BNL - 3 Top REIT Picks For 2024

2023-11-26 08:05:00 ET

Summary

- REITs are priced at their lowest valuations in years.

- Net lease REITs are particularly cheap, despite enjoying steady growth.

- We highlight three of our Top Picks for 2024.

In a recent article , we reminded you why we remain bullish on REITs ( VNQ ) despite the now much higher interest rates.

In short, REITs are today priced at their lowest valuations in a decade, and as a result, quite a few of them now offer >20% expected annual total returns over the coming 3-5 years.

These high returns are the result of historically high dividend yields, strong fundamentals, consistent growth, and some repricing upside as valuation multiples expand back to more reasonable levels.

To take a simple example: if a REIT pays a 6% dividend yield, grows by 4% per year, and sees its FFO multiple expand from 10x to 14x over 3 years, that would result in ~20% average annual total returns.

6% dividend yield + 4% annual FFO per share growth + 10% annual repricing upside = 20% annual total return

Typically, such high expected returns would only be achievable if you took on significant risk and invested in risky REITs that were heavily leveraged.

But because REITs are now so heavily discounted, you can actually achieve these results by even investing in some of the highest-quality blue-chip REITs.

They have sold off just as much as other REITs (if not more in some cases!) and now offer asymmetrical risk-to-reward.

Today, we take a closer look at 3 of our favorite blue chips to accumulate today and add a bit more capital to each of them:

Net Lease REIT Blue-Chips At A Discount

When I first got into real estate, my favorite investments were net lease properties. Back in my private equity days, we would commonly target Aldi net lease grocery stores because they offered:

- A high initial cap rate of about 7%

- Steady annual rent hikes of about 2%

- Very long leases of 15 years + several 5-year extensions

- No landlord responsibilities, meaning that the tenant would pay for all expenses, including even the maintenance of the building

The Boulder Group

So to put it simply, these properties offered equity-like returns with bond-like safety . Even without any leverage, you could expect to earn a ~10% annual total return from the yield and the growth, and if you added some leverage to it, you could get your returns closer to 12-15% annually.

That's quite exceptional coming from an investment that's recession-proof, inflation-protected, and management-free.

We were especially interested in Aldis because we thought that the market was mispricing these properties. Aldi is a major German grocery retailer. Back in Germany, it is considered to be the "gold standard" of retail tenants. It has a very good reputation because of its scale, the nature of its business, and its track record of taking good care of its landlords. But in the US, few people knew about this, and Aldi was seen as a relatively small, foreign, private company with obscure financials. In Germany, these assets would have traded at a 5% cap, but we could buy them closer to 7-7.5% in the US and with better lease terms:

November Capital

To this day, I think that these properties offer some of the best risk-and-hassle-adjusted returns of the entire property market. You get high returns with highly consistent and predictable cash flow and it is management-free.

But there's one issue with net lease properties:

You would need $100+ million to build a well-diversified portfolio by tenant, sector, and geography. This simply isn't doable for most of us, and so it leaves us with REITs.

Unfortunately, during most times, these net lease REITs have been quite pricey. The market knows that net leases can be great investments, especially when combined with the REIT structure that provides diversification, economies of scale, and the ability to grow even faster via spread investing.

