O - 4 Cheap REITs To Take Advantage Of

2023-07-12 16:18:14 ET

Summary

- The S&P 500 and Nasdaq have seen strong growth in the first half of the year, with the S&P 500 climbing nearly 16% and the Nasdaq climbing more than 30%.

- The REIT sector has been under pressure due to rising interest rates, but these 4 high-quality REITs look very appealing at current levels.

- All 4 REITs have great portfolios, strong management teams, investment grade tenants, and all appear cheap.

The S&P 500 just completed a strong first half of the year, and the Nasdaq saw its best first half start to a year in four decades. Investors saw the S&P 500 climb nearly 16% with the Nasdaq climbing more than 30%.

However, the climb higher was very top heavy with Information Technology, Communication Services, and Consumer Discretionary sectors all climbing more than 30% in the first half with no other sector climbing double digit percentages. The Real Estate sector however eked out a 1% gain through the first half of the year as REITs dealt with a rising rate environment.

However, I really like REITs, not just for the real estate exposure they offer, but also because the sector has proven to be a solid performer over time. Given the rate pressures, it has provided long-term investors some great opportunities in some high-quality REITs.

As such, in today's piece we are going to look at 4 REITs that appear cheap at current valuations.

4 CHEAP REITS To Take Advantage Of

REIT #1 - Alexandria Real Estate ( ARE )

Alexandria Real Estate is technically an office REIT, but it is not your traditional office REIT. Traditional office REITs have been crushed since the pandemic took place and more business went to remote work or flexible work arrangements, lowering the demand for office space.

Alexandria on the other hand has properties that are utilized heavily by the biotech companies, where in person attendance is much more needed. The top three tenants for the REIT are some of the most trusted life science companies like Bristol-Myers Squibb ( BMY ), Moderna ( MRNA ), and Eli Lilly ( LLY ) to name a few.

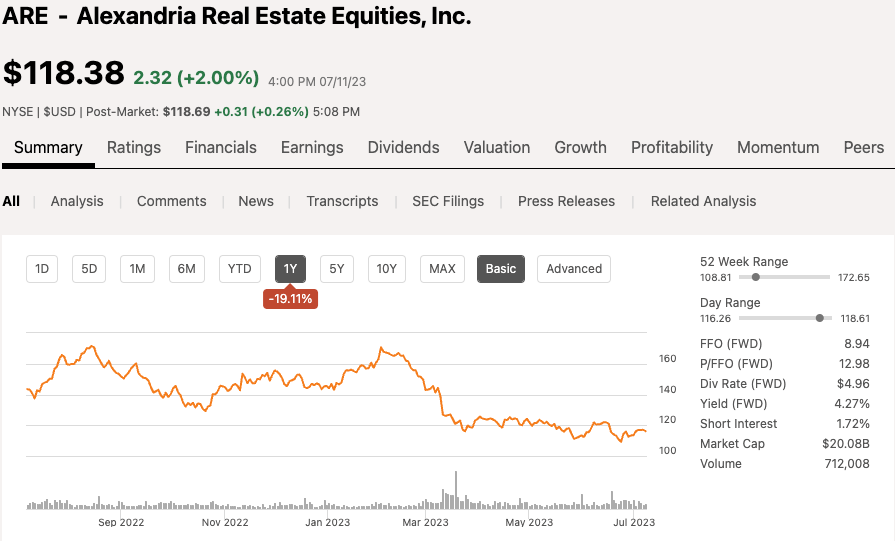

Alexandria Real Estate has a market cap of $20 billion and over the past 12 months, shares of ARE are down nearly 20%, with most of the losses coming in 2023.

{kind=link}

A few reasons shares of ARE have been under pressure:

- High interest rates negatively impact REITs

- ARE being mixed up in the office REIT debacle

- More recently, Activist investor Jonathan Litt shorted the stock last month

The high interest rates are a known within the sector, but that hiking cycle is nearing the end of the road according to the Federal Reserve, with only two remaining hikes expected.

#2 and #3 go hand in hand as Jonathan Litt is stating that essentially Alexandria is just another Office REIT, which is not proper from my standpoint.

He based much of his conclusion based on cell phone data entering and exiting the ARE buildings, showing they were down 50%. Mr. Litt also mentioned upcoming lease maturities and how Alexandria’s cap rate compares to others within the office space.

Again, Alexandria is not your typical office REIT, and the proof is right there with their latest data showing the company doing deals at a CAP rate far different from traditional office. For those unaware, a Cap Rate refers to the percentage of NOI as it relates to the total value of the property, or purchase price when making an acquisition. Companies can use these to gauge acquisitions prices and many use them as comps similar to if you were buying a home.

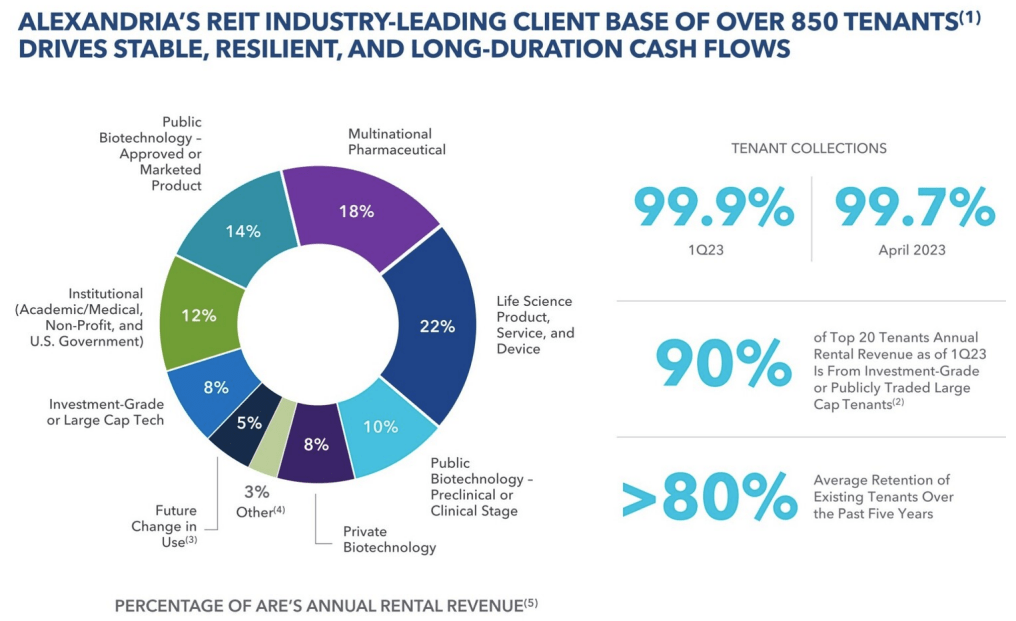

Here is a look at Alexandria’s portfolio and where the company’s revenue comes from. The largest exposure is to the Life Sciences industry followed by multinational pharmaceutical and Public BioTech companies.

