SPHY - 3 Reasons To Invest In High-Yield Corporate Bond ETF SPHY

2023-11-21 13:00:00 ET

Summary

- SPHY offers diversified exposure to high-yield corporate bonds with a strong 7.4% dividend yield.

- SPHY has an expense ratio of 0.05%, lowest in its peer group.

- An overview of the fund follows.

The SPDR Portfolio High Yield Bond ETF (SPHY) offers investors diversified exposure to high-yield corporate bonds, sports a strong, growing 7.4% dividend yield, is much cheaper than average, and has outperformed most of its peers since inception. SPHY is a strong investment opportunity, and a buy.

SPHY - Basics

- Investment Manager: State Street

- Underlying Index: ICE BofA US High Yield Index

- Dividend Yield: 7.36%

- Expense Ratio: 0.05%

- Total Returns CAGR 10Y: 3.78%

SPHY - Overview and Analysis

Index and Portfolio

SPHY is a simple high-yield corporate bond index ETF, tracking the ICE BofA US High Yield Index. Said index includes all dollar-denominated bonds with non-investment grade credit ratings, subject to a basic set of liquidity, size, and maturity criteria. It is a simple, broad-based index, and a good benchmark of the U.S. high-yield corporate bond market.

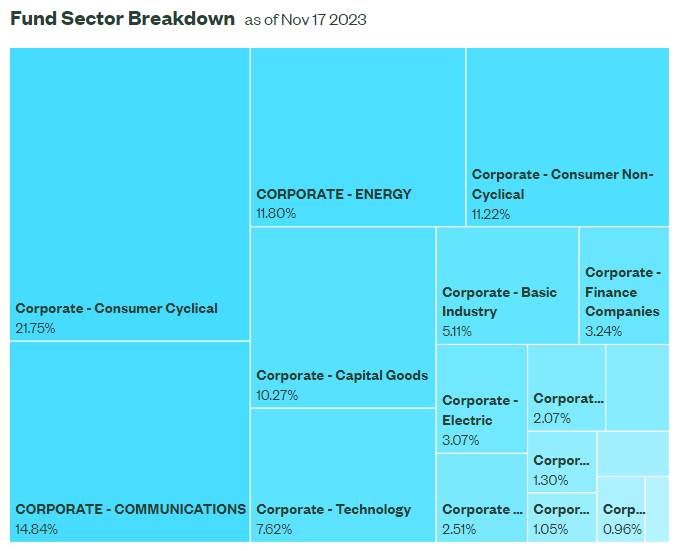

SPHY is an incredibly well-diversified fund, with investments in almost 2,000 different securities from all relevant industry segments. Concentration is quite low too, with very few issuers with weights higher than 1.0%.

{kind=link}

SPHY focuses on non-investment grade corporate bonds, with a small allocation to bonds rated BBB. These are likely recently upgraded bonds, which the fund should divest from in the coming months.

SPHY - Chart by Author

Besides the above, not much else stands out about SPHY's underlying index or portfolio.

Strong, Growing 7.4% Dividend Yield

SPHY focuses on non-investment grade corporate bonds, which almost always sport above-average coupon rates. SPHY itself currently yields 7.4%, a reasonably good yield, and higher than that of most bonds and bond sub-asset classes. SEC yield and yield to maturity, two more forward-looking dividend metrics, are higher still, at 9.2%. Dividends should be closer to 9.2% than 7.4% moving forward, assuming no significant changes in market conditions.

Fund Filings - Chart by Author

SPHY's dividend yield is also higher than average for a high-yield corporate bond ETF, and by reasonably healthy margins.

Fund Filings - Chart by Author

SPHY's dividends have seen very healthy growth since early 2022, due to Federal Reserve hikes. Further growth seems likely, as the fund still holds many older bonds, issued when rates were lower. Growth is strongly dependent on future Fed policy, so growth is not certain.

SPHY's strong, above-average 7.4% dividend yield is a significant benefit for the fund and its shareholders, and its core investment thesis. This is first and foremost an income vehicle, which investors buy (or not) for its dividends.

Moderate Potential Capital Gains

SPHY's strong dividends will likely account for most of the fund's long-term total returns, but the fund might see some moderate capital gains as well. This is because the fund holds tons of older corporate bonds, whose prices declined as the Federal Reserve hiked rates. Importantly, these bonds must be paid back in full at maturity, so prices should rise as this occurs.

As per my calculations, the fund's underlying bonds trade at a 12% discount to par, with an average maturity of 4.9 years. This amounts to 2.4% in (potential) capital gains per year, a reasonably good amount. Realized capital gains will likely be lower, as some bonds default, and as some are sold before maturity. Capital gains are incredibly uncertain, and strongly dependent on economic conditions, Fed rate policy, and investor sentiment.

High Credit Risk

SPHY's non-investment grade corporate bonds have high yields, but also high credit risk. The fund focuses on securities rated BB and B, as is the case for most high-yield corporate bonds.

Fund Filings - Table By Author

SPHY's credit risk is above-average, which results in above-average volatility and losses during downturns. As an example, the fund was down 13.6% during 1Q2020, the onset of the coronavirus pandemic.

Data by YCharts

SPHY's high credit risk is an important negative for the fund and its shareholders. I don't see it as a deal-breaker, but more risk-averse or bearish investors might disagree.

