OVV - 3 Oil And Energy Stocks To Buy As Oil Prices Dip

2023-03-23 12:41:26 ET

Summary

- Despite strong long-term fundamentals, energy prices are retreating as short-term demand fears offset any major tailwinds.

- In this article, I present three energy stocks that offer a variety of benefits, ranging from high expected dividends to aggressive buybacks.

- Two stocks are upstream oil drillers. The third one is a downstream wild card, which I would love to buy if demand fears push it down a bit further.

Introduction

I'm a long-term energy bull. Close to 20% of my dividend (growth) portfolio consists of energy stocks, which I started buying during the pandemic sell-off in 2020. Since then, I have developed my bull case and written countless articles, incorporating increasing issues like supply shortages caused by inventory depletion and government/corporate actions. One important part of my thesis has always been to use weakness to buy high-quality energy stocks. After all, energy stocks are highly cyclical. And while oil fundamentals have changed dramatically, demand expectations are still driving prices.

This article will highlight three energy/oil stocks to invest in now. Companies that I have started to like a lot in the past three years. Among them, two are drilling companies that have maintained excellent balance sheets and consistently grown their dividends. The third is a non-oil energy stock that has also experienced a negative impact from demand concerns. However, like its counterparts in the upstream sector, it is expected to benefit from ongoing supply limitations and the anticipated increase in demand in the near future.

So, without further ado, let's get to it!

Macro Fears Spoil The Party

On a long-term basis, I am a believer in a prolonged uptrend of energy prices. This is based on a number of factors, including but not limited to...

- Pressure on energy companies to reduce emissions and a push for net zero. This is hurting drillers' ambitions to increase production. After all, higher supply increases the chance of a steep oil price decline in a recession scenario. Oil companies know they cannot count on long-term outside financing, which means they need to provide a suitable industry environment for themselves.

- Energy companies are facing declining production quality, which means more money is needed to maintain the same production output. I highlighted this in a recent article , which I highly recommend people take a look at.

- Buying back shares is more attractive than increasing production in some cases, especially in light of rising production costs and often attractive share price valuations.

