NETL - 3 Reasons Inflation Will Continue To Fall: What To Buy

2023-06-19 07:30:00 ET

Summary

- Inflation is rapidly cooling off.

- This has major implications for investors.

- We explain what we are buying and why.

Co-produced by Austin Rogers

We have held the view all year that inflation has peaked and is now on the decline. This now seems to be the consensus view.

What is a little more hotly debated is (1) how low inflation will go, (2) how quickly, and (3) how long this period of disinflation will last.

The most recently reported CPI report (as of this writing) for May 2023 shows that year-over-year consumer inflation has fallen to 4.0%, compared to peak inflation of 8.5% in March 2022.

The ~40% surge in the money supply from the beginning of 2020 to the middle of 2022, resulting from unprecedented levels of fiscal stimulus, gradually worked its way through the US economy and produced a wave of price hikes in 2021 and 2022.

And then the Russian invasion of Ukraine happened, further disrupting supply chains. This had particularly pronounced effects on Europe, but it had ripple effects that made their way to the US, such as through higher oil & gas prices.

But today?

- Oil prices are falling...

- Supply chain bottlenecks are disappearing...

- Housing costs have stopped rising...

- Credit conditions are tightening...

- Commodities and producer prices are sinking...

And all of this is resulting in lower and lower inflation readings over time.

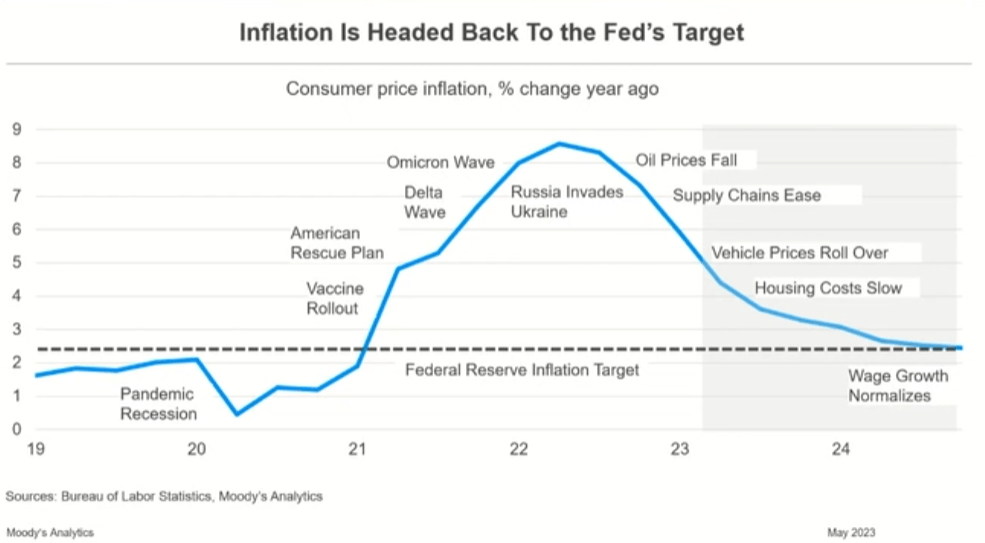

Mark Zandi - Moody's Analytics

{kind=link}

This chart from economist Mark Zandi forecasts the CPI to hit 3% by the end of 2023 and to return to the Fed's 2% inflation target by the end of 2024. We think this could be too conservative in terms of the speed with which inflation will come down.

Here are three reasons we see inflation continuing to fall rapidly and experience downward pressure for at least another year and a half.

