VWO - 3 Reasons To Buy VWO For 2023

Summary

- There is an opportunity to over-allocate towards emerging markets in 2023 due to softening USD, reopening China and firm commodities.

- Emerging markets do well when the USD is softening and cooling inflation may allow the Federal Reserve to pause earlier than expected.

- China is a significant holding in Vanguard Emerging Markets ETF and growth will benefit from reopening and stronger government support.

- Emerging markets are long overdue a period of outperformance and native currency tailwinds will help debt and equity returns.

Introduction

2023 looks like an opportunity to add non-correlated alpha to your portfolio by over allocating to Vanguard Emerging Markets Stock ETF ( VWO ). It's been more than a decade since the last time VWO outperformed the S&P 500 ( SPY ) but this year presents that opportunity for several reasons.

- A weakening dollar - This helps emerging markets and the US dollar has likely peaked.

- China - VWO's allocation to China shouldn't be a drag this year due to a boost from reopening following Zero COVID policy and a more supportive government policy package for the economy.

- Firm commodity prices - Partly due to Russia sanctions and partly due to economic stimulus in China we expect prices to remain firm and support commodity producer component of emerging markets.

We will discuss these items in more detail, the potential risks and also a potential alternative should you to invest in emerging markets without China.

Vanguard Emerging Markets Index ETF

Here is a quick overview.

Data Vanguard

Vanguard always runs an inexpensive fund and VWO has good asset size and liquidity.

It is also interesting to see the PE ratio at 11.5 which seems very fair and reasonable. Particularly when the S&P 500 is trading in the 18-20 times earnings range at present.

This author is old enough to recall the emerging market boom of 2005-2008. Back then, emerging markets and in particular BRIC funds, commanded a premium earnings multiple. This premium has turned into a discount over the last 15 years. Perhaps it is time for a decline in this level of discount.

Peak Dollar is in, helping Emerging Markets.

If you've followed global economics for a while, it will be obvious that a strong dollar is usually the cause of most emerging market crises. As US Treasury Secretary John Connally explained to the Europeans way back in 1971 "the dollar is our currency, but it is your problem."

That's doubly true for emerging markets.

A strong dollar means higher repayments of US dollar denominated debt from governments and private companies. It often also means higher interest rates as many countries try to stop inflation by preventing a currency decline. Recession, balance of payment shocks and IMF bailouts often result. Last year Sri Lanka, Pakistan and Argentina were among those that suffered.

Below, can you see the inverse correlation between a dollar index and VWO?

The opposite also holds true - when the dollar weakens, that's good for emerging markets. Despite the strength of the US dollar in the last couple of weeks, we expect a return to US dollar easing in 2023.

Why a soft US dollar? Inflation is beaten

Short term movements in currencies are often driven by interest rate differentials and last year the Federal Reserve was aggressive.

