VNQ - 3 REIT Stocks That Pay Monthly Dividends

2023-10-26 08:05:00 ET

Summary

- There are several REITs that pay monthly dividends.

- And since REITs are on sale, quite a few now offer high dividend yields.

- I highlight three of my favorite monthly-paying REITs to buy today.

Most dividend-paying stocks ( SCHD ) make quarterly dividend payments.

But real estate investment trusts, or REITs ( VNQ ), are a bit different.

Quite a few of them pay on a monthly basis just as if you were a landlord collecting rent checks, month after month.

This is very attractive even if you don't need the income because it gives you a steady flow of liquidity, which then allows you to buy more shares. It also helps to stay patient during times like today when the market is very volatile.

But what are the best monthly-paying REITs to buy today?

In what follows, we will highlight 3 of our Top Picks that we are today accumulating:

Monthly-Paying REIT #1:

BSR REIT (HOM.UN:CA / BSRTF ) is one of a few apartment REITs that pay monthly dividends.

We think that it is one of the best opportunities in the REIT world right now because it owns very desirable assets in rapidly growing Texan markets, but it is priced at a huge 45% discount to its net asset value.

Its current share price is $11, but its latest net asset value estimate is $20.50.

So put simply, this is an opportunity to invest in Texan apartment communities at just 60 cents on the dollar.

BSR REIT

Why is it so cheap?

Is it overleveraged? No, it is not. The company has a conservative LTV of just around 40%.

Is the management conflicted? Again, no. The founders of the company are still its biggest shareholders and the management is making regular purchases in the open market and buying back stock at these levels.

Is the NAV estimate inflated and unrealistic? We don't think so. It is based on a 4.7% cap rate, but keep in mind that its current leases include an 8% mark-to-market so the forward normalized cap rate is closer to 5%. That's just about right for fairly new apartment communities in the Texan Triangle. Another REIT called UDR, Inc. ( UDR ) just recently acquired a similar portfolio at a 4.5% cap rate. Cap rates could expand a bit if we remain in a "higher-for-longer" interest rate environment, but rents would also rise a lot in that scenario since home ownership would remain unaffordable.

In any case, BSR is today priced at an implied cap rate of nearly 7% so there is a significant margin of safety even if cap rates expand a bit.

I think that this huge discount on quality assets is the #1 reason to buy the stock.

But another reason is the monthly dividend payment. Today, it yields 4.5%, which may not seem high, but keep in mind that this is because they retain 40% of their cash flow to buy back stock. Also, something attractive about this dividend is that it is today classified as "return of capital," which means that it should be tax-deferred.

A tax-advantaged 4.5% is the equivalent of a ~6% yield that would be taxed.

Again, that's very compelling coming from a REIT that owns such desirable growth assets and retains so much cash flow for buybacks.

{kind=link}

I believe the company's NAV will likely stabilize around $18 once cap rates are done expanding, which means that the stock has about 60% upside potential from here. While you wait, the monthly dividend payments will help you stay patient.

Monthly-Paying REIT #2:

If a 4.5% yield isn't enough for you, then consider Agree Realty ( ADC ), which is today priced at a 5.5% dividend yield, the highest level in a very long time for this monthly-paying REIT:

ADC is typically priced at closer to a ~4% yield, but it is now offered at 5.5% because its share price has crashed over the past year even as it kept hiking its dividend.

This crash appears to be the result of rising interest rates and fears of a recession.

But these fears appear to be way overblown in the case of ADC.

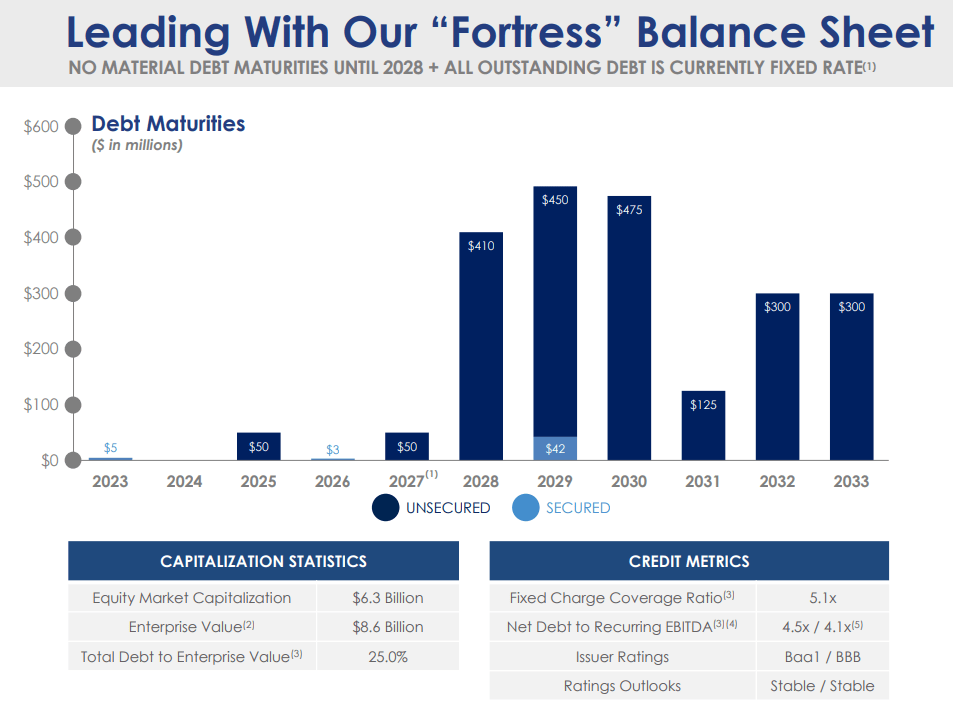

First off, its balance sheet is one of the strongest in the entire REIT world with a low LTV of 25% and no debt maturities until 2018:

{kind=link}

This means that it won't suffer any impact for the next 5 years. By then, interest rates will likely have dropped to much lower levels, but even if they haven't, ADC's leverage will be even lower by then as it keeps growing its cash flow and uses its retained income to pay off debt.

