kind=link}

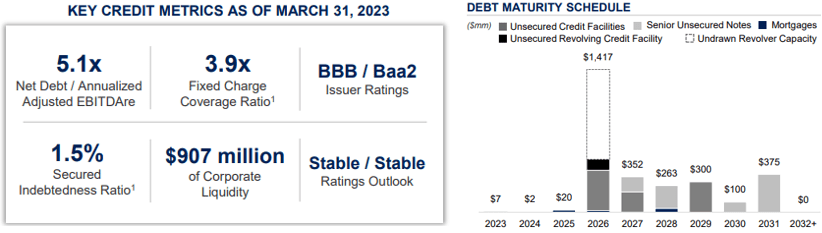

BNL is investment grade, with a BBB credit rating from S&P Global and a Baa2 credit rating from Moody's. They have a net debt to adjusted EBITDAre of 5.1x, a fixed charge coverage ratio of 3.9x, and a long-term debt to capital ratio of 39.16%. Additionally, BNL has $907 million in total liquidity and no significant maturities until 2026.

{kind=link}

We look at BNL as a possible acquisition target, with a likely suitor of W.P. Carey .

WPC is a much larger company, with a market cap of $15.05 billion vs. BNL that has a market cap of $3.22 billion. BNL's mix of property types match up well with WPC's existing portfolio, as both REITs own industrial, retail, and office properties.

Both REITs have a strong focus on Industrial properties, which make up about half of both BNL and WPC's ABR (annualized base rent).

