VNQ - 3 REITs That Should Suffer In Higher For Longer

2023-11-07 08:05:00 ET

Summary

- Interest rates have surged like rarely before.

- Some REITs will be fine, but others could face significant pain.

- We discuss three REITs that could suffer a lot.

Co-produced by David Ksir.

Our expectation remains that interest rates will decline at some point over the next 12-24 months and this should lead to substantial upside for most real estate investment trust, or REITs ( VNQ ).

But we recognize that predicting the exact course of interest rates is impossible, as is timing the bottom in the market. As a result, we find it useful to think in terms of scenarios and invest accordingly so that you don't rely on a single macroeconomic catalyst playing out.

Not all REITs are created equal, and while most of them should be fine even in a higher for longer environment, some others could suffer significantly in that scenario. So, today we look at three such examples:

Granite Point Mortgage Trust Inc. ( GPMT )

Granite Point is a mortgage REIT with a $3 Billion loan book that's invested primarily in office (42%) and multifamily loans (31%).

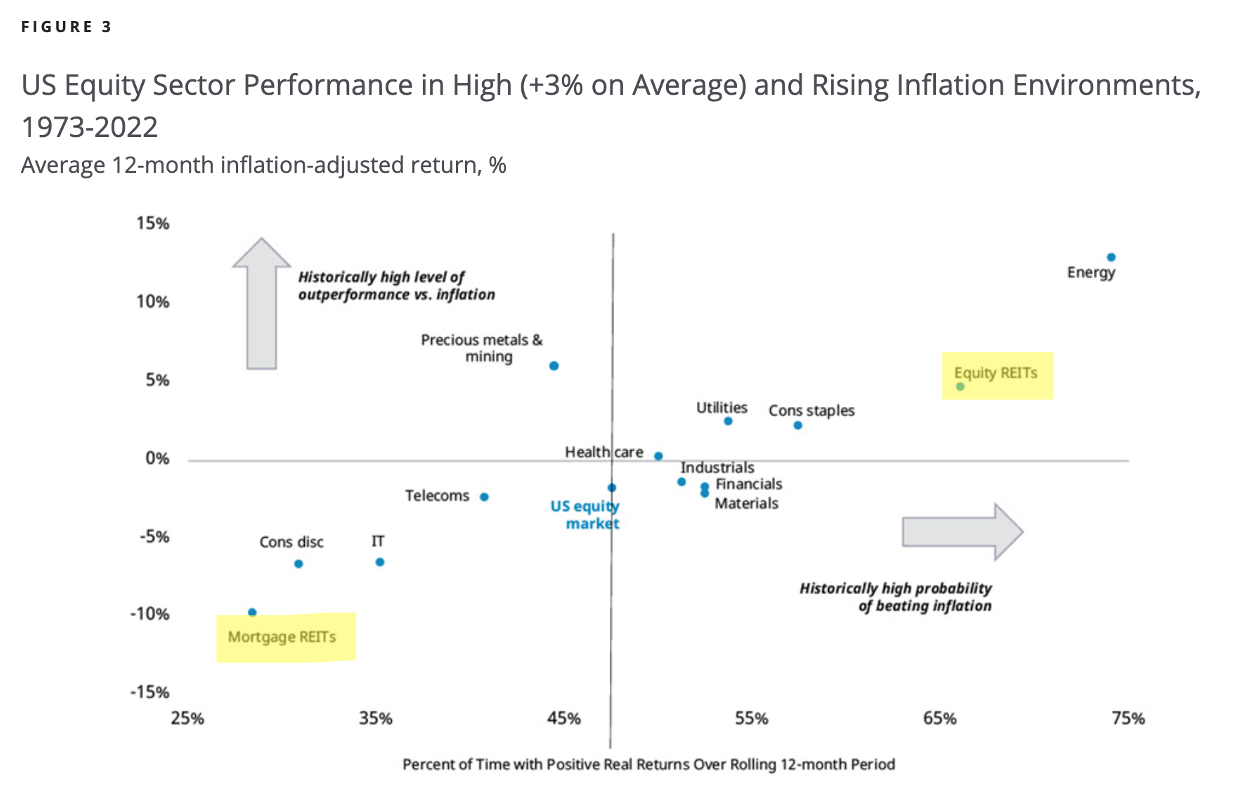

I'll get into this mREIT's specifics in a minute, but first I want to show you, how badly mortgage REITs tend to perform in a high (3%+) inflation environment.

