VYM - 3 Top Dividend Stock Picks For December

2023-12-04 07:45:00 ET

Summary

- Dividend stocks are today heavily discounted.

- Opportunities are abundant in REITs, MLPs, and utilities.

- We highlight three of the best opportunities for December.

Co-produced by Austin Rogers.

This year has been a harrowing one for dividend stock investors.

Generally speaking, the higher the dividend yield, the worse the stock has performed this year.

Among "high dividend yield" ETFs, the Vanguard High Dividend Yield ETF ( VYM ) is low-yielding at about a 3.2% yield, while the iShares Core High Dividend ETF ( HDV ) is higher at 4.1% and the Global X SuperDividend U.S. ETF ( DIV ) is very high at about 7.5%.

Sure enough, over the last year, VYM has suffered the least, followed by HDV, and DIV has seen the worst selloff.

While VYM's holdings are mostly in the financials, consumer staples, healthcare, and industrials sectors, DIV's holdings are heavily concentrated in high-yielding midstream energy companies ( AMLP ) and real estate investment trusts aka REITs ( VNQ ).

The sole exception to this general rule of high yield performing worse than low yield is the business development company ("BDC") industry. These non-bank lenders with predominantly floating rate loan portfolios have performed extraordinarily well amid rapidly rising interest rates and a strong, if softening, economy.

The VanEck BDC Income ETF ( BIZD ), for example, has put in virtually identical total return performance as the SPDR® S&P 500 ETF Trust ( SPY ) over the last year.

But while we remain fans of the BDC business model and owners of multiple BDCs ourselves, we think the best deals are mostly to be found outside of the BDC space right now.

As we go into December, we expect the rally in certain rate-sensitive dividend stock sectors like REITs, utilities, midstream energy to continue as the economy and inflation continue to cool and interest rates gradually decline.

Therefore, we'll look for the best opportunities in each of these three sectors.

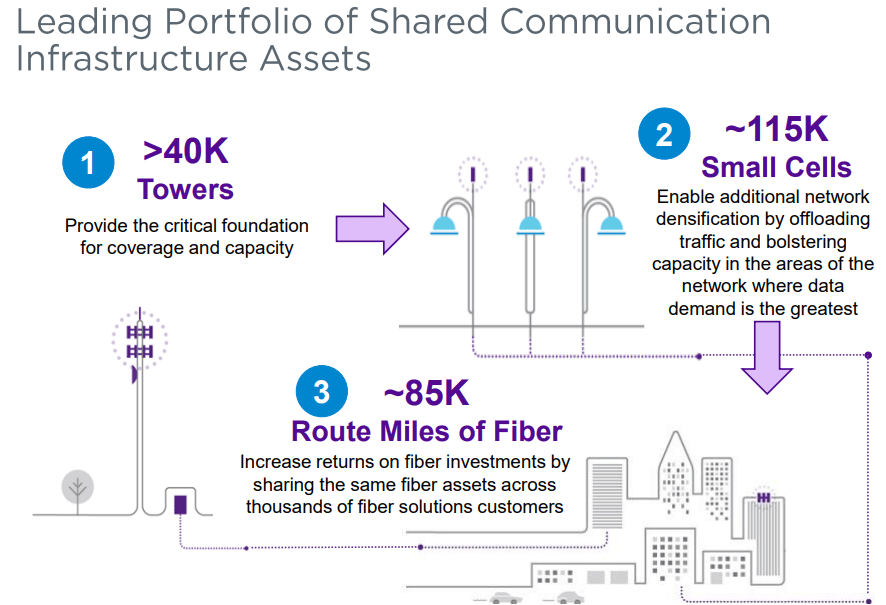

Real Estate: Crown Castle Inc. ( CCI )

CCI is the leading owner of telecommunications infrastructure assets in the United States, with over 40,000 towers, 115,000 small cells (mini towers), and about 85,000 route miles of fiber.