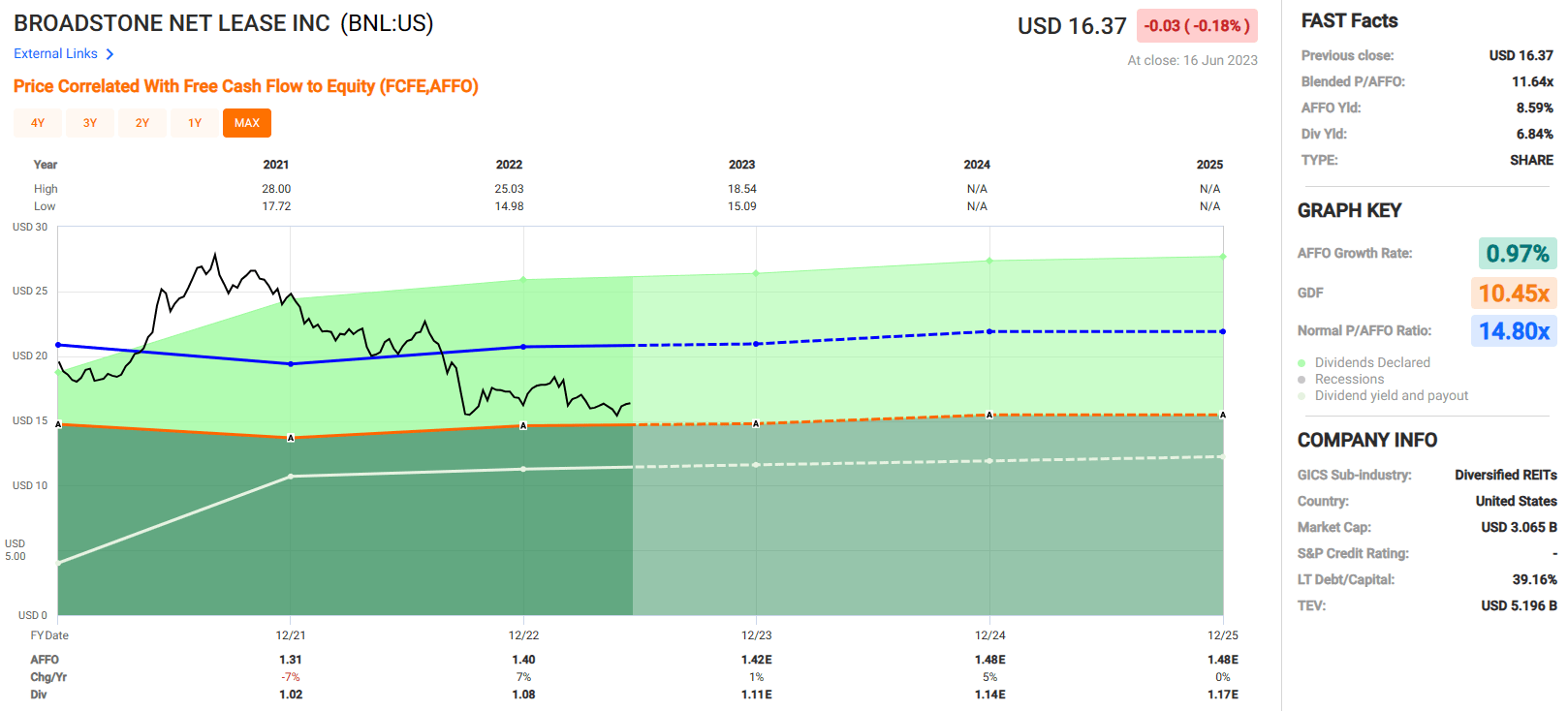

Additionally, BNL is trading at a discount to both its net asset value ("NAV") and its normal adjusted funds from operations multiple. Currently, BNL is trading at a P/AFFO of 11.64x, which is well below their normal AFFO multiple of 14.80x, and they are trading at a discount to their NAV with a P/NAV of 0.82x. At iREIT, we rate BNL a Spec BUY.

{kind=link}

Alpine Income Property Trust, Inc. ( PINE )

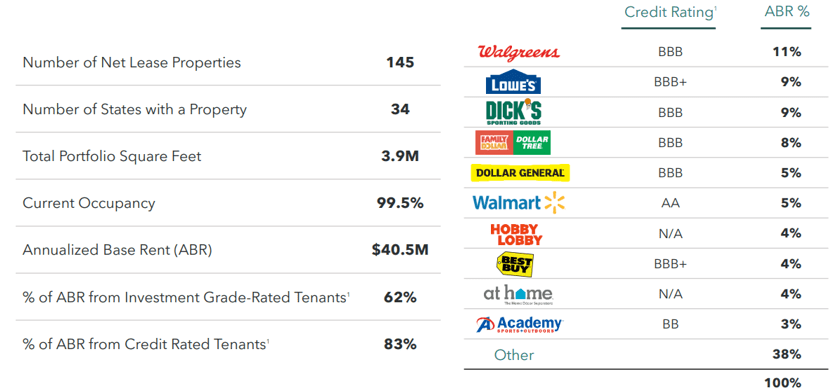

Alpine Net Lease is a net-lease REIT that is externally managed. They acquire and primarily lease properties to single tenants on a triple-net, long-term basis. Their portfolio consists of 145 properties that cover 3.9 million square feet and are located in 34 states.

PINE has high-quality tenants, with 62% of their ABR derived from investment-grade tenants. Additionally, 7 out of their top 10 tenants have investment grade credit ratings. Their portfolio has a weighted average remaining lease term of 7.3 years and a 99.5% occupancy rate.

{kind=link}

PINE has sound debt metrics with a long-term debt-to-capital ratio of 48.54%, a net debt-to-pro forma EBITDA of 6.4x, and an interest coverage ratio of 3.21x. PINE has more than $200 million in total liquidity, no exposure to floating rate debt, and no debt maturities until 2026.

{kind=link}

With a market cap of only $253 million, we view PINE as a possible acquisition target, with a likely suitor of Agree Realty . Both REITs own very similar property types with a heavy focus on retail properties. They both operate in many of the same sectors, including dollar stores, convenience stores, home improvement, and grocery stores, and both share several of the same top 10 tenants.

One of the biggest drivers of a possible takeover is that both PINE and ADC derive a large percentage of their ABR from investment-grade tenants. As previously mentioned, PINE receives 62% of their ABR from investment-grade ("IG") tenants, while ADC receives 68% of their ABR from IG tenants.

