VICI - 3 REITs For A Higher For Longer Scenario

2023-09-15 07:00:00 ET

Summary

- Recent CPI numbers missed expectations, and inflation is starting to run hot again.

- With mixed signals, it's unclear what the Fed will do, and investors should protect themselves against a higher for longer scenario.

- I highlight 3 REITs that are well-positioned to maintain and even grow their dividends even if rates remain elevated for years.

Dear readers,

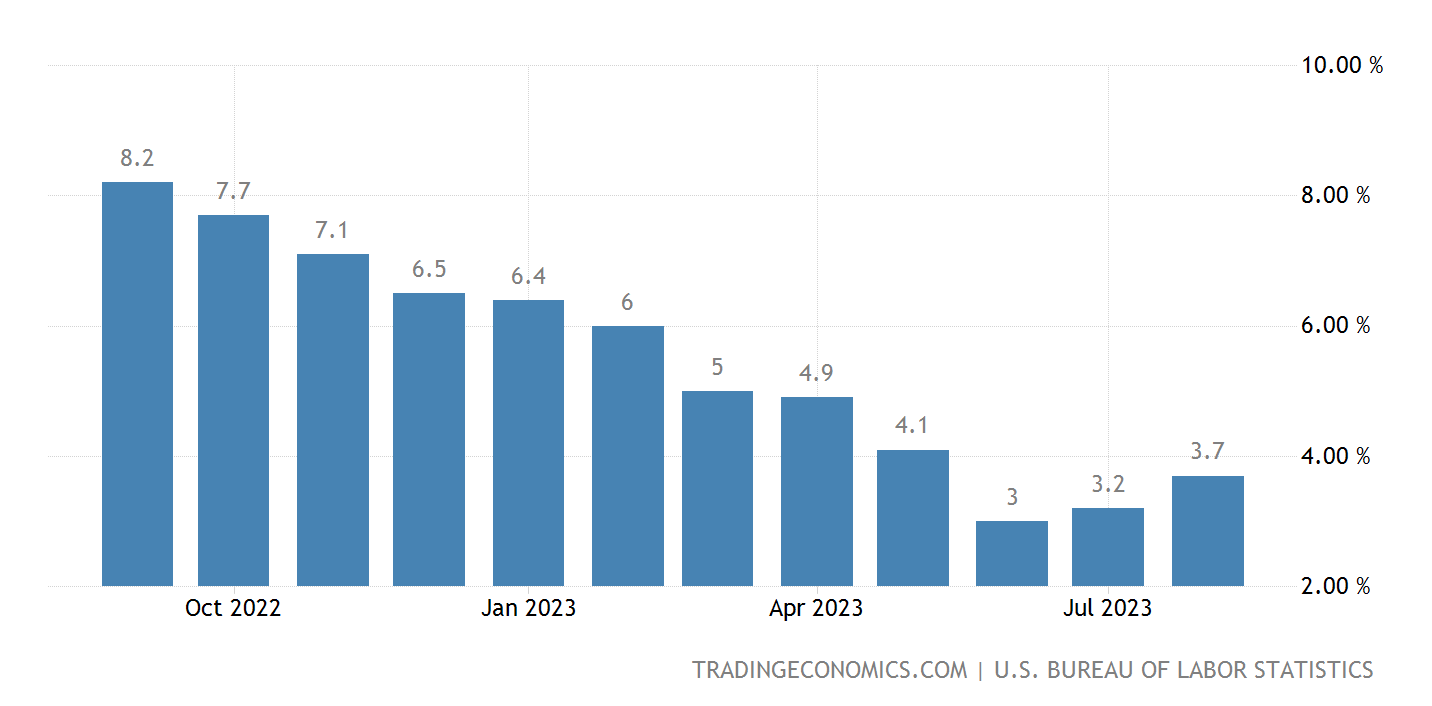

Yesterday's CPI numbers came in a bit higher than expected with headline CPI at 3.7% YoY and core CPI at 4.3%.

We've known for while that both metrics continue to be inflated by shelter CPI which was most recently reported at 7.3% YoY, despite real time data showing no real inflation for housing. So the expectation has been that as we work through the lag in shelter, which accounts for about a third of CPI, the headline number will trend lower.

Recently, however, energy has also got hot, increasing by 5.6% during the month of August alone. The increase was led by a 10.6% month-over-month increase in gasoline prices. In the meantime, oil has reached $90 per barrel and remains in a steep bull-trend which could easily result in further upwards price pressure on gas in future months.

The market doesn't like it when expectations get missed and might be getting worried about the second wave of energy price increase. Also, the fact that inflation has now broken a clear downtrend which it has been on since last fall clearly shows, that a soft-landing is far from guaranteed.