In fact, mREITs are the worst performers of all sectors and have only a 27% chance of beating inflation, with an average 12-month return of -10%.

Equity REITs, on the other hand, have a much better track record due to their ability to raise rents:

{kind=link}

At first glance, GPMT's floating rate loan portfolio actually benefits from higher interest rates because the mREIT gets to charge its borrowers higher interest. But the problem is that many of these borrowers are distressed office properties with low occupancy that simply aren't able to (or in some cases may choose not to) make the payments.

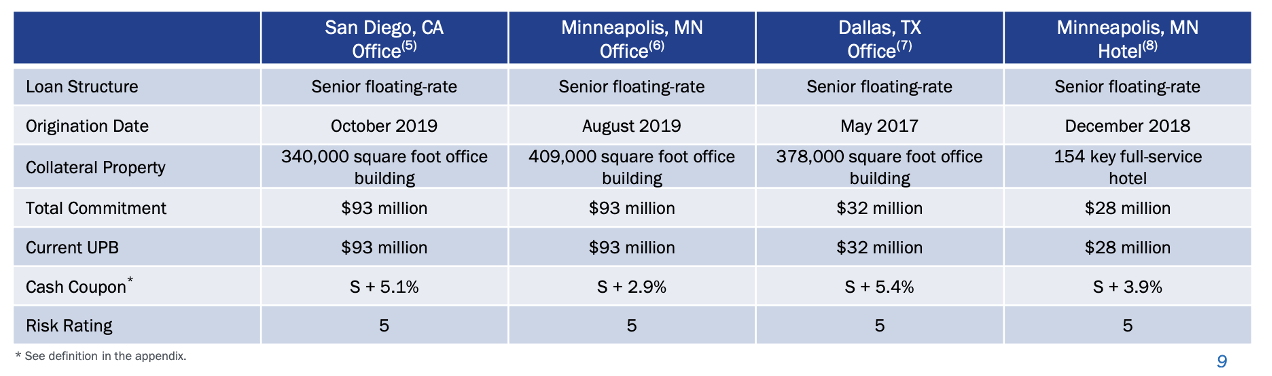

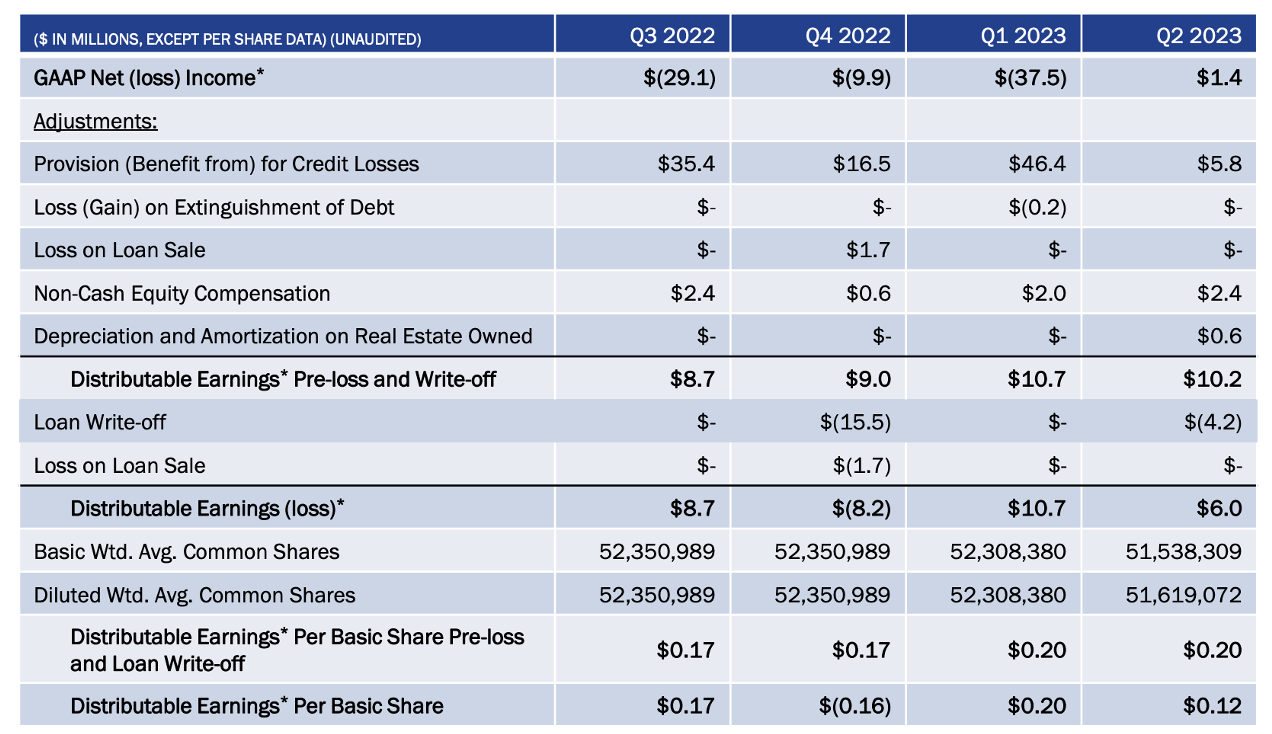

Granite Point already had to deal with a default on a $114 Million loan in Q4 2022, which resulted in a $15.5 million write-off. More recently, in Q2 2023, another $29 Million loan went into foreclosure and resulted in an immediate write-off of $4.2 Million.

Currently, there are four 5-rated loans (on the verge of default) worth a total of $246 Million. My worry is that if interest rates stay high for just a couple more quarters, more office loans will default, resulting in further losses.

{kind=link}

Management has been increasing its CECL reserve in anticipation of these defaults, but the problem is that the mREIT doesn't even make enough to cover its dividend.

Over the past 12 months, Granite Point has made an average of ~$0.15 per quarter, while paying out a $0.20 quarterly dividend. That is hardly sustainable and mind you distributable earnings are before the provisions for credit losses (i.e., the increase in the CECL reserve). So not only is the payout ratio too high, but it doesn't even account for the fact that further defaults and losses could likely happen in the near future.

{kind=link}

To be fair, Granite Pointe is not the only one. There are many other mortgage REITs that share similar characteristics. But the fact of the matter is that as long as interest rates stay high, distressed borrowers will be under immense pressure and some will likely default, leading to even lower distributable earnings and eventually a dividend cut. That is not something I want to participate in.

Brandywine Realty Trust ( BDN )

BDN is a small office REIT with 80% of its portfolio located in and around Philadelphia. Its share price has declined meaningfully over the past two years and the REIT now trades near its all-time low valuation and pays a 16% dividend yield.

Brandywine is cheap by any metric, but that doesn't make it an automatic buy.

The problem is that it's very poorly positioned for a prolonged period of high interest rates.

Here are two reasons why:

