SPG - 3 Undervalued REITs To Buy

Summary

- REIT valuations have been hit hard over the past 12 months creating cheap valuations in certain sectors.

- REITs tend to provide higher yields due to their structure.

- Warren Buffett historically has preferred REITs over investing in physical Real Estate.

Real Estate Investment Trusts, or REITs, are a great way for regular retail investors to gain exposure to Real Estate. Here are a few reasons why REITs are easily accessible for any level investor:

-

You do not need to worry about a 20% down payment

-

You do not need any experience in real estate

-

No worrying about the hassle of difficult tenants or capital expenditures

If you want Real Estate exposure, REITs are a great place to start, plus they have proven to be one of the top asset classes over a number of decades.

Physical Real Estate has also proven to be a great investment as well, however, many wealthy investors, not just retail investors, have been growing their exposure within the REIT sector.

Even the Great Warren Buffett seems to prefer REITs over physical Real Estate. According to an article from Benzinga , "Buffett isn’t opposed to investing in real estate and has invested in several real estate investment trusts (REITs) over the years. However, he knows it makes little sense to get into the business of being a landlord. Buying and managing real estate is more of a business than it is an investment, and Buffett knows that his time is better spent choosing companies to invest in than it is running a real estate business."

Not necessarily a knock against owning physical real estate, but I think Buffett is essentially saying he likes the returns and the hands off approach more with REITs.

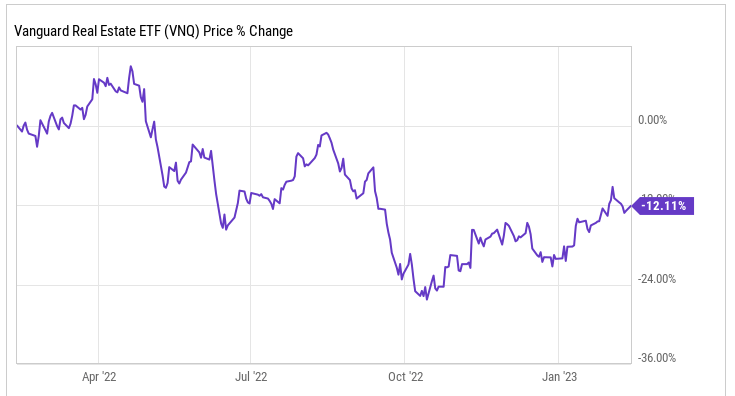

If you are new to REITs or looking to expand your exposure, now is a great time as the sector has been under pressure over the past 12 months. The Vanguard Real Estate ETF ( VNQ ) is down 12% over the past 12 months with the S&P 500 down only 6%.

{kind=link}

3 Undervalued REITs

Undervalued REIT #1 - Alexandria Real Estate ( ARE )

Alexandria Real Estate fits under the office REIT sector, but they are more than your typical office REIT. The company has a market cap of $28.6 billion.

We have seen a slew of businesses implement flexible work arrangements for employees or full fledged work from home options, which has put even more pressure on office REITs. Tenants have not needed as much space as they once did, so they are downsizing and the trend does appear like it will stick for the most part.

However, class A office REITs are still performing quite well because employers still want employees to come in person, so they are looking for some of the best properties with great amenities that will attract employees back to work in some capacity.

But again, this all relates to more traditional office REITs.

Alexandria is a leading owner, operator, and developer of collaborative campuses for life science, agtech, and technology companies in the nation’s top innovation clusters. That sounds like a mouth full but what it doesn't sound like is a traditional office REIT.

Alexandria Real Estate recently issued its Q4 and full year 2022 earnings that showed continued strength for the REIT.

Revenues grew 22.5% in 2022 with AFFO growing 8.5% to $8.42.

Since the company went IPO in 1997, you can see how Alexandria’s Total Return has surpassed that of blue chip names such as Walmart ( WMT ), Berkshire Hathaway (BRK.A) ( BRK.B ), and also out gaining major indexes like the Nasdaq, S&P 500 ( SPY ) and the MSCI US REIT Index.

{kind=link}

Alexandria maintains a strong balance sheet with $5.3 billion in liquidity available and 13.2 years left on a weighted avg in terms of outstanding debt with an avg weighted int rate of 3.53%.

