WELL - 3 Once-In-A-Decade REIT Buying Opportunities

2023-09-21 08:05:00 ET

Summary

- REITs offer a once-in-a-decade opportunity according to Principal Asset Management.

- Some high-quality REITs offer 50%+ upside potential.

- We present 3 of our favorite REIT buying opportunities to profit.

One of the biggest and most sophisticated investment firms in the world, Principal Asset Management, recently came out with a presentation making the case for investing in real estate investment trusts, or REITs ( VNQ ).

They explain that:

" Extreme bearishness towards REITs and a large valuation discount is creating a compelling entry point for investors... As Warren Buffett once famously wrote, “…be fearful when others are greedy and be greedy only when others are fearful.” In our view, investors should be greedy when it comes to REITs.

It appears contrarian to favor REITs today compared to the negative news headlines about real estate, but these challenges are well understood in REIT markets. When sentiment does shift back in favor and relative valuations are too cheap to ignore, REITs are poised for potentially strong fund inflows. After all, the number of potential buyers is outnumbering the remaining sellers by a bigger margin every day."

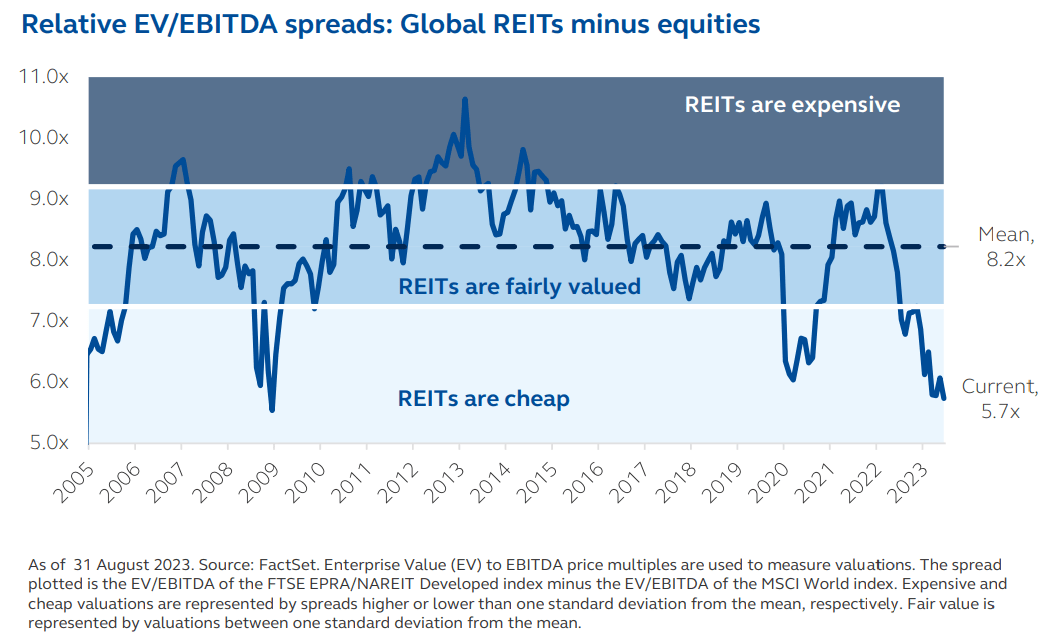

They support these statements with the following chart that shows that REITs are today priced at their lowest valuations relative to stocks (SP500) since the great financial crisis:

{kind=link}

Some REITs, of course, deserve to trade at these lower valuations because they may be overleveraged, own challenged properties, or suffer from poor management.

But the interesting thing is that all REITs have crashed, including even the high-quality ones that enjoy strong balance sheets and growing rents.

The market appears to think that all REITs will be very negatively impacted by the surge in interest rates, but in reality, this really isn't the case, and it depends heavily from one company to another.

This has created a once-in-a-decade buying opportunity according to Principal Asset Management, with REITs often trading at large discounts relative to the fair value of their assets.

They manage over $600 billion worth of investments and they are now buying REITs.

But which are the best to buy today?

In what follows, we highlight three of our Top Picks to accumulate today:

BSR REIT (HOM.U / BSRTF )

Principal is not the only big player to accumulate REITs.

Recently, Blackstone ( BX ) reported in its 13F filings that it had initiated a position in Camden Property Trust ( CPT ), which is a major apartment REIT.

At the same time, Starwood, which is another big private equity player, also reported that it had entered a position in Mid-America Apartment Communities ( MAA ).

Both of these are high-quality sunbelt-focused apartment REITs, and they are now so heavily discounted that these big private equity real estate players are accumulating them.

Mid-America Apartments

But I think that BSR REIT is an even better opportunity.

Its market cap may be too small for Blackstone and Starwood so it isn't getting their attention, but it is even cheaper.

