WPC - 3 Once-In-A-Decade REIT Buying Opportunities

2023-10-09 08:05:00 ET

Summary

- REITs are offering a once-in-a-decade chance to win big.

- Valuations are the lowest since 2008-2009.

- We highlight three "Top Picks" with 50%+ upside potential.

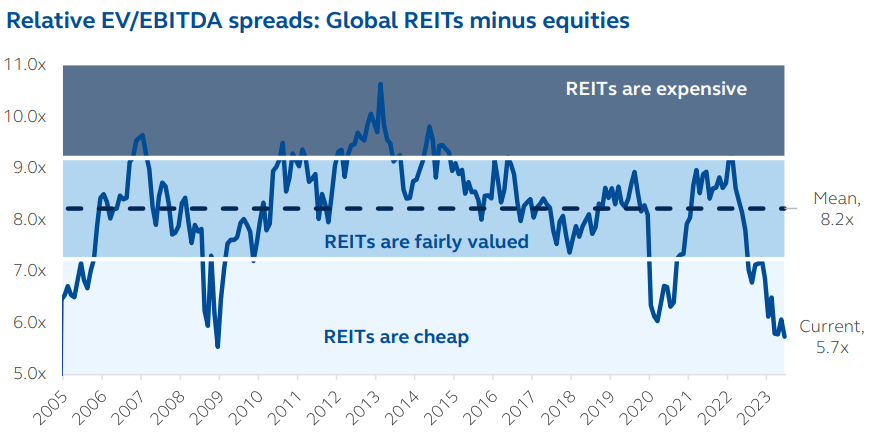

Today, real estate investment trusts, or REITs ( VNQ ), are priced at their lowest valuations since the great financial crisis. Their share prices have dropped by nearly 40% since the beginning of 2022 even as their cash flows have risen by 5-10% in most cases:

As a result, valuations are now roughly 2x lower than in early 2022.

And that's just the average!

There are a number of REITs that are down closer to 50, 60, or even 90% in the most extreme cases:

That's how brutal this market has been on REITs...

We are not talking about a correction anymore. This is a real crash.

The worst one since 2008-2009!

It reminds me of the following quote of Warren Buffett

" The years ahead will occasionally deliver major market declines -- even panics -- that will affect virtually all stocks. No one can tell you when these traumas will occur... The best chance to deploy capital is when things are going down. When it rains gold, put out the bucket, not the thimble. " Warren Buffett.

In short, what he is saying here is that fortunes are made during bear markets when fear is high and opportunities are abundant.

Prices typically drop too low due to excessive pessimism, and then on top of that, it also leads to indiscriminate selling with every stock in a given sector dropping, regardless of their fundamentals.

That's precisely what has happened with REITs, and it has led to some exceptional buying opportunities.

Sure, an overleveraged REIT with office properties may deserve to trade at a lower valuation, but those are actually the minority.

Most REITs today have strong balance sheets with low debt and own desirable assets that enjoy growing rents. And yet, they are now priced at huge discounts relative to the fair value of their assets.

The last time valuations were this low was following the great financial crisis, and REITs then tripled in the following two years:

{kind=link}

Once more, we think that we are presented with a "once-in-a-decade" chance to win big in the REIT sector. In what follows, we present three of our Top Picks to capitalize on this opportunity.

Crown Castle Inc. ( CCI )

Crown Castle is slowly becoming one of my largest holdings.

This is a blue-chip REIT that typically trades at a high valuation and low dividend yield because:

- It owns a cell tower portfolio that generates recession-resistant cash flow with steady and predictable growth prospects.

- It has a strong investment grade-rated balance sheet that limits the impact of rising interest rates.

- It has historically been able to grow its dividend by 9% per year on average and massively outperformed the rest of the stock market:

Crown Castle

{kind=link}

As a result, the market typically prices it at 20-25x FFO and a low 3-4% dividend yield. That's warranted given the resilience of its fundamentals and its compelling growth prospects.

Even a low 3% yield can get you to double-digit total returns when you pair that with an 8% annual growth rate.

But today is your chance to buy CCI off the discount rack. Its share price has been cut in half since the beginning of 2022 even as its cash flow and dividend kept on rising:

And this has resulted in the lowest valuation in over a decade for this blue-chip REIT:

| Typically |

| Today |

| FFO Multiple |

| 20-25x |

| 11.6x |

| Dividend Yield |

| 3-4% |

| 7% |

This exceptionally low valuation is the result of two things:

Firstly, the entire REIT market has crashed, and this caused all REITs, including even blue chips like CCI, to suffer from indiscriminate selling.

And then secondly, CCI is facing a temporary slowdown in its growth due to T-Mobile's recent acquisition of Sprint. It will lead to some lease cancellations through 2025 and prevent CCI from growing until then.

This warrants a somewhat lower valuation, but I believe that the market has overreacted to this and repriced CCI as if its growth story was over forever. In reality, our recent interview with CCI's management clearly revealed that they anticipate a return to their targeted 7-8% dividend growth rate by 2026. They are very confident in the reacceleration in their growth rate because they have already contractually secured much of that growth, giving them great visibility.

The headwind from the Sprint lease cancellations is only temporary, but the market is too focused on short-term results to recognize this.

As such, you today have the once-in-a-decade opportunity to buy shares of this blue-chip cell tower REIT at its lowest valuation since the great financial crisis.

I predict that as its growth accelerates, the market will reprice it at a materially higher valuation multiple, resulting in substantial upside to those who buy it today.

Just getting back halfway to its previous peak would unlock 50% upside and that would still price it at a historically low multiple.