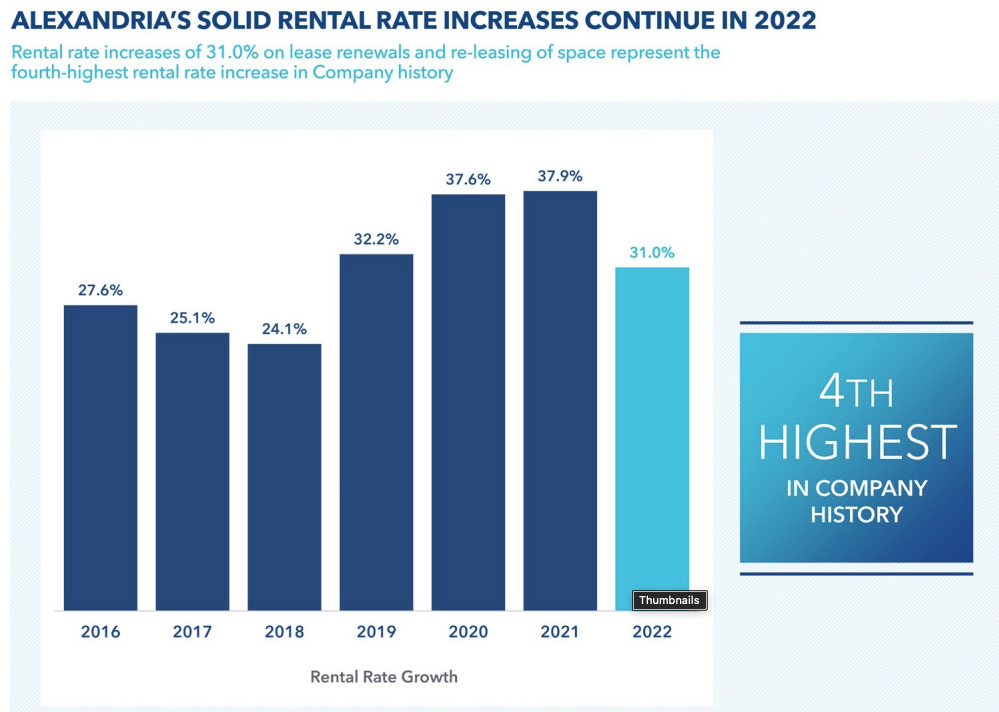

The quality of the company’s portfolio and strong demand is evidenced both by the high occupancy rate but also by the very strong rental rate increases we have seen the past few years. ARE saw 31% rate increases on renewals and re-leasing space in 2022, which was the 4th highest in company history, and the past 4 years.

{kind=link}

In terms of the dividend, ARE pays an annual dividend of $4.84 which equates to a dividend yield of 2.9%. Shares have a 5yr dividend growth rate of 6.1% and the REIT has increased the dividend for 13 consecutive years.

Looking at valuation, shares of ARE trade at a fwd AFFO multiple of 22.7x which is well below their 5-year avg of 27.3x. Higher interest rates have weighed on the stock price, but as we saw from their Q4 results, the company continues to excel regardless.

{kind=link}

Undervalued REIT #2 - Simon Property Group ( SPG )

Simon Property Group is the premiere mall landlord in the US, and a REIT that has been in my portfolio for a number of years. The size of the position has changed over the years, but SPG is again looking intriguing. Every time investors count them out, they always bounce back.

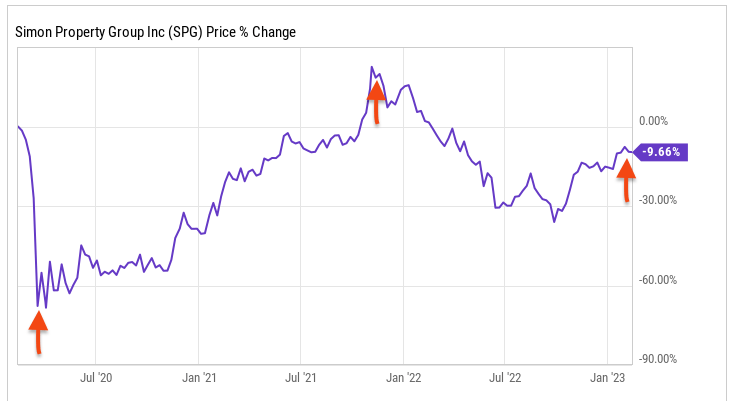

SPG currently has a market cap of $46.5 billion. The REIT was rocked at the start of the pandemic, falling over 60% in a short period of time as lockdowns were implemented, thus no one was shopping at malls.