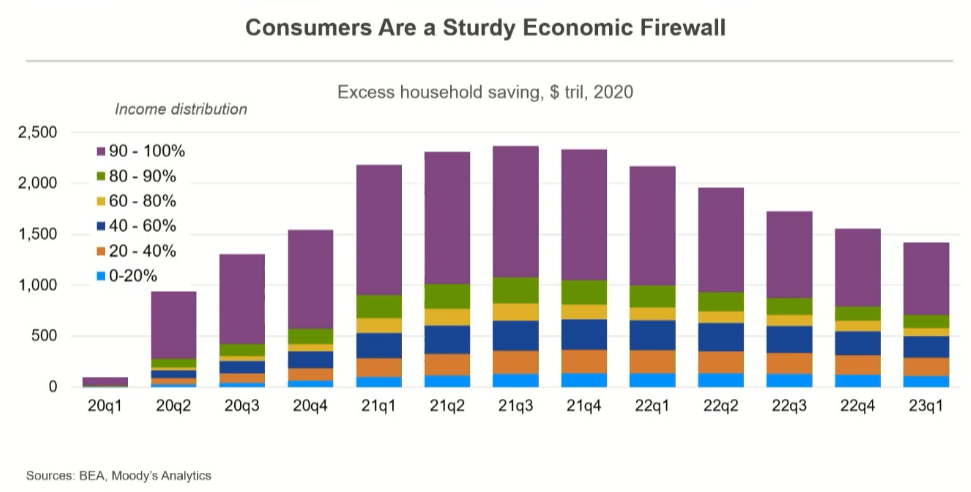

1. Pandemic-Era Savings Are Depleting

During the pandemic, the government distributed huge sums of fiscal stimulus, causing consumer excess savings to surge by nearly $2.5 trillion. Nearly half of that flowed to the highest income households through CARES Act tax holidays, PPP loans/grants, student loan relief that disproportionately benefited high-income workers, etc.

Mark Zandi - Moody's Analytics

{kind=link}

Putting them aside, you can see that the rest of households still have a decent amount of excess savings as well. This is why that long-anticipated recession hasn't gotten here sooner.

But those savings are running out, and they are depleting faster for some households than others.

Hence, we find that US credit card debt remains at its all-time high just shy of $1 trillion. Unlike the normal pattern of consumers paying off holiday spending in Q1, causing credit card debt to retrace a bit, credit card debt remained flat quarter-to-quarter in Q1 2023.

This, along with the fact that total personal saving of ~$802 billion remains well below pre-pandemic levels, certainly seems to suggest that many households don't have the level of excess savings that total numbers indicate.

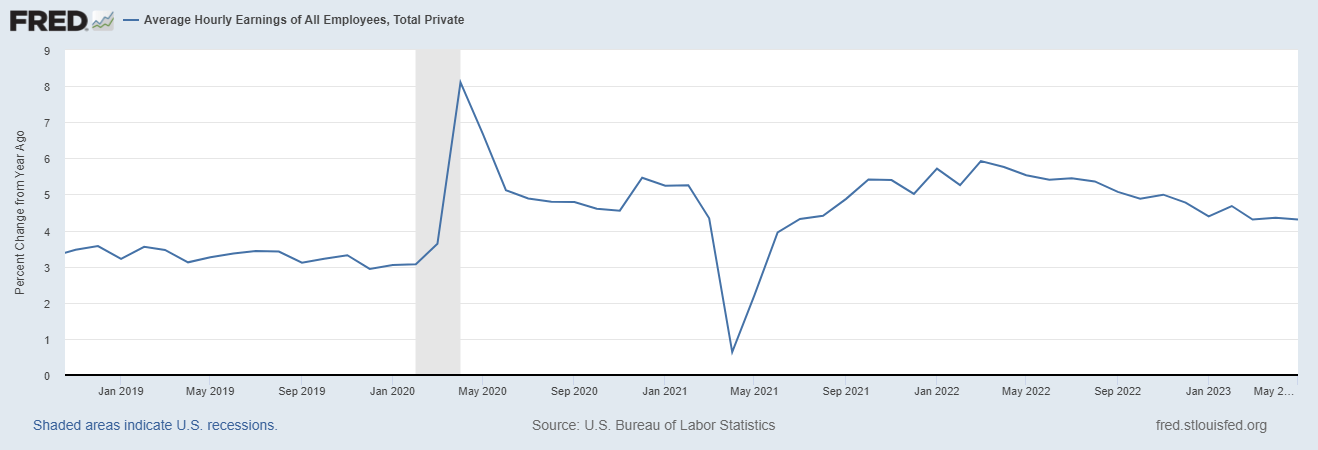

Adding to the overall picture of a weakening consumer is the gradual slipping of wage growth.

