IYW - 3 Reasons Why We Think Apple Could Be Attractive At Current Valuations

- We expect Apple to outperform during periods characterized by low consumer confidence, due to its loyal customer base, its strong brand recognition, and its diversified product portfolio.

- With the easing of COVID-19 restrictions in China, we believe that the demand for Apple's products is likely to continue growing in the near future.

- The firm has a strong track record of paying safe and sustainable quarterly dividends in the last decade while it has also purchased back a substantial portion of its shares.

- Currently, we rate Apple as "buy."

Apple Inc. ( AAPL ) has lost about 18% of its market value year to date, in line with the decline of the broader market.

In our opinion, this pullback could be an attractive opportunity to start a new position, or add to an already existing one, as we expect Apple to outperform the broader market in the near term.

In this article, we will take a look at three reasons why we believe that Apple could be an attractive holding for many investors.

1.) Performance during times of low consumer confidence

Consumer confidence is often referred to as a leading economic indicator, and it is used to forecast potential near-term changes in the consumer spending trend. In the past months, consumer confidence in the United States has been plummeting, even falling below levels seen during the financial crisis in 2008-2009.

{kind=link}

Although consumer spending has remained strong in the first half of 2022, we expect that the low consumer confidence will have a negative impact on spending behavior in the near future.

When consumers become more and more reluctant to spend, they are likely to cut or delay their purchases on durable, discretionary, non-essential goods. Either they choose not to buy a product at all, or reduce their spending by opting for lower cost, more affordable alternatives.

Based on this description, one would expect that Apple may underperform during such periods. However, in the last 20 years, during periods characterized by low consumer confidence, Apple managed to outperform the broader market three out of three times.

2001-2003

Although both Apple and the S&P 500 ( SPY ) closed in the negative territory in this time period, Apple has lost only 4%, while the SPY has declined by more than 32%.

2007-2010

Between 2007 and 2010, Apple's share price has more than doubled, while the broader market has declined by more than 20%. Important to note that Apple's stock price was quite volatile in this period.

2011-2013

Last, but not least, from 2011 to 2013, Apple once again substantially outperformed the broader market by gaining about 65%, in contrast to the 13% increase of the SPY.

So what could be a possible reason for the firm's outperformance?

We believe that there are two key reasons: customer loyalty combined with strong brand recognition, and a diverse product portfolio.

a) Loyalty and brand recognition

Over the years, Apple has managed to build up an unparalleled customer loyalty and brand recognition. With constant innovation and product improvement, the company has been able to retain existing customers and attract new ones, leading to a substantial increase for their products.