{kind=link}

These are not the type of companies that can necessarily work remote. In addition, 90% of the top 20 tenants are investment grade quality with an above 80% retention rate.

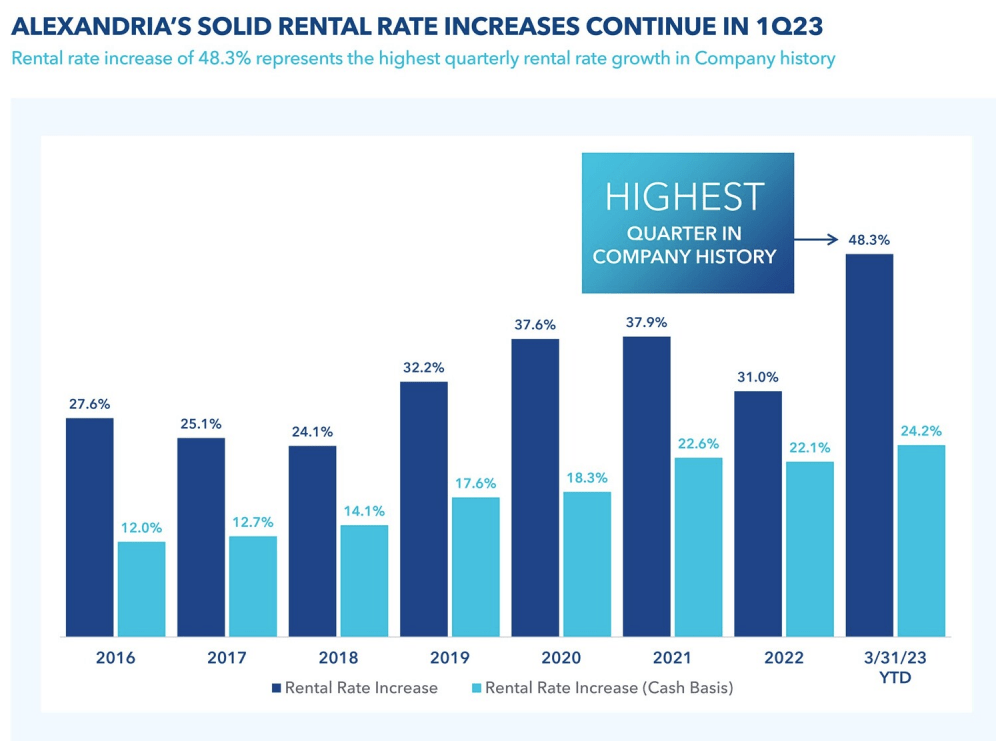

Another point to make, in a time when tenants are heading for the doors, one would think rental rates would be crashing. This has not been the case so far with Alexandria Real Estate as they saw the largest rental rate INCREASE in the company’s history in Q1. That right there should tell you how ARE differs from traditional office. Traditional office is seeing increased vacancy which will likely lead to rate cuts in the near term in order to try and rejuvenate demand.

{kind=link}

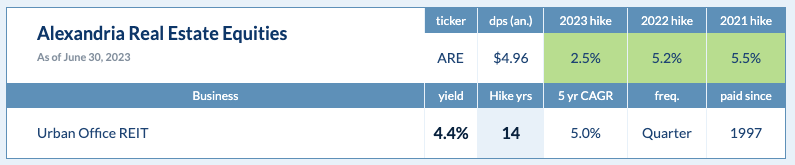

Over the years, Alexandria has consistently raised their dividend, with a five year dividend growth rate of 5%. Given the sell off, the dividend yield sits at 4.4%. The company has been increasing their dividend for 14 consecutive years.

{kind=link}

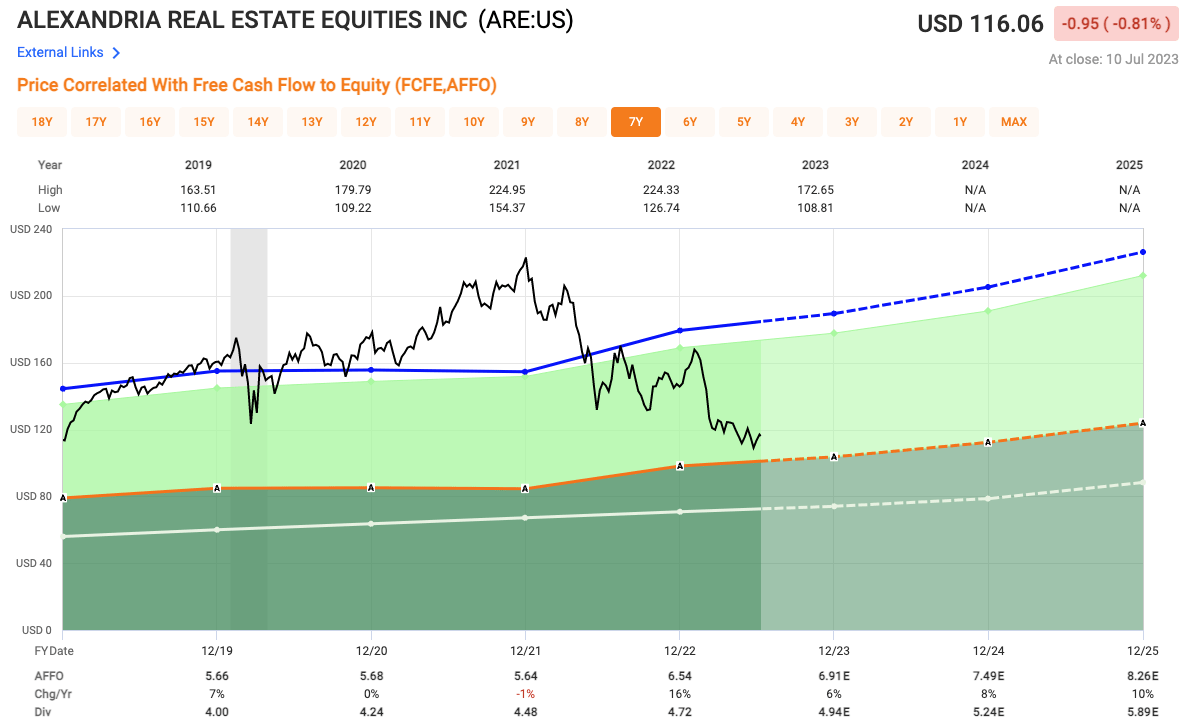

Given the sell-off in shares, Alexandria is now trading at very cheap levels, with a 2023 AFFO multiple of 16.7x. For comparable purposes, over the past five years, shares of ARE have traded at an average AFFO multiple of 27.4x and over the past decade closer to 25.2x, so well below its historical averages.