U.S. Average Hourly Earnings - YoY Change:

{kind=link}

The most recent reading from May 2023 shows a continued, gradual decline in wage growth, registering a 4.3% YoY rise in wages. Compare that to the peak in wage growth of 5.9% in March 2022. Interestingly, wage growth peaked at the same time as the CPI.

While the commonly held view is that wage growth causes inflation, we think the opposite is more true. Rising consumer prices puts pressure on employers (either from politicians, unions, CPI-based employment contracts, or the employees themselves) to raise wages to keep up with inflation.

So, in our view, wage increases are more of a catch-up to inflation than a cause of inflation.

Lastly, though the labor market does remain strong by and large, we are beginning to see some cracks appear. For example, initial unemployment claims recently reached near their highest level since the end of the pandemic.

It is not the strongest signal of a softening labor market, but as consumer spending continues to slow, more and more employers will rationalize their workforce through layoffs.

Layoffs mean less income to go toward consumer spending.

All of these metrics are pointing toward less inflationary pressure on the demand side.

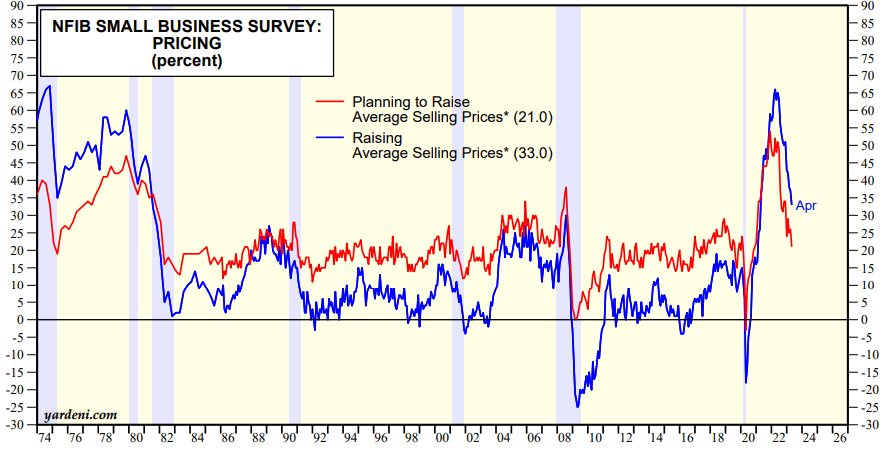

2. Small Businesses No Longer Planning Price Hikes Or Capital Spending

On the supply side, things have eased quite a bit as well.

For example, if you look at the NFIB survey of small businesses, you'll find that the number of small businesses reporting current price hikes and plans to raise prices in the near future is plummeting.

{kind=link}

As supply chains ease and consumers rein in spending, businesses don't have the room or need to raise prices anymore.

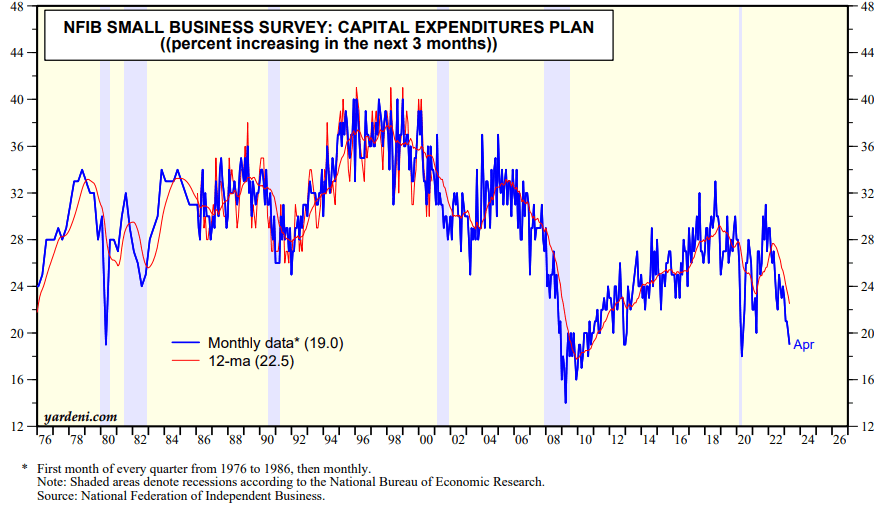

The same goes for small businesses' plans to increase capital expenditures in the next three months -- plummeting. It's already at recessionary lows with no signs of stopping.

