MCHI - 3 Stocks That Are Still A Buy On China's Recovery Story

2023-08-08 12:46:53 ET

Summary

- China's economic recovery has turned out to be slower than expected, with growth forecasts reduced for 2023. But strong domestic consumption indicates that there are still pockets of recovery.

- Segments like jewelry, apparel, and medicines are doing well. The stock picks among these also are subject to the criteria of being financially healthy, resilient, and geographically diversified with attractive valuations.

- The three best recovery plays right now based on these are Compagnie Financière Richemont, Ermenegildo Zegna, and AstraZeneca.

As China's lockdowns ended late last year, a sharp economic recovery was widely expected. Seven months into 2023 however, and initial forecasts have been slashed . Big banks expect growth to come in at 5.4% from 5.9% earlier. This still isn't too bad, to be sure. In 2022, the economy grew by a much smaller 3% .

Focus segments

But I believe that when investing in the China recovery story, caution is still called for. The drag on growth is driven by some specific segments like manufacturing and real estate, which are, broadly speaking, best avoided right now. Compared to GDP growth of 5.5% year-on-year (YoY) for the economy in the first half of 2023 (H1 2023), manufacturing grew by 3.9% and real estate was flat from last year.

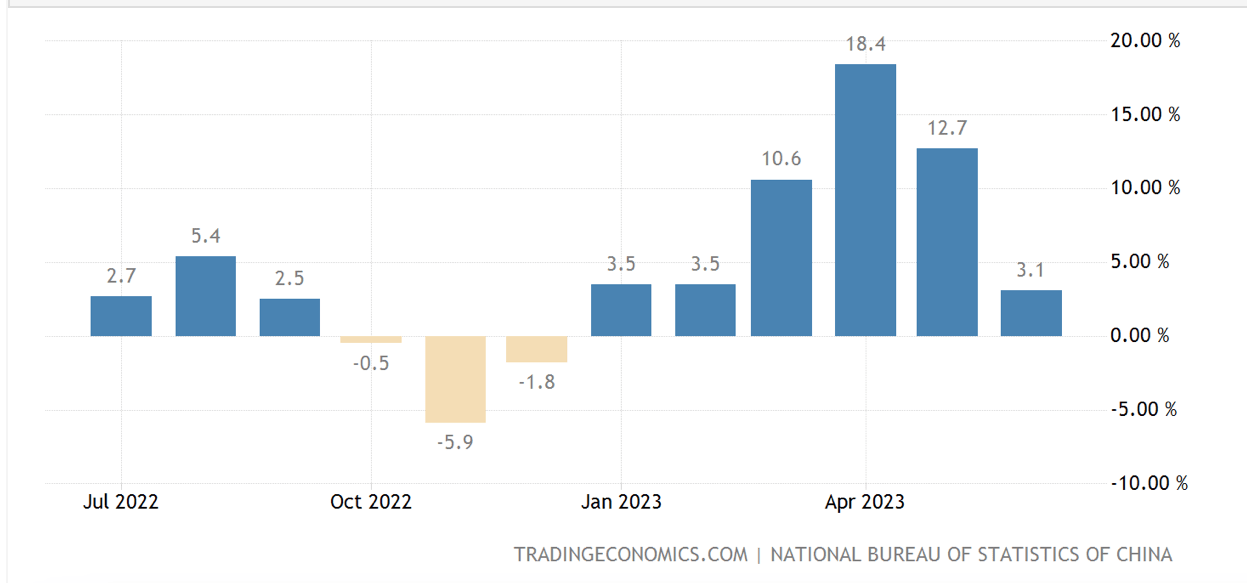

There are, however, some segments of the economy that are still seeing impressive growth. A look at the economy from the expenditure side reveals strong domestic consumption. Per capita consumption expenditure grew faster than overall GDP, by 8.4% on a nominal basis, and by 7.6% on a real basis in H1 2023. A healthy consumption expenditure trend is also confirmed by retail sales for consumer goods, which rose by 8.2% over the same period on account of double digit growth in April and May (see chart below).

{kind=link}

Zoning in on the segments shows that segments like "gold, silver and jewelry," "clothes, shoes, hats, and textiles" and 'traditional Chinese and western medicines" have seen the highest growth. They have all grown in double digits at 17.5%, 12.8% and 11.1% respectively, for enterprises above the size of CNY 20 million, far surpassing the average retail sales growth.

Criteria for stock selection

It's from these segments that I have picked the stocks as good plays on the China recovery story. But given how broad these categories themselves are and the signs of weakness in China itself, the following criteria have been applied:

- This is a no brainer. The companies need to be financially healthy, with growth supported by China's recovery.

