AROW - 4 Banks Stocks To Buy In April 2023

2023-04-10 07:19:19 ET

Summary

- We discuss four community banks with low valuations and decade-high dividend yields.

- The stock have at least 10 years of dividend growth and solid dividend safety.

- The four stocks are undervalued or fairly valued relative to their historical P/E ratio ranges.

- The four banks stocks are Arrow Financial, Bank of Marin, First of Long Island, and Washington Trust.

The turmoil in the banking sector caused retail and institutional investors to sell almost all financial stocks. However, they were indiscriminate, selling good bank stocks with little exposure to cryptocurrency and tech startups. Even regional banks with better asset and loan quality were sold off. As a result, early 2023 is an opportunity for investors to gain exposure to banks at low valuations and high dividend yields. Some regional and smaller community banks are valued like the worst months of the COVID-19 pandemic and even lower.

The four bank stocks the market has punished but are solid choices are Arrow Financial ( AROW ), Bank of Marin ( BMRC ), First of Long Island ( FLIC ), and Washington Trust ( WASH ).

Criteria for Selection

In our analysis, we look at three initial criteria in a screener. The bullets list what we need.

- Stocks in the banking industry.

- A 10-year or more dividend growth streak.

- A 4.5%+ dividend yield.

- A payout ratio of less than 65%.

- A price-to-earnings ratio (P/E ratio) less than 15X, below the value of the S&P 500 Index.

- A Dividend Quality Grade of B or higher.

This results in a list of 24 stocks. To further narrow the list down, we add two more criteria.

- We also require the banks to operate in different geographic regions.

- Lastly, we look at the asset and loan quality.