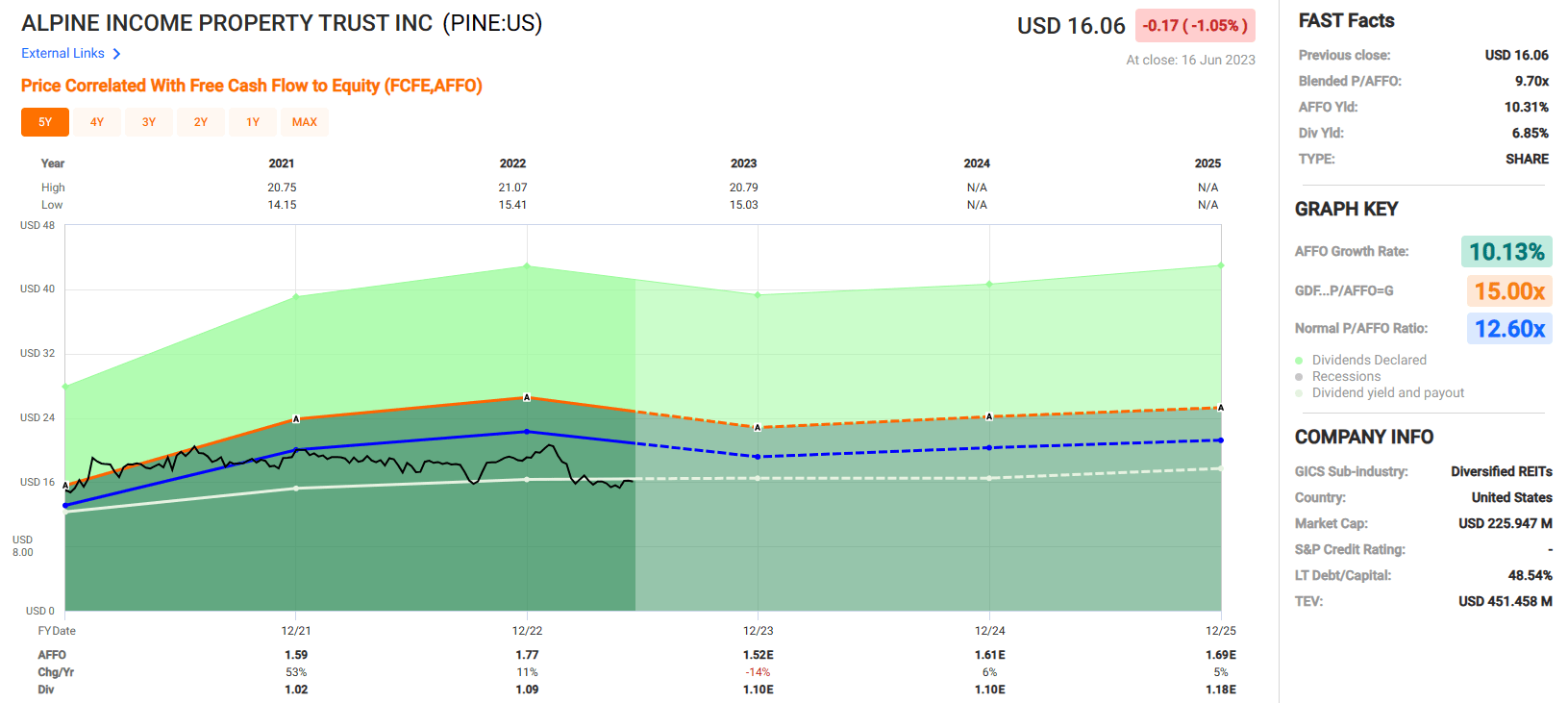

Another consideration is that PINE is trading at a steep discount compared to the multiple ADC trades at and the multiple PINE normally trades at. ADC trades at a P/AFFO of 16.95x, compared to PINE, which trades at a P/AFFO of 9.70x.

Additionally, PINE's current AFFO multiple is well below their normal AFFO multiple of 12.60x. PINE also trades at a significant discount to their net asset value with a P/NAV of 0.77x.

One other thing worth mentioning here is that PINE is externally managed by CTO Realty Growth, Inc. (CTO), which also owns an approximate 15% interest in PINE. CTO is also trading at a bargain (9.7x P/AFFO and 8.9% dividend yield).

The management contract is for a 5-year initial term (initial expiration November 2024), with one-year extension options and is terminable with payment of a one-time fee of 3x the annualized average management fee for the preceding 24 months.

We believe this is worth exploring, as this could unlock close to $40 million in value for CTO (Joey Agree, are you reading?). At iREIT, we rate PINE a Spec BUY.