Trading economics, U.S. Bureau of Labor Statistics

{kind=link}

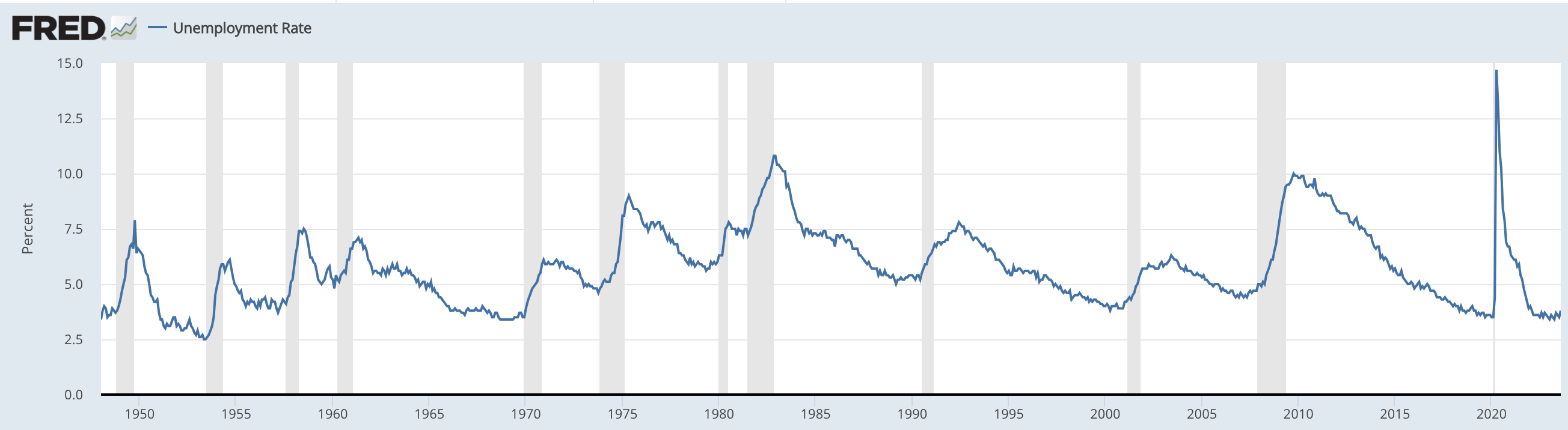

The Federal Reserve's mandate is maximum employment and price stability. And as the labor market remains very strong and unemployment historically low at just 3.8% , the Fed can (and has to) focus on achieving price stability.

{kind=link}

As a result, the bond market has already started to price in another rate hike in November. In particularly, the implied probability of a 25 bps hike to 5.5-5.75% now stands at 42%.

{kind=link}

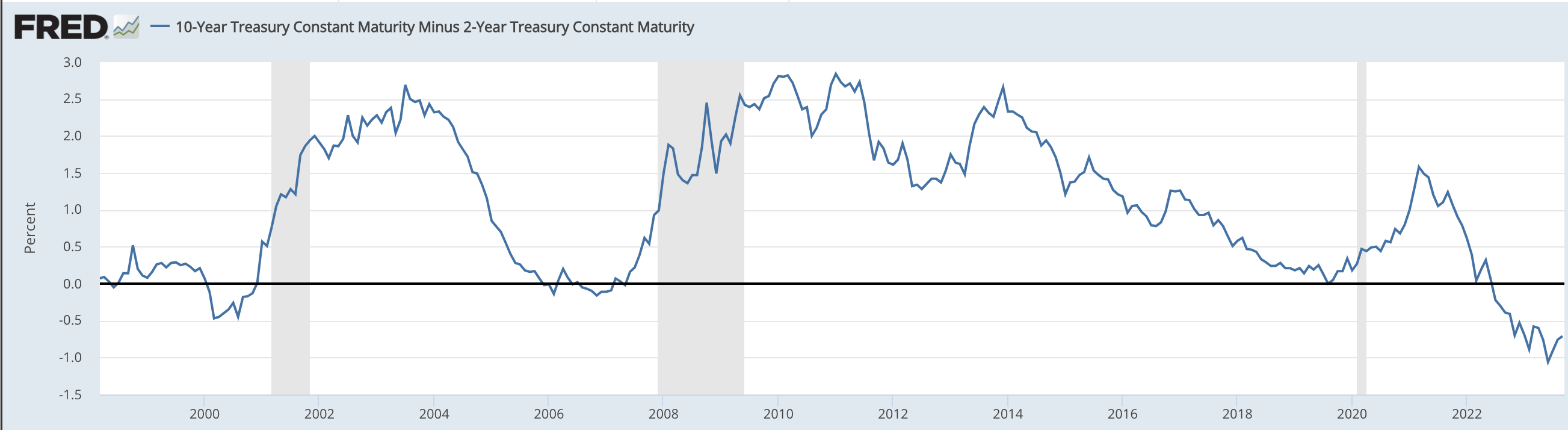

At the same time, the yield curve remains deeply inverted, pointing to a potential recession, which has historically always led to the Fed cutting rates. But the thing is that the rate cuts, always followed a steep increase in unemployment, which we don't have now. As long as unemployment stays low, the Fed has no reason to back away from their fight against inflation.