{kind=link}

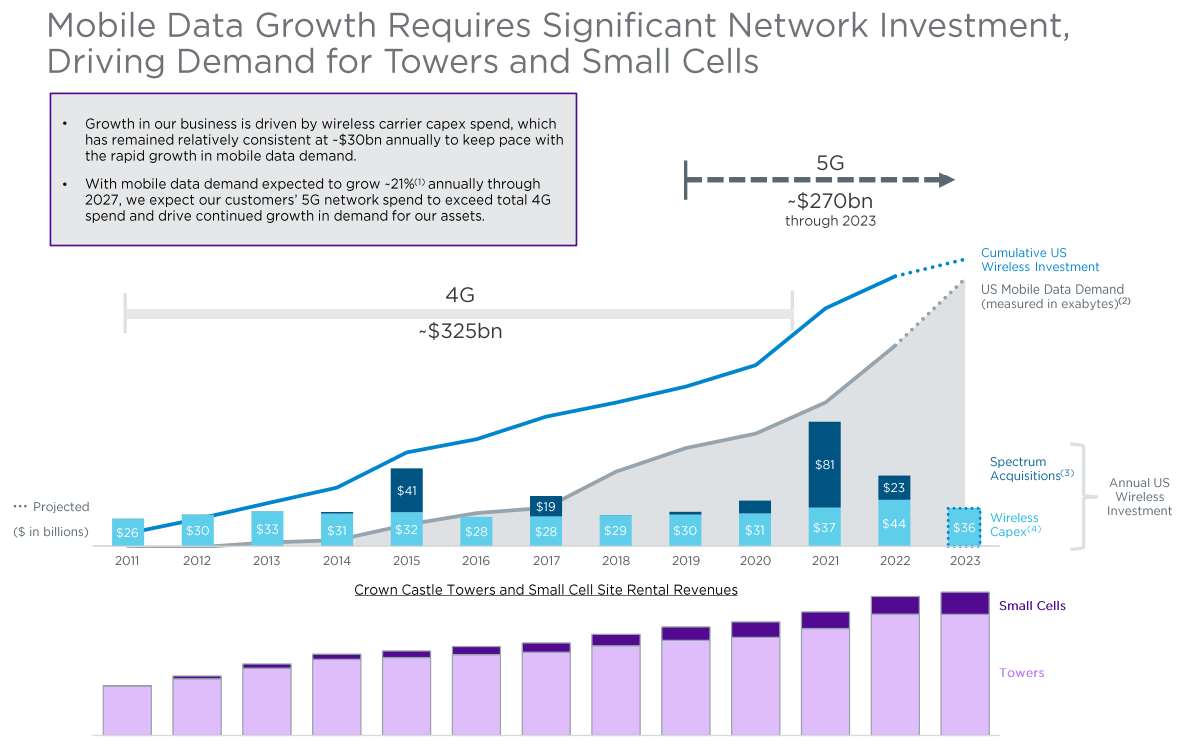

The fundamental driver of CCI's growth is wireless communication capex spending, and the fundamental driver of that is mobile data demand/usage. According to all expert projections, mobile data demand should continue rising at a strong pace going forward as 5G becomes widely adopted.

{kind=link}

The beauty of the communications infrastructure model is that multiple "tenants" can be co-located onto the same asset at little to no incremental cost to CCI. Thus, with multiple tenants co-located, assets' cash yields jump from the single-digits into the double-digits.

For example, CCI's average number of tenants per tower is 2.5, and the cash yield on investment for its towers segment is 12.6%.