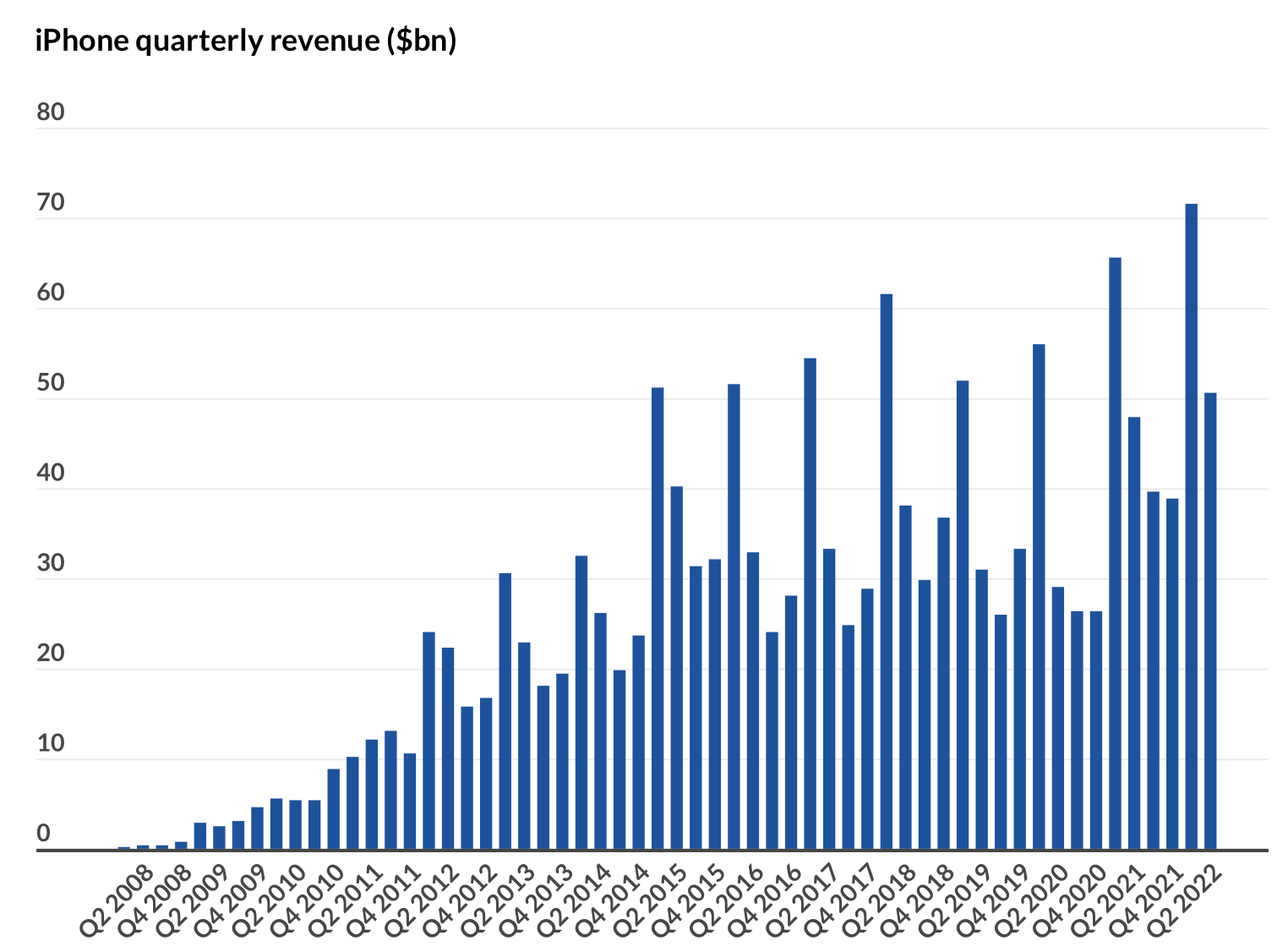

To illustrate our example, let us take a look at the quarterly iPhone revenue figures.

{kind=link}

As iPhone sales contribute about 50% to Apple's total revenue, we believe looking at this product segment is representative.

Between 2008-2015, sales have grown at an extreme pace. The growth has slowed down however in 2015, due to increasing competition from Chinese manufacturers, including Huawei and Xiaomi. On the other hand, in 2021 and 2022, sales figures started to increase again. In our opinion, the easing of COVID-19 restriction in China and the easing of chip shortage will likely support this growth trend in the near future.

Despite the competition, we believe that existing Apple customers are reluctant to change to other brands, especially if they have multiple products from Apple.

Loyalty and brand recognition do not only mean retaining customers, but it also gives the firm a certain pricing power. Having a strong pricing power in the current inflationary environment can be valuable, as the firm may potentially be able to pass on the elevated costs of production and transport to their customers.

b) Diverse product portfolio

In our opinion, the diverse product portfolio has several advantages. First of all, many of the products are in different price categories, catering for different customers with different financial backgrounds. People, who want to buy, for example, more sophisticated smartphones or laptops can do so for a higher price. On the other hand, people, who are less confident about their financial outlook and are reluctant to spend large sums on discretionary products, are likely to choose the more affordable items.