{kind=link}

The situation is complicated and historically, most have failed to predict the course of interest rates. That's why as investors, we should position ourselves in a way that is not dependent on a particular macro thesis playing-out.

A higher for longer scenario, implicitly assumes high inflation, high interest rates and low employment (i.e. not a severe recession, but a mild one at most).

Consequently, for a REIT to be well positioned for this scenario, it needs to be able to raise rents in a high inflation environment and its balance sheet needs to withstand several years of high rates, without significant increases in interest expense. This way the REIT can maintain its cash flow and dividend.

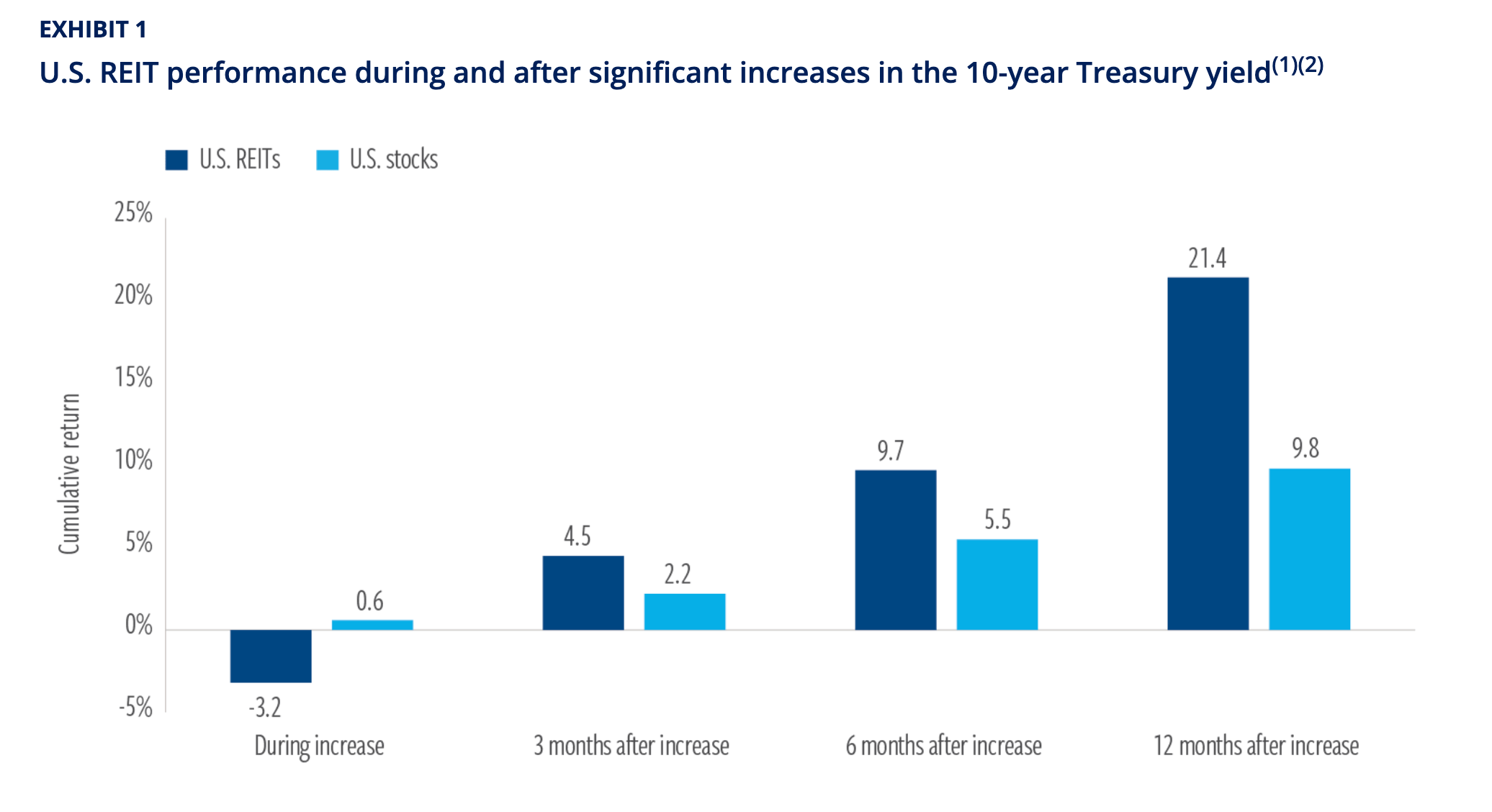

If you think that it's best to avoid REIT in this environment altogether, I urge to have a loot at a study which found that rising rents matter more than high interest rates and that REITs tend to outperform after interest rates stabilize, regardless what level they stabilize at.

{kind=link}

Today I present 3 REITs For A Higher For Longer Scenario .

Agree Realty Corporation ( ADC )

First on the list we have Agree Realty which focuses on single-tenant, net lease big box stores leased to the likes of Walmart ( WMT ) or Home Depot ( HD )

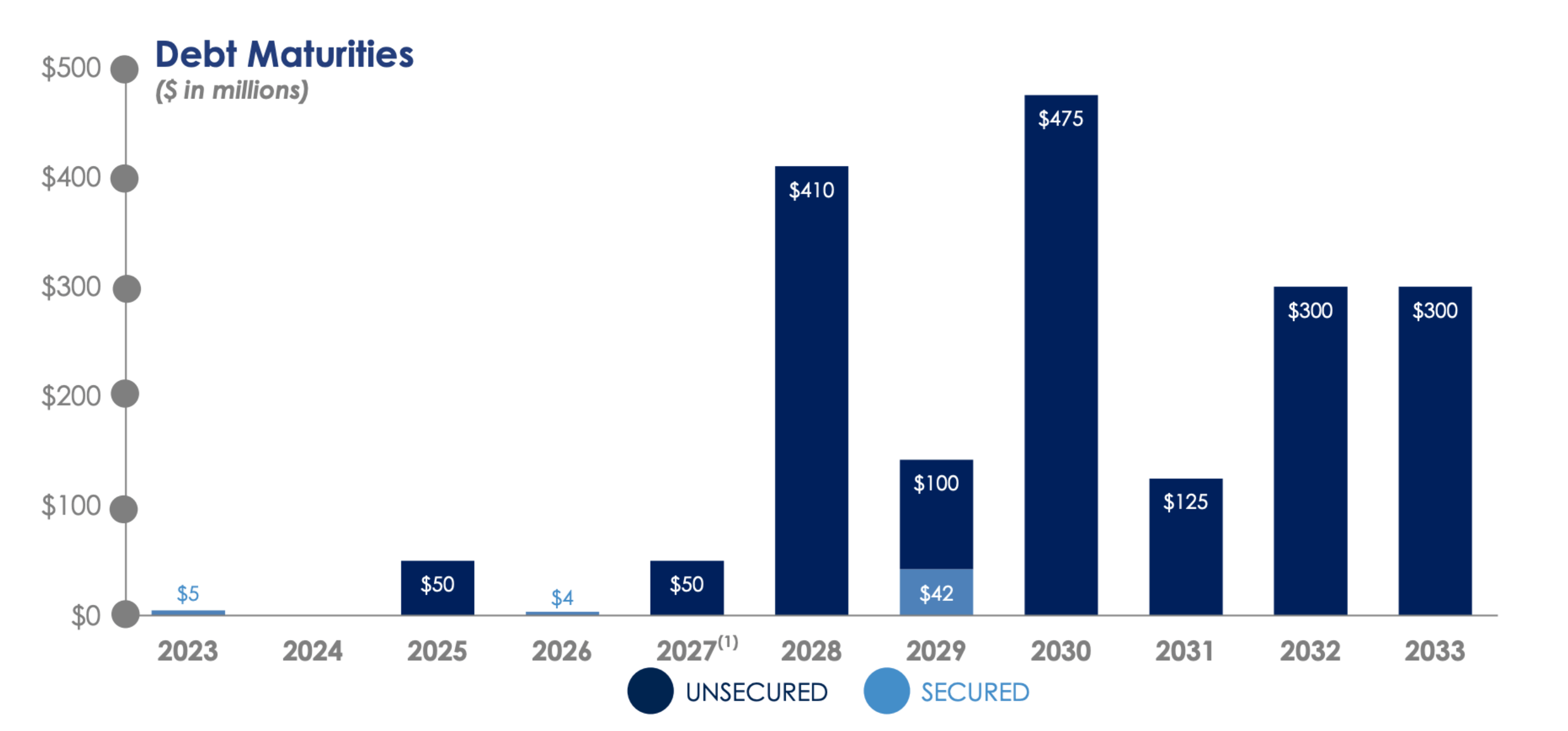

For ADC, it's all about the balance sheet, which has no material debt maturities until 2028 and 90%+ of their debt is fixed-rate.