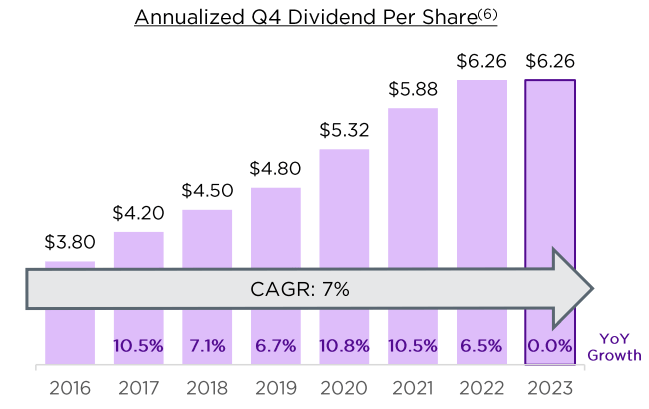

This model has facilitated strong dividend growth for CCI since its conversion to a REIT in 2014.

{kind=link}

CCI pays out substantially all free cash flow, and yet its combination of organic growth and issuing low-cost capital for investments has resulted in an over 90% increase in its dividend since 2015 and a 65% increase since 2016.

The problem for CCI is that capital costs have risen considerably over the last few years, and its fiber/small cell investments still require a steady stream of capital to fund them.

The market seems to think CCI's growth model has been broken by higher interest rates, despite the REIT's relatively modest use of leverage.

We disagree. We think CCI has many options to continue growing, and apparently the activist investor Elliott Management thinks so too.

After amassing an over $2 billion stake in CCI (~4.5% of market cap), Elliott is commencing a battle with management to replace the board and abandon the capital-intensive fiber segment. The next six months should be very interesting to watch, and we are confident that whatever the outcome of Elliott's activism, shareholders should benefit.

CCI still offers a very high yield of 5.8% while remaining near its lowest price-to-AFFO multiple since becoming a REIT in 2014. There's a lot of negativity priced into CCI, but we see far more upside than downside at this point.