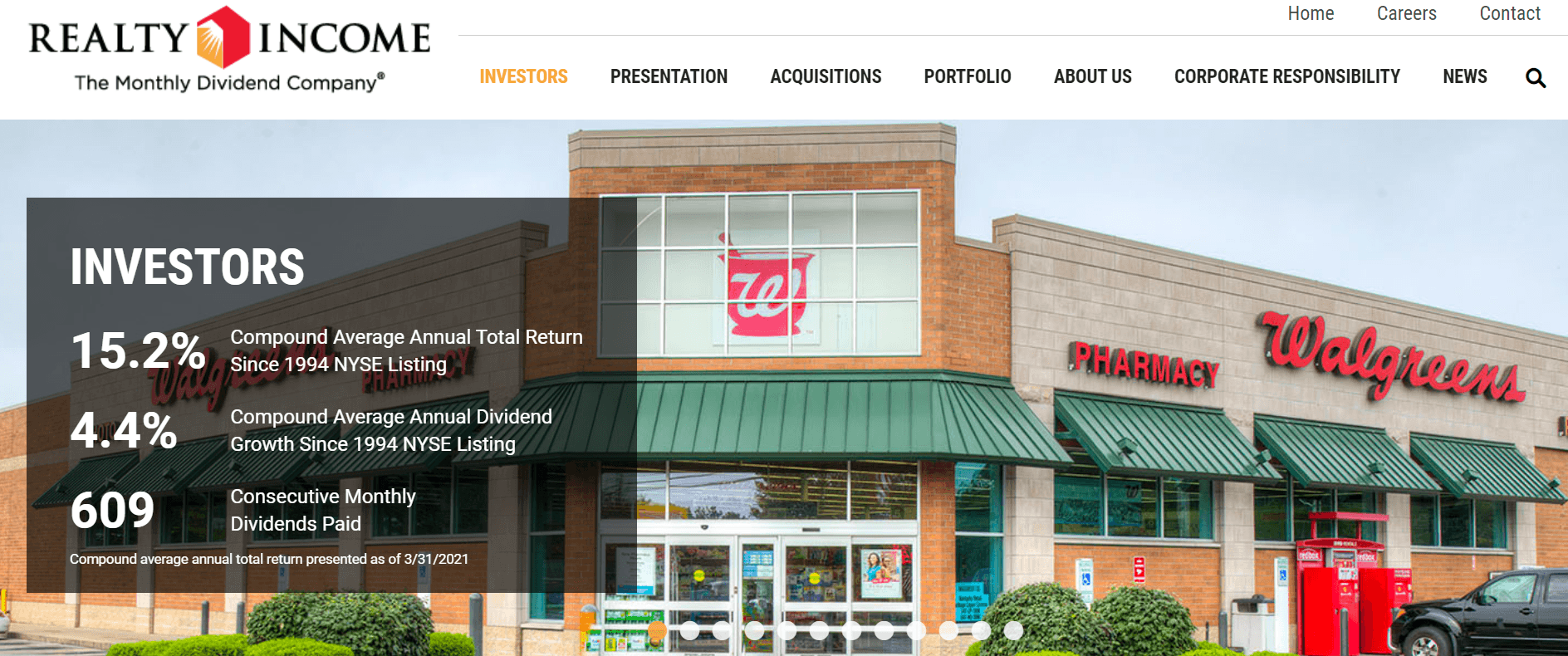

Take Realty Income ( O ) as an example. Its historical performance is a testament to how solid these properties can be. It has managed to grow its dividend for nearly 30 years in a row - all while generating a ~15% average annual total return. That's despite the dotcom crash, the great financial crisis, the pandemic, and the recent surge in interest rates...

{kind=link}

But today, these net lease REITs are heavily discounted.

Their income-oriented pool of buyers has dried up following the recent surge in interest rates. A lot of them would rather invest in a 5% yielding money market fund than a 5-6% yielding net lease REIT, which is perceived to be riskier.

And so with little demand for these REITs, their share prices crashed to historically low valuations:

This is an opportunity.

They are all now priced at low multiples and high dividend yields, despite continuing to grow consistently.

| Net Lease REITs |

| FFO Multiple |

| Dividend Yield |

| NNN REIT |

| 11.9x |

| 5.9% |

| W. P. Carey |

| 11.2x |

| 6.5% |

| Agree Realty |

| 14.4x |

| 5.2% |

| Realty Income |

| 13x |

| 5.7% |

| Essential Realty Property Trust |

| 14x |

| 4.7% |

| Netstreit |

| 14.9x |

| 4.9% |

| Broadstone Real Estate |

| 10.7x |

| 7% |

| Getty Realty |

| 14.4x |

| 5.7% |

| Four Corners Property Trust |

| 15.1x |

| 5.6% |

(Note that I did not include VICI or EPR because they are specialty net lease REITs)

But which is the best opportunity?

It is a tough question to answer because they are all quite attractive at today's prices and which you favor will heavily depend on your risk tolerance and what you are trying to achieve.

But there are three that really stand out right now in my opinion and these are NNN REIT ( NNN ), W. P. Carey ( WPC ), and Agree Realty ( ADC ).

Here is why:

- Realty Income is a great REIT and it is historically cheap, but its large size is likely going to slow down its future growth.