What this means is that even if interest rates stay elevated for years to come, their interest expense will not materially increase.

{kind=link}

Stable interest expense will enable the REIT to grow their cash flow despite relatively low build-in rent escalators of around 1.5% (lower contractual rent increases result from their focus on established tenants with lots of bargaining power).

As a result, cash flow should be fairly stable even under the higher for longer scenario. And with the payout ratio currently at 73% which is below the low-end of management's target of 75-85%, there may even be room for dividend growth beyond the current yield of 4.9%.

VICI Properties ( VICI )

VICI, being a casino REIT, takes a different approach and focuses more on the ability to raise rents in a high inflation environment.

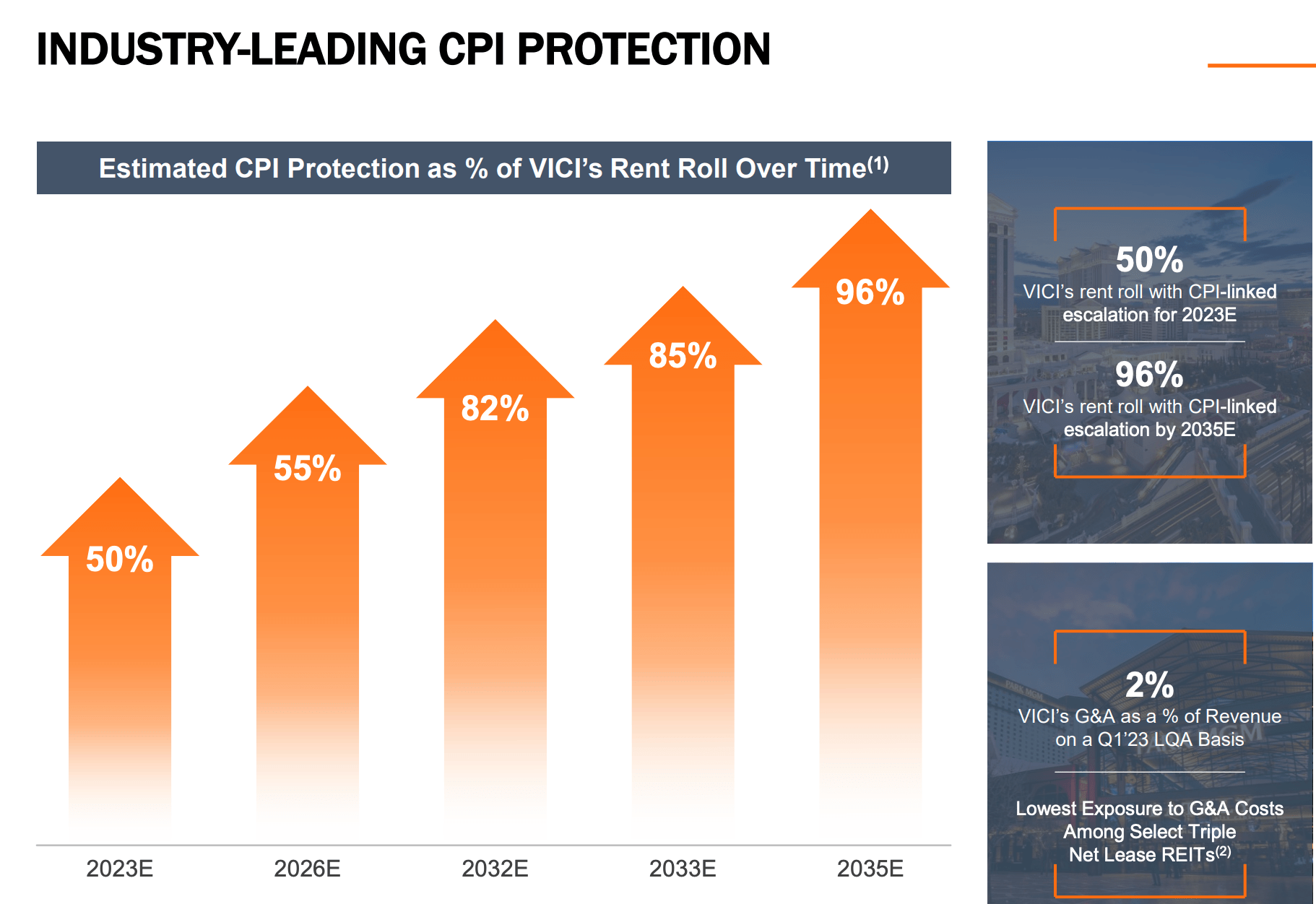

The REIT has some of the best lease terms in the sector with 76% of rent coming from S&P 500 tenants, an extremely long average lease terms of 42 years and most importantly industry-leading CPI protection.

