VNORP - 3 Questions And The Tornado Hitting Vornado

2023-04-27 12:08:40 ET

Summary

- The malaise in office space has been on the front pages for at least a year.

- Vornado Realty had two dividend cuts since the pandemic and then suspended it all together on April 26, 2023.

- The exodus of investors will keep VNO's common shares under pressure.

- We look at the preferred vs the bonds.

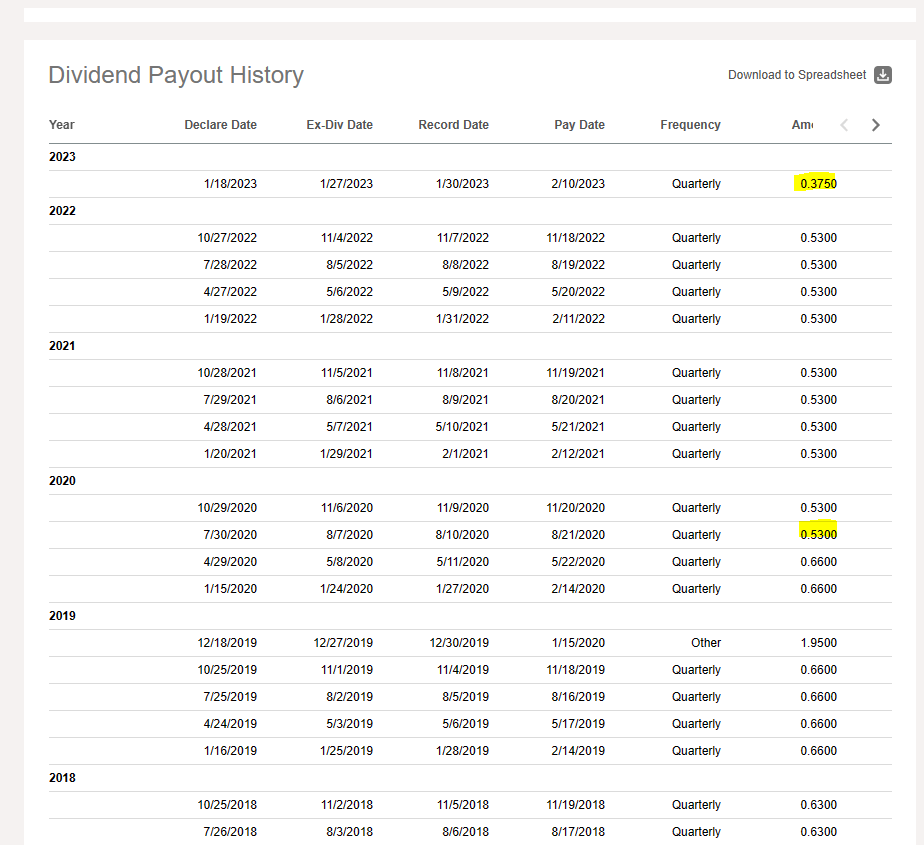

Investors were dealt a big surprise yesterday as Vornado Realty Trust (VNO) "paused" its dividends. Sure, one could argue that the stress in the office sector was clearly palpable and the writing was on the wall for some time. On the other hand the company had methodically cut its dividend twice, with the most recent one just last quarter. Surely that was enough?

{kind=link}

We look at what's going on and what this portends for the stock, preferred shares and VNO bonds.

The Recent Cut And The Lead Up

The commentary around the recent cut was interesting to say the least.

Steven Roth

Well the dividend is based upon a minimum of taxable income. Our taxable income allows us to reduce or I like to use the word right size our dividend. I mean, our dividend was 9.5% on our stock price, which everybody knows is kind of like, miss price and mistake. And we felt that it was inappropriate to overpay the dividends substantially over a taxable income. And we felt, the board felt also that it was appropriate to retain the extra 130 odd million dollars of cash. So that's what happened with the dividends.