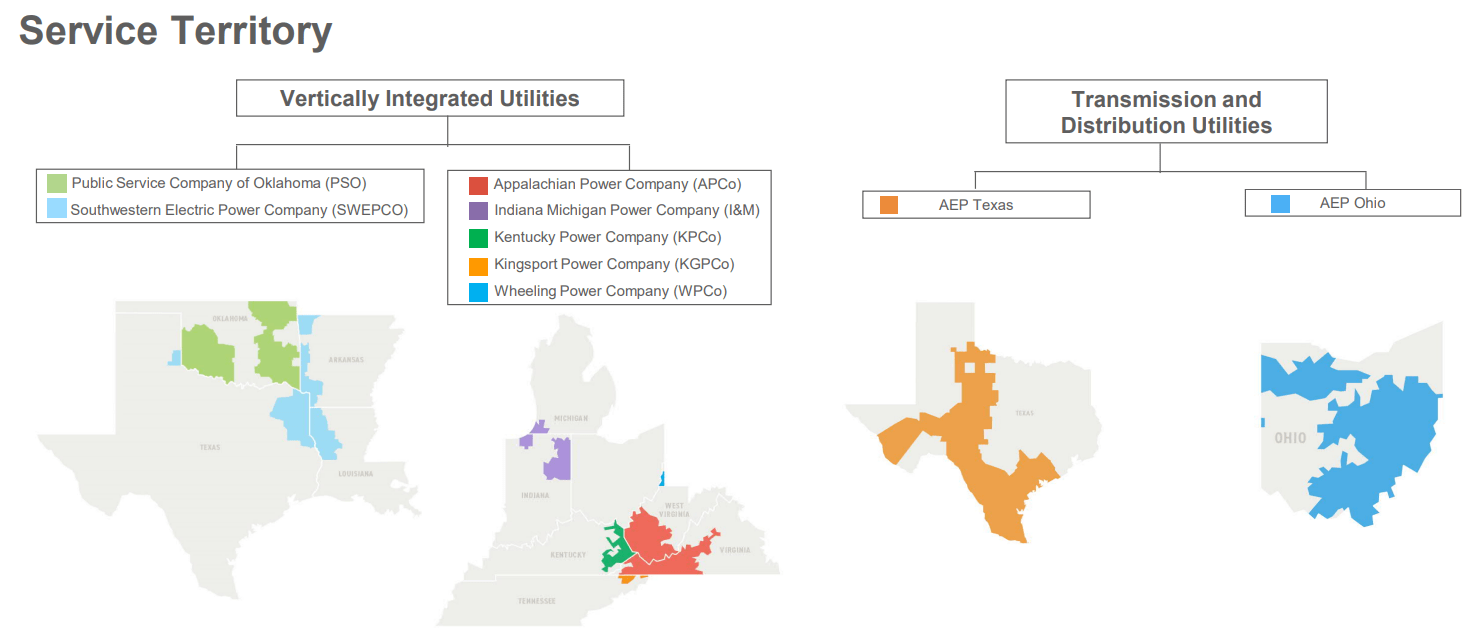

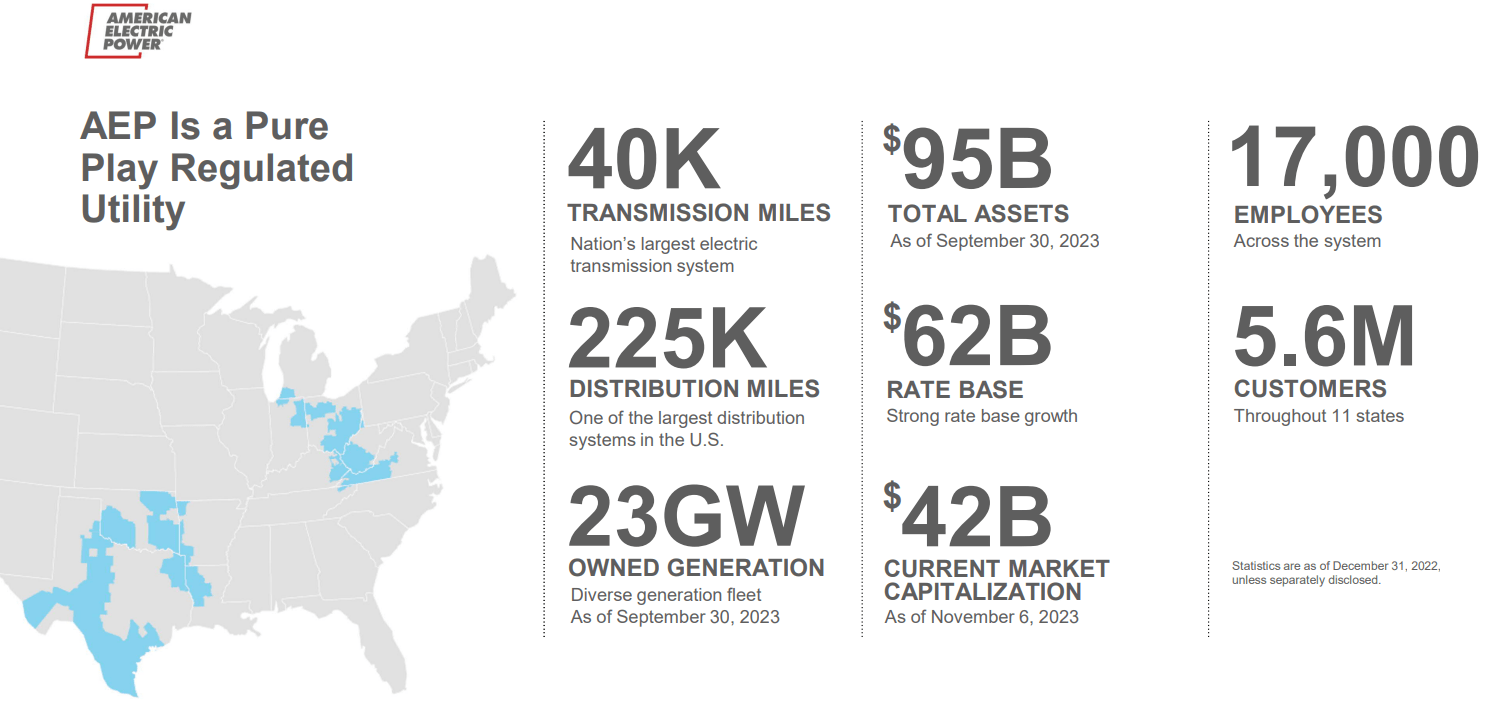

Utility: American Electric Power Company, Inc. ( AEP )

