QQQ - 3-Year VIX Low: 7 Reasons Why Even Lower Levels Likely Ahead

2023-06-22 18:49:41 ET

Summary

- The S&P VIX Index is known to spike during fear and panic, but market efficiency and safety have been increasing, which should limit the upside.

- The rise of more precise tools for hedging risk contributes to a subdued fear index.

- Despite initial bearishness, the S&P 500 rally and positive economic data indicate the potential for a soft landing, meaning the VIX likely stays subdued.

Sometimes the early bird gets the worm, but sometimes the early bird gets frozen to death.

Myron Scholes.

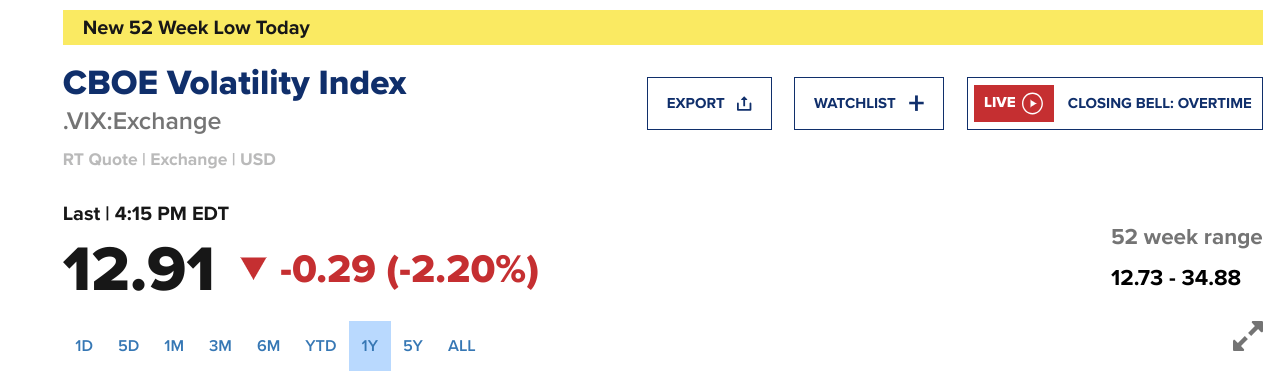

Well, the VIX closed in the $12 handle! If I were my old self, I would have seen market action recently and built a position in the S&P VIX Index ( VIX ) as it danced just above multi-year lows over the last few weeks. After the amazing runup in markets over the past months, the volatility seemed enticingly cheap. The fall of the fear index in the last month has been precipitous; all the while, people have been talking about how cheap volatility is.

{kind=link}

If you're looking at it from a technical analysis perspective, I'm sure you saw a huge opportunity. Or at least one could be seen if you squint right. But I believe there are idiosyncratic and fundamental factors restraining the VIX, and since I realized this, my portfolio has been doing a lot better.

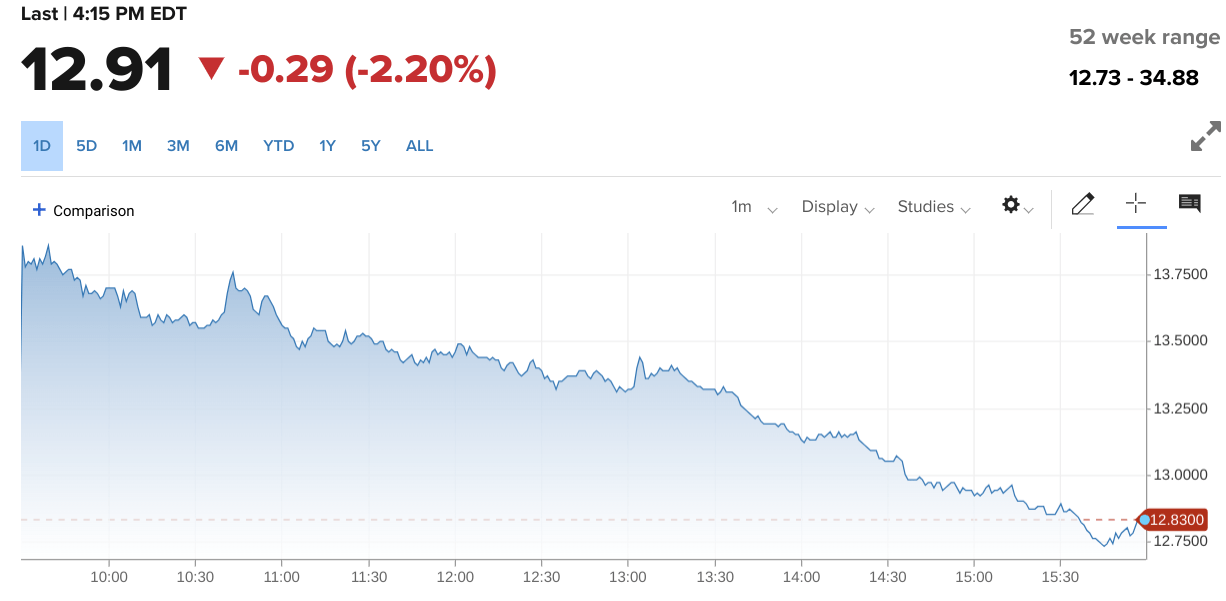

While I expect there to be short-term bounces, I don't expect them to be sustained or very consequential, and I think we will see new lows for the VIX this year. It reached a new post-COVID low today as of the close.