However, looking at this chart you can see just how resilient this company and stock was as it rose past pre pandemic levels in 2021, but over the past 12 months we have seen shares fall yet again, down 12%, and still down roughly 10% over a three year period, giving investors yet another opportunity to add to this blue-chip REIT.

{kind=link}

Many continue to think malls are dead with the rise in popularity around e-commerce. E-commerce is growing each and every year, undoubtedly, but there is still a place for retail real estate properties.

Similar to what we discussed with ARE, SPG is not a typical mall REIT. Instead, they are the premier mall REIT. Simon Property is made up of Class A malls, which is a classification based on their retail sales per square foot and over the years, SPG has remained an A or A+ rated portfolio. The malls that are dying are mostly C rated or lower malls.

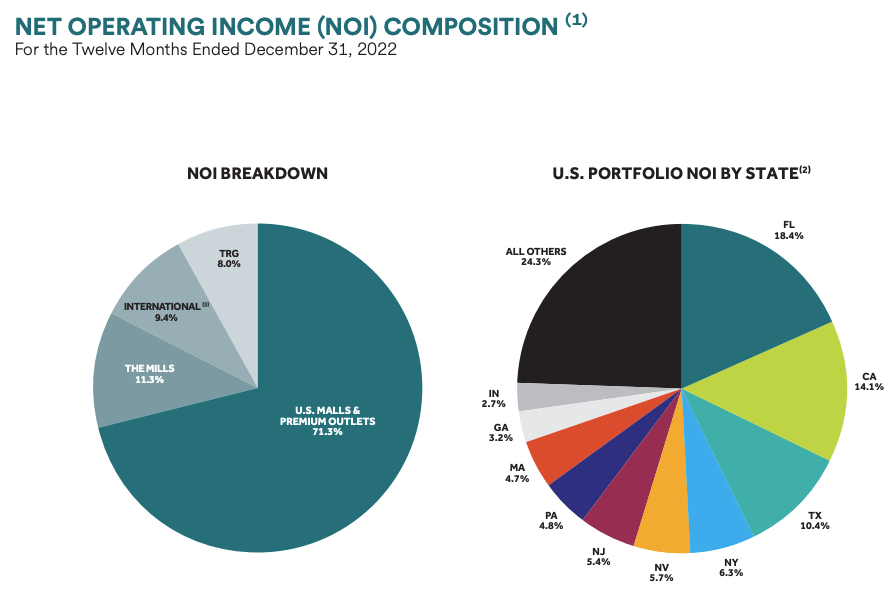

Consumers still like to shop in person and use malls as entertainment or meeting place, especially the best malls in the country, which are Simon Property Group properties. The company has a large footprint across the United States, with over 40% of the company’s NOI coming from the states of Florida, California, and Texas.

{kind=link}

71% of their NOI comes from US Malls and Outlets, but they also have an international presence that makes up nearly 10%. In 2022, the company saw their portfolio NOI grow 5.7% with the domestic property NOI growing 4.8% year over year.

Here is a look at SPG's top in-line tenants as well as their top anchors. As you can see, only one single tenant accounts for more than 1.7% of annual base rent and that is The Gap (GPS).

{kind=link}

So no real single tenant exposure that truly threatens SPG, which can give investors piece of mind, whereas other landlords that have large exposure to troubled retailers, could be more in jeopardy, not the case with Simon Property.

For years, SPG has been known to have a Fortress Balance Sheet, and that continues to be the case as of the end of 2022. The company maintains a fixed charge coverage of 4.8x with 6.7 years remaining on their debt on weighted terms and a very low payout ratio of less than 60%, suggesting the dividend is plenty covered.