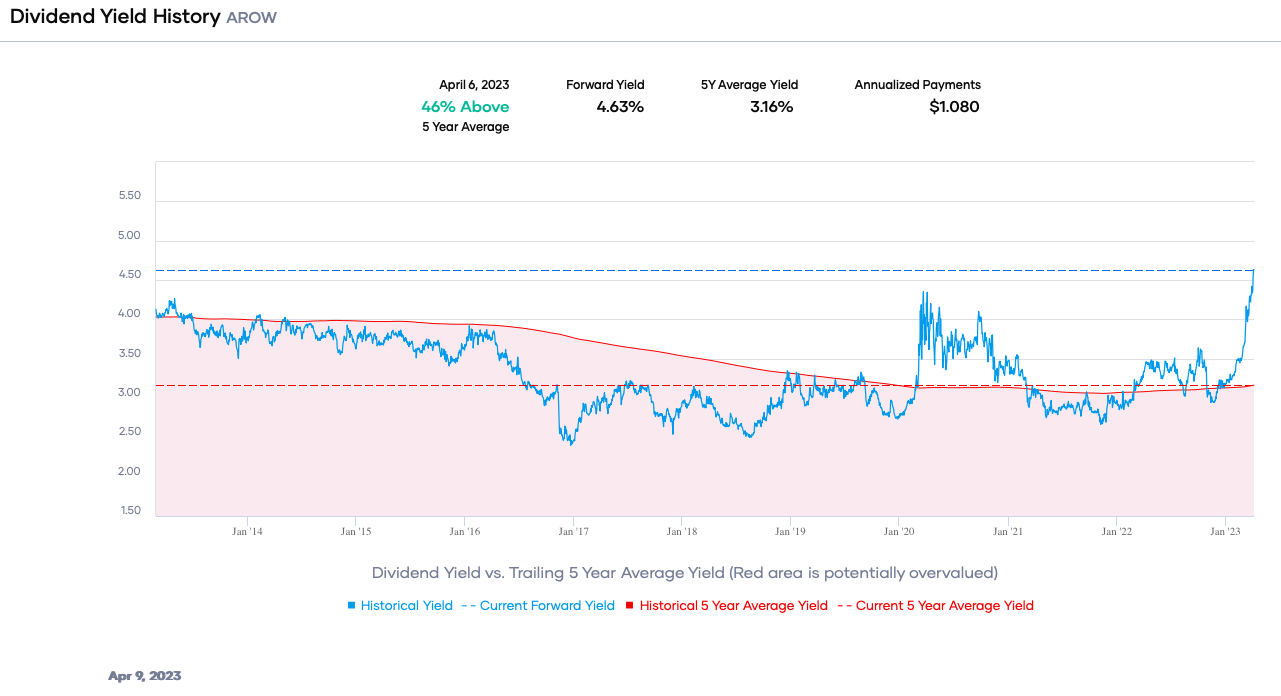

Arrow Financial

The Arrow Financial Corporation is a bank holding company offering consumer and commercial banking, wealth management, and insurance. Arrow operates through subsidiaries, including Glens Falls National Bank and Trust Company, Saratoga National Bank and Trust Company, and Upstate Agency. The bank is a small community bank operating in upstate New York. The market capitalization is only about ~$386 million.

Arrow is attractive because it is far from Silicon Valley and makes money the old-fashioned way off the net interest margin [NIM]. It has little exposure to tech startups and cryptocurrencies. But investors sold the stock regardless, pushing the valuation down and yield up.

But Arrow is growing because of the semiconductor industry in upstate New York. The firm has approximately $4.0 billion in assets, $3.0 billion in loans, and $3.5 billion in deposits. But asset quality is solid, with net loan losses at 0.08% and non-performing assets at 0.32%. For perspective, the national averages are 0.56% for non-performing loans [NPLS] and 0.30% for non-performing assets [NPAs]. In addition, Arrow is well-capitalized based on regulatory standards.

The dividend yield is ~4.63%, at a decade high and 1.5 percentage points more than the 5-year average. Arrow is also attractive because of its long dividend growth history of 30 years, making the stock a Dividend Champion. The dividend growth rate is about 5% annually, supported by earnings growth. Moreover, the payout ratio is modest at almost 36%, providing confidence about dividend safety and future growth. Additionally, Arrow receives a dividend quality grade of an ‘A.’

{kind=link}

The bank is undervalued, trading at a P/E ratio of ~8.0X, well below the long-term averages. Investors are getting a very undervalued stock with a solid yield and a growing dividend.