{kind=link}

There are many short and long-term drivers that converged for this to happen. Many folks were also likely expecting Powell to come out extra hawkish at his House Financial Services testimony. Instead, the opposite occurred , and markets responded by basically calling the Fed's bluff on two more hikes. Those hoping for a market pullback after the five straight weeks of gains were validated, kind of.

However, if you thought an accompanying VIX spike would be the way to play it, your portfolio had to be taken out on a stretcher.

The market dropped yesterday, as many would have thought, but curiously the VIX dropped nearly ten times as much ! I believe I know why these anomalous days keep occurring and why despite the panic in October 2022, the infamous fear index didn't even clear $35. What's keeping the VIX down? And will it stay down? I think the answer to the second question is yes, in the short to medium term.

{kind=link}

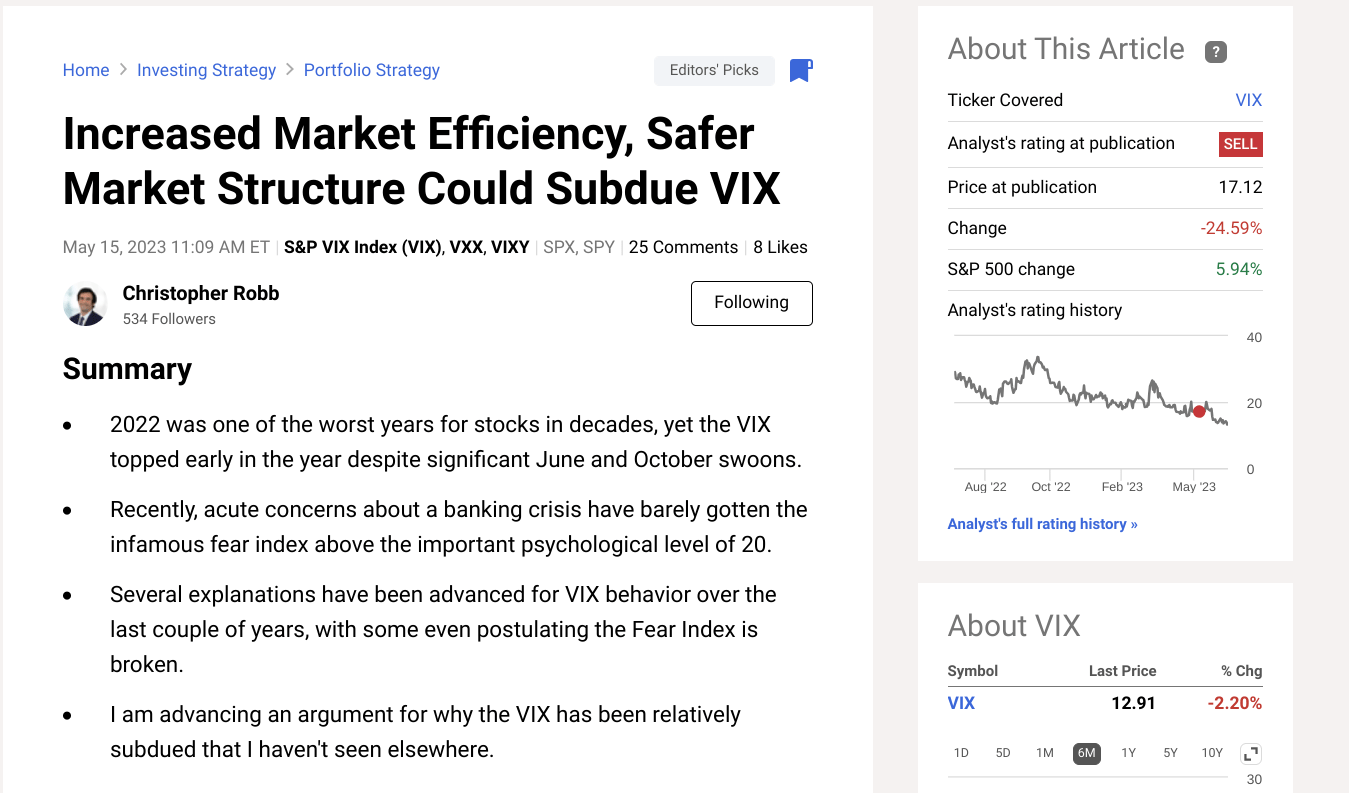

On May 15th, I published an article called " Increased Market Efficiency, Safer Market Structure Could Subdue VIX." The article argued that the VIX wasn't broken but was becoming somewhat obsolete due to a number of factors, including the rise of more precise hedging strategies and the successful implementation of market circuit breakers during COVID. To paraphrase a key point of the article, I'll quote it directly:

So what seems like a paradox of more risk, lower VIX actually makes perfect sense given the relatively blunt and inconsistent nature of using the VIX as a practical hedge and the added stakes of hedging correctly. The bluntness is only exacerbated by the necessary limitation of upside created by market circuit breakers, which historical observations now suggest are successful in their aim to reduce the exact cascading sell-offs that result in the largest upside for the fear index.