{kind=link}

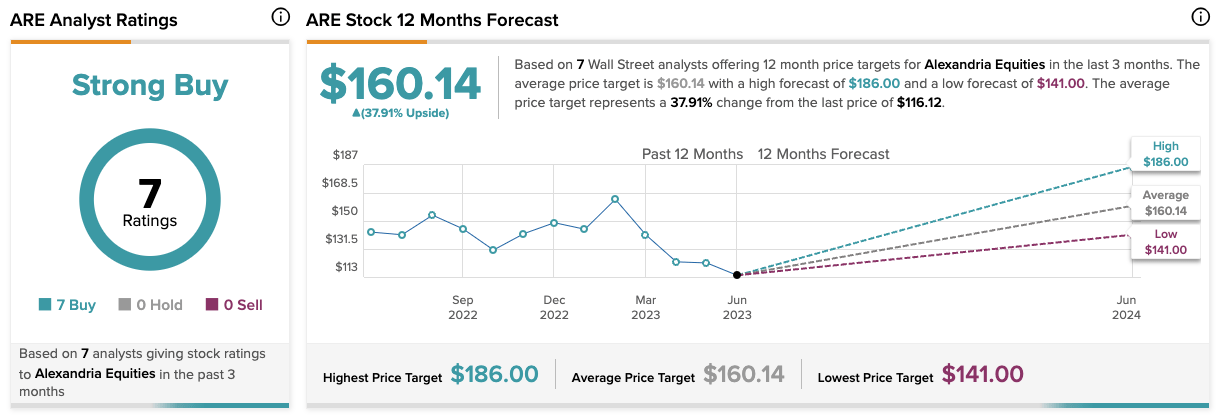

Analysts seem to agree, as they rate the stock a STRONG BUY with an average 12-month price target of $160, implying 38% upside from current levels.

{kind=link}

REIT #2 - Realty Income ( O )

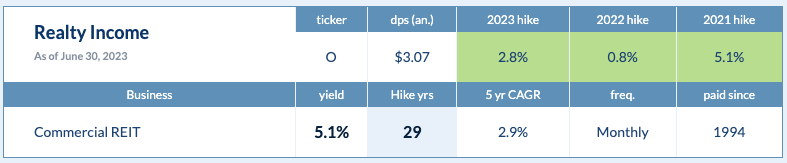

Realty Income is far and away the most popular REIT on our list today and really period. After all, the company is widely known for their Monthly Dividend as they even coined themselves The Monthly Dividend Company.

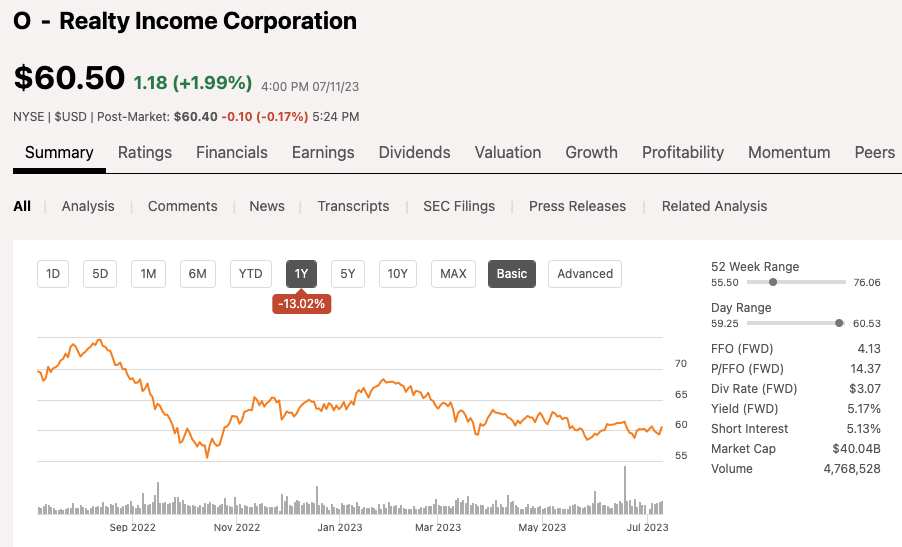

Realty Income is a net lease Retail REIT with a market cap of $40 billion and over the past 12 months, shares are down 13%, and down 5% year to date.

{kind=link}

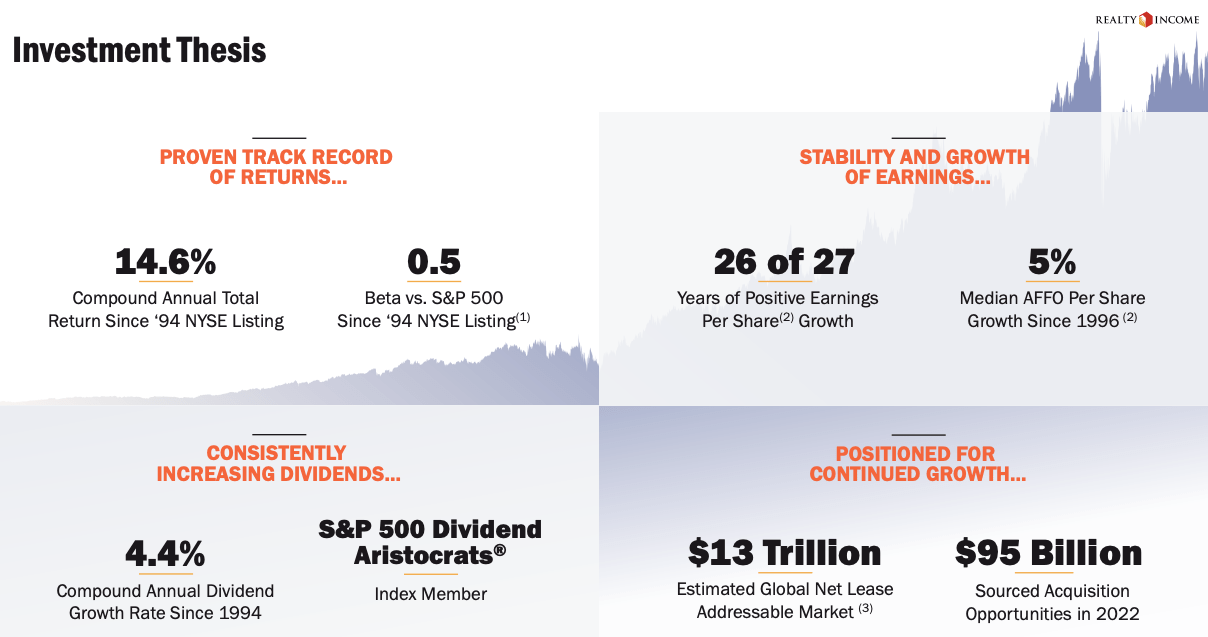

When it comes to consistency, Realty Income is right there. They have been through various economic cycles but still manage to find their way through and come out stronger. As you can see here, since going public in ‘94, Realty Income has a Compounded Annual Total Return of nearly 15%.