AEP is one of the nation's largest regulated electric utilities, concentrated entirely in two regions of the U.S.: the Midwest and the South. Slightly over half of AEP's retail revenues come from Ohio (23%), Indiana (15%), and Texas (15%).

{kind=link}

The company boasts 5.6 million customers across 11 states as well as an expansive portfolio of transmission and distribution assets (power lines) that will be increasingly valuable as the electric grid relies more and more on renewable energy.

{kind=link}

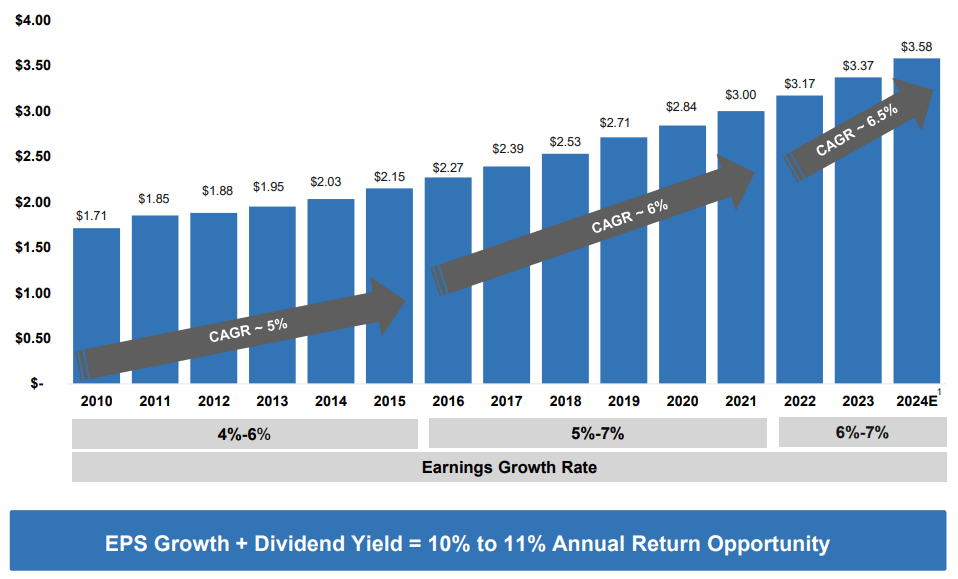

With a robust capital spending plan focused largely on transmission and distribution assets over the next decade, AEP targets 6-7% EPS and dividend growth going forward. On top of AEP's ~4.5% dividend yield, this should result in 10-11% total returns even assuming no multiple expansion .

{kind=link}

However, given that AEP is trading near the lower end of its P/E ratio range from the last decade, we believe AEP has around 20-30% of upside on top of this, which should push total returns up to the mid-teens over the next five years.

The market seems to be concerned about AEP's cost of capital, but there are two pieces of good news. First, AEP has only 10% of corporate-level debt maturing in 2024. Far less of its asset-level debt matures next year. And second, utilities can gradually be recouped for increased interest expenses through their regulated ROEs.

AEP's strong, investment-grade credit ratings of BBB/BBB+/Baa2 should ensure that its cost of debt returns to an adequately low level once interest rates more broadly decline.

Midstream Energy: Enterprise Products Partners L.P. ( EPD )

Note: EPD is a master limited partnership ("MLP") and sends out a K-1 form for tax purposes. This makes tax preparation a bit more complicated, but an experienced accountant should be able to handle it just fine. Besides, most investors find that the tax benefits of EPD's distribution more than makes up for the additional tax prep hassle.