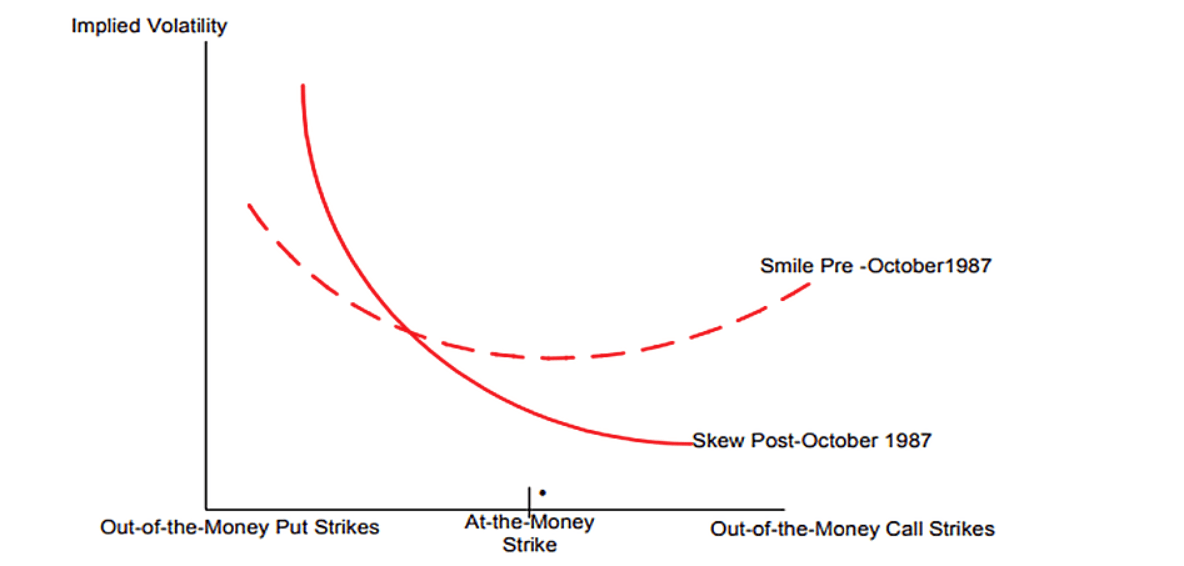

To provide a refresher and to ensure you can get a visual to understand my theory, I'm going to use the same graphic I used last time. In 1987 the market dropped so much more than was considered possible that it resulted in a permanent skew to the left, effectively meaning it has been more expensive to hedge against downside moves than upside ones ever since the infamous volatility smirk.

{kind=link}

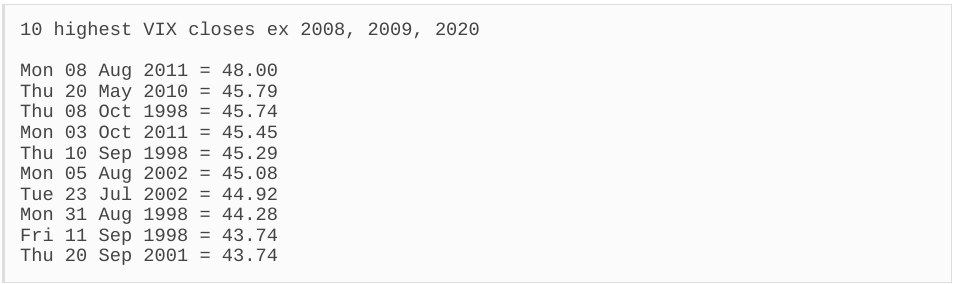

So, since the unprecedented drop of Black Monday in 1987, there haven't been any single-day drops that approach its severity. Given that COVID is arguably the largest threat to economic activity in post-industrial human history and the fact that the market didn't exceed the drops of 1987 suggests it may have been a result of inefficient markets. When you look at the highest spikes for the VIX's predecessor, the VXO, I think it also supports my thesis.

Macroption

In other words, since that drop is made a lot less likely by successful circuit breaker solutions, the curve should have shifted somewhere between the two curves above. To think about it logically, consider this: the market made the opposite mistake it did in COVID as it did in 1987.

Instead of thinking such a large drop wasn't possible, consensus didn't think such a sharp and quick rebound was possible, given the gravity of the situation.

Just think of it this way, reforms have been made, and markets have become more efficient since the events where the highest spikes occurred, reducing the chances of a repeat.

So the smirk shifted back toward a benign smile. However, the smirk is still intact, though not as steep, since avoiding drawdowns is so important for performance for many institutional investors, meaning there's still a premium for downside protection, and there likely always will be.

When the circuit breakers were successful in mitigating severely adverse outcomes and the type of cascading sell-offs that made the VIX spike the most, the market received new information. Many speculated that circuit breakers could actually exacerbate a selloff, and when they are poorly designed, this can certainly occur. But this didn't occur during COVID.

{kind=link}

The Volatility Index is known for spiking during times of fear and panic. I suspect if you're using COVID spikes and those from before COVID as a frame of reference, you'll be continually disappointed. This removes one of its most attractive features when using the instrument to insure against rare market outcomes.

I don't say this as a know-it-all or someone who hasn't been when you are if you've been slammed on the VIX. My insight on the VIX has been steeply purchased; I may have incinerated a higher proportion of my income on long VIX trades than perhaps anyone alive. I'd wager I'm in the top 2% at least.