The diversified product portfolio also allows for the creation of a well-functioning ecosystem. Using multiple Apple products together, including the iPhone, MacBook, AirPods, Apple TV, etc. could be substantially more convenient than using different gadgets from different manufacturers. This well-functioning ecosystem can also increase customer retention even further.

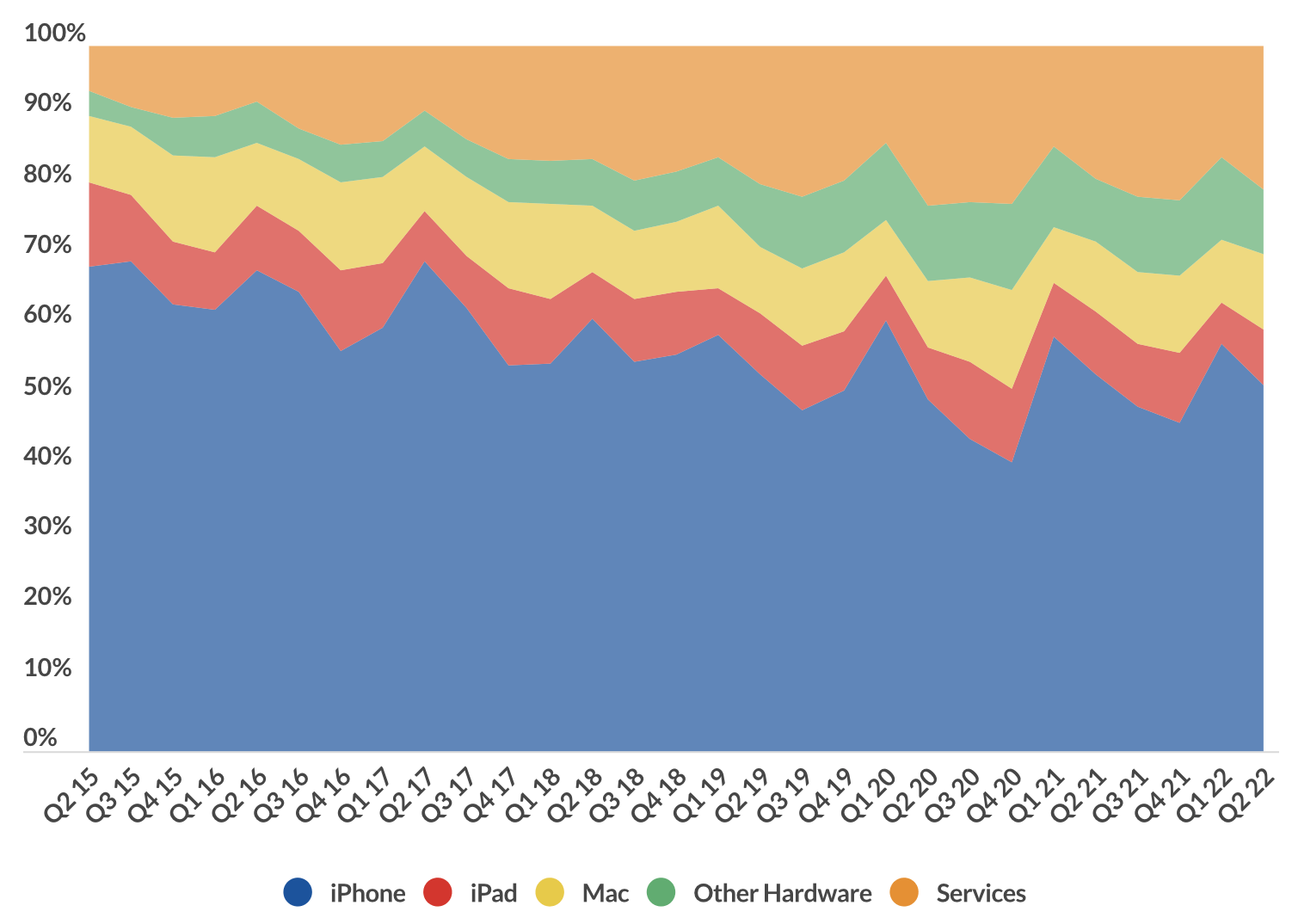

Last, but not least, we have to mention services.