{kind=link}

Spirit Realty Capital, Inc. ( SRC )

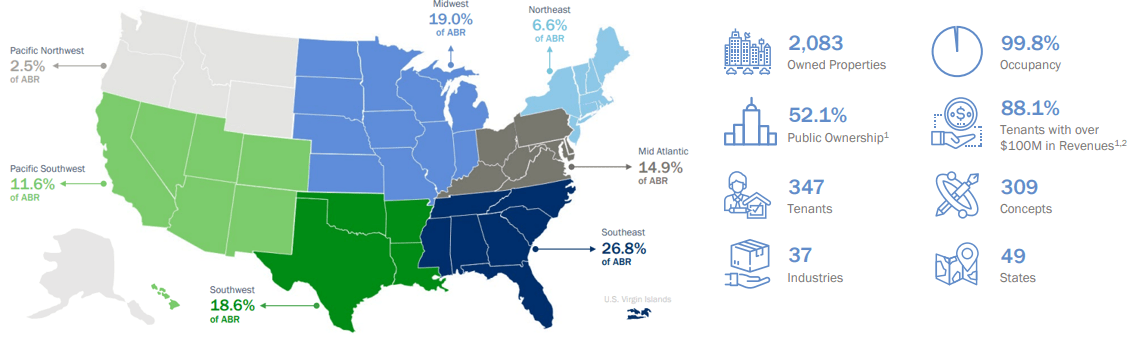

Spirit Realty specializes in single-tenant, freestanding buildings that are leased on a net basis. Their portfolio consists of 2,083 properties located in 49 states that serve 347 tenants in 37 industries. They have a weighted average remaining lease term of 10.4 years and a 99.8% occupancy rate.

SRC is well diversified by both tenant and asset mix. Their top 20 tenants contribute approximately 35% of their ABR and no single tenant makes up more than 5%.

Service retail makes up 40.9% of their ABR, discretionary retail makes up 14.7%, non-discretionary retail makes up 11.4%, industrial properties make up 24.6%, office properties make up 3%, while hotels, medical, and data center properties combined make up 5.4% of their assets when measured by ABR.

{kind=link}

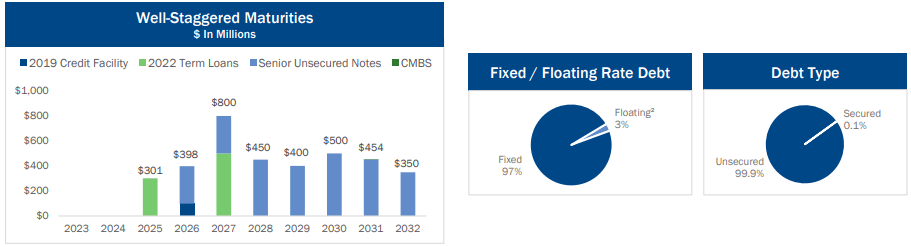

SRC is investment-grade with a BBB credit rating and has a strong balance sheet , with an adjusted debt to adjusted EBITDAre of 5.3x, a fixed charge coverage ratio of 5.1x, and a long-term debt to capital ratio of 45.04%.

Essentially all of their debt is unsecured and 97% of their debt is fixed rate. Plus they have $1.6 billion in liquidity and no debt maturities until 2025.

{kind=link}

We believe SRC could be a possible acquisition target, with a likely suitor of Realty Income . Both Spirit Realty and Realty Income's portfolios primarily consist of retail properties, but each owns industrial properties as well. 13.3% of Realty Income's annualized contractual rent comes from industrial properties, while 24.6% of Spirit's annualized base rent comes from industrial properties.

They both share several of the same tenants, such as Dollar General and Walgreens, and both have tenants that do business in the same industries, including drug stores, convenience stores, and quick service restaurants.

The acquisition of Spirit Realty would further diversify Realty Income's asset mix and give them more exposure to property types such as manufacturing and distribution centers. Realty Income's full year 2023 acquisition guidance is over $6 billion, so SRC would fall within that range with a market cap of $5.66 billion.