But let's get back to the peculiar behavior of the infamous VIX fear index. Let's take yesterday, for example. The market has had an incredible run-up, with some mega caps up triple digits on a YTD basis. The bears were foaming at the mouth to short. Now, if you got SPX put options that were played tight around the strike, you probably did alright in the last couple of days.

{kind=link}

If you tried to play a VIX call, I'm guessing you incinerated capital faster than a Silicon Valley venture bro in 2022. Again, not a slight. Ask me how I know! How do I know?

Firstly because I've done the same many times and secondly, because the VIX is a leveraged instrument, and it plummeted yesterday almost ten times more relative to the drop in the S&P 500 (SP500). That could certainly mess up a trader or risk manager's day, given that the normal course of things should be the reverse...

{kind=link}

It spiked earlier in the day today (June 22nd) after yesterday's significant drop. But then it began losing steam. This is possibly indicative of a return to the buy-the-dip regime that was so prevalent in the bull market that occurred in the wake of COVID.

Not Your Father's VIX

But this isn't your 2010s VIX or your financial crisis VIX. I can't stress that enough! The level of efficiency and safety in markets has been steadily increasing over the years. This fact is what led me to postulate a little over a month ago that the VIX was a SELL and that, beyond that, changing dynamics in markets, like the rise of more precise tools for hedging risk, would contribute to a subdued fear index.

{kind=link}

Since I made the call on the VIX, the index has declined by nearly 25%! It was near a 52-week call at around $17 when I made the call. Since my bearish call, the VIX has hit its lowest level since January 2020 and then got even lower today!

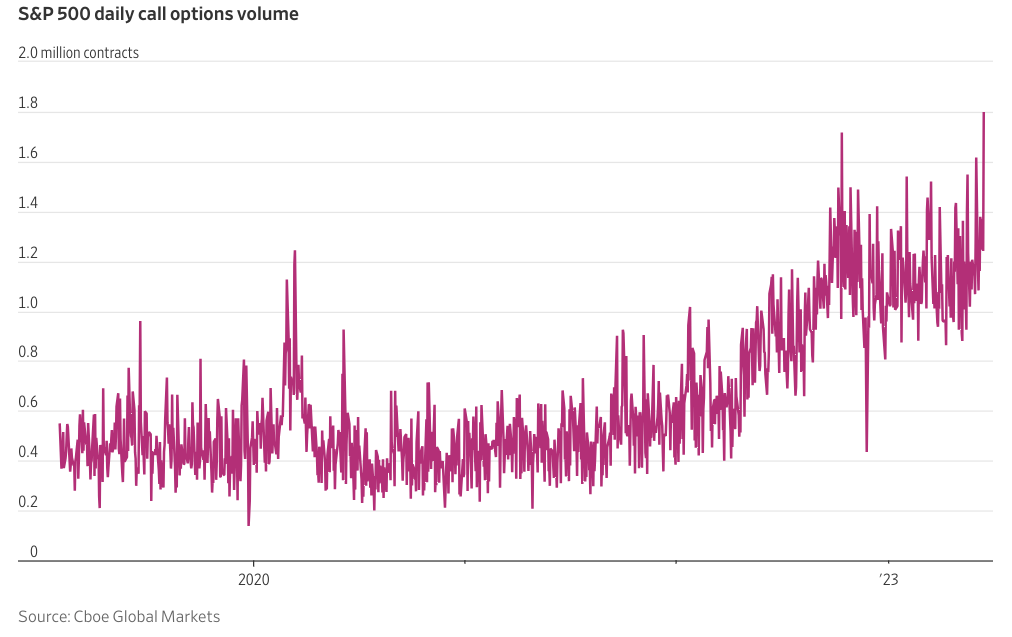

Furthermore, the VIX spikes when demand for S&P 500 Index (SPX) calls falls far below that for SPX puts. Recently, the demand for calls has been historically high , which can be a sign of further price gains. Of course, it can have a contrarian bearish value at times as well.