It owns a portfolio of affordable apartment communities in Dallas, Austin, and Houston - also known as the Texan Triangle. These are some of the most desirable apartment markets because they enjoy rapid population growth and rent-to-income ratios remain low, leaving ample room for future growth.

But despite that, the REIT is today priced at 60 cents on the dollar. Its latest NAV estimate is $20.50 per share, but it currently trades at just around $12 - an exceptionally large discount for such desirable assets.

BSR REIT

Does it have an overleveraged balance sheet ?

No. Its LTV is just 39% and only about 1/4 of that expires before 2026. Moreover, it also retains a large chunk of its cash flow, which will allow it to organically reduce its leverage and limit the impact of rate hikes.

Is its management conflicted?

Again, no. Insiders own a large chunk of the equity and the management is today busy buying back shares to take advantage of the valuation disparity.

Here is what they commented on a recent conference call:

"As long as our units trade at a significant discount to NAV, we see buybacks as an attractive option. We will continue to capitalize on opportunities to repurchase REIT units to drive stronger financial returns."

I would add that they explained that it would today cost $250k to $275k per unit to build a comparable product of BSR, but their units are now priced at $165k per unit according to our estimates. So there is also a huge discount relative to its replacement cost.

Legendary real estate investor Sam Zell has famously said that:

"The most reliable measure of our buildings’ value remained—and had always been, in my opinion—replacement cost."

That's because if you are buying good assets that are growing in demand, eventually their value should be reflective of their construction cost - otherwise, there simply wouldn't be an incentive for anyone to build more to meet the growing demand.

BSR REIT

So in short, the shares of BSR are offering you an opportunity to invest in a portfolio of desirable Texan apartment communities that are enjoying growing rents at 60 cents on the dollar. The balance sheet is good and the management is busy buying back shares to create value.

While you wait for the long-term upside, which could be up to ~65% just to return to its net asset value, you also earn an ~8% cash flow yield, out of which the company pays about half to shareholders in the form of dividends and retains the rest to buy back shares and deleverage.

If you were offered such an opportunity in the private market, you would probably jump on the opportunity.

Crown Castle Inc. ( CCI )

Crown Castle is the REIT that I have been accumulating the most lately.

It is a cell tower REIT that I have followed for over a decade, patiently waiting for the opportunity to own it, and that opportunity has now arrived.

Typically, it is priced at well over 20x funds from operations, or FFO, and it only offers a small ~3% dividend yield because its business is very defensive and it enjoys rapid growth prospects.

But today is the exception.

You can now buy it at a historically low valuation following its recent crash:

| Typical |

| Today |

| FFO Multiple |

| >20x |

| 12.6x |

| Dividend Yield |

| ~3% |

| 6.4% |

You may ask yourself what could have caused such a crash.

And the answer would be that CCI is going through a temporary slowdown in its growth and this has caused a market overreaction.

This slowdown is the result of two things: the surge in interest rates and the recent merger of T-Mobile ( TMUS ) and Sprint, which is leading to some lease cancellations in the near term.

Therefore, the REIT won't grow by much for the next 2 years and since the public markets only care about the short run, this has been enough of a reason for its share price to crash to such low levels.

But this is just temporary.

The long-term thesis for investing in CCI is still as strong as ever. We just recently interviewed its management and they explained to us that they expect a return to 7-8% dividend per share growth post-2025.

They are very confident in this guidance because they have already secured a good chunk of that growth in advance, and so when you remove the temporary headwinds, their growth should pick up nicely.

Therefore, we think that this is a great opportunity for long-term-oriented investors who can look past the next 24 months and focus on the next 5-10 years.

Today, you get to buy shares at a high 6.4% dividend yield, and as growth returns to 7-8% per year, you will be earning near-15% annual total returns from the yield and growth alone.

And here's the kicker:

The reacceleration in growth will likely lead to a rerating of the stock and result in significant upside. Even just returning to halfway of its previous peak would result in 50%+ upside from here.

And if you still doubt this company, take a look at its long-term track record of beating even the likes of Berkshire Hathaway ( BRK.B ):

Healthcare Realty Trust Incorporated ( HR )

Healthcare Realty is the leading medical office building REIT.

This is a property sector that's commonly perceived to be one of the safest because:

- Your tenants are doctors

- Their businesses are recession-resistant

- Rent coverage ratios are typically very high at >5x

- The population is aging rapidly

- Thus lease defaults are rare and rents grow consistently.