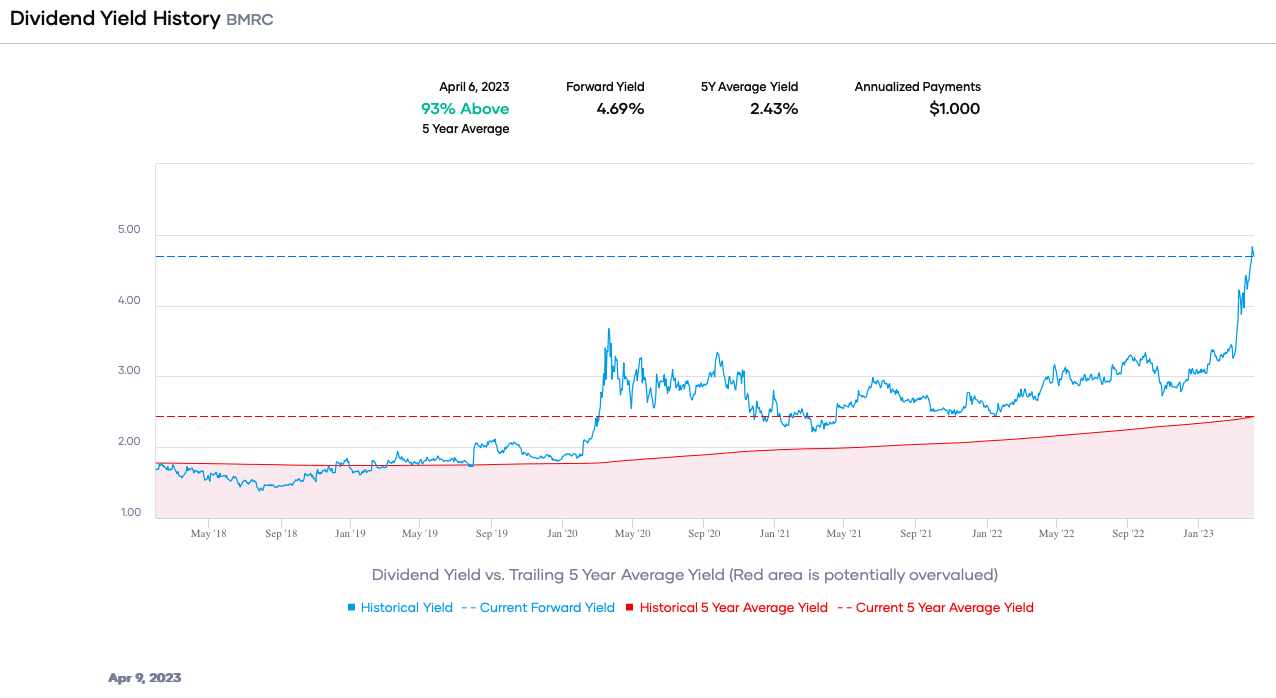

Bank of Marin

The Bank of Marin Bancorp is another community bank. It was established in 1989 and reorganized into a bank holding company in 2007. The Bank of Marin provides personal and commercial banking in Northern California. It focuses on small-to-medium-sized businesses. The market capitalization is only ~$340 million.

The small community bank focuses on relationships, service, and banking fundamentals. Although located in Northern California, the Bank of Marin makes money by working with smaller businesses and retail clients through its branch network, not backing riskier startups. It has 31 retail branches and eight commercial banking centers in ten counties. However, the stock price is clearly in a bear market territory and is down about 35% year-to-date.

That said, the Bank of Marin is growing organically and by acquisitions. For example, the firm bought American River Bancshares in 2021. Now, the firm has approximately $4.3 billion in assets, $2.1 billion in loans, and $3.57 billion in deposits. But asset quality is solid, with non-accrual loans at 0.12% and non-performing assets at 0.21%. Additionally, the firm is well-capitalized based on regulatory standards.

The stock is yielding ~4.69%, a decade high and 2.2 percentage points more than the 5-year average. Moreover, the Bank of Marin is a Dividend Contender with 18 consecutive years of increases. The dividend is growing ~12% CAGR in the trailing five years, but the rate is slowing. In addition, the payout ratio is only 33%, meaning there is little risk of a cut at the moment. Additionally, the bank receives a dividend quality grade of an ‘A.’

{kind=link}

The Bank of Marin is severely undervalued, trading at a P/E ratio of 7.84X. This value is significantly below the 5-year and 10-year ranges. Hence, investors are getting a deal.