Reason #1 - poor tenant mix

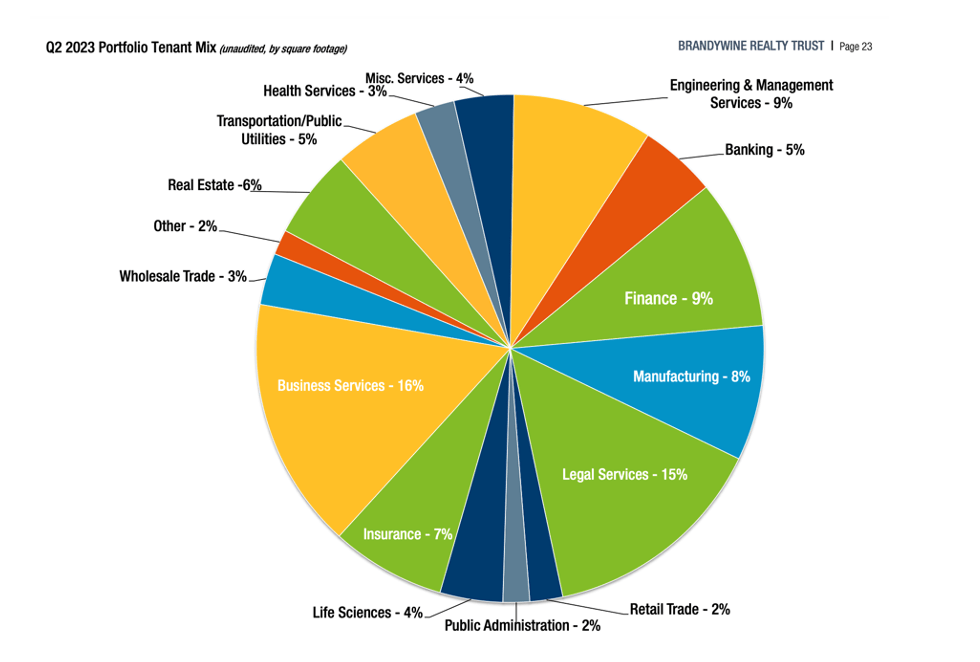

BDN's portfolio consists of traditional office properties, some A-Class and some B-Class, leased to tenants in sectors such as legal and business services, insurance, finance, and banking. These sectors share one characteristic - a significant amount of the work that they do can be done remotely (or even by AI these days...). The result is a real risk of declining occupancy if tenants choose to downsize.

{kind=link}

There's already clear evidence, that the REIT is not able to keep tenants. Over the first six months of the year, BDN only managed to retain 55% of expired leases, which resulted in negative net absorption and a drop in occupancy to 89.4%.

To make matters worse, these renewals had very low rent increases of only about 3% on a cash basis. For reference, Alexandria Real Estate ( ARE ) has been achieving cash rent spreads of 15%+ and people still fear that occupancy will decline.

To me, low retention and low rent spreads are clear signs that tenants don't value the space. Therefore, I expect occupancy to come under even more pressure over the following quarters.

And there are really only two things that BDN can do to turn things around. They can lower rents and/or provide higher incentives to tenants or they can invest heavily into the refurbishment of their properties to make them more attractive. Both options will hurt their cash flow substantially and likely eventually lead to a dividend cut.

Reason #2 - highly leveraged balance sheet

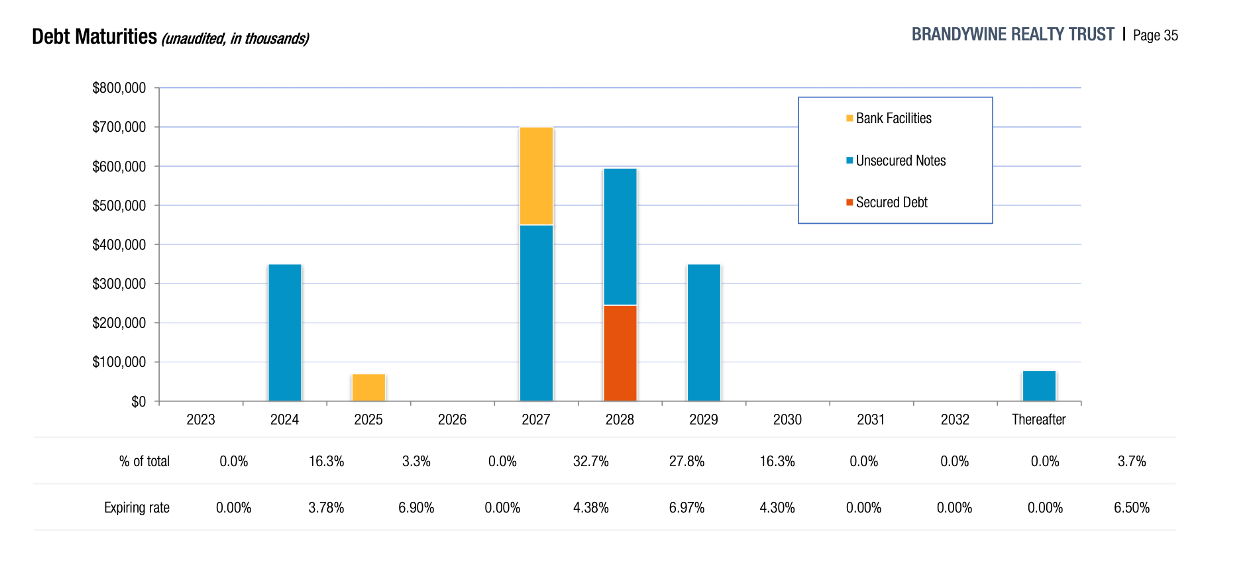

BDN has a low-rated BB+ balance sheet with high leverage of 7.6x EBITDA and a relatively high average cost of debt of 5.2%. With just 80% of debt fixed-rate and a significant debt maturity of $350 Million less than 12 months from now, I expect that BDN's interest expense will rise materially if interest rates stay high. This will also hurt the company's cash flow.