- Essential Properties Realty Trust ( EPRT ) is a fantastic net lease REIT to hold for the long run, but it has significantly outperformed its peers in the recent past and it now trades at a premium valuation, despite typically trading at a slight discount.

- NETSTREIT ( NTST ) focuses on class A net lease properties just like Agree Realty and also trades at a similar valuation. However, Netstreit has a high exposure to pharmacies at 17%, which is a riskier net lease sector, and it doesn't own ADC's ground lease properties, which we think are very desirable. Finally, ADC has had far more insider purchases in the recent past.

- Broadstone Net Lease ( BNL ) owns a diversified portfolio just like W. P. Carey and it is priced at a slight discount. We think that both are undervalued, but we think that it is worth it to pay a small premium to own the blue-chip: WPC. It has better leases, a lower cost of capital, and a long track record of excellence.

- Getty Realty ( GTY ) owns recession-resistant gas stations that are well-positioned to generate safe rental income for many years to come. However, this is a sector that presents significant long-term uncertainty and it is tough to predict how the move to Electric vehicles will impact these properties. This concentration on gas stations should warrant a lower multiple relative to its peers in my opinion.

- Four Corners Property Trust ( FCPT ) focuses on restaurants. Just like Getty, it is heavily concentrated and this presents risks. The rapid growth of food delivery apps and shadow kitchens will benefit some and hurt others. Unfortunately, FCPT is not well diversified by tenants either with over 40% coming from Olive Garden. All in all, a premium valuation does not appear to be warranted, especially given that its balance sheet is weaker than that of ADC and NNN.

Why NNN, WPC, and ADC Stand Out

NNN REIT is one of a few "blue chips" in the net lease REIT sector. It has managed to grow its dividend for over 30 years in a row, it has a fortress balance sheet, owns defensive properties, and should be able to grow by about 4% per year on average over the long run. Its unique strategy of doing sales and leasebacks with middle-market tenants arguably offers the best risk-to-reward of the entire net lease segment and NNN has perfected this strategy. Despite that, it is now priced at one of the lowest valuations in its sector, and its dividend yield is at its highest in over 10 years (with the exception of a brief period following the pandemic crash) at nearly 6%.

Today, it is priced at just 11.9x FFO, but over time, we think that it is likely to return to 16x FFO, and possibly quite a bit more if interest rates return to lower levels as we expect. This gives us the following expected return:

~6% dividend yield + ~4% FFO per share growth + ~10% annual repricing upside over the next 3 years = ~20% annual expected total returns.

{kind=link}

W. P. Carey is also considered to be a "blue chip" for the same reasons as NNN, but its valuation is not reflective of these qualities. Its recent decision to spin off its office properties into a separate REIT called Net Lease Office Properties ((NLOP)) has alienated a lot of investors and caused its shares to sell off.

Its forward dividend yield is expected to be around 6.5% (post anticipated cut) and that's despite earning most of its revenue from industrial net lease properties that enjoy CPI-based rent adjustments that are today resulting in sector-leading rent growth.

The REIT has some near-term growth headwinds, but those are only temporary, and as it gets passed those, it should return to ~5% annual growth in the coming years.

Assuming that its average growth will be just 3% per year on average over the next years and its FFO multiple expands to 16x FFO, we could again expect to earn roughly 20% average annual total returns:

~6.5% dividend yield + ~3% FFO per share growth + ~10% annual repricing upside over the next 3 years = ~20% annual expected total returns.

W. P. Carey

Agree Realty Capital is arguably the highest-quality net lease REIT. It owns Class A assets with mostly investment-grade tenants in superior locations and it also owns a growing portfolio of ground leases that generate potentially ultra-safe rental income. Moreover, it has one of the safest balance sheets in its sector with low debt and long debt maturities. Rightfully so, it trades at a premium to most peers, but we think that the premium should be even greater. Priced at 14.4x FFO, it does not have as much upside potential as NNN and WPC, but by getting to 18x FFO, it should also achieve near 20% average annual total returns in the coming years.

~5.2% dividend yield + ~5% FFO per share growth + ~8% annual repricing upside over the next 3 years = ~18% annual expected total returns.

Agree Realty Capital

For further details see:

3 Top REIT Picks For 2024