PSA - 3 Speculative Stocks That Generate Robust Free Cash Flow

2023-08-22 07:54:49 ET

Summary

- Net cash and future expectations of enterprise free cash flows are the primary cash-based sources of intrinsic value for a company.

- Dividends are not a driver of a company's value, but rather a component of capital appreciation that otherwise would have been achieved had the dividend not been paid.

- Tesla, Nvidia, and Public Storage are three speculative companies that generate strong free cash flows. Tesla and Nvidia have nice net cash positions on the books, too.

By Brian Nelson, CFA

There are two primary cash-based sources of intrinsic value: net cash on the balance sheet and future expectations of enterprise free cash flows. The more net cash a company has on its books, the more valuable the company, all else equal. If expectations of future enterprise free cash flows increase, the value and share price of the company should increase, too. On the other hand, if expectations of future enterprise free cash flows decrease, the value and share price of a company should decline. Though there are many variables that play into an individual company's preference for leverage, how much cash it wants to hold on the balance sheet, and strategic decisions that may impact the trajectory and changes in future enterprise free cash flows, generally speaking, knowledge of a company's net balance sheet position and its prospects for ever-increasing expectations of future enterprise free cash flows is par for the course for any investor.

But why isn't something like a dividend a driver of a company's value? For starters, it is well-documented that a company's share price is reduced by the amount of its dividend payment on the ex-dividend date, so just to keep up with the capital appreciation potential of companies that don't pay dividends, reinvesting those dividends almost becomes a necessity. This makes perfect sense and is explained within the enterprise valuation process--also known as the discounted cash flow valuation [DCF] approach. Net cash is an add back to the present value of future expected enterprise free cash flows. When a company pays a dividend, its net cash is reduced on the balance sheet, and therefore, its intrinsic value is reduced. This dynamic is captured when the stock price is marked down by the amount of the dividend payment when it trades ex-dividend. The dividend, itself, therefore is not a driver behind total return, but rather a component of capital appreciation that otherwise would have been achieved had the company not paid a dividend. In this article , we dig a bit deeper to better facilitate the understanding of the dividend, and we've reproduced an excerpt for this work:

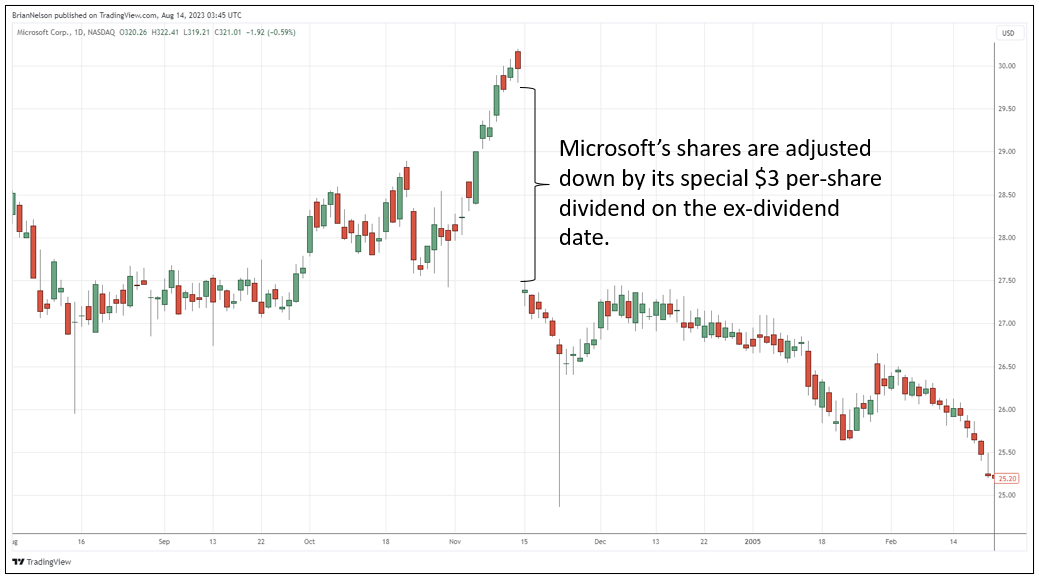

Let's use [a] real-life example of a...prominent company such as Microsoft. Back in 2004, Microsoft announced a special one-time dividend in the amount of $3 per share. It was payable to shareholders of record as of November 17, 2004, so to be eligible for the dividend, one had to buy the stock the week before, at least two trading (business) days before the record date, before the company went ex-dividend after November 12, 2004. Clearly, the chart below shows that Microsoft's shares were adjusted downward by the $3 per share dividend following the ex-dividend date, and while trading subsequent to that event impacted the stock, it is still important to understand this important market function when it comes to the dividend. If Microsoft had not paid this $3 per-share special one-time dividend, it is fair to assume that its share price would not have been adjusted down by the dividend. Perhaps this is easy to understand for many readers; for other readers, it may be helpful to evaluate the chart below to facilitate the understanding.

When a company announces a dividend, its share price is reduced by the amount of the dividend on the ex-dividend date. (Trading View)

Don't get me wrong: Dividends are great. They serve a number of purposes for investors, and companies that pay a free cash flow backed dividend can be great long-term investments. Visa Inc. (V), Apple Inc. (AAPL) and Microsoft ( MSFT ) are just a few of our dividend-paying favorites. We also provide a Dividend Growth Newsletter as well as a High Yield Dividend Newsletter to our members, but a dividend is what it is: capital appreciation that otherwise would have been achieved had the dividend not been paid. Within the enterprise free cash flow construct, the dividend is cash that otherwise would have piled up on the balance sheet instead of being dispersed to shareholders. Looking at how stock prices adjust following large, one-time dividends is perhaps the best way to understand the dividend payment, while studying the enterprise valuation process, or the discounted cash-flow method, helps investors understand why this adjustment occurs.