EPD is in the midstream energy Hall of Fame. The MLP boasts a 25-year dividend growth record as well as a best-in-class board and management team that owns about 1/3rd of the business. Most of that is owned by the children of EPD founder Dan Duncan, making EPD a second-generation family business.

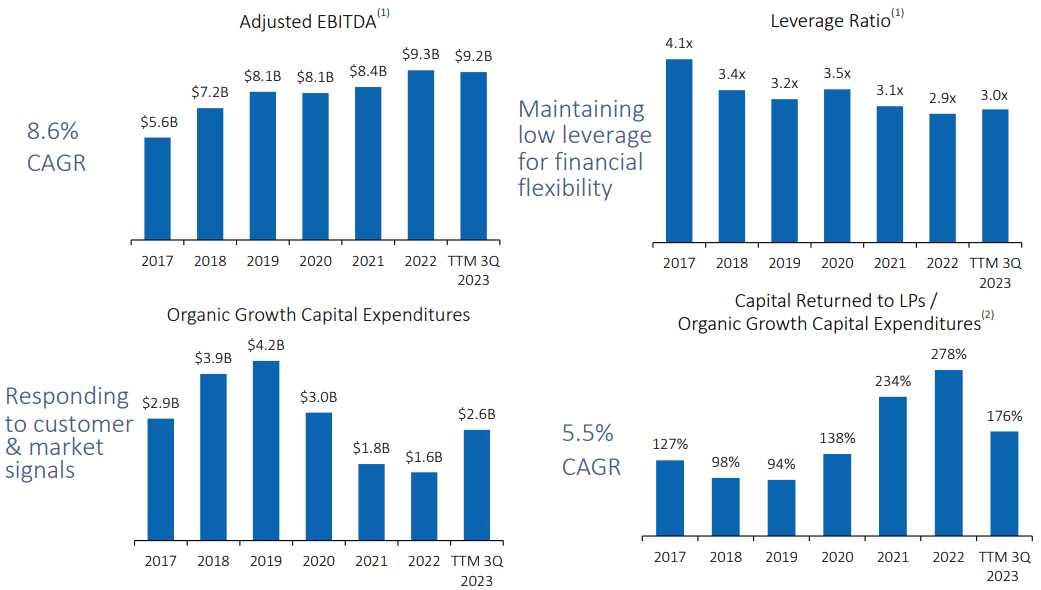

This multi-generational nature of the controlling owners facilitates a rare farsightedness and long-term orientation, as well as smart, patient capital allocation. EPD is also self-funding, allowing both maintenance and growth capex spending to be funded by cash flow from operations.

This allows for a few virtuous cycles to take effect. First, it has allowed leverage to sustainably fall to management's target of ~3x.