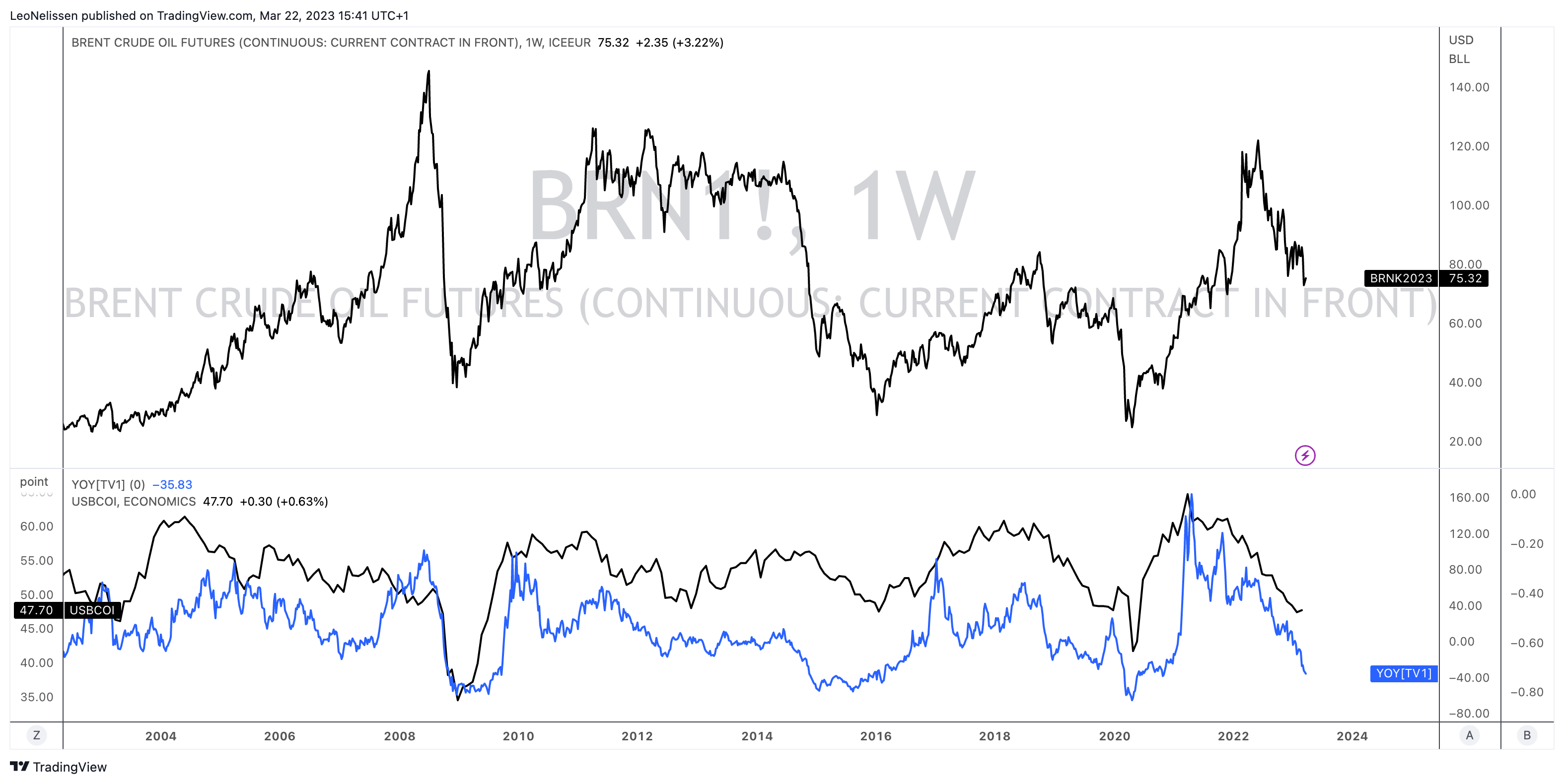

While oil prices have come down, prices are still close to the peak of the prior cycle (2018), which, I believe, is only possible because of the supply situation.

{kind=link}

Having said that, the lower section of the chart presented above displays the year-on-year progress of Brent oil (blue line) in contrast to the ISM Manufacturing Index. As observed, the current oil prices have factored in numerous negative developments. The current performance level is similar to previous market cycles, despite the fact that oil prices remain substantially higher.

Presently, a heated conflict is ongoing between the predicted increase in demand due to the reopening of the Chinese economy and new concerns of a recession as a result of aggressive interest rate hikes and the associated consequences for the economy, including risks in the banking sector.

{kind=link}

According to Bloomberg , while the oil market in the US and Europe is showing signs of weakness, the market in Asia, especially China, is displaying strength, thanks to the country's recovery from Covid restrictions. Chinese refiners are purchasing crude oil from the Middle East and the US and have increased their processing rates after the country's Covid Zero policy was abandoned. Meanwhile, European oil is displaying weakness, driven in part by French strikes and strong US flows, leading to already-weak Brent prices.

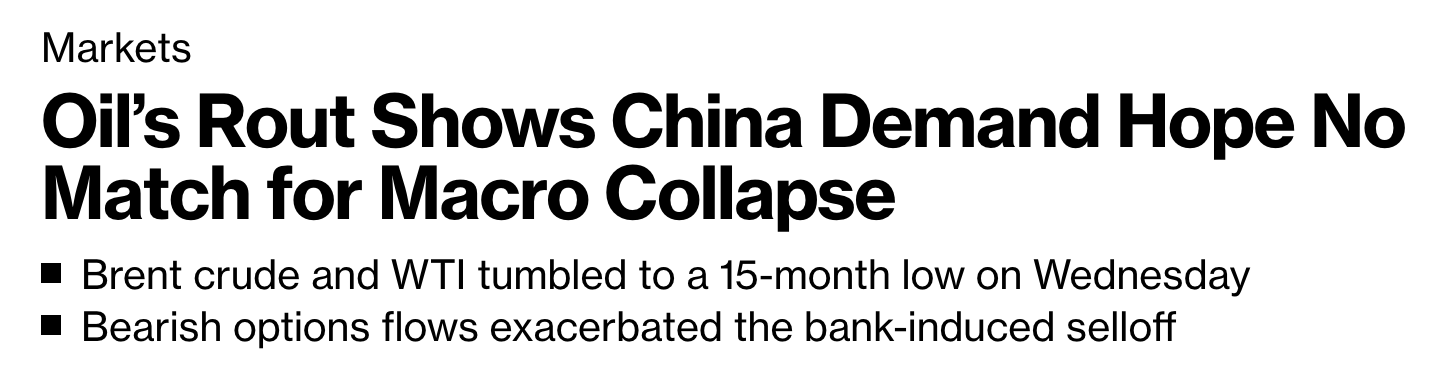

Despite Russian output leading to a market surplus, the market is focused on banking problems. However, Citigroup analysts suggest that the drop could offer buying opportunities, as banking fears seem to be overblown.