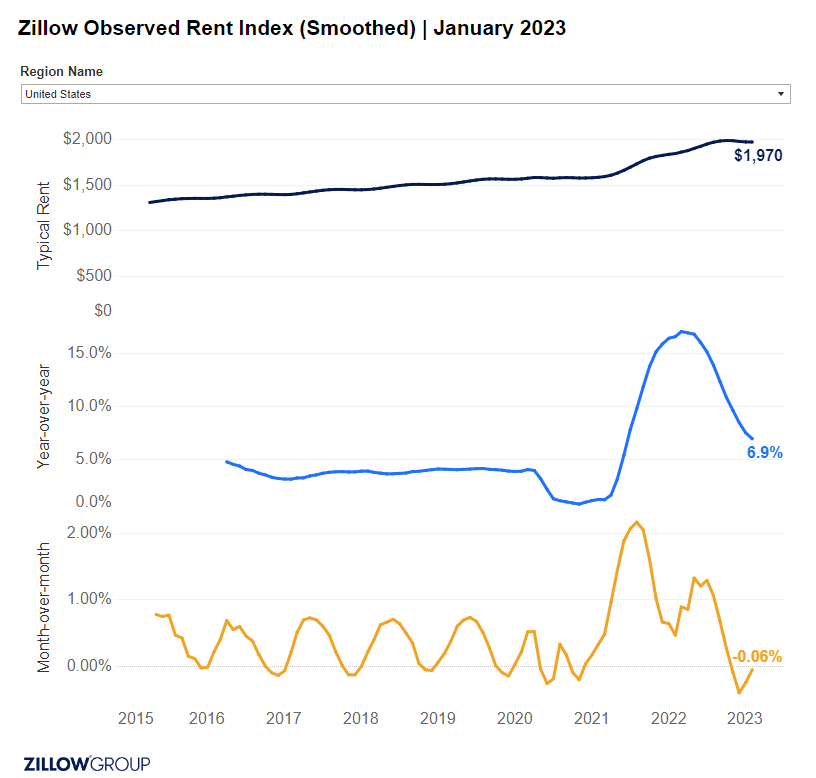

The good news is that we see signs that core CPI in the US already being defeated. All we are waiting on is for the CPI data to reflect the rental price falls that the Zillow Monthly Rental Survey is already showing. We discussed this in our article on VGLT a few weeks ago, but to briefly restate our case.

{kind=link}

The Core CPI data from the Bureau of Labor Statistics is conducted by survey on what all renters are paying. Zillow surveys those who started a lease during the current month. Thus the CPI data lags. Some estimate as much as 4 quarters but we'd say the impact shows up sooner, but is still 6-9 months.

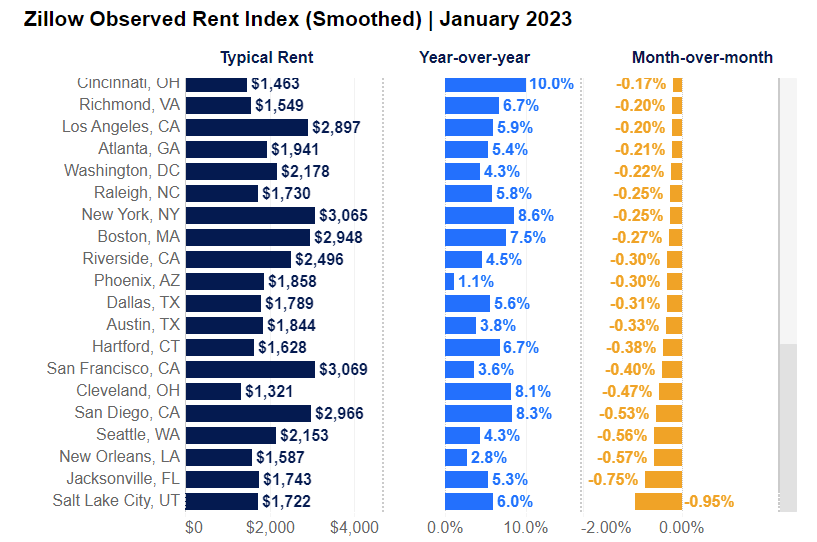

Below, we have highlighted the softest metro markets on a month-on-month basis. In particular large expensive cities like LA (-0.20%), New York (-0.25%), San Francisco (-0.40%) and San Diego (-0.53%) are pulling the index down yet they are far from alone.

{kind=link}

Relatively smaller and more affordable markets like Louisville (0.87%), Buffalo (0.80%) and Memphis (0.47%) were the strongest on a month-on-month basis in January.

Overall a moderation and equalization of property rents seems to be underway. The Zillow monthly rent index was negative again, just, in January.

This was the 4th month of falling prices in a row. Given rent is 42% of Core CPI, a decline in prices at a rate of just 0-2% annualized makes the inflation measures moderate very quickly and effectively.

China Reopening and Government Support

Given China is the 35.8% of VWO and also second largest economy globally, it is important to understand how these markets might perform.