Realty Income Q1 Investor Presentation

{kind=link}

The company has seen 26 out of 27 years of positive per share growth, how is that for consistency with a 5% median AFFO per share growth to go along with it.

So the growth is not going to knock your socks off, but the consistency is why people invest. You need stocks you can rely on within your portfolio.

In addition, Realty Income has an A- credit rating with a portfolio of more than 12,000 properties leased out to 1,259 tenants.

Operating as a REIT, it is important to have great properties in great locations, but you also need great tenants. Here is a look at the company’s top 20 tenants, with many notable names:

Realty Income Q1 Investor Presentation

The top industries include Grocery, Convenience Stores and Dollar stores, all well insulated from any economic slowdown.

Realty Income Q1 Investor Presentation

In terms of the dividend, Realty Income as I mentioned at the start pays out a MONTHLY dividend. That dividend currently yields 5.1% and the dividend has been increasing for 29 consecutive years, making the REIT one of the few REITs on the Dividend Aristocrats list.

{kind=link}

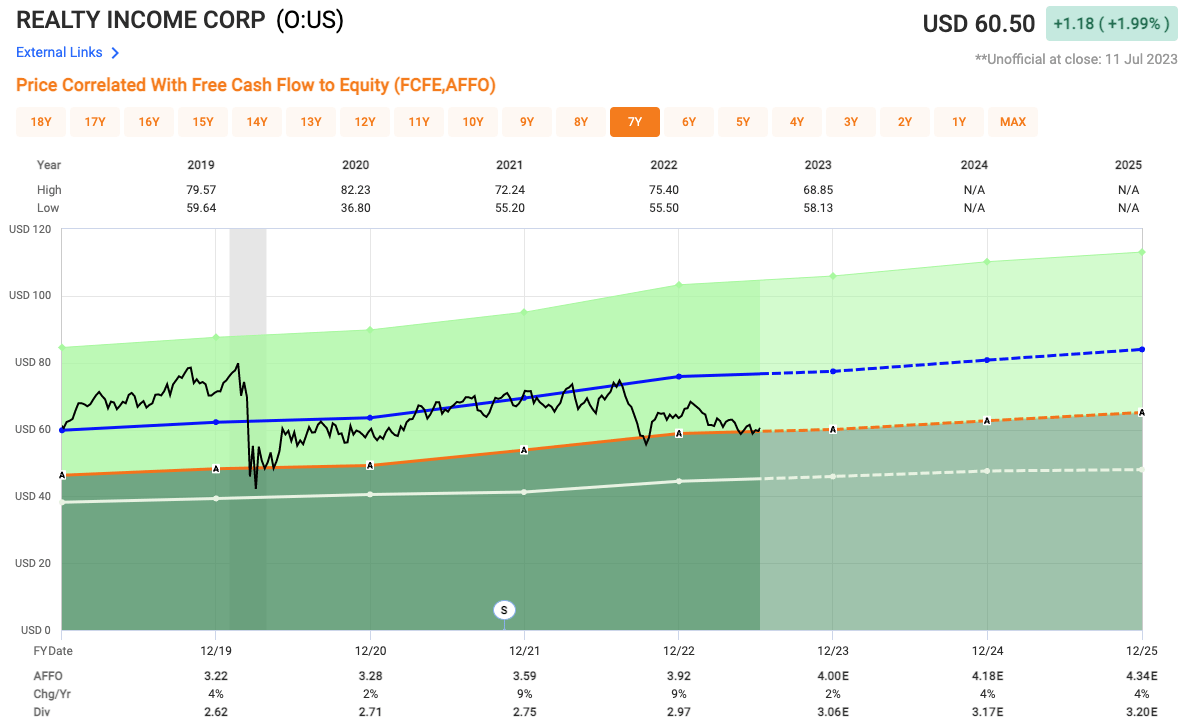

In terms of valuation, Realty Income, due to its quality, tends to trade at a premium within its sector. Over the past five years, shares of O have traded at an average AFFO multiple of 19.4x and over the past 10-years at an average of 18.8x. Right now, you can pick up shares of O at an AFFO multiple of just 15x, well below their historical averages.

{kind=link}

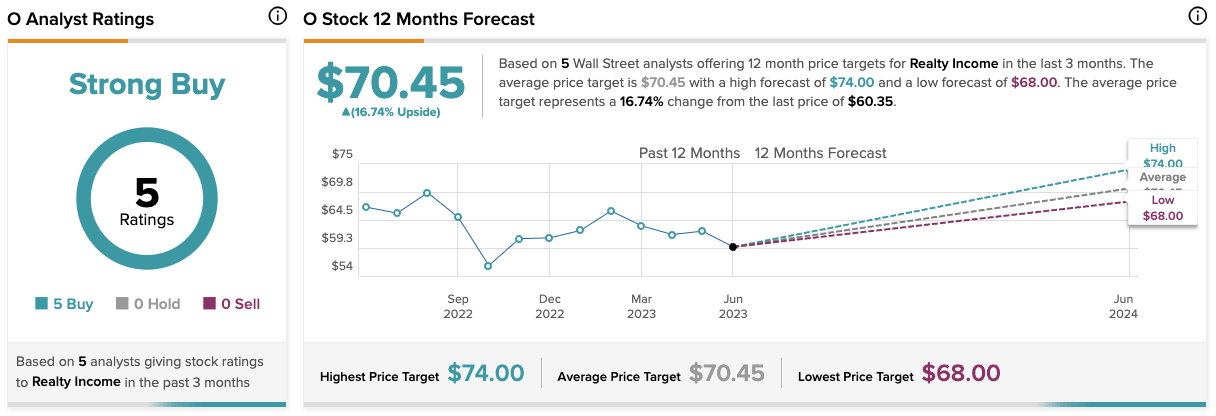

Analysts tend to agree, as they rate the stock a STRONG BUY with an average 12-month price target of $70.45, implying nearly 17% upside from current levels.