{kind=link}

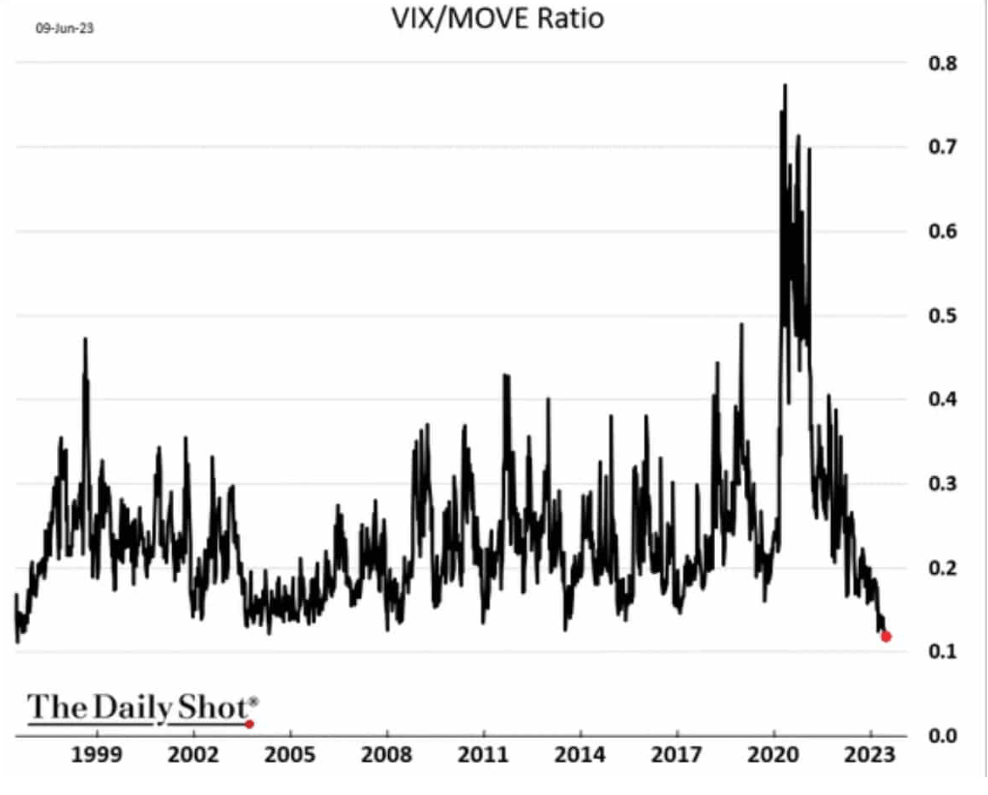

The VIX measures expected volatility for stocks, and the MOVE Index measures volatility in fixed-income markets. I pointed out the divergence in my last VIX article as evidence that the suppression of the VIX may be more artificial in nature rather than reflecting tranquil times. That divergence has only increased since.

{kind=link}

The divergence of the bond market volatility versus stock market volatility suggests to me that the VIX suppression has to do with specific factors to its calculation and events or changes that may have affected the underlying demand for instruments used in that calculation. These factors will continue to suppress the VIX, but not the volatility itself.

However, now I also believe the causal suppression of the VIX I previously noted is going to be exacerbated by an emerging bull market, and I will give very actionable and specific recommendations in the conclusion. Look at this illuminating chart from the Wall Street Journal article Why Are Markets So Calm? It's Revenge of the Quant Funds by Caitlin McCabe . As you can see, the elevated call buying seems to coincide with the significant decline in realized volatility in 1H23.

{kind=link}

There's been a marked decline in volatility. While it may be tempting to think some mean version backup should begin, I think it's more likely that this is the beginning of true mean reversion to more normal historic levels, particularly since we've had two major black swan events in the last fifteen years that saw the lion's share of the highest VIX spikes. My friend @SethCL (Seth Golden, a veritable VIX master) also makes a fascinating and highly relevant point below:

{kind=link}

In more normal periods where the integrity of the global financial system isn't in question or a pandemic isn't threatening to inundate global healthcare systems, the potential for VIX spikes in terms of the terminal VIX price before reverting lower is much less, and given the idiosyncratic drivers that I've theorized are suppressing the VIX, I am doubling down and suspect:

1. The VIX will remain suppressed.

2. Spikes will be relatively meager compared to previous cycles; I suspect nothing much above $25 for the next few months. (Remember the recent banking crisis and debt ceiling only got it just $20).

3. Hedging will likely be more effective with more precise instruments.

TO CLARIFY: I AM NOT SAYING, 'DO NOT HEDGE AGAINST VOLATILITY,' I AM SAYING, 'USE MORE PRECISE FINANCIAL INSTRUMENTS TO DO IT!'

Seven Reasons Why I Suspect VIX Will Remain Low

In my opinion, there are a number of things contributing to a suppressed VIX and suppressed volatility. There has been a lot of speculation on what caused the VIX to be suppressed, and I think the first item on my list is a cause of a lot of what other folks have been observing.

- When the VIX gets low, the imprecise nature of the index is exacerbated since strikes are at the dollar level and absolute price movement is a lot less. Record call buying likely compounds the effect of it already being low, and bull markets have been known to pin the VIX low.

- One of the consequences of the increasing efficiency of markets is also increasingly efficient derivatives across a number of metrics, including expirations. 0DTE options are an example of market efficiency increasing, which results in less demand for the SPX futures used in VIX calculation.

- The Limit-Up, Limit Down rules for when trading will be ceased on individual stocks permit much more downside to be captured than at the market level. Single-stock volatility and rolling corrections through different sectors have encouraged more precise hedging strategies at the expense of the VIX.

- Quant trading has taken a front seat in driving the market as many investors have sat on the sidelines. Fundamental investors and quant investors have diverged more than at any time since before COVID.

- There are increasing signs that the economy may avoid a recession, including the recent June economic projections from the FOMC. Strength in housing starts and homebuilders smells of an early expansion.

- There is a ton of money still on the sidelines that could be dragged in as short squeezes occur. Retail is getting dragged back in on AI enthusiasm, and the US consumer's resilience has continually surprised to the upside.

- There are a lot of indicators suggesting recession, but there's also a lot of anticipation. When you're tightening your belt and recession doesn't come, that means you've expanded margins in many cases. The declining dollar and a diplomatic thaw with China could result in better-than-expected earnings.

