VNQ - 3 Once-In-A-Decade REIT Buying Opportunities

2023-04-21 08:05:00 ET

Summary

- REITs are heavily discounted relative to their net asset value.

- Some REITs would need to double to close their discount.

- We highlight three one-in-a-decade REIT buying opportunities with up to 100% upside potential.

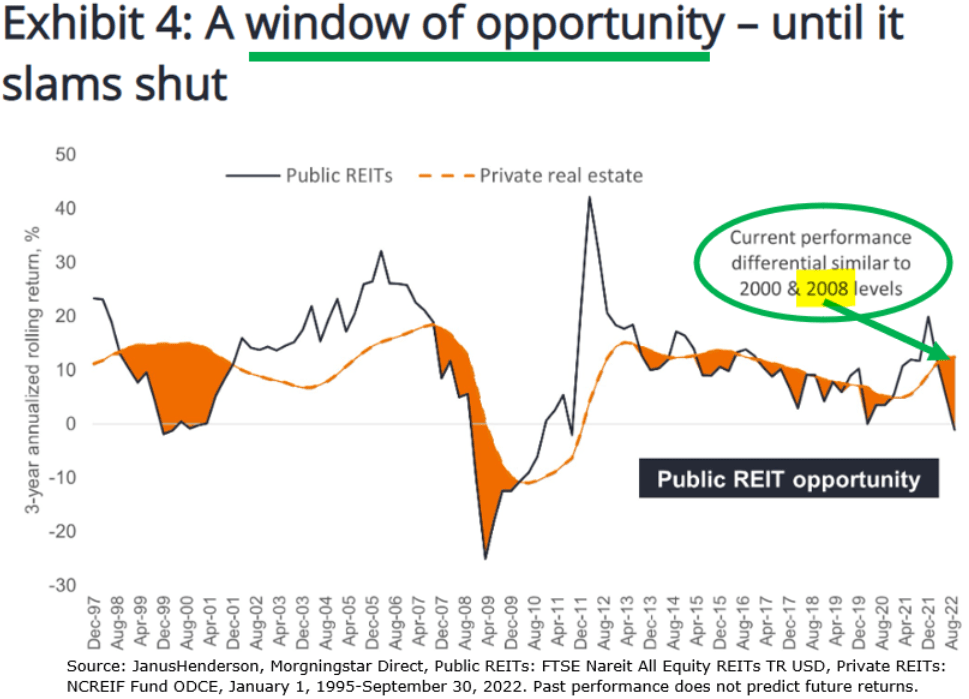

A recent study found that REITs ( VNQ ) are currently priced at a 28% discount to their net asset value.

This essentially means that the equity of REITs is priced at ~70 cents on the dollar, which is quite exceptional when you consider that REITs have historically traded at a slight premium during most times. This premium also makes sense when you consider that you are buying real estate with the added benefits of liquidity, diversification, and professional management.

{kind=link}

These discounts are similar to those of 2008-2009, which was a once-in-a-decade buying opportunity.

And that's not all.

The 28% discount is just the average for the sector. There are a number of REITs that trade at even lower valuations with 40, 50, or even up to 70% discounts on their net asset values.

Now, the interesting thing here is that if a REIT trades at a 50% discount on its net asset value, it means that its share price would need to double just to get back to its net asset value.

Now, obviously, this net asset value may not hold and that's what is happening in some cases. A good example of that would be office REITs. SL Green ( SLG ), as an example, is heavily discounted relative to its net asset value, but it owns mainly office buildings in NYC, which are now losing value as cap rates expand and their rents decline.

That's probably not what you want to own.

But believe it or not, there are also some REITs that own desirable properties with growing rents, and they are also discounted. They dropped in association with the office REITs and now offer significant upside potential as their valuations eventually recover.

In what follows, we highlight 3 such REITs that could potentially double over the coming years:

BSR REIT ( BSRTF / HOM.U:CA )

BSR REIT is an apartment REIT that owns mainly affordable class B communities in rapidly growing Texan markets like Dallas, Houston, and Austin.

Its current share price is $13 per share, but its latest net asset value is $22 per share, which means the discount is around 40%.

This would imply that the company is going through some severe stress but in reality, this is a high-quality REIT with:

- Defensive properties: ~$1,500 average rent level.

- Rapidly growing rents: 13% same property NOI in 2022.

- Strong balance sheet: 35% LTV.

- Great management: high insider ownership.

- Catalyst: share buybacks to create value.

{kind=link}

Rent growth is slowing down in 2023, but it remains strong at around 5%, and it is not the operational performance of its assets that could justify such a low valuation.

The market appears to have simply overreacted to the surge in interest rates, thinking that the value of its properties would crash, but this hasn't happened, and likely won't because there is still high demand for Texan apartment communities given their long-term growth prospects.

We recently interviewed the REIT's CEO at High Yield Landlord, and he explains that their average rent is only ~$1,500 per month and represents just ~20% of its resident's income on average. That's 2x lower than in popular coastal markets, leaving ample room for further growth and also margin of safety in case of a recession.

{kind=link}

Now, I am not saying that cap rates won't expand at all, but I think that the company's NAV should remain more or less stable because rents are also growing and BSR is using this opportunity to buy back shares, which is very accretive at these levels.

If you expect the company to grow its cash flow by 5-10% annually over the coming 3 years... and interest rates eventually return to lower levels... I think that BSR could potentially double your money as it returns to a slight premium to its NAV. You also earn a monthly 4% dividend yield while you wait.