{kind=link}

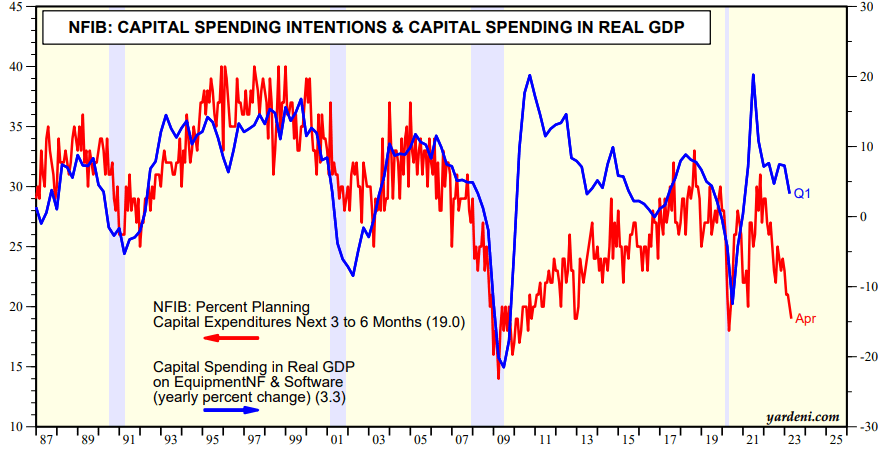

Less business spending has a similar effect on inflation as less consumer spending. It contributes to lower prices, and it correlates strongly with an oncoming recession.

In fact, if you look at capital spending in in real GDP terms, it tends to slow to very low growth (low single-digits) right before a recession, and then it plunges into deep contraction during recessions.

{kind=link}

As of Q1 2023, capital spending continued to be in slightly positive territory in terms of real GDP, but if businesses' future spending plans are an indication, that should soon be dropping into contractionary territory.

So, in short: Small businesses are no longer raising prices, nor are they planning further capital spending. This is a strong indicator of both recessionary conditions and lower inflation in the coming months and quarters.

3. The Lagged "Shelter" Component Of The CPI/PCE Is About To Turn Down

Housing/shelter makes up about 40% of the CPI by weighting, so whatever housing prices do strongly affects the overall CPI rate. A relatively little-known fact about the shelter component of the CPI is that it lags behind real-time housing data by about a year. It tends to correlate with the average of all rents, which reset roughly every 12 months, rather than lease-over-lease rent growth for expiring leases.

According to Apartment List's National Rent Report, residential rent growth peaked in late 2021 and has been easing since then.

At this point, real-time rent growth has slowed to the low single-digits, roughly where it hovered in 2018 and 2019, although it continues to go down.

Apartment List

It's the same story with home price growth, which peaked at over 20% in early 2022 and has since been falling. Home prices have even begun declining across much of the country.