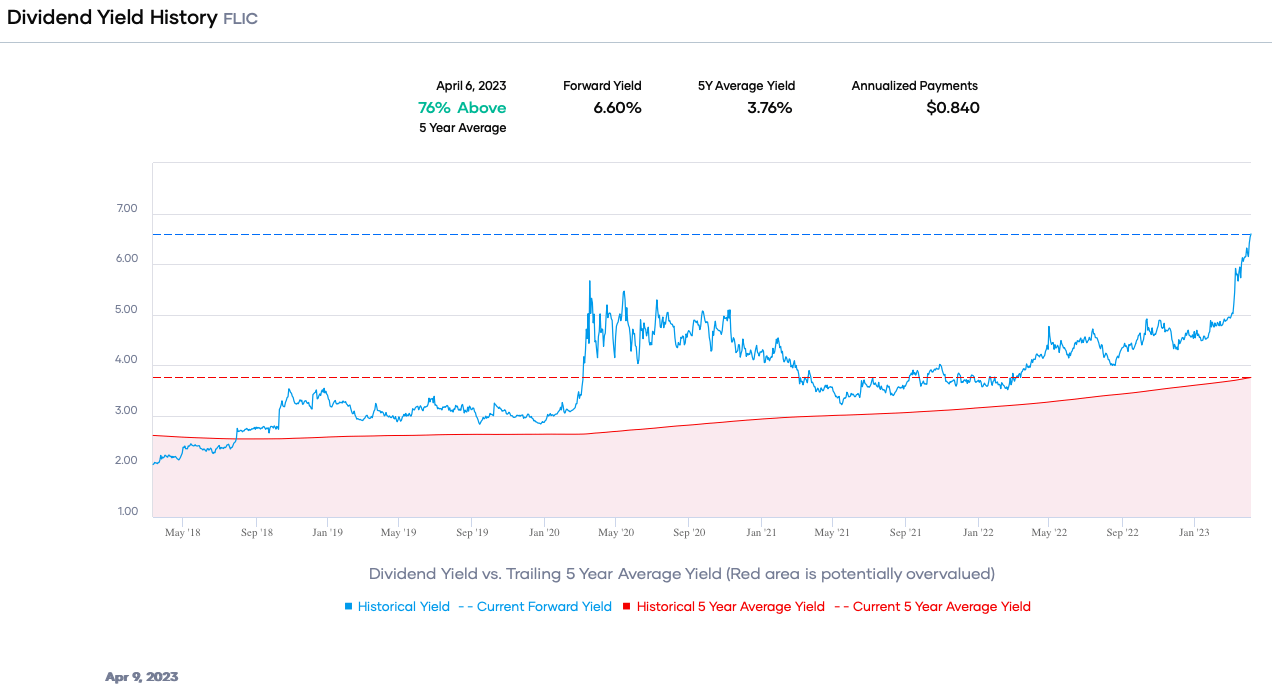

The First of Long Island

The following bank on this list is The First of Long Island Corporation. This is another community bank whose stock price was affected by the recent turmoil. It was established in 1927. Today it operates 41 branches in Long Island and New York City [NYC], offering business and personal banking, investments, and life insurance.

The firm is growing its digital presence and branch network. It is also expanding commercial banking relationships. The First of Long Island has approximately $4.3 billion in assets, $3.3 billion in loans, and $3.5 billion in deposits. The bank’s asset quality is strong, with non-accrual loans at 0.01% and non-performing assets are low. Further, the firm is well-capitalized based on regulatory standards at the end of 2022.

The First of Long Island's yield is at the higher end at 6.6%. This high quantity is nearly three percentage points greater than the 5-year average. It is also a decade high. In addition, the bank is another Dividend Champion with 27 years in a row of increases. The bank has been increasing the dividend at a double-digit rate of almost 12% in the past 5-years. However, the payout ratio is higher than the other banks at roughly 50%. The dividend quality is a bit lower at a score of ‘B+,’ but that is still a strong grade. Overall, we expect the dividend growth rate to slow in the near future, but the safety is still high.

{kind=link}

The banking crisis of 2023 has pushed The First of Long Island’s earnings multiple down to 7.9X, less than half of the long-term average. As a result, investors are getting an undervalued bank stock with a yield better than U.S. Treasuries and many REITs.

