PSCE - 3 Reasons To Invest In Energy Funds XLE

Summary

- Energy was the best-performing industry in 2022.

- Energy fundamentals remain strong, and getting stronger.

- The best is yet to come.

Energy was the best-performing equity industry in 2022, and by quite a large margin. The Energy Select Sector SPDR ETF ( XLE ), the industry benchmark, was up 64.3% during the year, even as the S&P 500 tumbled 18.2%. Outstanding performance, and one which I believe will continue into 2023, for three key reasons.

Improved economic fundamentals should underpin strong energy demand and prices.

Capital discipline means energy prices should remain elevated, and that dividends and buybacks remain strong.

Cheap valuations means potential capital gains remain strong, even though share prices have skyrocketed these past few months.

Energy outperformance is set to continue, in my opinion at least. XLE is a simple U.S. energy equity index ETF, should benefit from these three trends, and is a buy.

XLE - Quick Overview

Quick overview on XLE before looking at some energy industry trends.

XLE is a simple U.S. energy equity index ETF, tracking the Energy Select Sector Index. It is a simple index, investing in all S&P 500 energy stocks. By virtue of only investing in S&P 500 stocks, the index only includes large-caps. It is a market-cap weighted index.

As the energy industry is quite small, the resultant portfolio is quite concentrated. XLE only invests in 23 securities, while most broader equity indexes investing in hundreds / thousands of securities. Concentration is quite high too, with the fund's two largest holdings, energy giants Exxon ( XOM ) and Chevron ( CVX ), accounting for over 40% of the value of the fund. All of the fund's holdings are U.S. energy stocks, as expected.

XLE

XLE's lack of industry diversification means the fund's performance is entirely dependent on the performance of one specific industry, which increases risk, volatility, and the probability of significant underperformance. Risk is magnified by the fund's relatively low number of holdings, and high concentration. In my opinion, although XLE is not an excessively risky investment, risks are higher than average, so investors should take care to properly size any prospective investment. Massive overweight positions in energy are unwise, in my opinion at least.

XLE yields 3.6%, more than double the S&P 500's 1.6% yield, but a relatively low yield relative more income-focused asset classes.

XLE focusing on U.S. energy stocks means the fund should outperform when the energy industry does well, and several trends are pointing towards continued industry strength. Let's have a look.

Energy Industry Investment Thesis

Improved Economic Fundamentals

Energy industry performance is strongly dependent on energy demand and prices. When demand is high, energy companies can sell a lot of oil, natural gas, and other assorted energy products for very high prices. When demand is low, energy companies can't do so, and are forced to shutter their most unproductive, marginal oil wells and production sites, and sell their remaining production for very low prices.

Demand is everything for energy companies, and demand seems set to boom. Locally, the U.S. economy keeps humming along, with GDP growing at a reasonably good 2.9% pace last quarter , and with strong job growth in January . Internationally, China is set to re-open its economy / modify its Zero Covid policy in early 2023 , which should lead increased economic growth and manufacturing production in the country, boosting energy demand and prices. Improved economic fundamentals should benefit the energy industry and, by extension, XLE.

Normalizing inflation also serves to significantly reduce the risk of reduced demand / a recession. As readers are probably well aware of, inflation is currently elevated, reaching 6.5% in January . Inflation is significantly above target, and so the Federal Reserve is engaging in aggressive rate hike cycle to bring inflation back under control. These rate hikes are something of an albatross over the economy in general, and the energy industry in particular.

Rate hikes could be severe enough to cause a worldwide recession, depending on how inflation evolves from here on out. If inflation remains higher than expected for longer, the Federal Reserve would be forced to hike rates until a recession crushes inflation. Energy demand and prices would almost certainly decrease during said scenario, leading to significant losses for XLE. If inflation normalizes relatively quickly, the economy just might achieve a soft landing, with inflation easing as the economy continues to grow. Inflation is slowly normalizing, slightly decreasing YoY, moderately decreasing MoM, so a brutal, hike-induced recession seems unlikely, at least if current trends continue.

As a final point, although economic fundamentals are important for all equity industries, they are particularly important for the energy industry. Energy prices are famously volatile, so even small changes in underlying conditions can lead to significant changes in energy prices, and energy company returns and valuations. The energy industry is also structurally leveraged, with small changes in revenues leading to outsized changes in earnings. All industries benefit from rising prices in their industries and vice versa, but the effect is particularly pronounced for energy.

J.P. Morgan Guide to the Markets

Capital Discipline

Energy prices are highly cyclical, going through long periods of elevated prices, due to increased demand, followed by low prices, due to increased supply. The energy industry is quite cyclical too, and tends to perform quite well when prices are elevated, less so when prices are low.

There is, however, no law saying that both energy prices and energy industry performance must be cyclical. Both are somewhat dependent on decisions taken by energy industry players, and these might not necessarily reinforce the natural cyclical pattern of the industry. As an example, the U.S. energy industry responded to moderately elevated oil prices in the 2010s by massively ramping investment in unprofitable shale plays, leading to $300 billion in losses , and to (almost) a lost decade for energy investors.

Energy cycles won't save investors if the industry decides to set $300 billion on fire, as they decided to do last decade. Importantly, the industry has steadfastly decided not to repeat their previous mistake, opting for capital discipline instead. CAPEX is being restrained while dividends are being increased and buybacks doubled . The industry seems intent on making the best out of the current energy price boom.