Speaking of the dividend, SPG currently pays an annual dividend of $7.20 per share, which equates to a high dividend yield of 5.8%. The company had to cut the dividend at the start of the pandemic but has been aggressively increasing it ever since. Investors saw a 26.9% dividend hike in 2021 and a 9.1% dividend hike in 2022.

The valuation looks very intriguing here with an 11.3x forward AFFO multiple, which lags their historical average of 13.0x.

{kind=link}

Undervalued REIT #3 - Global Medical REIT ( GMRE )

Global Medical REIT is a net-lease healthcare REIT focusing on medical office buildings within smaller markets. They have cut out their own little niche within specific markets that are showing strong demand.

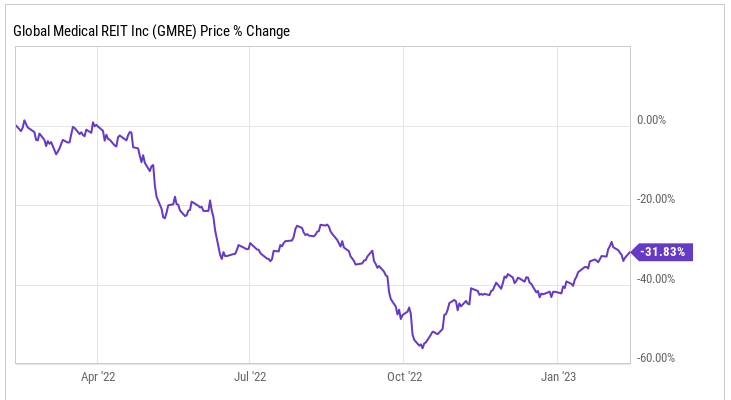

GMRE has a current market cap of $730 million. Over the past year, shares are down over 30%, trading between a range as low as $7 and as high as $17.

{kind=link}

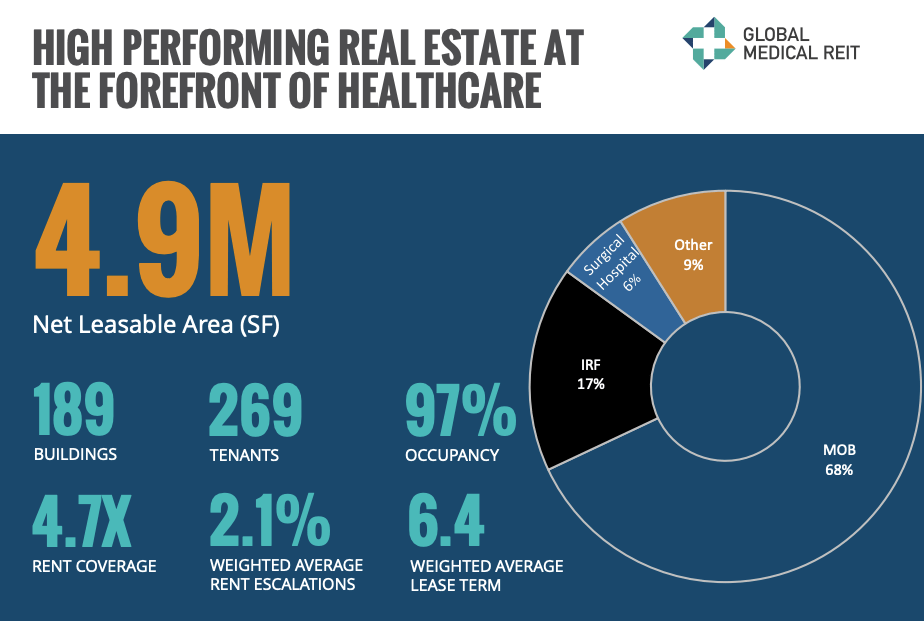

The company owns 189 properties that amounts to nearly 5 million square feet of leasable space. As of Q3 they had 97% of their space occupied. GMRE leases these properties out to 269 tenants with 6.4 weighted average years remaining on existing leases. This is a little lower than I would like to see, so something to keep an eye on.

{kind=link}

With GMRE focusing on secondary markets, it not only results in less competition from larger healthcare REITs or institutional buyers, but it also allows for larger spreads. On the flip side, the risk lies within the quality of the tenant.