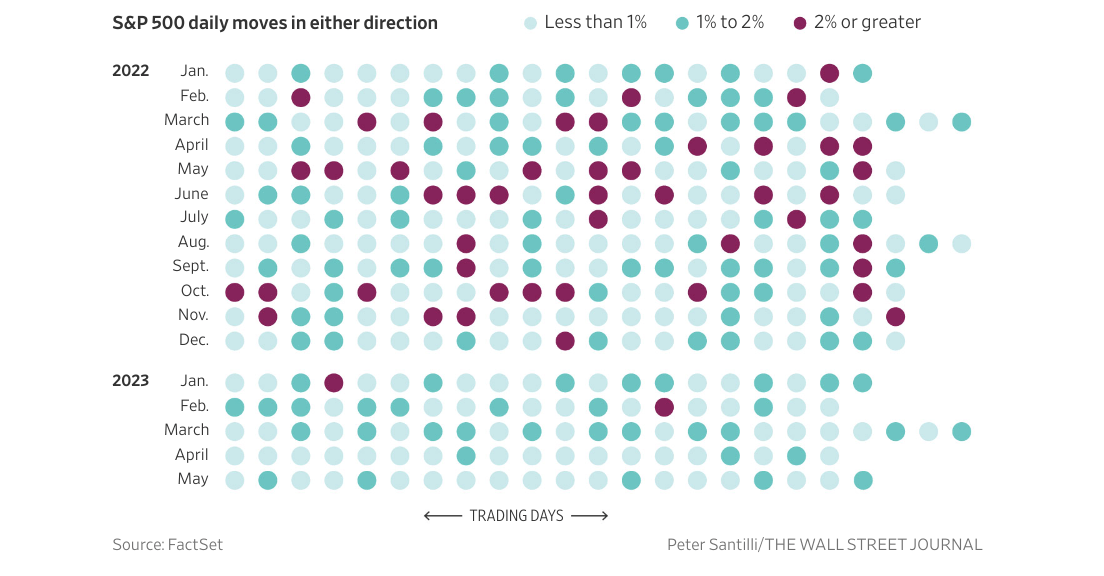

There will be some healthy pullbacks and minor VIX spikes, but not far above $20-$25, in my opinion, at least barring the emergence of a black swan risk that the market has underpriced significantly; I'd say we're exceptionally well-positioned to climb the wall of worry in this young bull market. Yes, that's right. Technically we're 20% above the October lows, and so the young bull has begun in earnest.

Risks and Where I Could Be Wrong

The Bears have been champing at the bit as the S&P 500 glided about 4,400. I was much more bearish and cautious at the beginning of the year myself. Still, the momentum of this rally as well as positive economic data, is making me optimistic about the potential for a soft landing.

However, sometimes the consensus is correct, and given that there's a flock of ominous black swans stalking the market, I certainly could end up with my foot in my mouth.

Goldman Sachs

Any of the following risks could result in the cascading sell-off and ubiquitous fear and uncertainty that cause the highest VIX spikes. But my sense is that any risk we face, other than the very extreme ones like nuclear war, wouldn't have as profound an effect on the economy as synchronized global economic shutdowns and millions of pandemic deaths. Still, the below risks could all result in my thesis being proven wrong:

- Escalation in Ukraine or Taiwan.

- Fed Policy Error.

- Banking Crisis Worsens.

- Return of Inflation.

- CRE meltdown.

- Write-downs of Private Assets.

Relative to the nightmare we just faced, which is causing the bearishness via recency bias, much of the worst has been priced in. But unforeseen risks can always derail even the soundest market analysis.

Conclusion

Bull markets are born on pessimism, grown on skepticism, mature on optimism, and die on euphoria.

John Templeton.

There are a lot of complicated arguments that some might consider highly technical regarding my theory for why the VIX is relatively suppressed. However, there's also a very easy way to say it that compliments my thesis.