- They need to be in resilient industry segments in the event of a bigger than expected slowdown in China. I'm not ruling this out, considering the mixed signals from data points. Retail sales slowed down to 3.1% in June 2023 and consumer prices have been flat during the month, though GDP growth actually accelerated to 6.3% during Q2.

- They need to be geographically diversified enough not to depend on a single market, on uncertainty across global markets right now.

- The market valuations are attractive enough to make a buy case for the stock.

Based on this, I like three stocks right now, which meet a majority, if not all of the criteria above.

Stock picks

- Jewelry: Compagnie Financière Richemont (OTCPK: OTCPK:CFRUY )

The Swiss luxury company Richemont is my pick for jewelry for two reasons. First, it has performed well on account of China's recovery. Asia Pacific demand for the company grew by 40% at constant rates in Q2 2023, far higher than the overall growth of 19%, which isn't bad to start with. Specific to China, Hong Kong and Macau, the company mentions "substantial sales increases ranging from double-digit growth in the mainland to triple digits in the latter two locations."

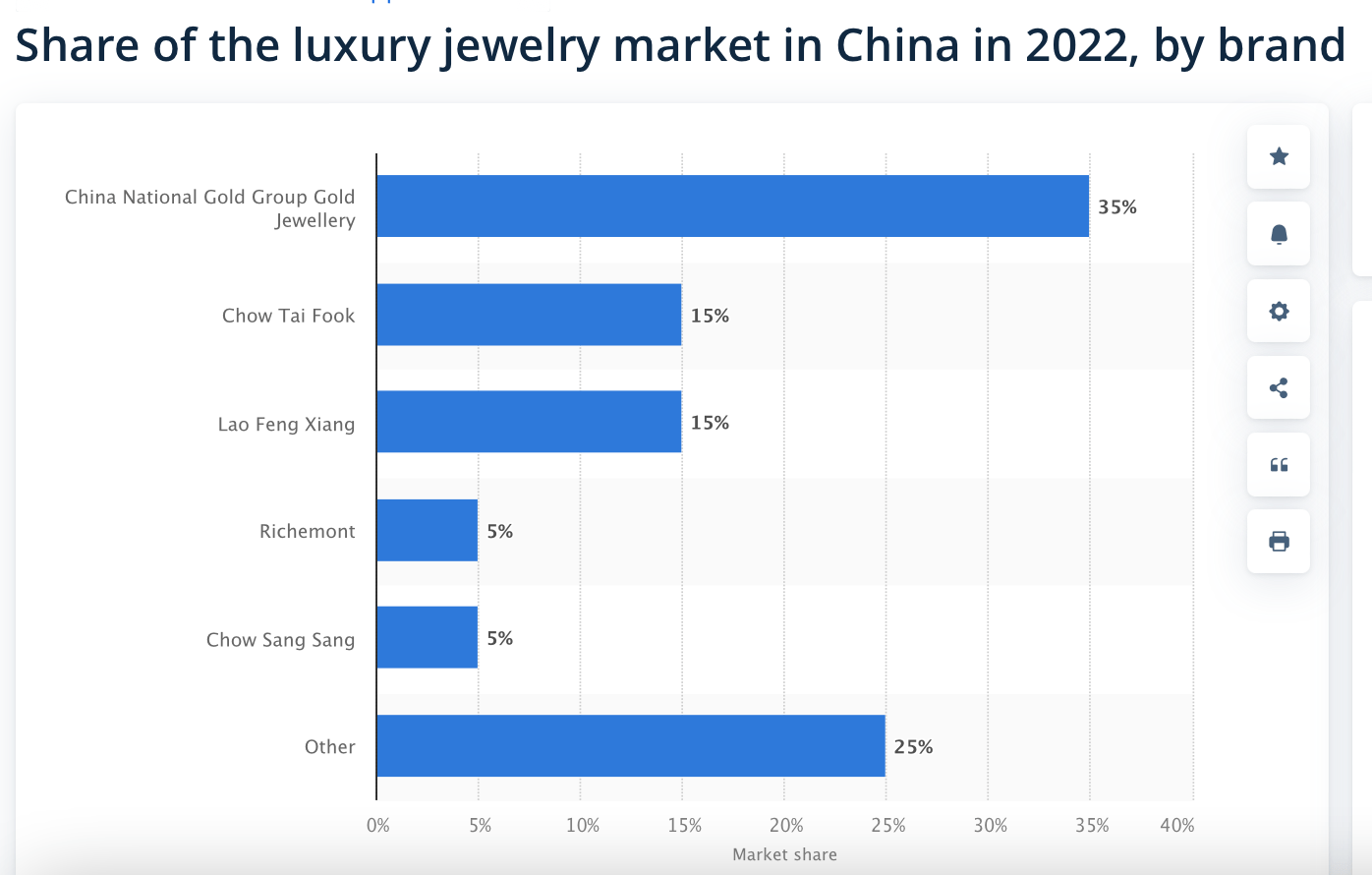

The company's big jewelry segment drove overall growth, with an increase of 24%, with an uptick in brands like Buccellati, Cartier and Van Cleef & Arpels. It's no coincidence, of course, that Cartier and Van Cleef & Arpels are among China's top 10 jewelry brands by market share. They're also among the only four international brands on the list, with the other two being LVMH ( OTCPK:LVMUY ) owned Tiffany & Co and Bvlgari. But interestingly, Richemont has an edge over LVMH in that it's the only international jewelry company among the top five by market share in the Chinese jewelry market (see chart below).

{kind=link}

It does face the challenge of weakening demand from the rest of the world, however. The company's growth ex-Asia Pacific for the latest quarter was a weak 4% at market exchange rates, compared to the 14% inclusive of the region.

At the same time, it has the advantage of being in the resilient luxury sector. While the segment is informed by trends in consumer expenditure, the slowdowns it sees are relatively shallow and the bounce back is quick. For instance, Richemont saw only a small dip in sales for the year ending March 2021, which was marked by the pandemic, and it also remained profitable.

Also, I like that while Asia Pacific demand is huge for it, with a 42% revenue share for the latest quarter, it's well distributed across Europe, the US and other markets like Japan and Middle East and Africa as well.

Even otherwise, Richemont is a financially strong company, with strong profit margins and a healthy balance sheet. Its market valuations are attractive too, compared to luxury peers. In fact, they're also fairly close to the average consumer discretionary sector. For example, its non-GAAP forward price-to-earnings (P/E) ratio is at 17.5x compared to the 15.9x for the sector.

- Apparel: Ermenegildo Zegna ( ZGN ).

As an apparel demand play, I like another luxury company, Ermenegildo Zegna. China contributes to a significant 34% of its sales, and a pickup in demand in the economy has positively impacted growth positively in H1 2023.