Source: Q4-2022 Conference Call Transcript

That $130 million comes from the approximate difference of between the new rate and old rate multiplied into the shares outstanding.

The announcement yesterday went the extra mile and created a halt till the end of 2023.

VNO announced today that it will postpone dividends on its common shares until the end of 2023, at which time, upon finalization of its 2023 taxable income, including the impact of asset sales, it will pay the 2023 dividend in either cash, or a combination of cash and securities, as determined by its Board of Trustees.

VNO also announced that, in order to enhance shareholder value, its Board of Trustees has authorized the repurchase of up to $200 million of its outstanding common shares under a newly established share repurchase program. Cash retained from dividends or from asset sales will be used to reduce debt and/or fund share repurchases.

Source: Seeking Alpha

Till the end of this year, the move saves VNO $220 million. We're assuming that VNO will not pay any cash dividends and that is likely to be an extremely strong bet in this case. More importantly, between now and the end of 2025, this move will save VNO about $786 million. Let's look at how this saved amount compares to VNO's cash flow requirements over this same timeframe.

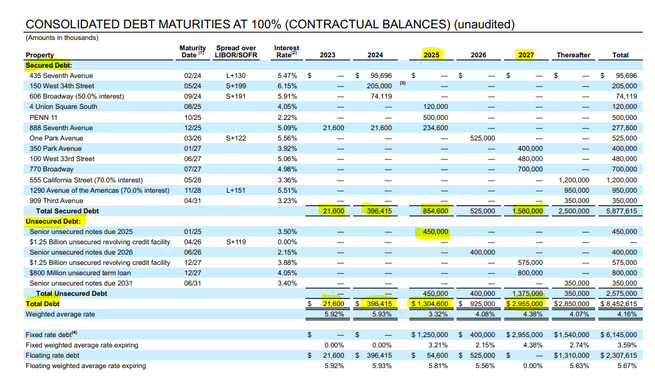

Vornado Realty's Debt Maturities and Cash Flow

VNO 2023 debt calendar looks extremely mild with just $21.6 million coming due. It picks up pace after that with close to $400 million in secured debt (as in against specific properties) coming due in 2024.

{kind=link}

2025 has a total of $1.3 billion and that is likely to be crucial year for VNO's viability. So the total debt payments, assuming nothing is refinanced, should equate to about $1.7 billion between 2023-2025.

While that may seem like a daunting number, let's keep in mind that according to analysts, VNO should produce close to $1.4 billion in funds from operations over this time frame.

{kind=link}

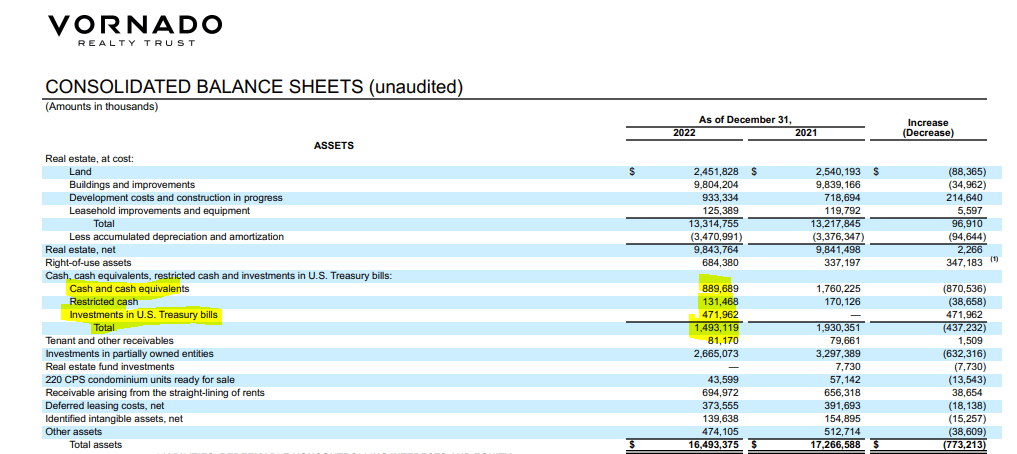

The company also had about $1.493 billion cash on hand at the end of 2022.