VICI states in their presentation that 50% of lease are currently CPI-linked and by 2035, this proportion will rise to 96%.

{kind=link}

I find this slightly misleading, because while the leases are indeed CPI-linked, a lot of them have caps at 3%, which really doesn't count as full inflation protection, especially under a higher for longer scenario.

I've gone through the leases and the bottom line is that their portfolio averages a minimum 1.9% annual rent increase and 43% of leases are CPI-linked with no caps.

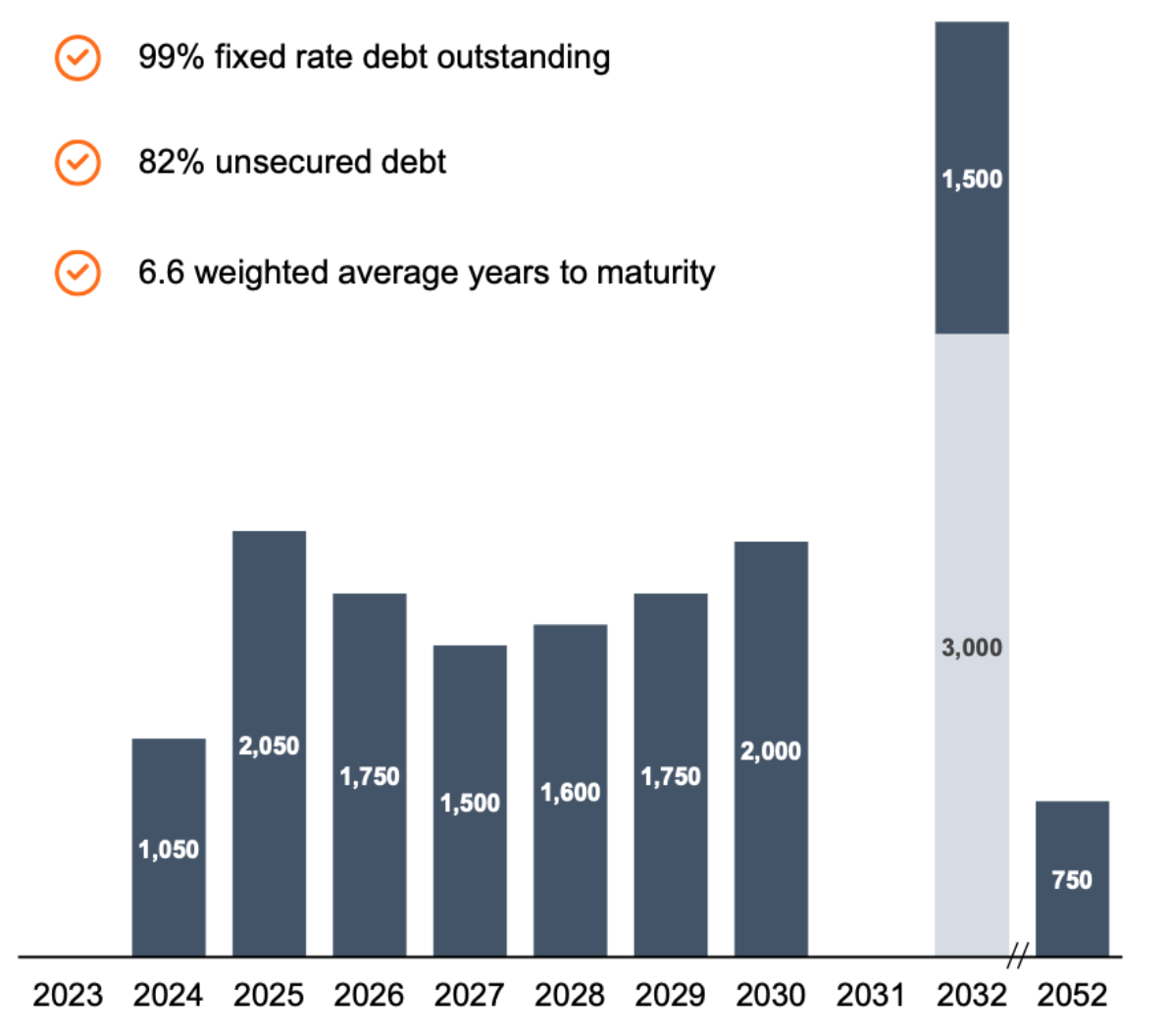

That's really solid inflation protection, especially when combined with a strong balance sheet which has 99% of debt fixed-rate and a relatively long average duration of 6.6 years, which means that near-term maturities (say 2024 and 2025) are relatively low.