{kind=link}

REIT #3 - Agree Realty ( ADC )

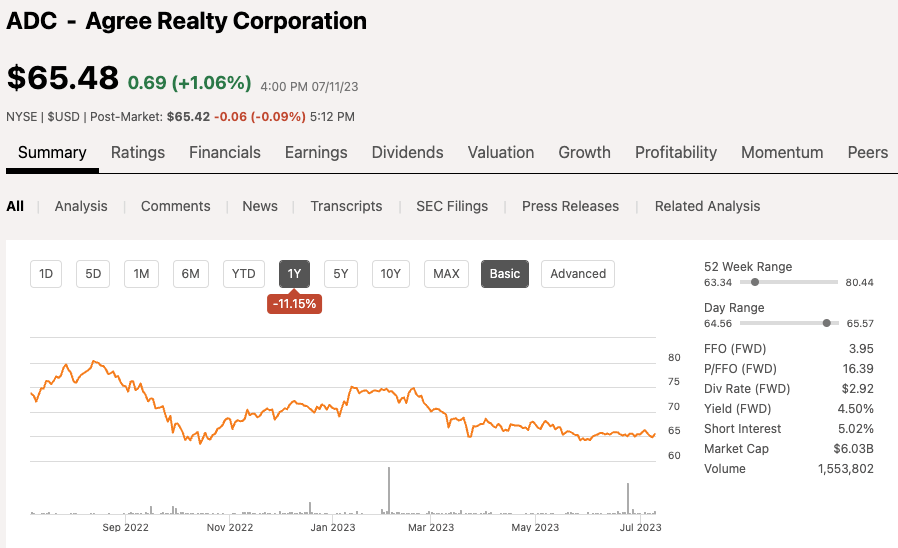

Agree Realty is another net lease REIT built eerily similar to Realty income which we just looked at, but much smaller in scale. ADC has a market cap of $6 billion and over the past 12 months, shares are down 11%.

{kind=link}

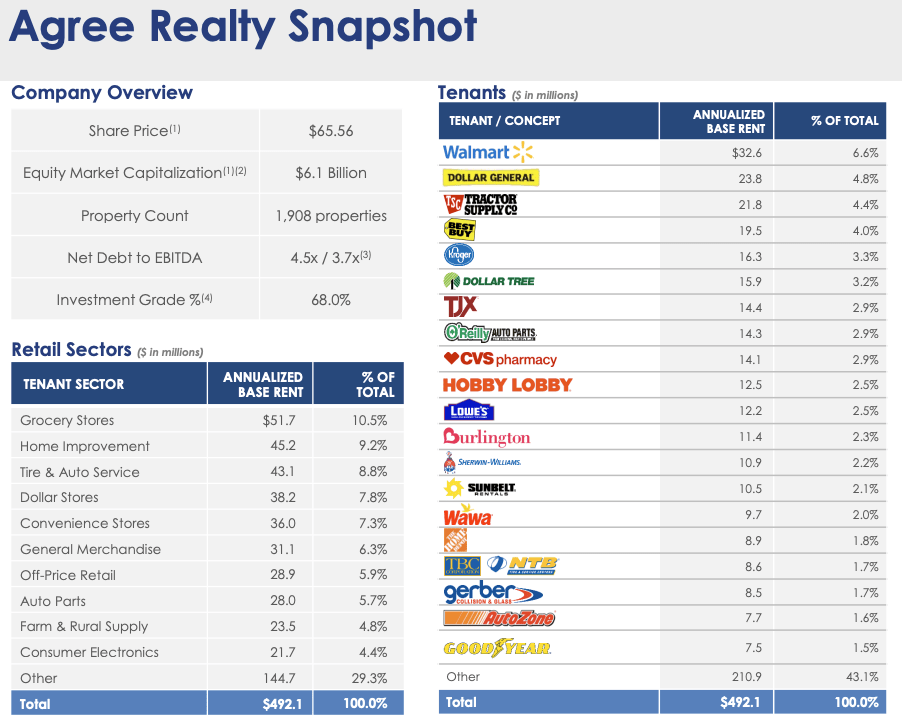

Agree Realty has a property portfolio of more than 1,900 properties within 48 states. Like Realty Income, the REIT also focuses on high-quality tenants with 68% being investment grade, even higher than Realty Income.

Agree Realty Q1 Investor Presentation

{kind=link}

One of the things I like about net lease REITs like Realty Income and Agree Realty is they tend to enter into long-term leases with built in rent escalators that are either fixed or tied to CPI. For Agree Realty, they have a weighted average lease term of nearly 9 years.

Over the past five years, the stock has a total return of nearly 75% with a 12.3% compounded average annual total return since going IPO in 1994, the same year Realty Income went public.

Agree Realty Q1 Investor Presentation

{kind=link}

Here is a snapshot at the company’s portfolio and their top tenants:

Agree Realty Q1 Investor Presentation

{kind=link}

The largest sector exposure for the REIT is Grocery, followed by Home Improvement and Tire and Auto, making up nearly 30% of the entire REIT.

The company also has a strong balance sheet and has no large amounts of debt due until 2028.

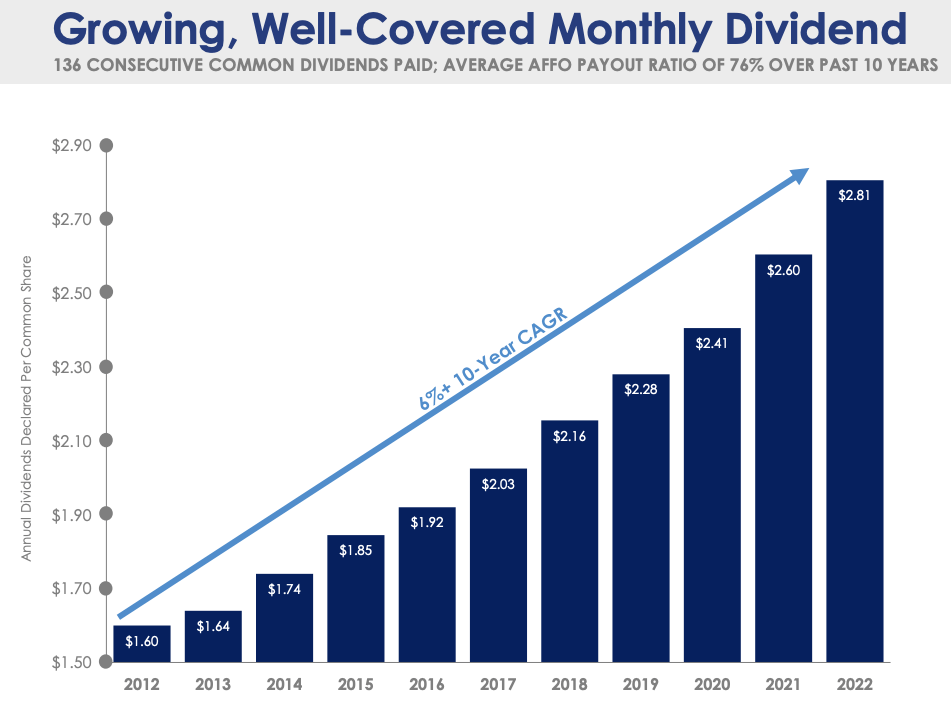

ADC has also placed an emphasis on growing their dividend for 10 consecutive years and they have a five year dividend growth rate of 6.7%. The stock currently yields a dividend of 4.4%.