Alexandria Real Estate ( ARE )

Alexandria is a healthcare REIT that specializes in life science buildings.

Its current share price is $120 per share, but its latest net asset value is nearly $200 per share, which means that its discount is nearly 40%.

Again, this would imply that the company is going through some severe stress, but in reality, this is a high-quality REIT with:

- Defensive properties: healthcare is recession-resistant, and many of its tenants are big pharma companies like Pfizer ( PFE ) and Moderna ( MRNA ).

- Rapidly growing rents: 20%+ rent hikes on expiring leases in 2022.

- Strong balance sheet: BBB+ investment grade rated balance sheet.

- Great management: one of the best track records in the entire market.

- Catalyst: selling JV interest in properties at low cap rates to reinvest in higher-yielding development projects.

Alexandria Real Estate

The market worries about VC funding for biotech companies, and this is why it is pricing Alexandria at such a low valuation.

But I just recently attended the Citi Global Property Conference and got to attend Alexandria's roundtable. They explain that despite all the negative headlines, last year was a record-breaking year for the VC funding of their tenants, and it will take years for them to put all this capital to work.

The main takeaway from the conference was that they remain very bullish on their future growth because:

- Their current rents are deeply below market.

- There is high demand for lab space but limited supply.

- They can access capital at low cost via JVs and reinvest it in high-yielding development projects.

- They have no major debt maturities for many years, with a 13-year average debt term.

We expect the company to grow its FFO per share by 5-10% annually over the coming 3 years. Add to that a repricing to near its NAV, and you would again possibly double your money when including the 4% dividend yield.

Vonovia (VNA/ VONOY )

Vonovia is the biggest apartment landlord in Europe. It owns 500,000+ apartment units, mainly in Germany.

It is also one of the cheapest REIT-like entities in the world.

Its current share price is €18 per share, but its latest net asset value is €57 per share, which means the discount is around 70%.

In other words, its share price would need to more than triple to get closer to its NAV. This is especially surprising when you consider that this is a blue-chip company with:

- Defensive properties: rent regulation in Germany leads to steady and consistent rent growth, even during recessions.

- Steadily growing rents: Vacancy rates are at an all-time of 2% and rents are growing at 3-4% per year.

- Strong balance sheet: BBB+ investment grade credit rating.

- Great management: one of the best track records in the entire market.

- Catalyst: selling JV interest in properties at low cap rates to pay off debt maturities and buy back shares.

Vonovia

Why is it so incredibly cheap then? The historic surge in interest rates has led to lots of concerns. Investors mainly fear that Vonovia's assets will lose significant value as cap rates expand to higher levels.

We have explained in a video why we think that this is unlikely, but in short, the company's net asset value is already priced at a steep discount to the replacement cost of these assets. Rents are also growing at a good pace, vacancies are non-existent, and a lot of institutional investors remain interested in these assets, despite the surge in rates.

But even if you expected the NAV to come down a lot, let's say from €57 down to €36... then Vonovia's share price would still need to double from here to get back to its discounted NAV. Historically, it has traded at a ~10% premium to its net asset value during most times, and once we put this crisis behind, we think that the company's valuation will once again normalize closer to its net asset value. While you wait, you earn a 5% dividend yield.

Bottom Line

A lot of REITs are today deeply undervalued. They are priced at valuations that remind us of the great financial crisis in some cases, and yet, few investors appear to be taking advantage of these opportunities.

Investors only see the negative and fixate on the near-term risks of today's environment. We think that they should instead focus on the bigger picture and the long-term potential.

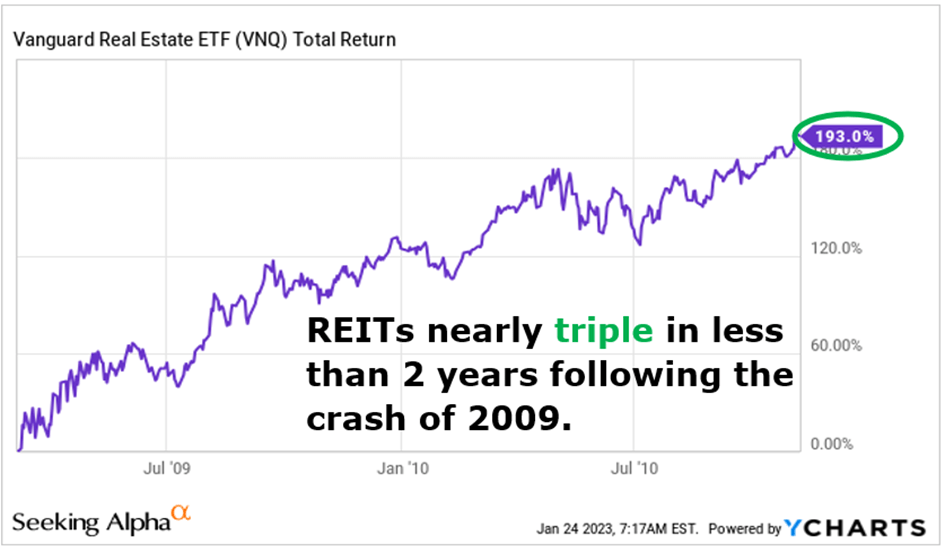

Risks were also great during the great financial crisis, and yet, those who bought REITs at discounted valuations earned a fortune in the recovery:

{kind=link}

For further details see:

3 Once-In-A-Decade REIT Buying Opportunities