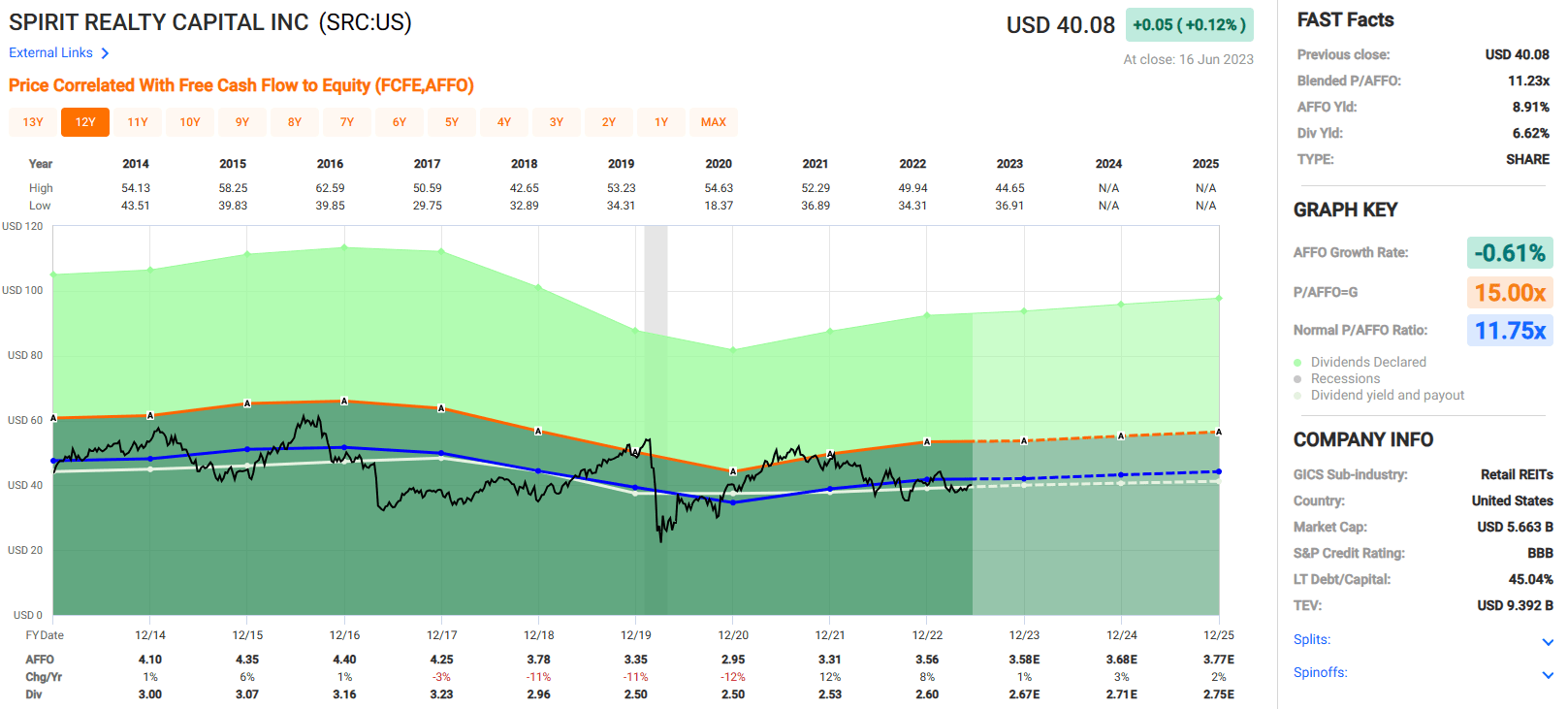

Additionally, Spirit Realty trades at a lower AFFO multiple of 11.23x when compared to Realty Income's current AFFO multiple of 15.52x. At iREIT, we rate Spirit Realty a STRONG BUY.

{kind=link}

In Closing…

Given the wide discounts today in REIT-dom, I believe it's a perfect storm for M&A activities, especially within the Net Lease sector. I would not be surprised to see Broadstone Net Lease, Alpine Net Lease, or Spirit Realty being sold to either public or private REITs.

Agree Realty, Realty Income, and W.P. Carey have terrific platforms in which they can use their scale and cost of capital advantages to generate solid accretion and long-term shareholder value.

Regardless of M&A, we'll see all three of these larger REITs (ADC, O, and WPC) continue to dominate the Net Lease arena, and I'm happy to be an owner of all of them.

Happy SWAN Investing!

For further details see:

3 Net Lease REITs That May Not Be Around A Year From Now