Agree Realty Q1 Investor Presentation

{kind=link}

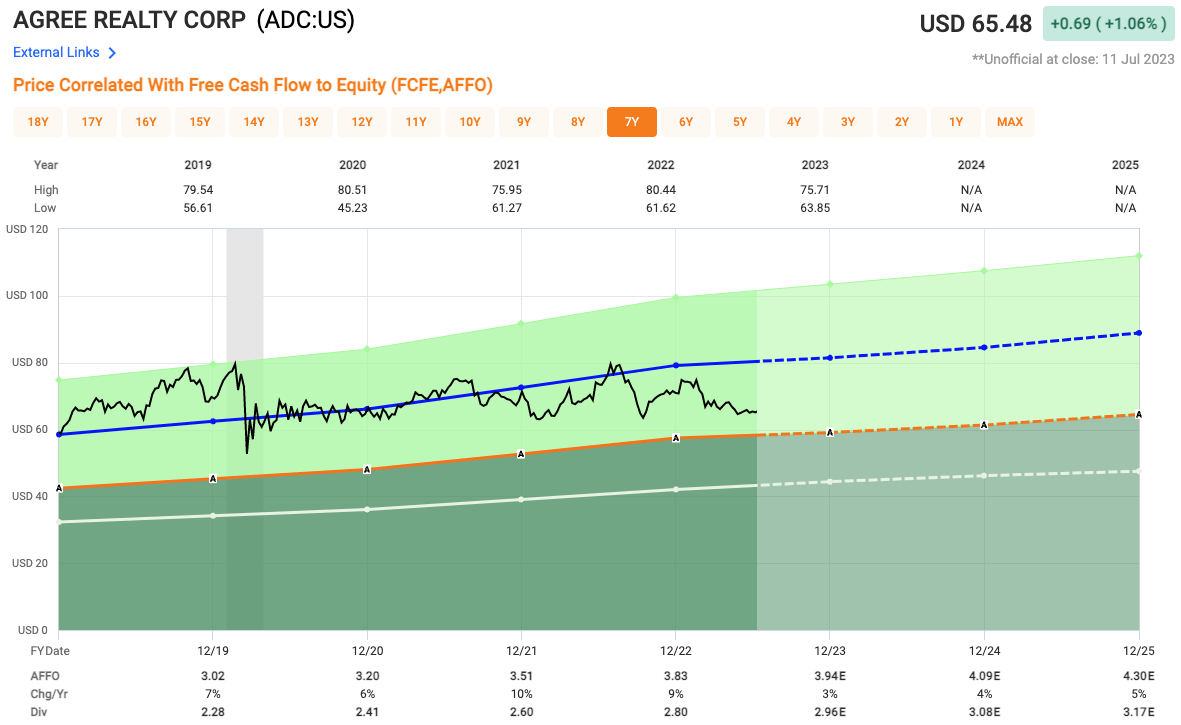

Shares of Agree Realty also look quite cheap at current levels with analysts looking for 2023 AFFO of $3.94 per share, which equates to an AFFO multiple of 16.6x. Over the past five years, ADC has traded at an average multiple of 20.7x and over the past 10 years, shares have traded closer to 18.3x.

{kind=link}

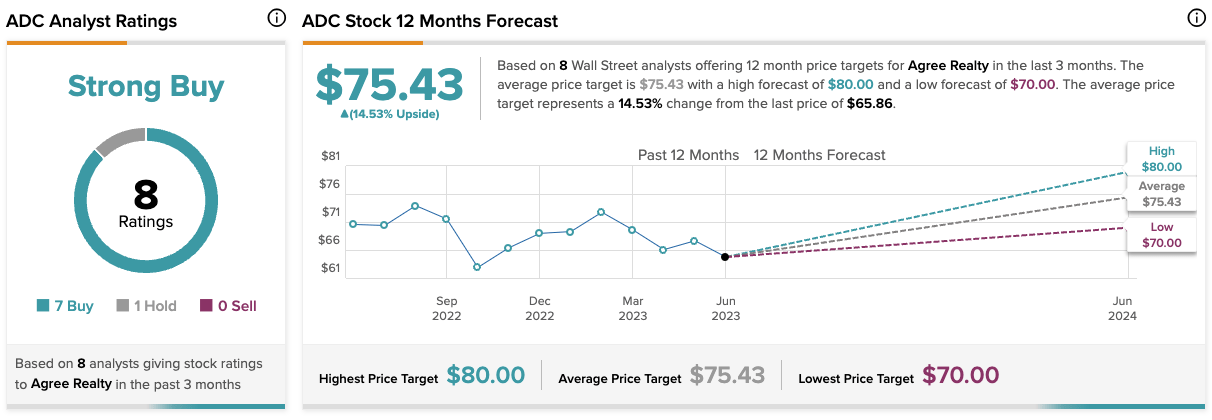

Analysts again agree as they rate shares of ADC a STRONG BUY with a 12-month price target of $75 and change, implying 14.5% upside from current levels.