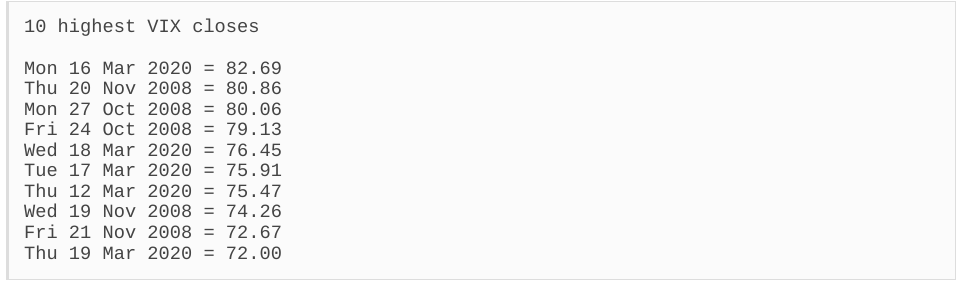

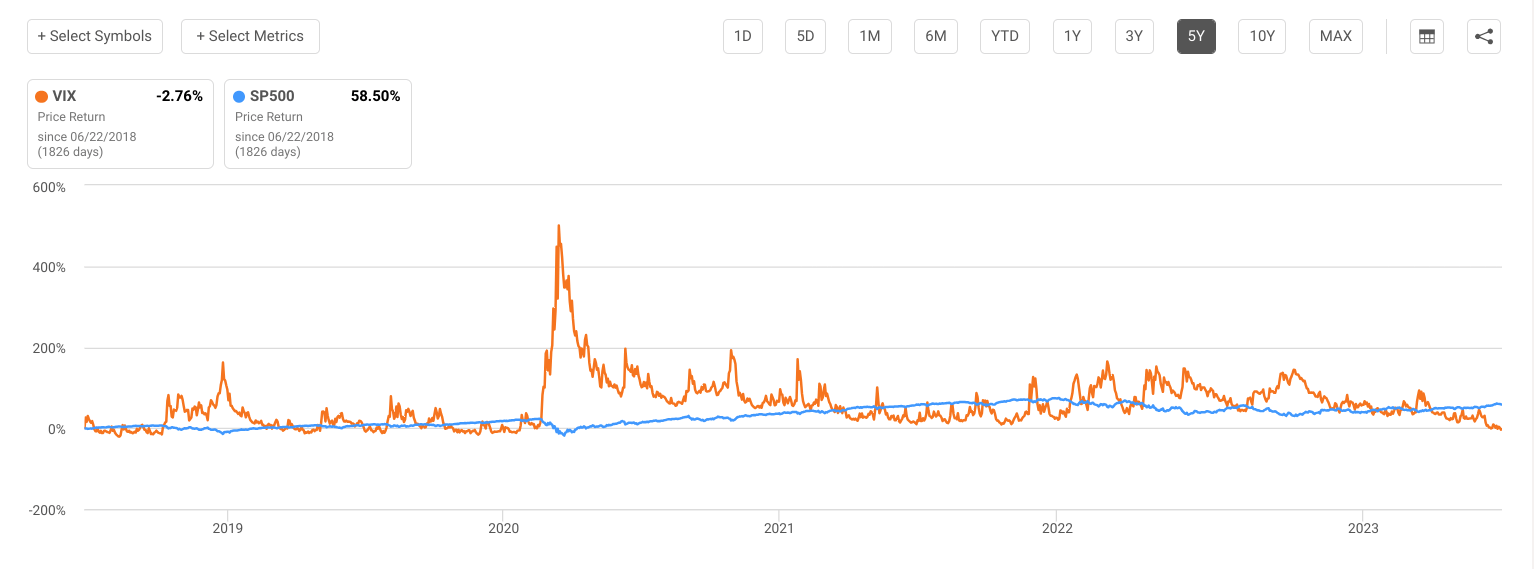

The fact the VIX's highest levels were almost exclusively concentrated in the last two crises means that it's quite likely we will get more subdued spikes by nature of how outside the norm these last two crises were. Hopefully, they weren't black-necked white swans (a risk term I coined). This is particularly true given that we now have officially entered a bull market by eclipsing 20% of the October highs.

{kind=link}

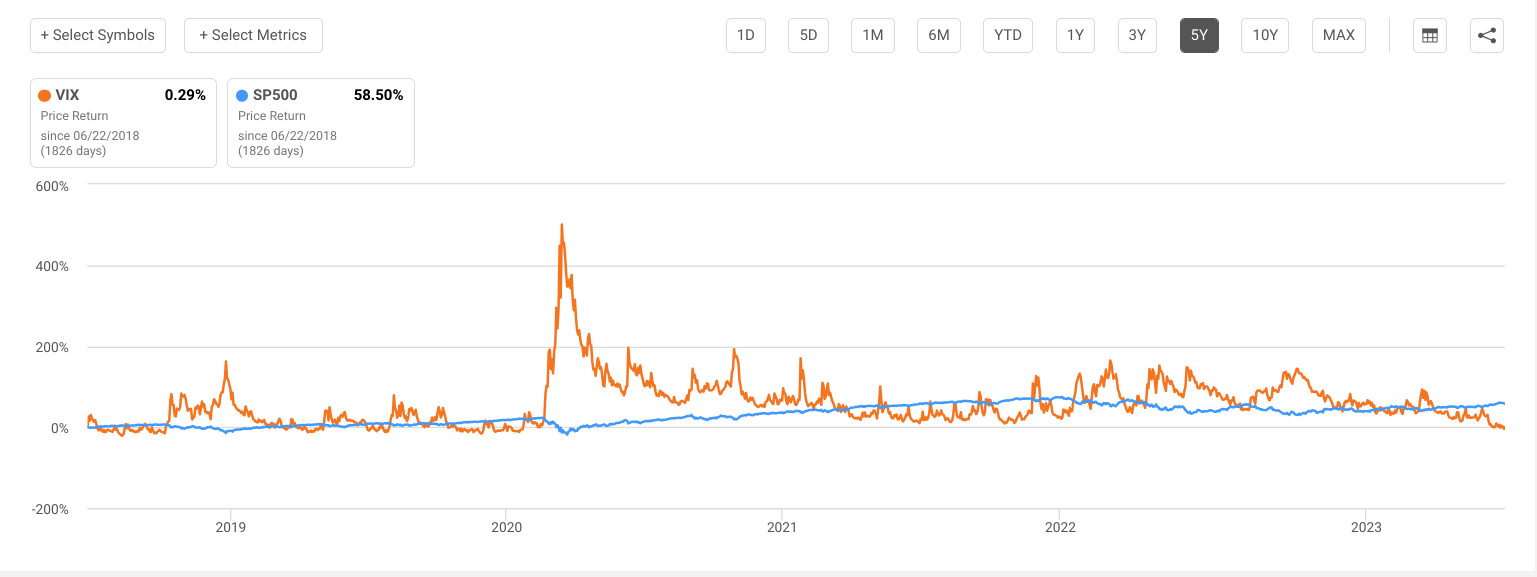

This is, of course, a technical definition, and it could possibly be reversed in a big way if a low-probability risk comes to fruition. However, I think since the market just faced the largest threat to the post-industrial economy ever and made it through, every economic risk we currently face is relatively subdued compared to that extraordinary event. The VIX's action in the last five years seems to confirm this.