{kind=link}

The key to getting through a longer period of high inflation and high-interest rates is to invest in companies that are able to increase their revenues and have low (and fixed-rate) debt. BDN has neither.

Safehold Inc. ( SAFE )

I'm actually quite bullish on Safehold, but it is important to recognize that the investment is dependent on interest rates decreasing. In other words, it is not the best pick for a higher for longer scenario.

SAFE is a one-of-a-kind REIT that focuses on extremely long duration (99 years in most cases) investment-grade ground leases. Ground leases provide an additional layer of safety compared to traditional real estate because in case of default, the landlord gets to keep the tenant's property free of charge.

As a result, the REIT earns a very reliable and visible cash flow.

But safety comes at a cost.

Firstly, the REIT's ability to raise rents is mostly capped at 2-3% per year as a result of built-in rent escalators and extremely low turnover of tenants.

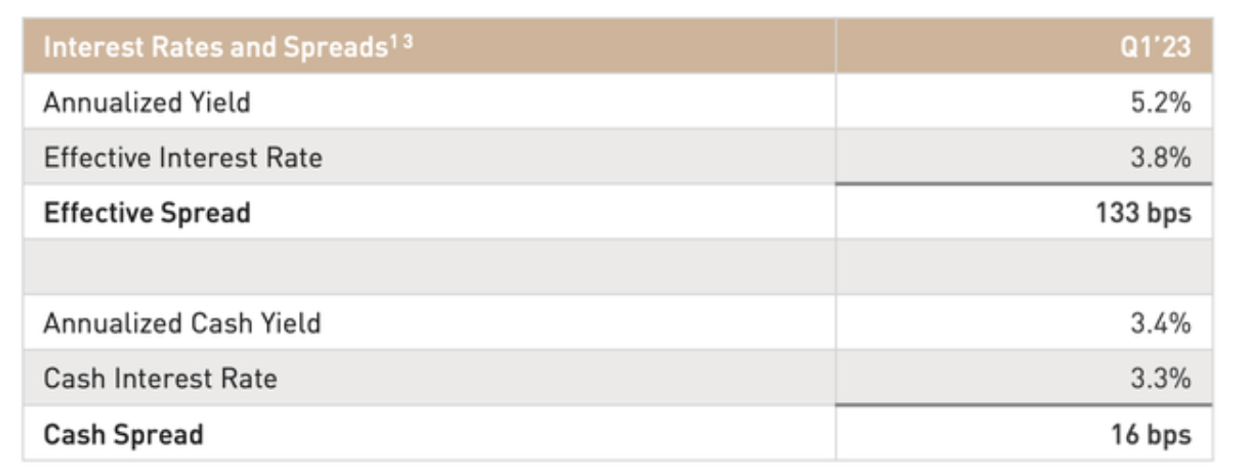

And secondly, investment-grade ground leases tend to have very low cap rates. In the case is Safehold, the yield is only 5.2% (and 3.4% on a cash basis). This results in a very low spread to the REIT's cost of capital, which makes earnings and valuation very sensitive to changes in interest rates.

{kind=link}

The balance sheet mirrors the long-term nature of the leases but has about $1 Billion outstanding on the revolving line of credit, which matures in 2026 and incurs interest at SOFR + 1%. Clearly, if interest rates stay elevated, the interest expense will increase and the spread that SAFE earns will be under pressure.

Don't get me wrong, this is a REIT that has triple-digit upside potential when interest rates decrease, which is why I've been slowly accumulating shares - and so has CEO Jay Sugarman.

{kind=link}

But for the reasons discussed, the share price is very likely to stay suppressed for as long as interest rates remain high.

Bottom Line

Not all REITs are created equal.

Some are likely to outperform no matter which route interest rates take and some will continue to bleed. In my opinion, it comes down to the REIT's ability to increase cash flow and the 3 REITs highlighted above will struggle to do that in a higher for longer scenario.

For further details see:

3 REITs That Should Suffer In Higher For Longer