{kind=link}

REIT #4 - American Tower ( AMT )

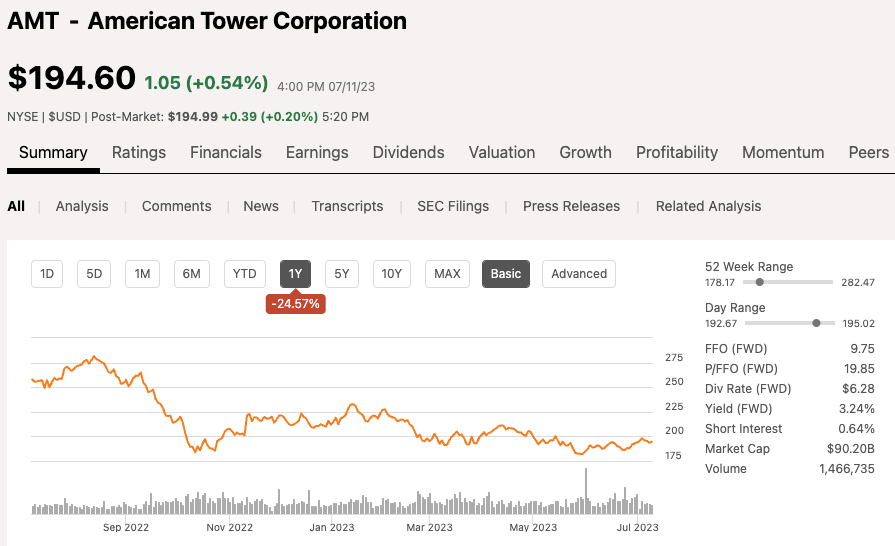

American Tower is the leading cell-tower REIT on the market today with a market cap of $90 billion. Over the past 12 months, shares of AMT are down nearly 25% and down nearly 10% in 2023 alone.

{kind=link}

This stock may be the largest of the group in terms of market cap, but it is also the worst performing of the group as well. Similar to the other REITs, rising short-term interest rates have impacted the REIT sector as a whole. In addition, American Tower acquired data center REIT Core Site for $10 billion, which investors were not crazy about, more related to the timing and the floating rate debt that came along with it.

Another negative for American Tower, which can be seen as a positive at times is the fact that you gain global exposure when you invest in AMT. However, over the past 12+ months, the negative impacts from Foreign Currency has weighed on the stock.

Management is aiming for consistent 5% AFFO Growth through 2027. The largest tenants for the company includes the likes of Verizon, AT&T, and T-Mobile.

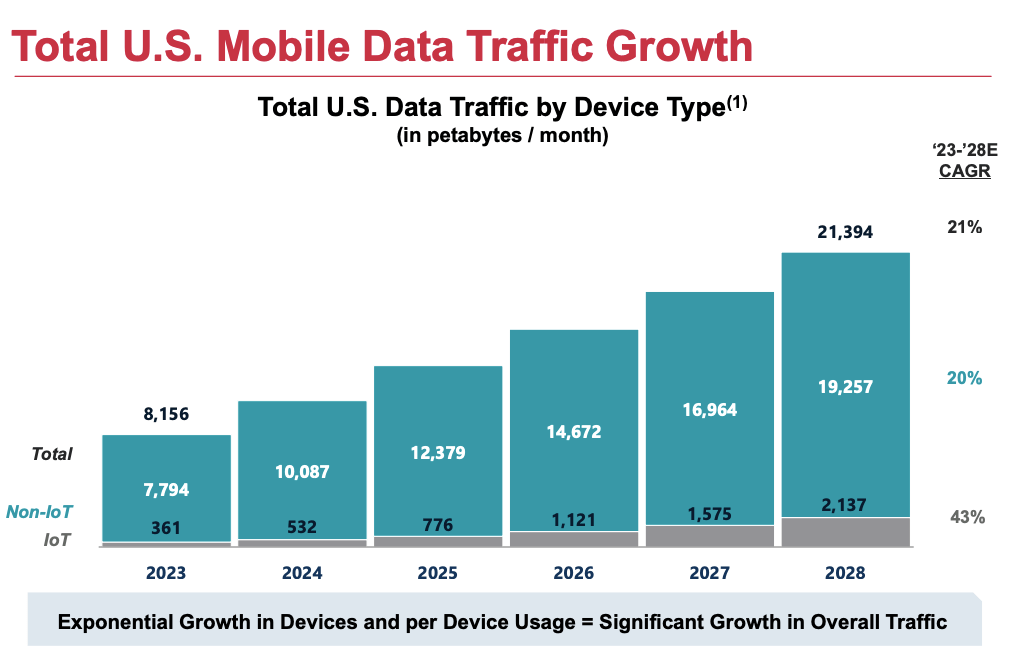

This day in age, cell service and data is a requirement, as everyone is connected one way or another and with the rollout of 5G, the growth factor remains as the fast band for 5G does not travel as far as 4G, creating a need for more cell towers in certain areas moving forward.

{kind=link}

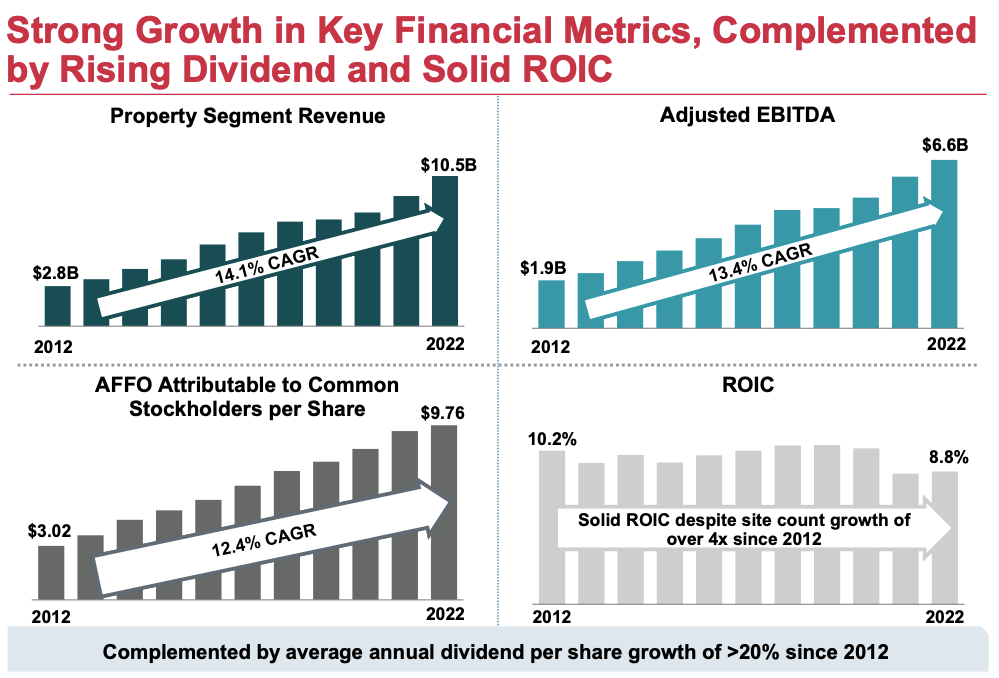

Over the years the company has done a great job at not only increasing top line revenues, but also EBITDA and AFFO. Since 2012, property segment revenue has grown at a 14.1% CAGR, Adjusted EBITDA growing at a 13.4% VAGR and AFFO a 12.4% CAGR.