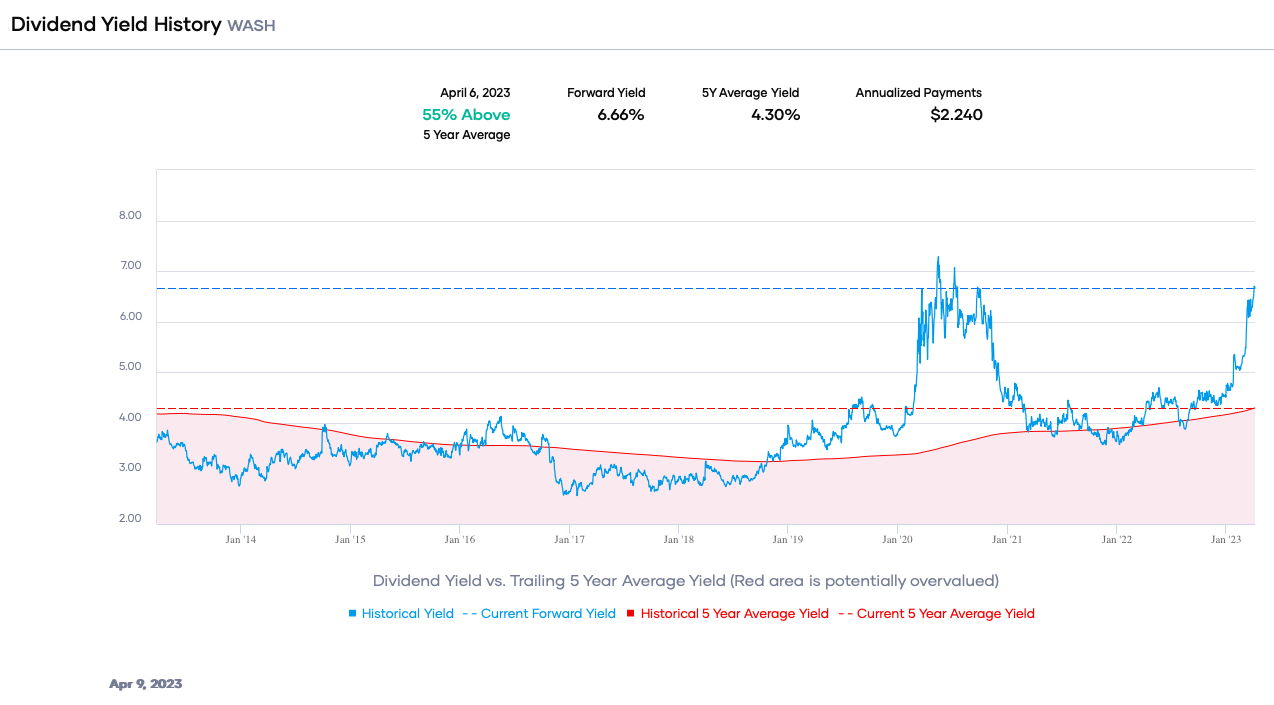

Washington Trust

The last bank on this list is Washington Trust Bancorp, another small community bank. This firm is the oldest community bank in America, dating back to 1800. It is a Rhode Island bank with commercial banking, mortgage, and wealth management businesses in Connecticut and Massachusetts. Today, Washington Trust has 25 branches, four commercial lending offices, seven residential mortgage loan offices, and five wealth management offices.

Washington Trust is growing organically by adding branches. In addition, it occasionally acquires competitors, especially in wealth management. At the end of 2022, the firm had approximately $6.7 billion in assets, $5.1 billion in loans, $6 billion in assets under administration, and $5 billion in deposits. The bank's asset quality is rock solid and is a differentiator. Non-accrual loans are 0.25%, and non-performing assets are 0.19%. Moreover, the bank's asset quality was a plus during the subprime mortgage crisis.

Despite its strengths, investors sold the stock off, and it is down nearly 29% in 2023. Consequently, the dividend yield has soared to almost 6.7%, a value last seen during the pandemic’s bear market. In addition, the bank is another Dividend Contender with 13 years of growth. But the growth rate has slowed as the payout ratio has risen to 53%, still below our limit of 65%. Dividend quality is a little lower with a grade of a ‘B,’ but the safety is still acceptable.

{kind=link}

Washington Trust is worthwhile and, like the other banks on this list, is trading at a depressed P/E ratio of 9.3X. Thus, investors will get an undervalued community bank with an unparalleled yield.

Final Thoughts

The banking crisis of 2023 has seemingly faded. But community and smaller regional bank stocks have not bounced back yet. To quote Warren Buffett,

“The true investor welcomes volatility…a wildly fluctuating market means that irrationally low prices will periodically be attached to solid businesses.”

Consequently, investors can lock in dividend growth stocks with high dividend yields and low valuations.

For further details see:

4 Banks Stocks To Buy In April 2023