{kind=link}

If you use this starting point ($1.5 billion in cash), add the expected FFO ($1.4 billion) and subtract the debt maturities ($1.7 billion), you're standing in a rather healthy position. This also is assuming that none of these get refinanced and everything needs to be paid to the bank. Of course there are three crucial things missing from this analysis.

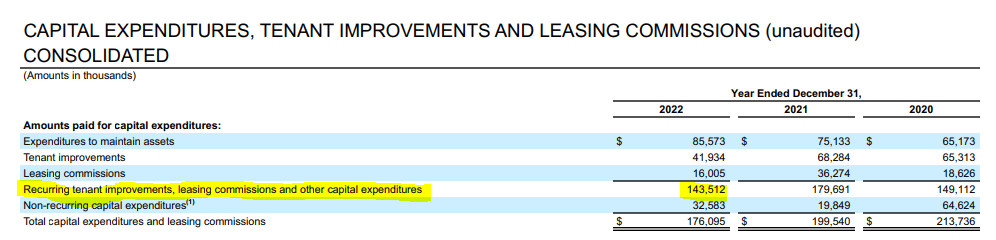

The first being that FFO is a very crude measure and in this case ignores all capex and tenant incentives that need to be done to keep tenants coming in. VNO breaks its capital expenditures down by recurring and non-recurring capex.

{kind=link}

Even using the recurring number and sticking to the $143 million, we're looking at $400 million till end of 2025. So that blows through a lot of our cushion.

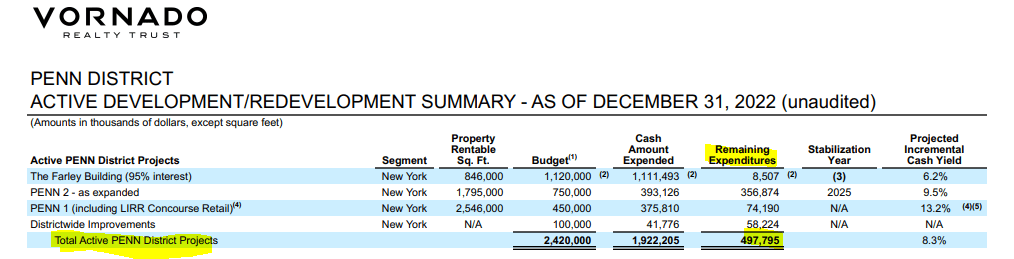

The second aspect here is the amount that's required to complete their active mega projects. PENN 2 is the big kahuna there and PENN 1 will be requiring $75 million worth as well.

{kind=link}

The total of close to half a billion is yet another big blow to the free cash flow over our projected timeframe.

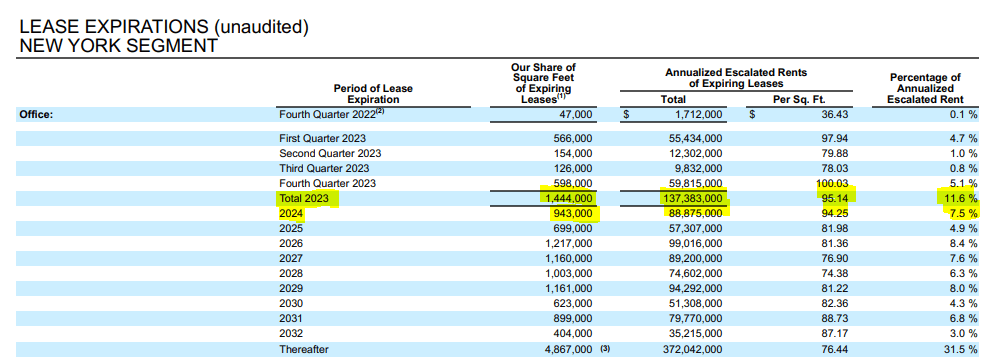

The third and final aspect here is that absolutely no analyst ever projects numbers based on a recession. Those FFO and free cash flow estimates likely get revised down when (not if, when) , we enter a recession. VNO has well spaced out lease maturities but even the amounts it does have, are challenging for today's times. Close to a quarter of the total revenues are scheduled for renewal over the 2023-2025 timeframe. On the New York office side, the nominal numbers are pretty large as well and VNO will likely have some serious step downs and/or some big tenant incentives to keep tenants in place.