The Wall Street Journal noted the same on Tuesday .

{kind=link}

Crude prices dropped to 15-month lows after strains in the U.S. banking system sent tremors throughout financial markets and intensified fears of a broader economic slowdown. Those worries have hit prices just as energy-hungry China has finally shown signs of revving up from strict pandemic lockdowns.

That split has left traders and analysts weighing declines in U.S. construction, manufacturing and vacationing during a potential recession against resurgent Chinese demand for diesel, gasoline and jet fuel.

OPEC warned that China's growing appetite for crude oil is currently being offset by Western slowdown fears.

However, I believe these fears are temporary. Chinese demand is set to remain a strong tailwind. According to OPEC, it could reach more than 16.0M barrels of oil per day in 4Q23.

S&P Global

Hence, when looking at the bigger picture, we could see a rising supply gap in the second half of this year, which is bullish for oil and various other fossil fuels. Note that the chart below also displays the current demand weakness, leading to rising global energy inventories.

Energy Information Administration

So, while economic uncertainties persist, let me show you some stocks that, I believe, are terrific buys on weakness. Stock one is a massive on-shore producer with a high likelihood of substantial long-term dividend income. Stock number two is a rebound candidate. Stock number three is a downstream giant.

Pioneer Natural Resources ( PXD ) - The Dividend Generator

Pioneer Natural Resources is an Irving, TX-based onshore giant with a market cap of roughly $50 billion. Moreover, the company is well-known among most of my readers, as I have praised the company in a number of articles. For example, last month , I called it one of the best energy plays on the market.

Essentially, Pioneer has it all. It has low breakeven prices, a healthy balance sheet, and the ability to reward investors with both buybacks and dividends.

In 2022, the giant produced 650 thousand barrels of oil equivalent ("BOEPD) per day. 352 thousand barrels were crude oil. This year, the company expects to slightly boost production to 670 thousand to 700 thousand barrels of OE per day.