First some history. To show how these allocations have performed, we have chosen proxies. These are iShares MSCI Hong Kong ETF ( EWH ) and xTrackers Harvest CSI 300 A-Share ETF ( ASHR )

It is clear that the release from zero-COVID policies in late November 2022 was a clear turning point after an awful 2 year period. Prior to the policy change, the economy was in an increasingly weak position.

Chinese consumers are cashed up and ready to spend

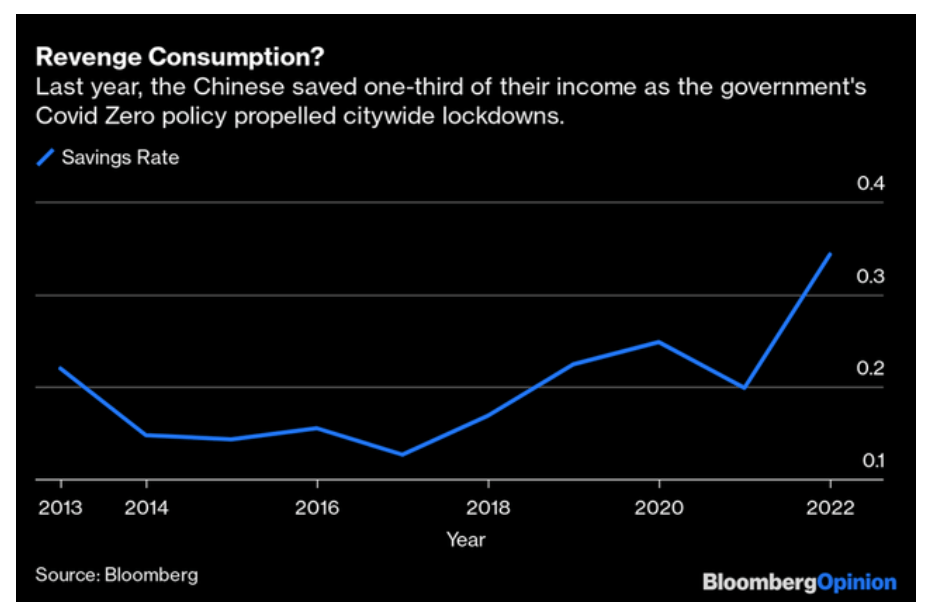

We believe China's economy was significantly weaker than the officially reported 3% growth rate in 2022. Based on our extensive contacts in China we estimate that the economy was in moderate recession. Note past tense.

By contrast 2023 will be radically different and this will flow through to earnings. Spending growth will come from savings, which spiked massively in 2022 to about 1/3 of income. A high savings rate often causes recession.

Consumer spending will rebound strongly in 2023.

{kind=link}

With money to spend and the freedom to do so, Chinese consumers will drive a rebound in the F&B, travel and household service sectors.

The Government is Helping the Economy

The government worked to cool the economy with various policy measures and was very successful. The property sector is now very week.

We don't see a strong rebound in the moribund Chinese property market, but a stabilization and completion of existing projects will help the economy and sentiment enormously. The government has finally recognized it needs to stimulate and support the sector and economy, which is itself good news.

The government released a significant package of policies. These include relaxing leverage ratios for Chinese developers, lower mortgage rates for home buyers. In some cities like Wuhan, the government has relaxed rules on buying second and third homes.

Between reopening and government support, the China economy will be far stronger in 2023.

Firm Commodity Prices

Firm commodity prices are usually associated with being a positive for emerging markets. Better export prices help currencies and economies.