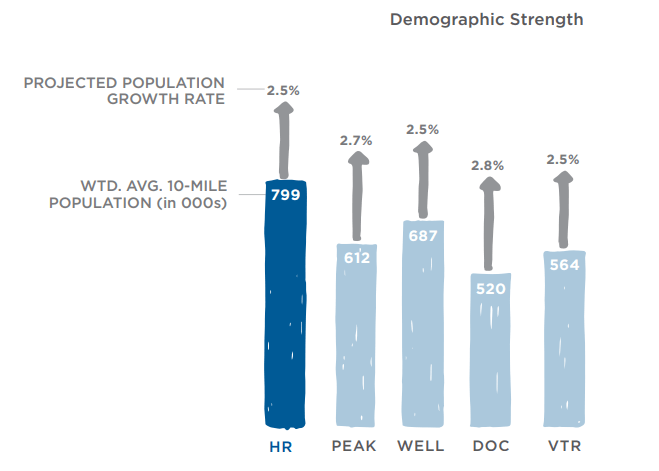

All of this is especially true for HR because it owns medical office clusters, which enjoy even greater demand and higher barriers to entry. Moreover, its clusters are located in some of the stronger neighborhoods of rapidly growing markets:

{kind=link}

{kind=link}

See how its demographics compare to those of blue-chip peers Welltower ( WELL ) and Ventas ( VTR ):

{kind=link}

But despite that, HR has recently seen its share price cut in half and it now trades at its lowest valuation in a decade:

| Typical |

| Today |

| FFO Multiple |

| >15x |

| 10x |

| Dividend Yield |

| ~5% |

| 7.7% |

We think that this is a historic opportunity.

HR has crashed so much because the market appears to perceive it as a REIT with above-average leverage and no growth.

But this is now changing.

HR recently merged with another REIT called HTA, and the timing of this merger was unlucky because it expanded leverage right as interest rates surged.

But now, HR will begin to reap the benefits of this merger as it increases the occupancy of HTA's underutilized properties.

They noted on their most recent conference call that they expect 5-7% FFO per share growth in the coming years and that's despite the now higher interest rates.

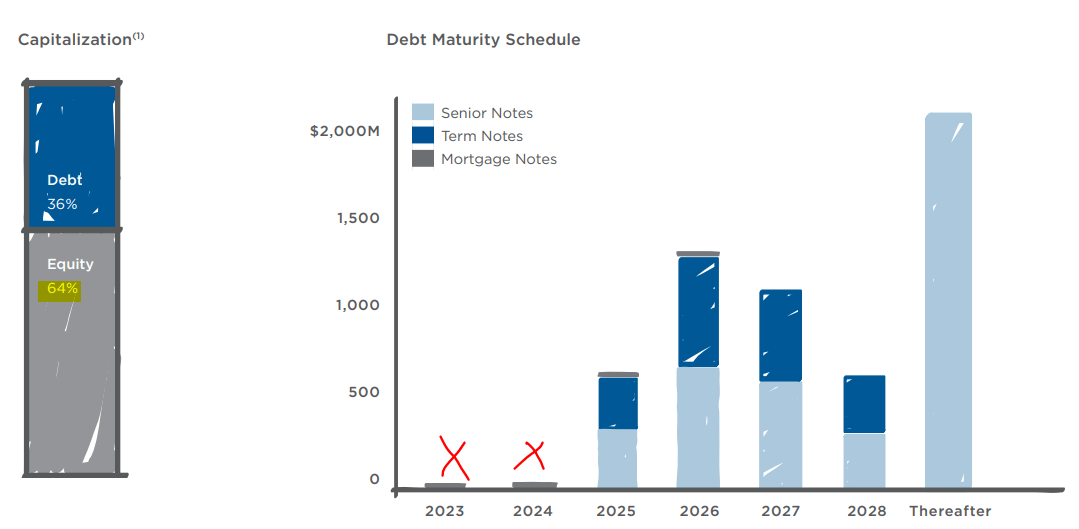

Moreover, while it is true that HR has a bit more leverage than average with a Debt-to-EBITDA of 6.6x, it is important to note that it has no debt maturities until 2025 and by then, its leverage will have been brought closer to 6x:

{kind=link}

Therefore, I expect the market to soon perceive HR very differently.

Within 24 months, its balance sheet will be greater and the company's growth will have accelerated, and both of these factors should warrant a materially higher valuation multiple. Simply expanding from 10x to 15x FFO would unlock 50% upside and this wouldn't be unreasonable by any means.

And the great thing here is that we are not relying on this.

By simply adding the 7.7% dividend yield with the 6% growth rate, investors can expect to earn a ~14% annual total return on a constant-multiple-basis.

That's very attractive coming from such properties.

Closing Note

These are just 3 examples of high-quality REITs that are now on sale.

But we own 20+ others that are equally attractive as part of our Core Portfolio, allowing us to mitigate risk, and optimize our risk-to-reward.

The REIT market is rarely this opportunistic so don't miss your chance to buy real estate at a discount!

For further details see:

3 Once-In-A-Decade REIT Buying Opportunities