While you wait, you earn a 7% dividend yield , and when the growth reaccelerates to 7-8%, you will be earning ~15% average annual total returns on a constant multiple basis.

It is hard to find better risk-to-reward in today's market.

W. P. Carey Inc. ( WPC )

W. P. Carey is another blue-chip REIT that has sold off heavily and now trades at a historically low valuation multiple:

- It owns mainly industrial net lease properties that enjoy CPI-based rent adjustments, resulting in rapid rent growth in today's inflationary world.

- It has a strong investment grade-rated balance sheet that limits the impact of rising interest rates.

- It has a multi-decade track record of significant market outperformance, just like CCI:

But it is now priced at just 10x AFFO, or put differently, a 10% cash flow yield.

This low valuation is especially surprising when you consider that most industrial REITs commonly trade at >20x AFFO even following the recent crash. The largest, Prologis ( PLD ), currently trades at 22x AFFO.

They trade at such high valuation multiples because industrial properties are highly sought-after as they directly benefit from the growing trends of e-commerce and onshoring.

So why is WPC so heavily discounted?

Well, it seems that the market is failing to see WPC as an industrial REIT because historically, it has owned a diversified portfolio, including some retail and office properties.

However, this is now changing rapidly.

Just recently, WPC announced that it would spin off most of its office properties into a separate REIT and sell off the rest. It will then reinvest the proceeds into mostly industrial properties, which will increase its allocation to ~2/3 of its portfolio:

W. P. Carey

The other 1/3 is today invested in highly resilient net lease retail properties such as those owned by Realty Income ( O ). Think about grocery stores and home improvement stores leased to a strong tenant under a 10+ year lease with inflation-based rent escalators. This is very resilient.

W. P. Carey

I believe that this spinoff is great news for shareholders because it will allow WPC to rapidly get out of its worst assets - all while increasing its exposure to its best assets - reducing risks and improving its future growth prospects.

But the market hates it because of one reason: it will lead to a small dividend cut.

WPC announced that following the spinoff, it will slightly reduce its dividend in order to be in a better position to self-fund its future growth prospects.

That's perfectly understandable and the right thing to do in my opinion, considering that they are losing 10% of their assets and their cost of capital is today too high to pursue accretive investments.

By setting up the payout ratio at 70-75%, they will be less reliant on capital markets and be able to retain significant income to buy more industrial properties, further increasing their allocation to this desirable sector.

I predict that 5 years from now, their portfolio will be closer to 3/4 industrial and this will lead to massive rerating of the stock.

As I noted earlier, WPC is today priced at just 10x AFFO because the market doesn't know to which peer group it belongs and dividend-oriented investors are exiting the stock.

But in 5 years, the market will perceive WPC very differently and I expect it to trade at a multiple that's closer to those of industrial REITs.

This could unlock 50-100% upside from here and while you wait, we expect to earn a 7% dividend yield even after the cut.

Again, this is a once-in-a-decade chance to buy WPC at such a low valuation. It is temporarily hated, but I don't think that this will last.

Camden Property Trust ( CPT )

Finally, I want to discuss one of my favorite apartment REITs.

If cell towers and industrial properties aren't your thing, then perhaps discounted apartment communities will gain your interest.

Camden Property Trust is one of the highest-quality apartment REITs in the market:

- It owns a high-quality portfolio of mostly affordable apartment communities in strong sunbelt markets.

- It has one of the lowest leverages of all REITs with a low 30% LTV and just 4.3x debt-to-EBITDA. This gives it a strong A-rated balance sheet .

- Once more, this is a blue chip REIT with a long track record of significant market outperformance and steady dividend growth:

But it wasn't immune to the recent crash.

Nothing was.

And as a result, it is now heavily discounted:

This crash occurred even as CPT kept growing its rents at a rapid pace and so the discount is even greater than it may seem.

To give you a sense of just how cheap CPT has gotten, consider that it is now priced at a near 7% implied cap rate.

Yet, these assets generally trade at closer to a 4.5-5% cap rate in the private market. Just recently, UDR, Inc. ( UDR ), another apartment REIT, announced the acquisition of a Sunbelt apartment portfolio at a 4.5% cap rate.

This means that CPT is priced at a roughly 40% discount to its net asset value according to our own estimates.

Camden Property Trust

That's rather extreme! Typically, only distressed REITs would trade at such a large discount, but CPT is an A-rated blue chip with a growing cash flow.

This is its lowest valuation in a decade.

In fact, its valuation has gotten so low that it recently got the attention of Starwood, which is a major private equity group that's run by legendary billionaire investor Barry Sternlicht.

Starwood's latest 13F filling showed that they had built CPT into their single largest position. I would add that Barry Sternlicht said the following earlier this year in a televised interview:

"By the way, when credit comes back, you are gonna see REITs take off... There are some unbelievable bargains in REITs. We did the same thing during the pandemic. We bought a dozen stocks all over the world and we had a 70% IRR on that stuff. We are already buying some stuff in the public market..." Barry Sternlicht, CEO/Chairman, Starwood Q3 2023 CNBC Interview.

That sums up the opportunity quite nicely.

Even if you are conservative and assume that CPT's NAV will come down quite a bit as a result of the now higher interest rates, we estimate that it would still have about 50% upside from here and you get a 4% dividend yield while you wait.

Bottom Line

CCI, WPC, and CPT are three examples of once-in-a-decade buying opportunities in the REIT sector, but there are many others.

I made a small fortune buying discounted REITs following the crash of 2020, and today, these opportunities are even more compelling in many cases.

For further details see:

3 Once-In-A-Decade REIT Buying Opportunities