{kind=link}

Even-though VICI's interest expense would increase in a higher for longer scenario when it refinances their debt due in 2024 and 2025, I estimate that this increase would be offset by higher rents, resulting in stable cash flow.

With a healthy payout ratio of 75%, this means that the 5.3% dividend yield should be safe even in interest rates stay elevated.

Alexandria Real Estate Equities ( ARE )

Last, but certainly not least, we have ARE which combines the best of both worlds - an ability to raise rents and a balance sheet with low interest rate risk, making it an ideal candidate for a higher for longer scenario.

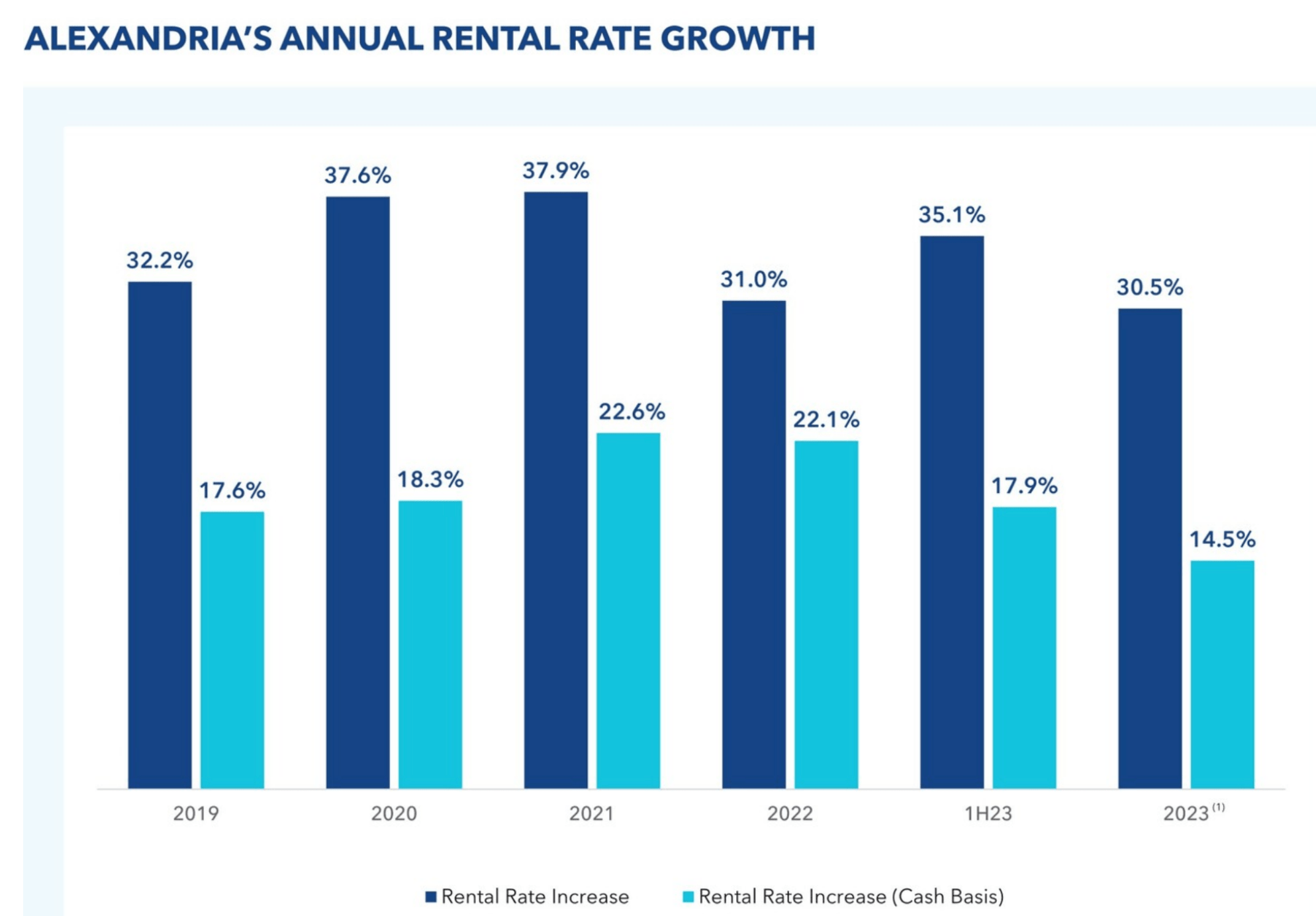

The REIT has high build-in rent escalators that average 3% and on top of that has been able to significantly raise rents on renewals/new leases. And I mean significantly, with rent spreads of >30% and 15-20% on a cash basis.