Although services are not yet a substantial part of Apple's revenue, this segment has been consistently growing over the past years.

{kind=link}

Services, like Apple TV and Apple Music subscription, create reoccurring revenue for the firm. This could be especially advantageous during times of low consumer confidence. Services are usually the last to be influenced by spending cuts.

In the past periods that we have looked at, services was actually a negligible part of the revenue. However, in the current market environment, we expect that services could put the firm in an attractive position to outperform the broader market once again.

2.) Share buybacks

Apple has a strong track record of returning value to its shareholders through share buyback programs.

{kind=link}

During the last decade, the firm has reduced its number of shares outstanding significantly, by as much as 38%.

Further, we expect the firm to continue with this trend. In April this year, the firm announced that they are planning to add another $90 billion to their stock buyback program.

Capital gains and share buyback programs are not the only way AAPL is generating value for the shareholders. They also have a relatively long history of dividend payments.

3.) Dividend payments

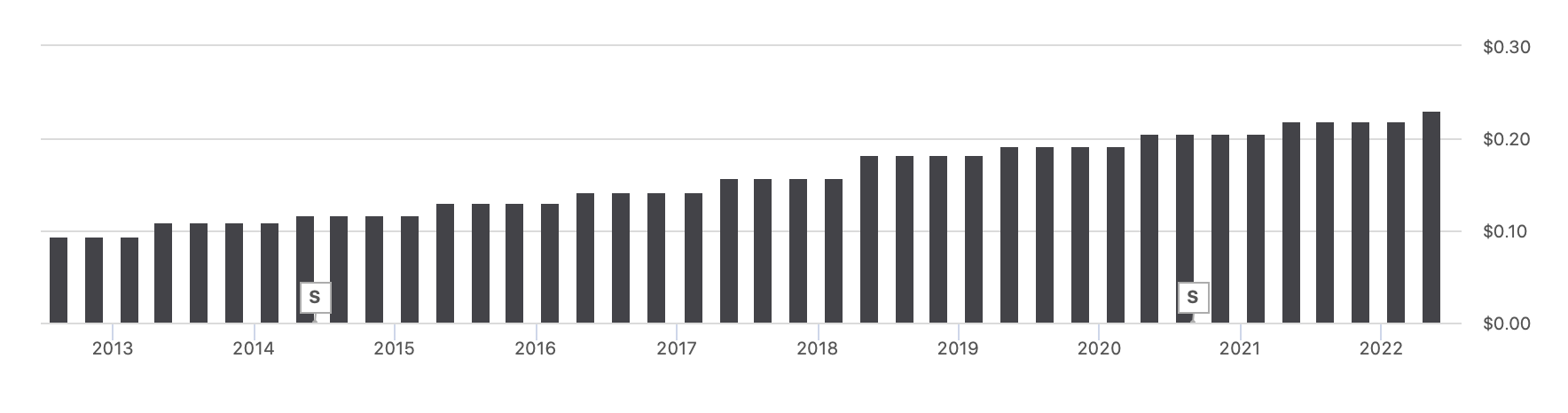

Apple has been paying quarterly dividends to its shareholders since 2013.

{kind=link}

In this time frame, they have been paying each quarter consecutively, even during the 2020 COVID-19 pandemic. Also, important to note that they have managed to increase the dividend payments each year.

Currently, the firm pays $0.23 quarterly dividend per share, which corresponds to a 0.63% annual yield. Although the yield does not appear to be exceptional, for dividend and dividend growth investors, not only the yield matters but also the safety and the sustainability of the dividend payments.