{kind=link}

{kind=link}

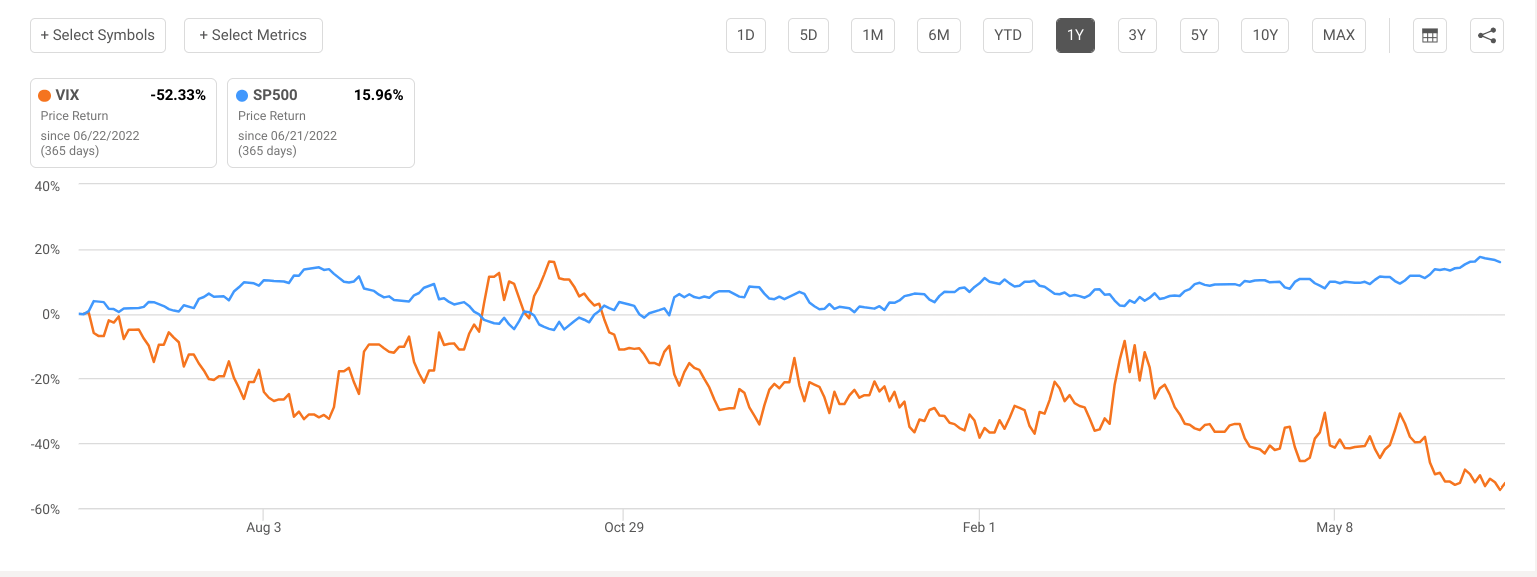

When you look at the VIX versus the S&P 500 in the last year, the relationship I'm talking about comes into pretty stark relief. There are a number of things that can cause the VIX to stay suppressed once a bull market starts. There's mounting evidence that some of these things have begun to occur.

{kind=link}

I think there is a combination of factors weighing on the VIX, both the idiosyncratic factors caused by increasing market safety and efficiency and, more recently, the animal spirits that are beginning to take hold as we enter a new bull market. You can see above that the spikes you probably remember from the last two crises are actually out of the norm.

That being said, we face very sobering risks, and I do not discourage anyone from not hedging against them. However, I think the proliferation of hedging instruments means you have a lot more precise options that can capture more alpha than the clunky VIX. Some of the instruments I'd recommend are:

- Equity options using either short (obligations) or long (rights) strategies, but just hedging equity positions directly with puts or calls or multi-leg strategies.

- VIX ETFs can often provide a more tailored exposure or exposure to a different set of expirations than is captured by options on the main index.

- (ONLY FOR HIGHLY EXPERIENCED OPTIONS TRADERS WHO MIND THEIR GREEKS!!!) 0dte options can be considered controversial, but given that the Fed is so data-driven and that volatility around impactful releases can be sharp and short, these instruments that expose you pretty purely to price movement can be a cheap and effective way to hedge against nasty short-term moves!

I think a lot of market participants have figured this out, and this might explain why when there's a key catalyst like yesterday's Fed Chair testimony in Congress, the VIX actually goes down. This is similar to the concept I discussed in my last VIX piece of why the index goes down in advance of volatile earnings seasons.

It's all about the spike (picture for article), and there are several things that seem to be chopping the tails off of SPX options used in the VIX calculation or diminishing the kurtosis. This is the crux of why I think the VIX will become increasingly less useful as a hedge relative to alternatives. The price will reflect this, and these dynamics will remain a drag on the potential upside in my opinion.

I hope this article has been helpful for the volatility hounds and for students of the game that never ends: the market. I am always open to directly discussing my VIX theory with interested parties.

If you think I'm incorrect, I will welcome any critique that helps advance our collective understanding of volatility. Thank you for reading!

For further details see:

3-Year VIX Low: 7 Reasons Why Even Lower Levels Likely Ahead