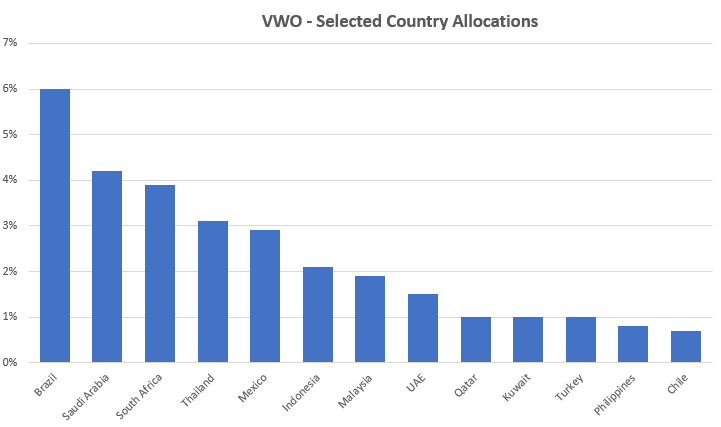

This isn't just a rumor. After China, the next dominant trend would be the 20-25% of VWO's country allocations would be to commodity exporting firms.

Following the Top 3 (China, Taiwan, India) the remaining allocations are dominated by commodity producers.

Here is a list for countries ranked 4th to 16th in VWO allocations.

{kind=link}

On this list, only Thailand, Malaysia, Turkey and Philippines are debatable as being described as commodity exporters.

Usually during a recession, or the expectation of one, you can expect commodity prices to fall - see 2020 below for example.

Yet commodity prices continue to remain elevated.

This cycle is different because of the Ukraine war.

Russia's invasion of Ukraine, and subsequent sanctions, has caused a spike in commodity prices that has only partially unwound. The commodity price index above remains well above pre-COVID levels that existed in the 2016-2020 period. This will drive GDP growth in commodity driven emerging markets.

A unfettered return Russia's commodity exports to world markets does not appear imminent. This would probably only occur under drastic changes such as a change of Russian leadership and Ukraine withdrawal. Sadly, neither appears likely in the short term.

Risks

The future is unknowable, but here are a couple of possible scenarios that could affect emerging markets in 2023.

- Equity markets have another bad year.

Consecutive negative years for equity markets are very rare, but they can happen. Emerging markets do have a correlation with developed markets. It is often the case that when markets turn risk averse, so-called 'riskier assets' are affected more. The chances of another large market drop in 2023 however aren't high in our opinion given the tailwinds of falling inflation and China reopening and firm employment.

- The US dollar unexpectedly goes on another strong run.

Another strong run past recent highs for the US dollar is unlikely, but possible. This will again return pressure to emerging economies and crimp USD returns. The chances here don't seem high because we find inflation cooling arguments to be very persuasive, as above. However a significant expansion of conflict in Europe outside Ukraine might be such a catalyst. It's doubtful however, that Russia can spare the resources and Europe, mostly, lacks the will.

- The world enters significant recession.

Just a couple of months ago this looked close to inevitable but China has had COVID in record time and is almost fully reopened. Europe avoided an energy crisis via a warm winter and the US employment situation remains strong. It's still not impossible if the US Federal Reserve overtightens.

- What about emerging market volatility?

We believe that a broad based ETF like VWO will have lower volatility than all but the most conservative individual stock. Thus an ETF like VWO should fit in most portfolios, with the obvious exception of a capital preservation strategy.

- What if China and the US come to military blows?

In 2023 the chances of conflict are next to zero.

Russia's difficulties demonstrate the dangers of military misadventures. However year-by-year, the risk here inches up. The recent balloon controversy illustrate the risk of unexpected accidents in an environment lacking both trust and communication.

If it happens, then exit emerging markets immediately. But for a China-US war, you should probably re-consider your entire stock market holdings. Then buy US treasuries and possibly an underground bunker. It would be that awful. Luckily it is still very much a long tail risk not worth hedging at present.

Summary - Buying the Dip to $40

Buying when negativity is around is obvious but trickier than it looks.

The recent return of worries of inflation/rates and Federal Reserve hawkishness has created a small pullback that is worth buying.

We believe that the lows of this cycle were in October and buying near the December low point around $39-40 per share is an opportunity worth taking.

We hold this position for ourselves and clients. Emerging Markets however are not suitable for Capital Preservation and other ultra-conservative portfolios.

For further details see:

3 Reasons To Buy VWO For 2023