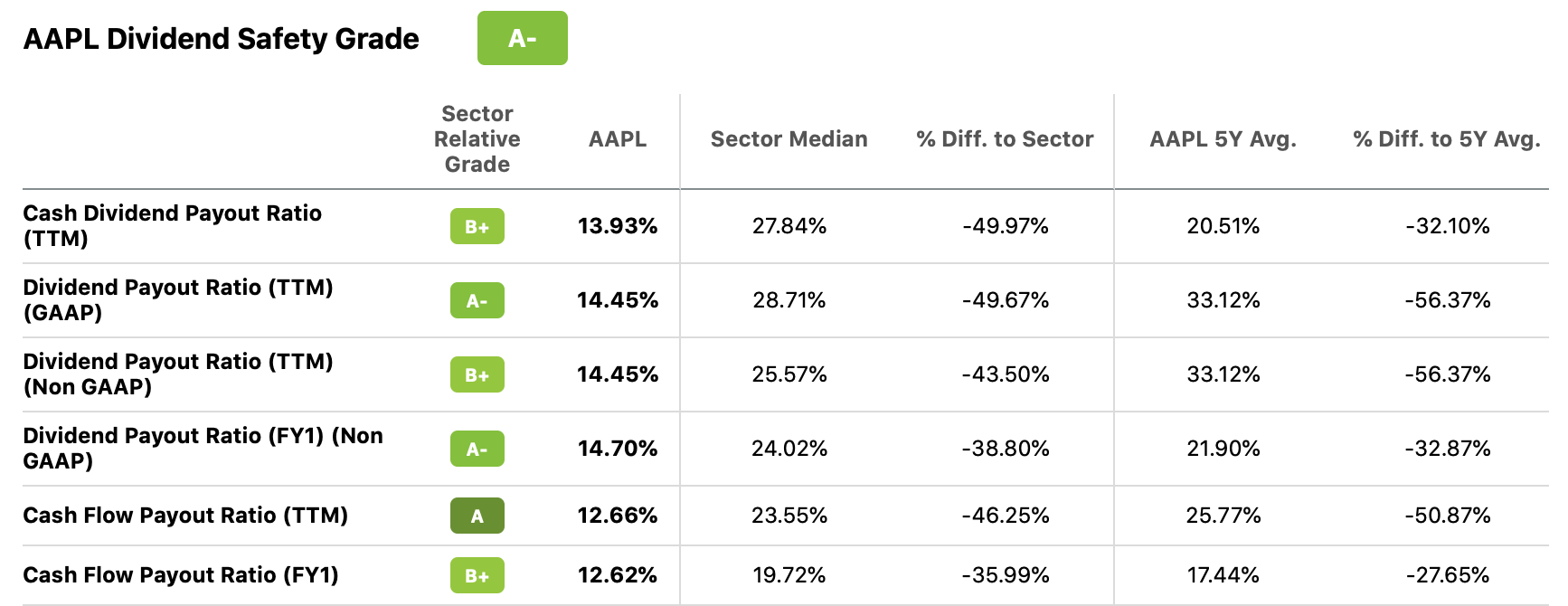

The firm has a great dividend safety grade of "A-." The firm's dividend payout ratio appears to be sustainable as it is less than 15% across all metrics. Further, these figures compare favorably with the consumer discretionary sector medians.

{kind=link}

Going forward, we believe that Apple's dividend is likely to remain safe and sustainable.

Key takeaways

Apple has a strong track record of outperforming the broader market in times of low consumer confidence. We believe that, in the current market environment, Apple is once again positioned well due to its diverse product portfolio and strong brand loyalty, despite the increasing competition.

The firm has been generating and returning value to its shareholders both in forms of dividends and through share buyback programs over the years.

Despite the headwinds, including the COVID-19 related restriction in China and the chip shortages, we currently rate Apple as "buy."

For further details see:

3 Reasons Why We Think Apple Could Be Attractive At Current Valuations