{kind=link}

It's important that income and dividend growth investors don't let the dividend tail wag the total return dog. Most important to all investors should be total return, as the dividend yield should be viewed as being "paid out" of total return, not a driver of it. I think it makes sense to say that investors are going to get their total return whether they like it or not. We think that enterprise valuation (i.e. the DCF model) is the key driver behind the total return profile of equities, as the process does a great job explaining the magnitude of market capitalization variations, while changes in key levers of the DCF, including changes in interest rates and future expectations of financials such as free cash flows drive changes in share prices. For example, the aggressive rate-hiking cycle last year during 2022 not only destroyed many bond allocations (as bond prices fell), but also hurt equity prices as long-duration assets faced pressure (their long-duration free cash flows were worth less given higher discount rates). When companies issue forward guidance generally ahead of market expectations, forecasts within the DCF process often have to be raised, and this reset also resets the stock's valuation and price higher.

With all of this said, we're huge fans of companies that have strong net cash positions on the balance sheet and future expectations of enterprise free cash flows. Net cash on the books creates an asymmetric risk/reward scenario as the strong financial position generally pushes bankruptcy and capital-market dependence risk to practically nothing, while it offers businesses option value where a company might be able to scoop up assets on the cheap during troubling times when credit is tight or prohibitive. We also like stocks that have the prospect of the market ever-increasing its expectations of future enterprise free cash flows. As future expectations of enterprise free cash flows increase, the probability of a strong stock price advance that follows the intrinsic value advancement also increases. Sometimes the price move may come ahead of the value increase. In this article, let's go up the speculative risk spectrum and release three ideas with strong free cash flow generation that may fit the bill for more risk-seeking investors.

Tesla ( TSLA )

Tesla is a battleground stock. Some believe that the company could be heading for bankruptcy, while others believe it may turn into a broadly diversified technology behemoth that also happens to make electric vehicles. Whatever your opinion, it's hard not to like its cash-based sources of intrinsic value. When Tesla reported its second quarter 2023 results July 19, the EV-maker revealed that it finished June 30, 2023, with $23.1 billion in cash and just $2.3 billion in debt--good for a material net cash position. For the trailing twelve months ended June 30, 2023, Tesla generated ~$6.2 billion in free cash flow.

We think both of these measures are strong, and while free cash flow generation has slowed in recent quarters, for the second quarter of 2023, it still advanced more than 60%. Bears will continue to find reasons to not like the stock, but Tesla continues to fit the bill of a net-cash-rich, free-cash-flow generating, secular-growth powerhouse, a far cry from what one might have thought given the sentiment on the name over the years. The high end of our fair value estimate range of Tesla stands at $335 per share (its equity is trading at ~$226 at the time of this writing).

Nvidia ( NVDA )

Artificial intelligence represents a huge catalyst for Nvidia. (Nvidia)

{kind=link}

Nvidia's outlook for the second quarter of its fiscal 2024 was phenomenal thanks to tremendous interest in its chips that power artificial intelligence [AI]. Revenue during Nvidia’s fiscal second quarter is expected to be ~$11 billion versus consensus that had been looking at ~$7 billion, implying a forward outlook more than 50% better than what the Street was looking for at the time. The company ended April with $4.37 billion in net cash on the balance sheet, while it hauled in $2.67 billion in free cash flow during its fiscal first-quarter 2024, more than it generated in all of operating cash flow during the same period a year ago.

Artificial intelligence [AI] is the real deal, in our view, and Nvidia has the chips to power it. When we first tested generative AI via ChatGPT, we were blown away by the technology. There may be some hype surrounding the technology powering large language models at these early stages of adoption, but from where we stand, the future is as much AI as the present is Apple products, Google ( GOOG ) ( GOOGL ) search, and Microsoft and Amazon ( AMZN ) cloud. Though our valuation of Nvidia may be conservative, it's hard to make the argument that the company does not have the prospect for the market to build in ever-increasing future expectations of enterprise free cash flows.

Public Storage ( PSA )

REITs have not performed as well as one might have thought. (Vanguard)

Why is Public Storage included in this list of three speculative plays? Well, for starters, REITs tend to have huge net debt positions and they are heavily levered to changes in interest rates, which have punished their shares in recent years. Among the REIT sub-sectors, however, we continue to favor the self-storage space mostly because its traditional free cash flow dynamics are much more attractive than other areas within the broader REIT arena. Self-storage REITs are generally recession-resistant, too, offer high operating margins, and generally lower maintenance capital requirements.

Public Storage is our favorite self-storage REIT, and the firm recently announced that it would acquire Simply Self Storage after walking away from its proposed transaction for Life Storage, which merged with Extra Space Storage ( EXR ). Public Storage has a net debt position on the books, but its free cash flow generation of ~$1.38 billion easily covered its total dividends/distributions of $1.15 billion during the first half of this year. As a speculative play, the company's dividend yield ~4.4% at the time of this writing isn't too shabby.

For further details see:

3 Speculative Stocks That Generate Robust Free Cash Flow