{kind=link}

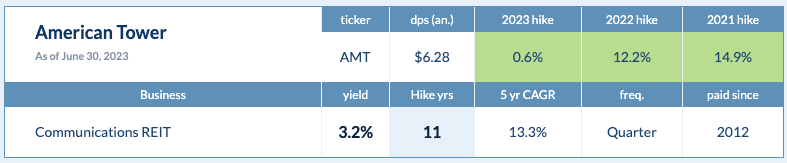

These strong metrics have helped produce strong dividend growth, something that makes this REIT very unique. Given the structure of REITs, having to payout 90% of their taxable income to shareholders in the form of dividends, you don't often see REITs with strong dividend growth, AMT has bucked that trend as they have a five year DGR of 13.3% and they have been increasing their dividend for 11 consecutive years. The stock currently yields a dividend of 3.2%

{kind=link}

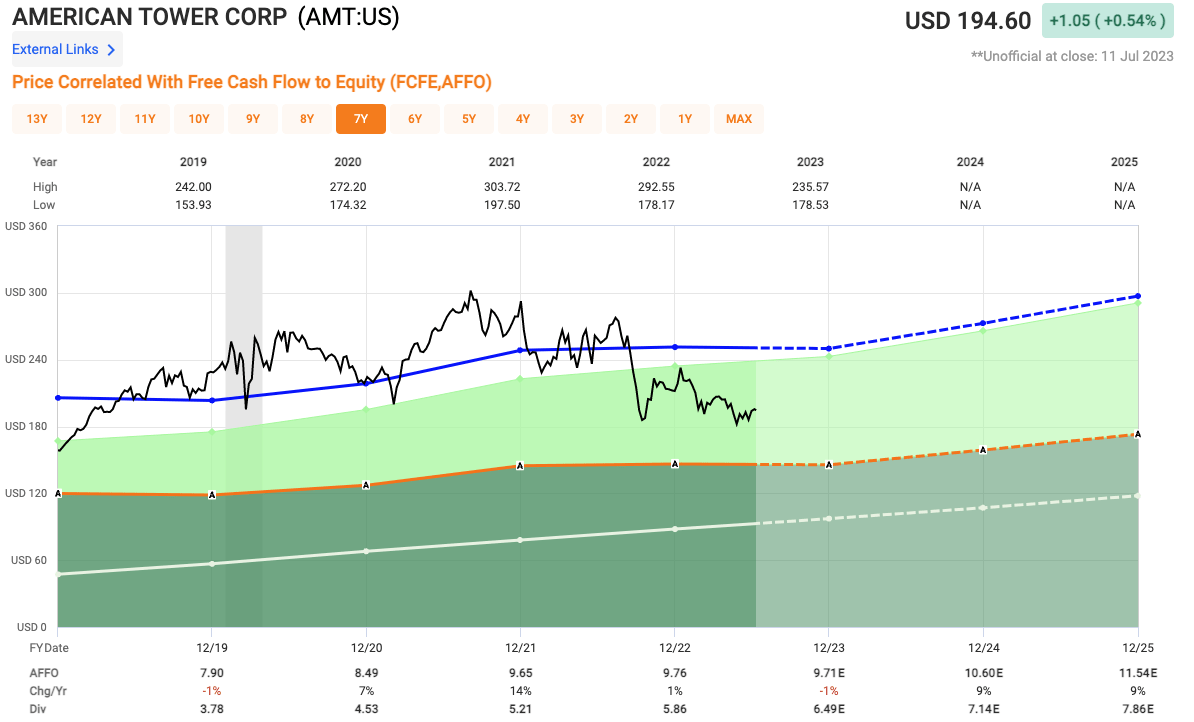

In terms of valuation, AMT shares look very cheap relative to their historical averages. Over the past five and 10-years, shares of AMT have traded at an average AFFO multiple of 25.7x and 22.8x, respectively. Right now, shares of AMT trade at a 12-mo AFFO multiple of 20.0x, well below their historical averages, making the REIT worthy of a second look.

{kind=link}

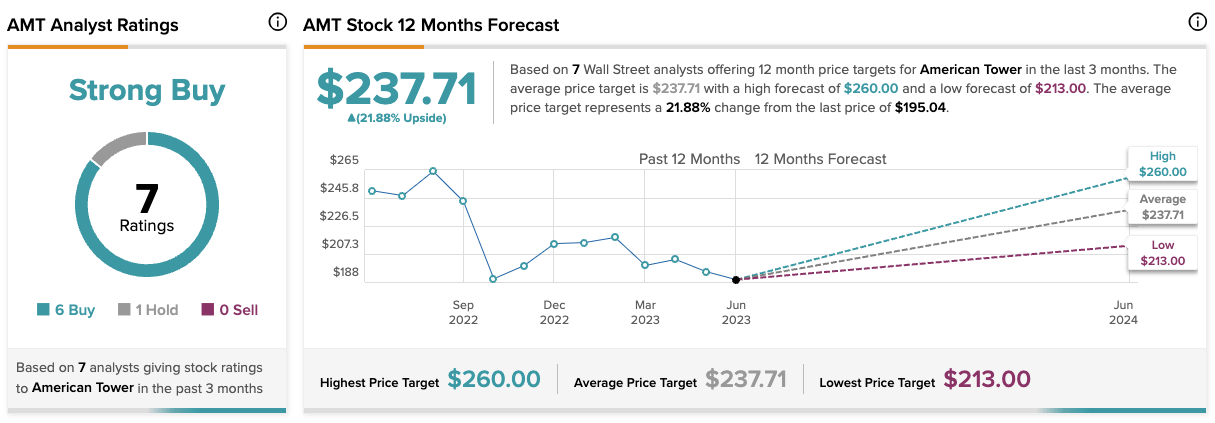

Analysts also agree as they rate the stock a STRONG BUY with an average 12-month price target of $237.71, implying more than 20% upside from current levels.

{kind=link}

Investor Takeaway

REITs have been under heavy pressure during this rising interest rate environment we have all endured for the past year plus. However, the REIT sector is a very broad sector in terms of not only types of REITs but the quality of REITs. The highest quality names, four of which we looked at today, have major advantages in terms of borrowing than their smaller counterparts.

Also, not only are these REITs high quality, but they also have strong management teams and appear to be trading at great valuations.

The commercial real estate sector does have some risks, but I believe it is more sector specific than anything. These REITs still have strong portfolio fundamentals and partner with high-quality tenants.

Comment below which of these REITs you like best.

Disclosure: This article is intended to provide information to interested parties. I have no knowledge of your individual goals as an investor, and I ask that you complete your own due diligence before purchasing any stocks mentioned or recommended.

For further details see:

4 Cheap REITs To Take Advantage Of