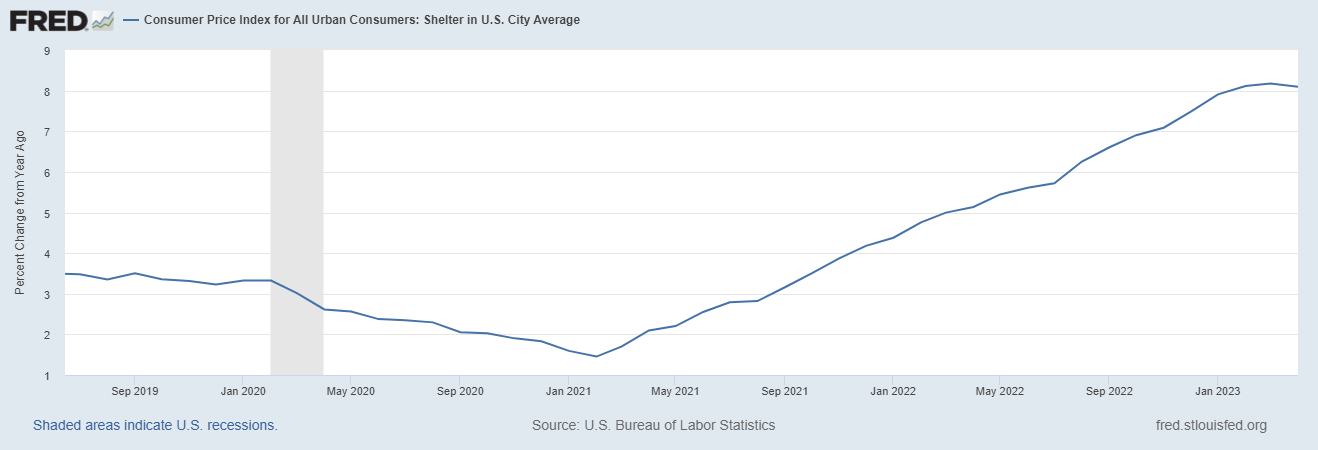

And yet, as recently as April, the shelter component of the CPI (and personal consumption expenditures or "PCE" which the Fed prefers to use) continued to show 8% YoY growth!

Shelter Component of CPI - YoY Change:

{kind=link}

This lag is a major reason why the Fed was slow to see inflation coming in 2021 and early 2022. It's also a major reason why the CPI and PCE continue to mid-single-digit growth even though real-time prices aren't rising that much.

And it's a major reason why the shelter component of inflation metrics is about to turn down and slide lower for at least a year, probably closer to two years. This will steadily weigh further and further upon the topline inflation rates being reported.

What To Buy Today

At High Yield Landlord, we are bottom-up value investors. We seek to own quality companies at deep discounts to fair value while capturing high dividend yields in the process.

But understanding the macroeconomic backdrop does help us think through our portfolio and which REITs to emphasize in our current buying.

In short, our macro view is that inflation measurements will continue to steadily fall for at least another year, probably closer to two years, unless some unexpected economic shock interrupts the trend. Economic growth will also weaken, though, and the combination of these factors will eventually lead to falling interest rates.

About 25% of our portfolio is invested in net lease REITs ( NETL ) ( VNQ ), which we think is strategic. These REITs have long lease terms, typically 10 years or more on a weighted average basis, at contractually fixed rent rates and rent escalations of 1-3% per year.

Obviously, 1-3% annual rent growth sounds pitiful during periods of inflation reaching as high as 8-9%. But keep in mind that net leases obligate tenants to pay for all or most property taxes, insurance, and maintenance, so those 1-3% annual rent hikes flow directly into NOI and cash flow.

And that doesn't even consider the effect of external growth through acquisitions, which are the primary channel of growth for most net lease REITs.

Here are some examples of net lease REITs to consider buying today:

- Agree Realty ( ADC ) : Focused solely on the largest and strongest retailers in the nation in highly fungible, freestanding box-style store formats. ADC enjoys perhaps the strongest balance sheet and lowest cost of capital in the net lease REIT space, allowing it to grow its portfolio rapidly through acquisitions, offsetting the low ~1% annual rent escalations.

Agree Realty

- Alexandria Real Estate ( ARE ) : Though it owns and develops life science properties leased primarily to the world's largest and strongest biotech companies, ARE almost exclusively uses net leases with 3% annual rent escalations. On top of that, it enjoys a healthy development pipeline in the nation's best located and most productive life science clusters.

Alexandria Real Estate

- Essential Properties Realty Trust ( EPRT ) : Focused on sale-leasebacks to middle-market businesses primarily in service and experience-based industries, EPRT is similar in many ways to the formerly public STORE Capital. Its leases feature rent escalations of 1.5-2% per year, master leases (covering multiple stores), and unit-level financial reporting.

Essential Properties Realty Trust

- VICI Properties ( VICI ) : The "landlord of Las Vegas" that is the largest owner of casino resort real estate on the Las Vegas strip as well as regional gaming hotspots around the country. Gambling tends to be fairly recession-resistant, and VICI's multi-decade leases feature ~2% annual rent escalations.

VICI Properties

In the current late-cycle or early recessionary environment, we think net lease REITs are the perfect blend of growth potential and defensiveness.

For further details see:

3 Reasons Inflation Will Continue To Fall: What To Buy