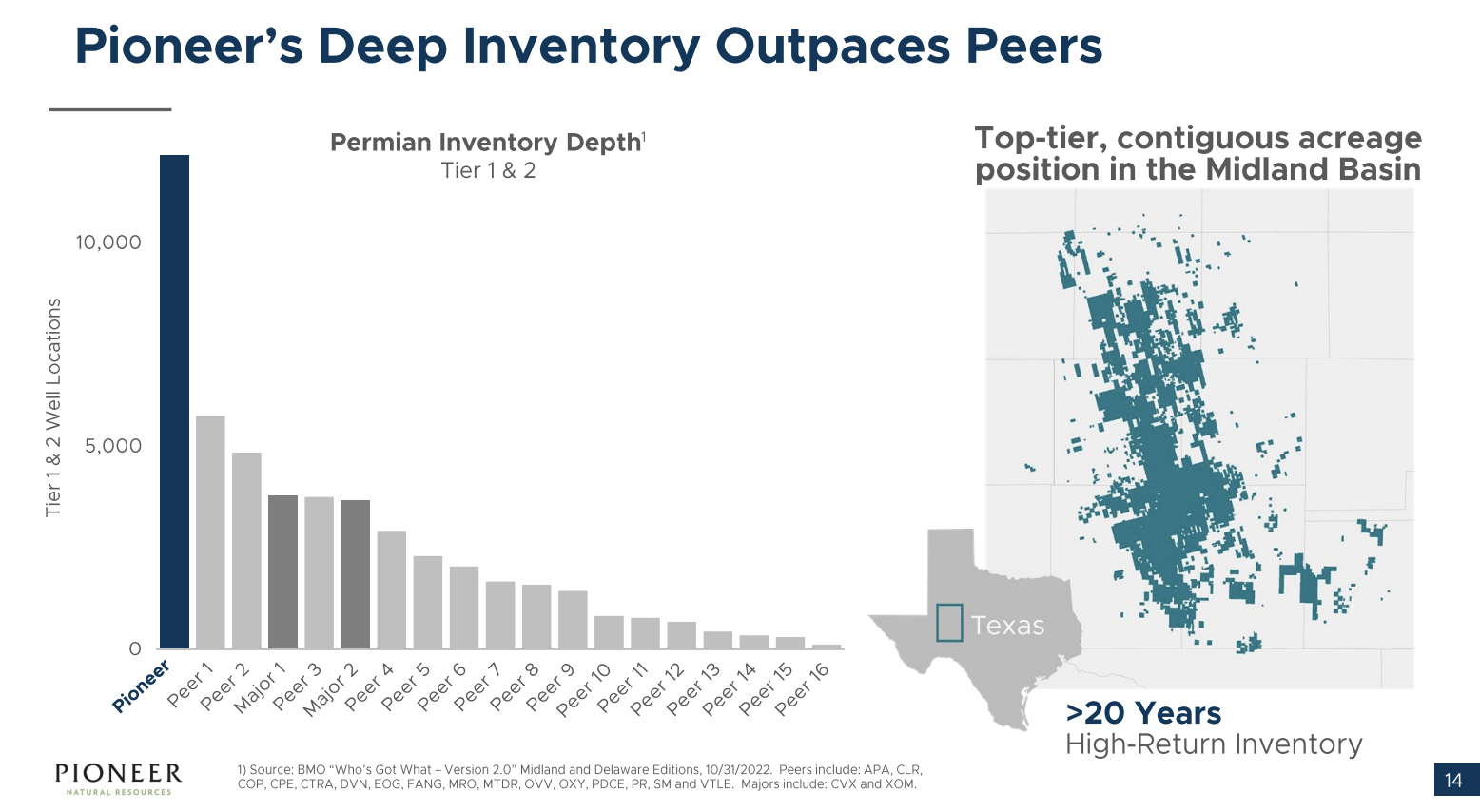

Moreover, with regard to my comments on industry inventories, PXD has more than 20 years of high-quality inventory, which is way more than any of its major peers.

{kind=link}

Moreover, this company has no hedges, which translates into higher cash flows. While not using hedges is a risk in a scenario of subdued oil prices, it needs to be said that PXD has a healthy balance sheet. It is more common for companies with high leverage to use hedges, as low operating cash flow could endanger the ability to service debt during recessions.

PXD has a terrific balance sheet. It has a net debt-to-book capitalization of 15%. This year, it has maturities of just $750 million. In 2024, the company has no maturities. Net debt ended 2022 at just 0.3x EBITDAX.

Furthermore, PXD has low breakeven prices. The company has a 2023 corporate maintenance breakeven WTI oil price of $39 per barrel, which includes the compact of 10% inflation, which includes higher production costs.