{kind=link}

We also can glean this by the average asking rent.

JLL Office Insights-Twitter

The First Big Question

Investors are of course interested in knowing whether cash dividends will resume and our take there is "no." Depending on taxable income, VNO does need to pay certain minimum amounts and VNO will do what it needs to comply with this. This amount can also be paid in shares and at this stage of the war, VNO will not hesitate to dilute shareholders with non-cash payments. On the other hand, if it turns out that a small amount is needed to complete the requirements, you might get a few pennies of regular dividends near year-end. Either way, the regular dividends are not coming back any time soon.

The Second Big Question

Will VNO buyback shares in size? We think that's a hard "no." The whole idea here was to shore up liquidity and VNO is going to be in no hurry to start repurchasing shares until it can see the light at the end of the tunnel. The dividend cut was also designed to preserve its investment grade rating and the credit agencies are unlikely to look kindly upon splurging on share buybacks.

Fitch Ratings - New York - 30 Jun 2022: Fitch Ratings has downgraded the Issuer Default Ratings or IDR, for VNO and its subsidiary to 'BBB-' from 'BBB' and has maintained its Negative Rating Outlook . The ratings reflect VNO's persistently high leverage offset in part by its favorable competitive position in high-quality Manhattan properties that benefit from above-average access to institutional mortgage debt and private equity capital. VNO's portfolio has faced challenges since the onset of the pandemic and its impact on New York property market fundamentals, including higher vacancy rates.

VNO's initial high occupancy rates and long-term leases with solid credit tenants help balance this effect. Fitch has tightened its negative leverage sensitivity range by 0.5x and increased its stressed cap rate by 25bps to 7.25% to address the perceived relative strength of the NYC office market versus other REIT sectors.

Source: Fitch

The Third Big Question

With all this said investors must be wondering whether VNO shares are a buy. We think the answer is a no here. Without dividends coming back, the stock is likely to face a huge exodus over the next year and the risks are to the downside. As the recent dividend cuts in the office space show (see exhibits 1 , 2 and 3 ), the bottom comes months after the dividend cut. Heroes don't do very well jumping in on day 1.

An extension of this is should you buy anything else if you think the bottom in office is close? VNO has four preferred shares and their dividends are cumulative and will continue for now at least.

1) Vornado Realty Trust PFD SER L 5.40% ( VNO.PL )

2) Vornado Realty Trust 5.25% CUM PFD M ( VNO.PM )

3) Vornado Realty Trust 5.25 PFD SR N ( VNO.PN )

4) Vornado Realty Trust 4.45% CUM PFD O ( VNO.PO )

While the preferred shares should be rejoicing at the common dividend cut, they seem a little worried. We have also shown some of the upcoming bonds in the screenshot below.

Interactive Brokers Apr 27, 2023

{kind=link}

Keep in mind that those dividends are cumulative and also an outlet to meet minimum dividend requirements for REIT status. The counterpoint is that there are few scenarios where the debt blows through common equity cushion, without blowing through the preferred cushion.

These preferred shares are offering 10% yields for a reason and that reason is that they are very risky. If we were to buy something here, it would be the June 2026 bonds with an 8.232% yield to maturity.

Interactive Brokers Apr 27, 2023

{kind=link}

We think the combination of primarily secured debt maturing before that and the dividend suspension make it a very safe bet.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

3 Questions And The Tornado Hitting Vornado