Capital discipline helps energy investors in two key ways.

First, it helps sustain elevated energy prices, and hence energy industry earnings and valuations. Exxon, Chevron and the rest are not massively ramping up CAPEX, so supply seems certain to remain constrained moving forward, which should help keep prices high.

Second, it serves to significantly de-risk the industry. Investing in shale plays might increase earnings. Buybacks almost always increase EPS and dividends almost always increase shareholder returns, with extremely few exceptions. Investors should feel much more comfortable investing in companies with sizable dividends and buybacks programs compared to those with massive CAPEX, although returning cash to shareholders does somewhat reduce potential returns. CAPEX might be more profitable or beneficial to investors than dividends, but dividends are always a safe, reasonably good choice.

Energy industry capital discipline should serve to maximize shareholder returns during the current price cycle, a significant benefit for XLE and its investors.

Cheap Valuations

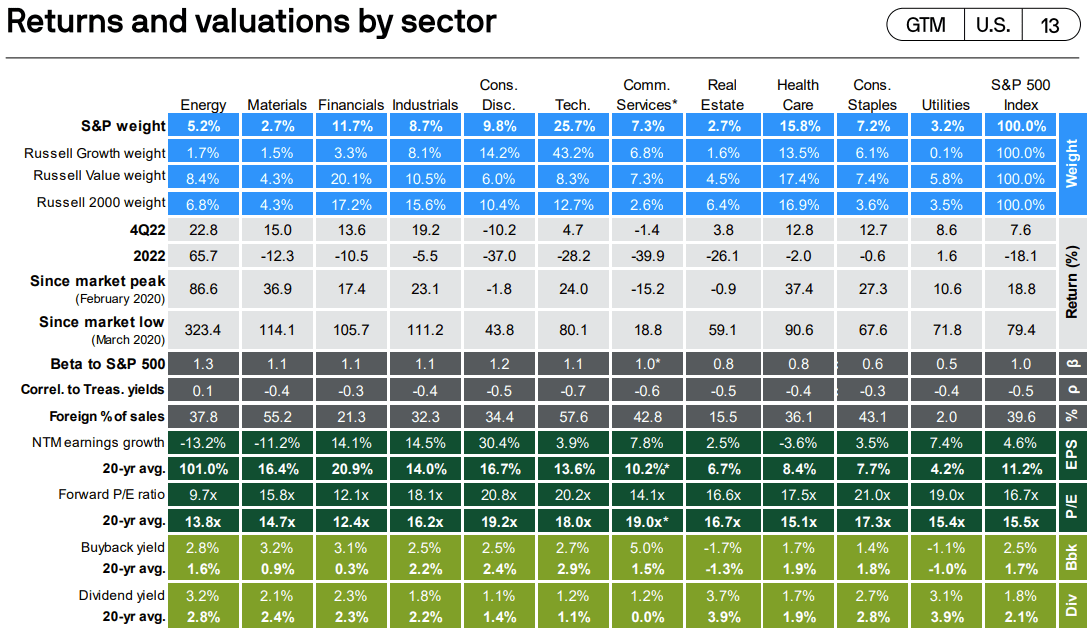

Even though energy industry share prices and valuations have skyrocketed these past twelve months, they remain relatively cheap relative to historical and equity industry averages. As per J.P. Morgan, the U.S. energy industry is the cheapest industry in the market today, with a low 9.7x PE ratio. Energy valuations are over 40% lower than their historical average, a sizable valuation gap. For reference, the S&P 500 currently trades with a 16.7x PE ratio, around 10% higher than its historical average. Table for reference, you might have to squint to see the information though.

J.P. Morgan Guide to the Markets

{kind=link}

Cheap energy valuations means strong potential capital gains for XLE and its investors, a benefit for the same.

Cheap energy valuations also mean that prospective investors can still initiate a position in XLE or other energy funds: they are not late, valuations are still decent.

As a final point, energy looks cheap under current economic conditions , which can always change. Although I believe that trends point towards strong economic conditions moving forward, these are far from certain. The energy industry and XLE would almost certainly underperform during a recession or commodity price crunch, and energy prices are somewhat more elevated than usual.

Some Other Energy Funds

Finally, a quick look at some other strong energy funds as alternatives to XLE.

The Invesco S&P SmallCap Energy ETF ( PSCE ) is a simple small-cap energy index ETF. PSCE's small-cap holdings are riskier than average, but sport very low valuations, and so potential returns are stronger. PSCE is riskier than XLE, but its potential returns are stronger too.

The Global X MLP & Energy Infrastructure ETF ( MLPX ) is a simple midstream energy index ETF. MLPX's midstream holdings have below-average exposure to energy prices, and so tend to underperform relative to peers when energy prices are high / increase, and outperform when energy prices are low / decline. MLPX also sports a 5.3% dividend yield, higher than XLE's 3.6% yield. MLPX is less risky and volatile than XLE, yields more, but should underperform during energy bull markets.

Conclusion

XLE is a simple U.S. energy industry ETF. In my opinion, said industry and fund is set to outperform in the coming months and years, due to improved economic fundamentals, capital discipline, and cheap valuations. XLE is a strong investment opportunity, and a buy.

For further details see:

3 Reasons To Invest In Energy Funds, XLE