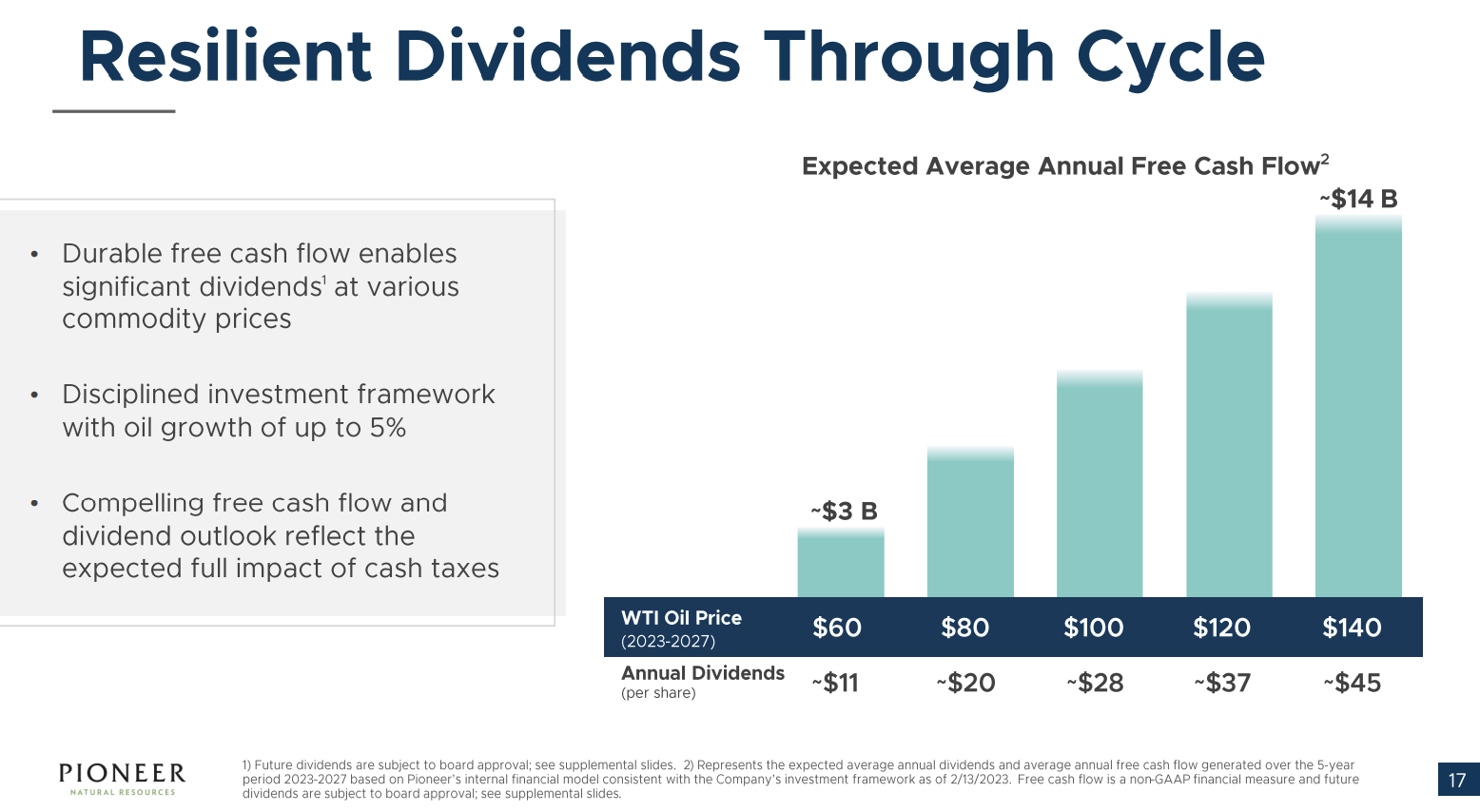

As a result, the company has a lot of room to pay dividends. The company pays a base dividend of $1.10 per share per quarter. This translates to a 2.3% yield. This yield is fully covered at $47 WTI. However, the company also distributes 75% of its excess free cash flow using special dividends. In 1Q23, that number was $4.48, bringing the total quarterly dividend to $5.58 (a 12% annualized dividend yield).

If oil prices rise to triple digits, the company is in a good spot to pay an annual total dividend of close to $30 per share.

{kind=link}

In other words, Pioneer is a great source of dividend income, thanks to efficient production, high inventories, a healthy balance sheet, and the commitment to share any benefits with shareholders.

Ovintiv ( OVV ) - The Comeback Star

I covered Ovintiv in August 2022. Prior to that, I had never covered the company, as it was a truly awful place to be. Between 2011 and 2020, shareholder value was almost entirely wiped out.

Ovintiv

While OVV is improving, it is still among the biggest decliners. Among US-based oil companies with a market cap of more than $2 billion, OVV shares were the worst performers over the past four weeks, losing 20% of their value.