{kind=link}

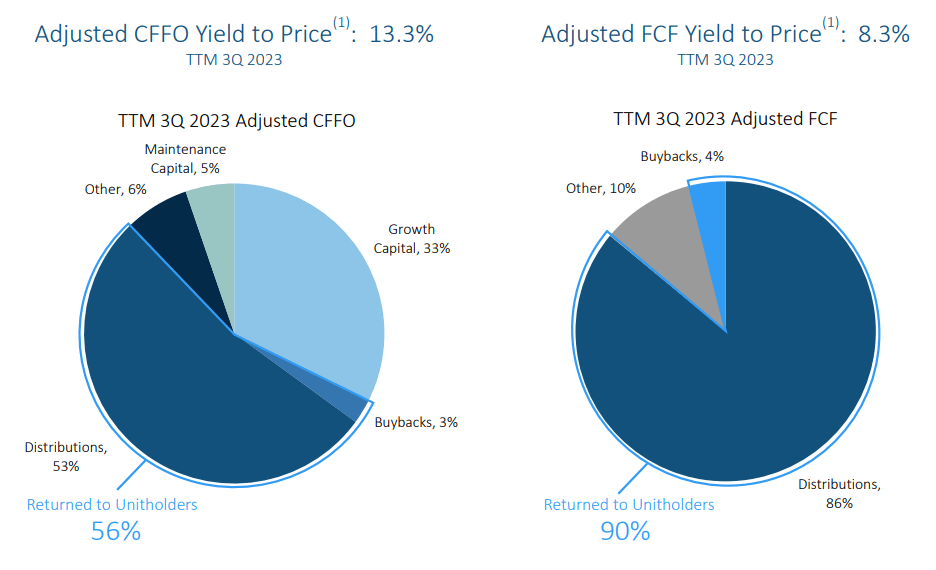

Second, it has allowed more free cash flow ("FCF") to go toward distributions and unit buybacks.

Note in the illustration below that the 90% payout ratio seen on the right is based on FCF after growth capital spending .

{kind=link}

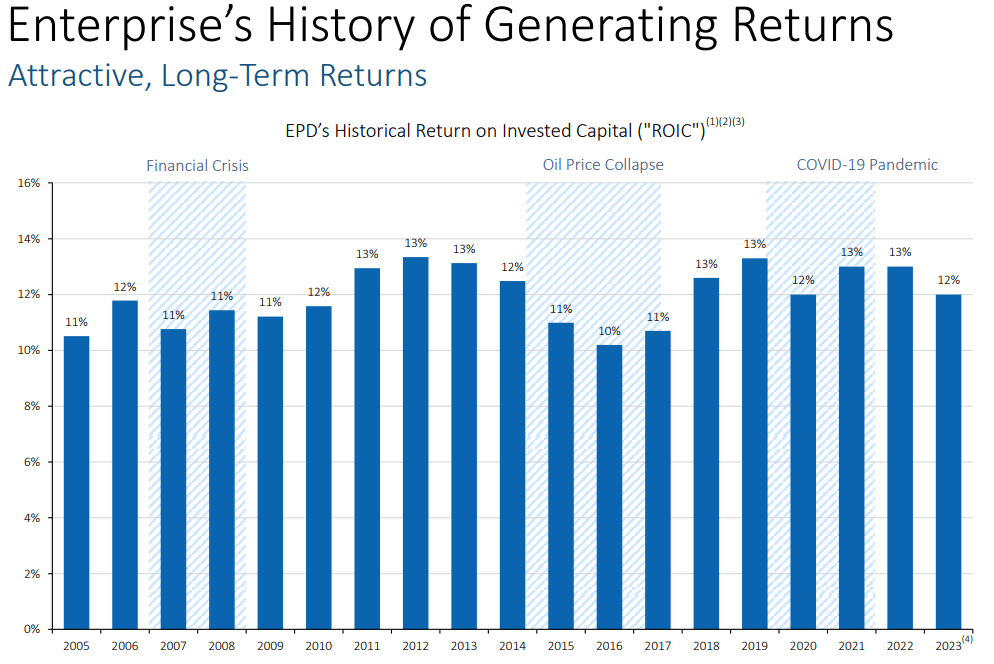

With continued capital allocation prudence as well as a low cost of capital from EPD's A- and equivalent credit ratings, the MLP should continue to generate double-digit returns on invested capital going forward, just as it has consistently done in the past.

{kind=link}

As you can see, this year's 12% ROIC isn't an anomaly. It is about average for this highly stable and conservatively managed MLP.

EPD is truly best-in-class and fairly valued today. Between a 7.5% yield and 4-5% earnings and distribution growth, we think EPD will easily be able to turn in low double-digit total returns going forward.

Bottom Line

Opportunities still abound in today's market. Who knows what challenges and opportunities 2024 will bring, but we are confident that buyers of quality dividend payers like the three discussed above will be richly rewarded in the long run. Not only do they each sport attractive dividend yields, they also have strong prospects for dividend growth going forward.

For dividend investors, that is a wonderful combination.

For further details see:

3 Top Dividend Stock Picks For December