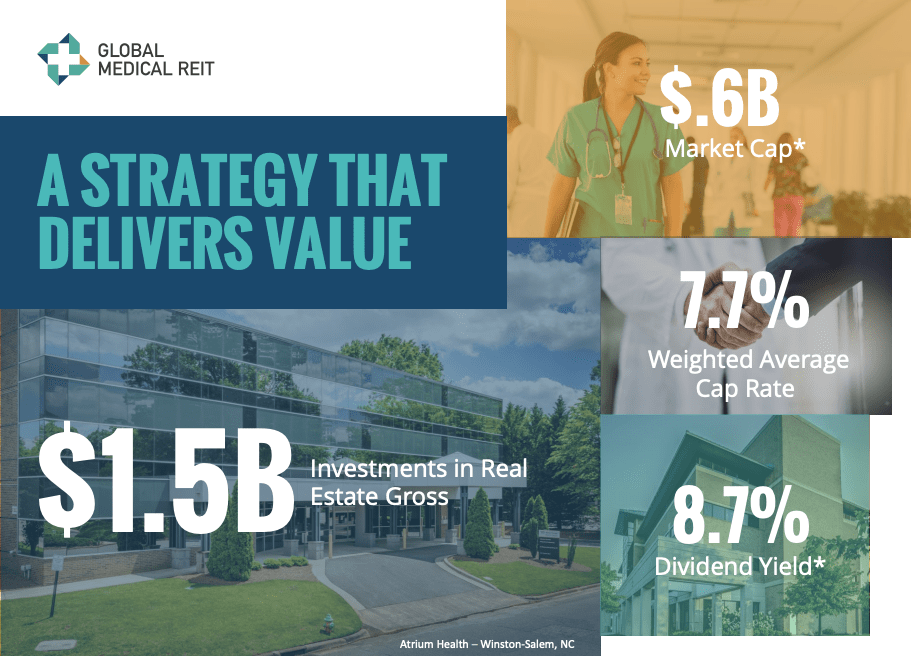

This slide here was from the company’s Q3 presentation, as we are still waiting for the company to report Q4, but as of Q3, the company had a 7.7% weighted average cap rate, which is higher than the average 5% cap rate found in major markets for similar properties.

{kind=link}

Cap rates can be thought of as the percentage of NOI compared to the property value of that particular asset.

Looking at the sector, whether we fall into a recession or not, as long as the landlord works with solid tenants, the healthcare industry is rather recession-proof in many ways.

The health care continues to evolve and so do its clientele. According to WebMd, they took a survey that found 90% of Americans age 50 and older want to age in place and 65% of seniors between the ages of 60-70 want to live independently, meaning not in a senior living facility. This means there is more of a need for visits to their doctors which means a need for doctors offices like ones owned by GMRE.

GMRE's balance sheet remains in good shape, with a weighted average interest rate of 3.9%. It also maintains a healthy fixed charge coverage ratio of 3.4x, sitting well above the minimum 1.5x required by its debt covenants.

This suggests the company’s dividend is well covered. The company pays an annual dividend of $0.84 per share which equates to a high dividend yield of 7.7%.

The valuation looks quite intriguing as the company trades at a forward P/AFFO multiple of 10.9x. Over the past 5 years shares have traded closer to 14.7x.

{kind=link}

Investor Takeaway

All three of these REITs appear to be trading at a discount to where they historically trade. If you are a long-term investor on the hunt for solid companies trading at reasonable valuations, these three REITs could be worth a look.

All three are unique in the fact they have solid businesses and properties, but their sectors are under pressure.

Alexandria Real Estate is considered an office REIT, but their properties are more for pharmaceutical companies that are much different from traditional office.

Simon Property Group is a blue-chip REIT with some of the best properties around, but the mall and retail sector in general have been lagging.

Global Medical is a newer REIT to the public markets, thus the smallest on our list, but they have some great healthcare properties in secondary markets.

Comment below what you think of these three REITs.

Disclaimer: This article is intended to provide information to interested parties. I have no knowledge of your individual goals as an investor, and I ask that you complete your own due diligence before purchasing any stocks mentioned or recommended.

For further details see:

3 Undervalued REITs To Buy