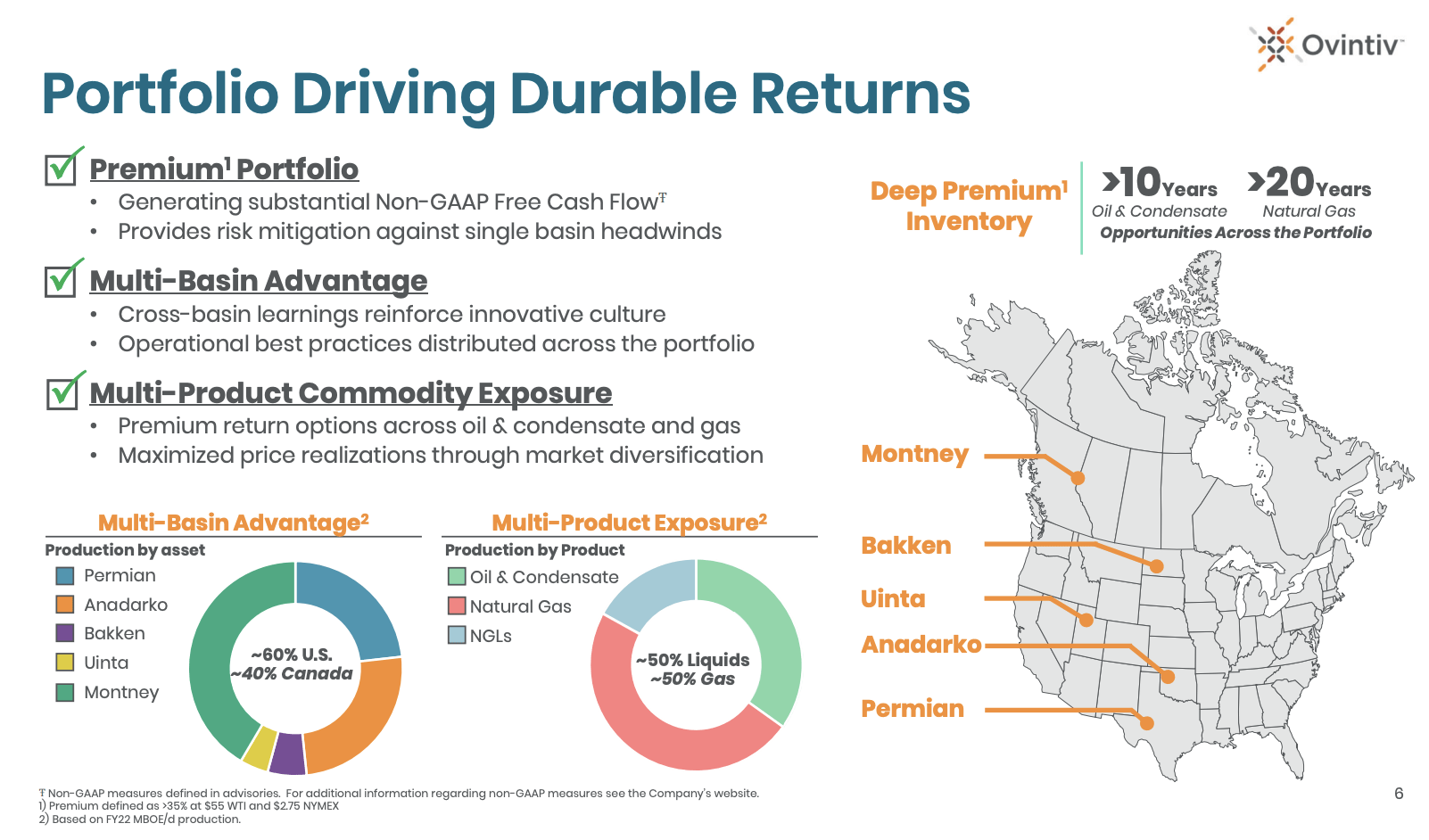

With that said, OVV is unlikely to go back to what happened prior to 2020. The $8.7 billion market cap oil producer produces close to 520 thousand barrels of OE per day. Roughly 175 thousand barrels are oil and condensate. 89 thousand barrels are natural gas liquids.

The company has at least ten years' worth of high-quality oil and condensate inventory, with natural gas inventories exceeding 20 years. 40% of this Denver-based oil company's inventory is located in the Montney Basin, one of the world's largest resources for shale gas and tight oil.

{kind=link}

For 2023, the company has hedged roughly a quarter of its oil and natural gas production. According to the company, this structure allows it to benefit from oil prices of up to $110 per barrel and $8 per MMBtu natural gas.

Ovintiv's earnings call highlighted the company's capital efficiency, which is supported by its multi-basin multiproduct portfolio. This portfolio provides diversification and learning opportunities, and the company's ability to shift capital to maximize returns is a competitive advantage. In response to weaker short-term North American natural gas fundamentals, Ovintiv is making use of its option to shift capital again in 2023.