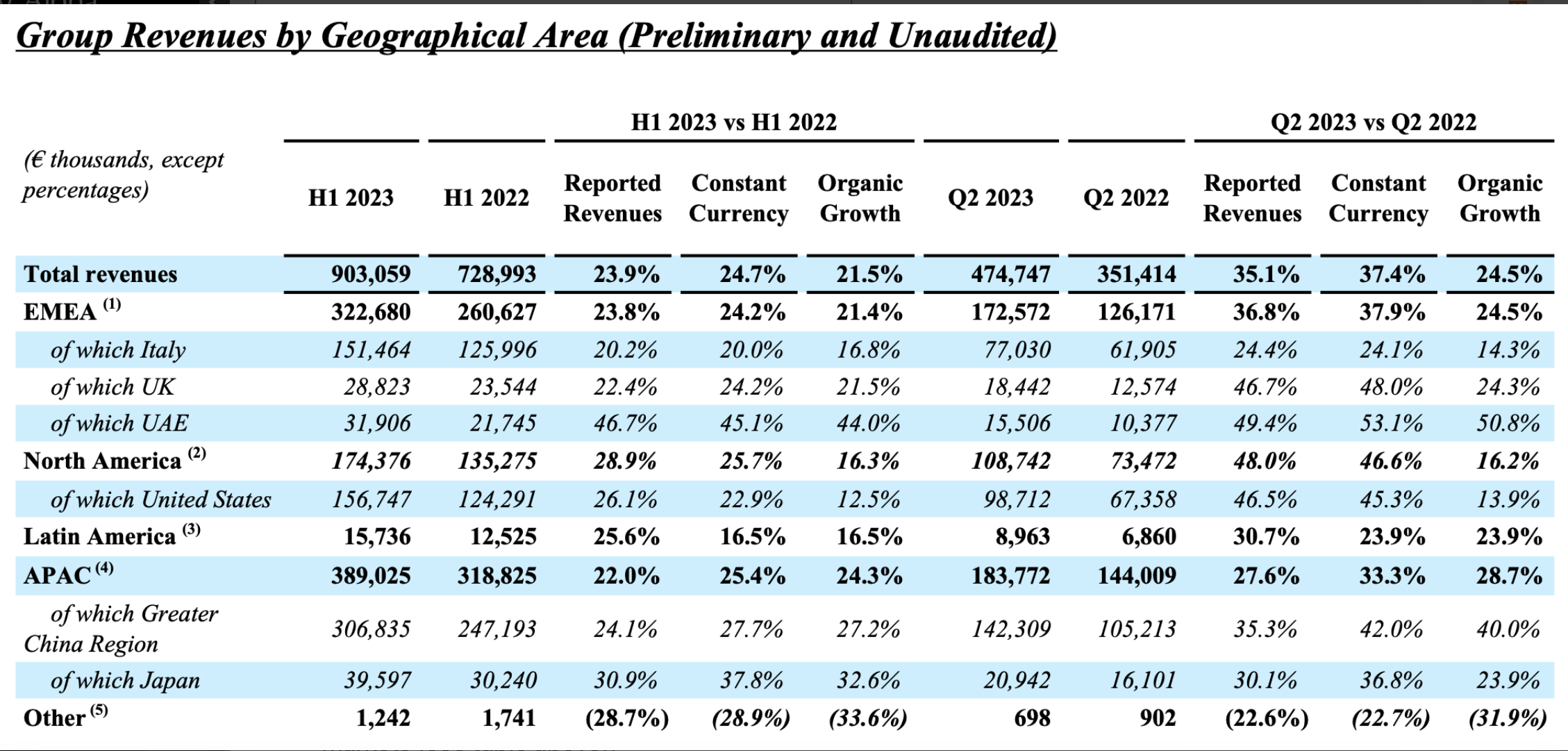

While its total revenues in constant currency grew by 24.7% during this time, growth from China was higher at 27.7%, with an acceleration in growth in Q2 2023 (see table below). Backing its considerable demand from the market, is its history in China. It was the first luxury apparel company to enter it, in 1991. Its in-house manufacturing capabilities are said to make it more responsive to change trends in the market too.

{kind=link}

Much like Richemont, it too is diversified with markets like Europe and the US big for it too. In fact, in sharp contrast to other luxury companies, Ermenegildo Zegna also showed strong growth in the US market due to its acquisition of Tom Ford International, the owner of Tom Ford Fashion, during H1 2023. This indicates that it's very well placed in the event of a slowdown in China or the US or both, because so far it seems unlikely that its growth is going to be dented significantly.

Its margins have been wanting so far, with sub-10% operating margin for 2022. However, it's likely to see an improvement soon because of the acquisition too, as Tom Ford's net margins are over 2% higher at 5.7% compared to its pre-acquisition numbers. In any case, the company has a guidance of 15% adjusted operating margin by 2025, even leaving out Tom Ford fashion.

Compared to Richemont, its market valuations are definitely high with a forward non-GAAP P/E of 31.6x. However, going by its robust growth, especially in the US, and the fact that the P/E has actually come off from a higher 35x towards the start of the year, indicates that there's still upside for the stock.

- Healthcare: AstraZeneca ( AZN )

Arguably, the least affected by China, is the pharmaceuticals major AstraZeneca, which still finds a spot on the list as a play on strong medicines' sales. Here's why. China's far from the most significant market for it, but with a 14% share in revenues, it's far from trivial either. So far, growth from the market has actually been a drag on the company (see table below), but going by is guidance, that's set to change.

{kind=link}

In the only mention of a single market in its outlook, it has raised its forecast for China for 2023. It expects revenues from the market to increase by "low to mid single digit" percentage compared to the earlier forecast of a "low single digit" during this year. Growth expectations for China are now at par with its overall sales forecast. This means that there will be a sharp slowdown from its other markets, while demand from China will actually help steady it.

While the outlook reflects slowing down in the remainder of the year, so far, AstraZeneca has done rather well. It recently reported a fine set of results for H1 2023. Its ex-COVID medication sales grew by 16% at constant exchange rates and by 12% at actual rates. Its core EPS also showed strong growth of 21%.

In any case, as a healthcare company, it qualifies as a classic defensive, which is likely to be coveted by investors if there's a growth slowdown across the market. AstraZeneca looks attractive in terms of its market valuations too, with a non-GAAP forward P/E at 19.1x compared to the 20x for the healthcare sector. Its P/E also is a bit lower than the company's own five-year average ratio of 19.5x. The stock also has a long history of both good price returns and passive income gains from its dividends.

For further details see:

3 Stocks That Are Still A Buy On China's Recovery Story