{kind=link}

With about 9% of leases expiring in each of 2024 and 2025, it's likely that rent spreads on new leases alone will generate 2.5-3% growth on a portfolio level. Add to this the 3% rent escalators and internal growth is "locked-in" at 6% per year.

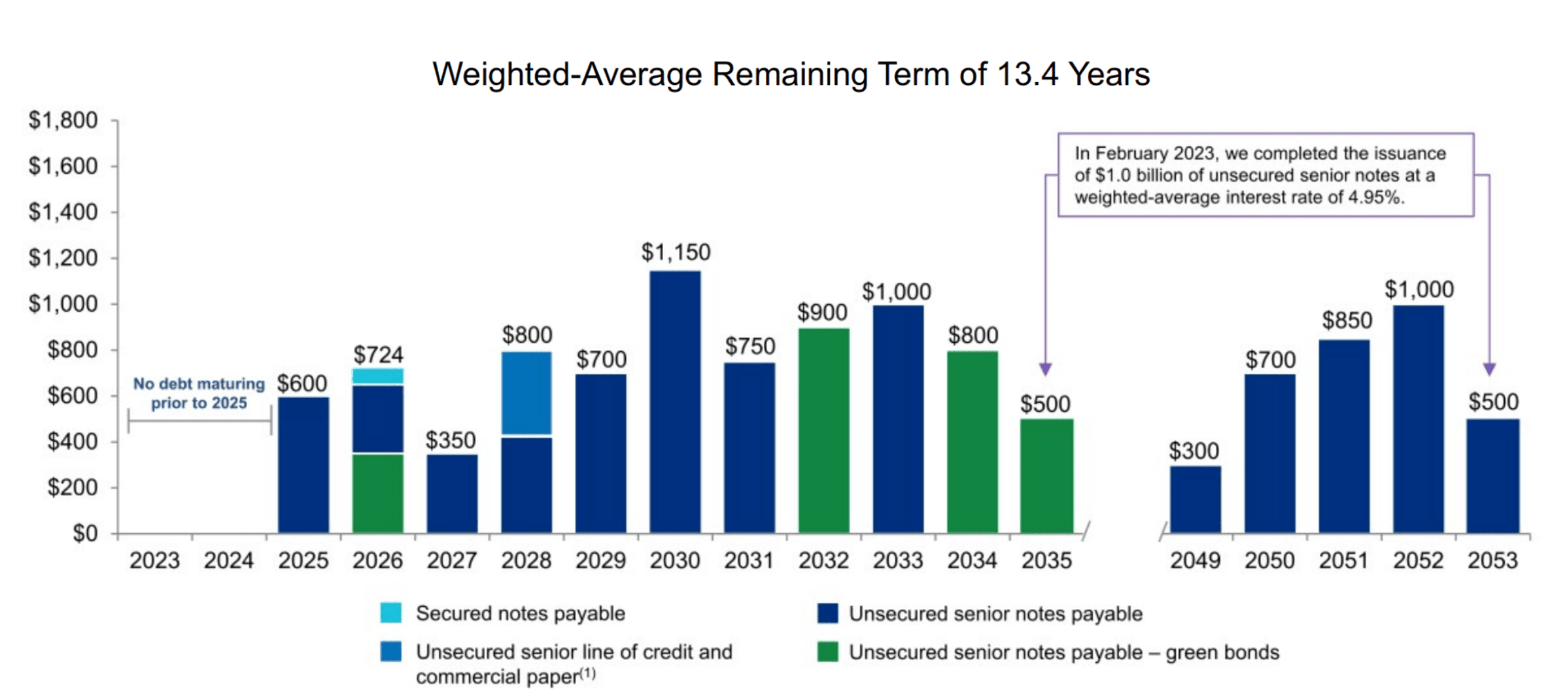

Additionally, ARE has a strong balance with very low interest rate risk. Maturities are well spread out, with a long average remaining term of 13.4 years and 96% of debt fixed-rate.

Once again, I estimate that while the interest expense will increase when the REIT refinances their $600 Million debt maturity in 2025, the increase will be more than offset by rent increases which will have really added up by then at 6% annual growth.

{kind=link}

As a result, I think ARE is extremely well positioned to grow its cash and therefore increase its now 4.4% dividend yield, no matter how long interest rates remain high.

For further details see:

3 REITs For A Higher For Longer Scenario