Interest Rate Risk

SPHY's non-investment grade corporate bonds tend to have short maturities, as investors are loathe to extend long-term credit to risky issuers (too risky). Due to this, interest rate risk and duration are both quite low, with the fund itself sporting a duration of 3.5 years, much lower than average.

Fund Filings - Chart by Author

Due to the above, the fund tends to experience below-average capital losses / reductions in its share price when interest rates rise, leading to outperformance during the same. As an example, the fund has outperformed since early 2022, when the Fed started to hike.

SPHY's low rate risk decreases portfolio risk and volatility and is, in my opinion, a net positive for investors. More dovish investors might disagree.

Low 0.05% Expense Ratio

SPHY's most important advantage to other high-yield bond funds is its low 0.05% expense ratio. Expenses are much lower than average, and are the lowest I have been able to find for a fund in this niche.

Fund Filings - Chart by Author

SPHY's below-average expenses directly increase (reduce by less) fund dividend and total returns, a straightforward benefit for investors. Importantly, lower expenses are one of the only surefire ways to increase returns. Dividends might get cut, capital gains might fail to materialize, but lower expenses always directly increase (reduce by less) total returns.

A strong actively-managed fund might generate sufficient alpha to overcome a high expense ratio, but that is almost never the case for a simple, diversified index fund. Due to this, I place great important on expense ratios when selecting index funds, and gravitate towards the cheaper ones. In this case, that means SPHY.

SPHY's below-average expenses are an important benefit for shareholders, and the fund's key advantage relative to peers.

Strong Performance Track-Record

SPHY's overall performance track-record is quite good, with the fund consistently outperforming its benchmark, and most other high-yield corporate bond ETFs. Returns were partly due to the fund's below-average expenses, but there seems to have been returns in excess of this as well.

Seeking Alpha - Table by Author

On the other hand, the fund tends to underperform relative to funds focusing on recently downgraded high-yield bonds, or fallen angels. These securities tend to see significant declines in price after their downgrades, leading to outsized returns after conditions stabilize and prices recover, or when bonds mature. I am quite bullish on these securities and funds too, and last covered them here .

As is the case for most bond funds, SPHY's long-term returns are quite low, as rates were much lower in the past. Returns for the past year, after rates stabilized at higher levels, are much higher. Returns moving forward are likely to be higher, although much will depend on future Fed rate policy. Still, conditions right now are quite positive, and conductive towards higher returns moving forward.

Seeking Alpha - Table by Author

SPHY - Recent Developments

As I've covered SPHY several times in the past, thought to have a quick look at how the fund has changed since my previous coverage.

Dividends have seen significant growth, due to a combination of higher Fed rates and widening credit spreads.

Higher dividends benefit investors. Wider credit spreads too, and are an advantage vis a vis investment-grade bonds and bond funds.

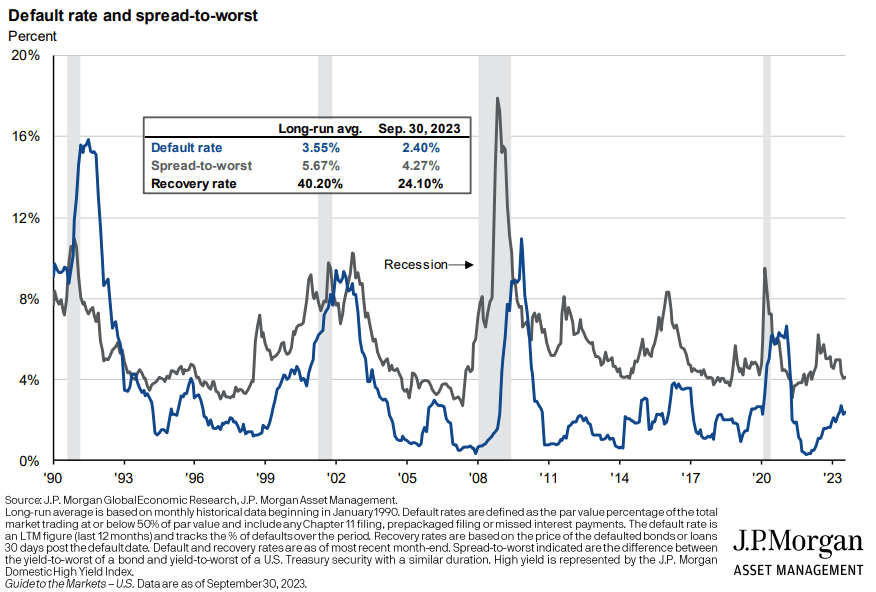

Spreads have widened as economic conditions have somewhat deteriorated, and default rates have risen. S&P expects further increases, and is forecasting a 4.25% default rate for 2Q2024 . Said figure would be above long-term historical average, but not significantly so.

{kind=link}

Higher default rates are, off course, a negative for SPHY and its investors, and more or less cancel out the positive benefits from wider credit spreads.

Finally, share prices are slightly up. I was expecting higher gains, perhaps next year.

In my opinion, fund fundamentals have very slightly improved since I last covered the fund. Higher default rates are a concern, but these remain at reasonably low levels, and are not forecasted to significantly increase.

Conclusion

SPHY offers investors diversified exposure to high-yield corporate bonds, sports a strong, growing 7.4% dividend yield, is much cheaper than average, and has outperformed most of its peers since inception. SPHY is a strong investment opportunity, and a buy.

For further details see:

3 Reasons To Invest In High-Yield Corporate Bond ETF SPHY