The impact is really not significant.

What about a recession?

Again, the market appears to strongly underestimate ADC here. Triple net lease properties are recession-resistant real estate investments because:

- They enjoy 10+ year-long lease terms.

- The rents are pre-set with automatic rent hikes for the entire duration.

- Rent coverage ratios are typically >3x, meaning that the tenant's profitability would need to drop by 2/3 before they potentially miss rent payments.

- These are typically service-oriented properties such as grocery stores, gas stations, and fast food restaurants, which don't suffer much in recessions.

- Finally, the assets are the tenant's profit center and so they are highly dependent on them. They don't want to lose their assets because of 1-2 years of lower profitability.

Agree Realty

This explains why the cash flows of net lease properties typically keep on growing steadily even during recessions. You don't believe me?

Just consider that NNN REIT ( NNN ) and Realty Income ( O ) have grown their dividends for decades in a row by investing in net lease properties:

Realty Income

ADC actually owns even safer assets than NNN and O. You can see that in their much higher exposure to investment-grade rated tenants:

| ADC |

| O |

| NNN |

| Investment Grade Tenants |

| 68% |

| 40% |

| N/A |

So again, the fears of a recession appear to be way overblown.

But this has resulted in a rare opportunity to buy ADC at just 13.5x FFO and a high 5.5% dividend yield, which is paid on a monthly basis.

Just like BSR, ADC also retains a lot of cash flow with a low 70% payout ratio, which allows it to keep reinvesting in new properties to keep growing its dividend.

We estimate the fair value at closer to 18x FFO, which would unlock about 30% upside from today's level. Note that 18x FFO is fairly conservative as it is quite a bit lower than the multiple at which it traded in recent years.

While you wait, you earn a 5.5% dividend yield that's set for ~5% annual growth over the long run. That alone should get you to >10% annual returns even ignoring any repricing upside.

Monthly-Paying REIT #3:

Finally, if ADC's 5.5% yield isn't enough, then I have one final REIT for you to consider.

EPR Properties ( EPR ) is one of the highest-yielding monthly-paying REITs in my portfolio. It is today priced at an 8% dividend yield and that's despite having a low 70% payout ratio and having guided for 9% FFO per share growth in 2023.

Why is it priced at such a low valuation and high yield if it is able to grow at such a rapid pace?

In one word: theaters.

EPR Properties

EPR is a net lease REIT that specializes in experiential properties such as ski resorts, golf complexes, water parks, and movie theaters.

Today, about 1/4 of its portfolio (as measured by NAV) is invested in movie theaters and this is causing the market to worry.

The other 3/4 is performing exceptionally well in the post-pandemic world as people want to go and have fun. Rent coverage ratios now even exceed pre-pandemic levels.

But the movie theaters are a cause for concern for many.

I believe that the fears are overblown and here's why:

- EPR is the triple net lease landlord that earns pre-determined rent checks from 10+ year leases. It is not the operator of the theaters.

- Today, the rent coverage of these properties is positive, meaning that they are profitable at the property level.

- The rent coverage will likely only keep increasing as the box office continues its recovery following the huge successes of Barbie and Oppenheimer.

- EPR owns some of the highest-quality theaters in the nation. Those are here to stay and benefit as lower-quality theaters close down since it leads to traffic consolidation.

- EPR already renegotiated its lease with AMC Entertainment Holdings ( AMC ) during the pandemic and Regal's recent bankruptcy resulted in rent hikes (not cuts!) across most of its properties.

Finally, the pandemic proved to the market that movie theaters remain needed to monetize new blockbusters. Streaming and other digital strategies are not a replacement because people don't pay as much to watch at home. At best, one person pays and the rest of the family and friends watch for free, and it also leads to immediate pirating and significant lost revenue.

Besides, studies show that people mostly stream shows, not movies, and those people who stream the most are more likely to visit theaters for movies. So Netflix ( NFLX ) sure isn't replacing theaters. The box office was hitting all-time highs in 2019 and that's despite most people already having at least one streaming service at their disposal. Major studios like Disney ( DIS ) and Warner Bros. ( WBD ) have now all returned to theaters after having experimented with digital strategies during the pandemic. Even Amazon ( AMZN ) and Apple ( AAPL ) have announced that they will spend billions producing movies for theaters.

{kind=link}

So while EPR has risks, I believe that the risks are misunderstood, and it is causing its share price to be overly discounted.

Priced at just 8x FFO, the shares could return 50% if they simply returned to 12x, which would still represent a huge discount relative to most REITs. While you wait, you earn an 8% monthly dividend and the company's cash flow keeps growing at a good pace.

Here is what the management said on a recent conference call (emphasis added):

"Given these improvements in credit, the continued success of our non-cinema portfolio and the demonstrated consumer preference for out-of-home entertainment, we continue to believe that EPR offers a very attractive value for investors with a well-covered dividend and an opportunity for multiple expansion. "

Bottom Line

Earning steady monthly dividend income is my best-kept secret during times of market volatility.

It gives me peace of mind and allows me to make steady additions to my portfolio when valuations become heavily discounted.

Today, REITs are offering the best opportunities in a decade and I am pushing all my dividend income towards them.

My passive income streams are growing rapidly, and I also expect significant upside in the coming years as REITs recover.

For further details see:

3 REIT Stocks That Pay Monthly Dividends