Access to premium resources is also essential for generating durable returns, and Ovintiv is continuously evaluating opportunities to extend its runway through organic and bolt-on efforts. Over the year, the company made significant additions to its premium inventory, with a focus on the Permian and Montney regions. Ovintiv replaced 2x the number of wells it drilled last year, and it remains committed to being disciplined and opportunistic in its bolt-on efforts. These inventory renewal efforts make the company's business more sustainable and help extend its premium inventory runway across the portfolio.

Moreover, the company is now paying a 2.9% dividend yield, as part of shareholder distributions with an emphasis on buybacks. In 4Q22, the company paid $61 million in base dividends and $188 million in buybacks.

Net debt has been reduced to roughly 1x EBITDA, which is a healthy number - even *if* EBITDA were to come down further.

While the company is currently underperforming, due to a rush back to less-risky oil stocks, I believe the next upswing in oil prices will provide OVV with outperformance again.

With that said, stock number three isn't an oil producer, but it's an energy company that will benefit tremendously when demand expectations rebound.

Marathon Petroleum ( MPC ) - High-Quality Energy Returns

Marathon Petroleum is the peer of one of my largest energy holdings Valero Energy ( VLO ).

This Ohio-based refinery giant has a history of more than 135 years. It operates the nation's largest refinery system with roughly 2.9 million barrels per day of crude refining capacity. Since 2011, the company is a pure-play refining stock after it was spun off from Marathon Oil ( MRO ).

Over the past 12 months, the stock has returned close to 60%. It is less than 10% below its all-time high. Yet, I still put the stock in this article, as I believe that MPC makes a great buy on weakness - especially if demand fears push this stock a bit lower.

FINVIZ

While MPC does not produce oil, it benefits from tightness in the refinery product industry. In 4Q22, it achieved a 94% utilization rate. This happened despite disruptions at the end of the year.

Moreover, the company achieved a 109% capture rate, which means it outearned the industry thanks to high margins. The company also owns 50.4% of Midstream giant MPLX ( MPLX ), which added $500 million in cash flow in the fourth quarter alone.

Additionally, in light of sanctions on Russian oil, MPC expects global supply to remain severely impacted. Especially in Europe, the company sees new opportunities to fill the supply gap, according to its latest earnings call .

In general, Marathon Petroleum's outlook for the future is positive, as they report that demand for transportation fuels remains strong and that recovery in demand has been observed across all their products since coming out of the pandemic. They anticipate a further recovery in 2023, especially as consumers adjust their consumption patterns in response to lower retail fuel prices. Although uncertainties exist around the pace and impact of China's recovery, the magnitude of a potential US or global recession, and the impact of Russian product sanctions, the company believes that the current supply constraints and growing demand will result in robust refining margins in 2023.

This means that we can expect buybacks to remain strong - the same goes for its dividend. Since July 2021, MPC has bought back 28% of its shares. this includes the sale of its Speedway assets.

The dividend yield isn't very juicy. However, there's a lot of upside potential. In November, the company hiked its dividend by 29.3% to $0.75 per quarter. this implies a 2.4% yield.

Moreover, trading at 4.7x NMT EBITDA, I believe that MPC shares remain poised for more gains. The current consensus estimate is $152. The current stock price is $127.

Needless to say, before jumping in, I would wait for the market to do some more damage. I believe that a renewed wave of recession fears could push this stock to the $90-$110 range again (or lower). At that point, I believe that MPC offers a good risk/reward for long-term investors.

Takeaway

In this article, we discussed the factors behind the recent decline in oil and energy stock prices. While long-term fundamentals remain healthy, shorter-term demand fears continue to more than offset these benefits, including the expected rebound related to the Chinese reopening.

In light of these fundamentals, I present three energy stocks that I like on weakness. PXD offers a high potential yield, a stellar business model that comes with efficient production, low breakevens, and a focus on shareholders. Ovintiv is a rebound candidate, which is currently repairing its balance sheet and boosting production to enhance shareholder value. Marathon Petroleum hasn't sold off a lot, yet it's a great wild card for investors to buy high-quality refining exposure on weakness. The company benefits from long-term high-margin opportunities in refining and its ability to let shareholders benefit through aggressive buybacks and high dividend growth.

Please let me know what you think of the current energy situation in the comment section below. Are you preparing to buy energy on weakness? What stocks are you analyzing?

For further details see:

3 Oil And Energy Stocks To Buy As Oil Prices Dip