RLTY - 4 Closed-End Fund Buys In The Month Of December 2022

Summary

- The market finished 2022 with losses, the worst drop for the S&P 500 Index since 2008.

- That's not always bad for those who can reinvest or put more capital to work.

- I put capital to work every month; these are the moves I made to finish up the year.

This article was originally published to members of the CEF/ETF Income Laboratory on January 1st, 2023.

2021 was another year where investors were spoiled. We were blessed with solid gains for the third year in a row. When this streak ends, nobody knows. That being said, I would temper expectations heading into 2022. After such large runs, it would seem apparent that we need earnings to catch up with valuations

That's how I started off my article from exactly a year ago . I guess we know the streak ended in 2022, and "temper expectations" was too mild in tone.

Now, 2022 is finished up, but there might not seem like a lot of optimism for 2023. We still have the Fed hiking rates, which could put further pressure on the market - but more importantly, put pressure on the economy to cool it down. At the end of the day, that's their main goal to slow down the economy to slow down inflation. A fairly blunt tool, but it is what they have to work with.

The Dow Jones Industrial Average held up fairly well thanks to that index's value-oriented tilt. The heavier growth and tech-focused S&P 500 Index was hit quite hard, and the Nasdaq was slaughtered.

Ycharts

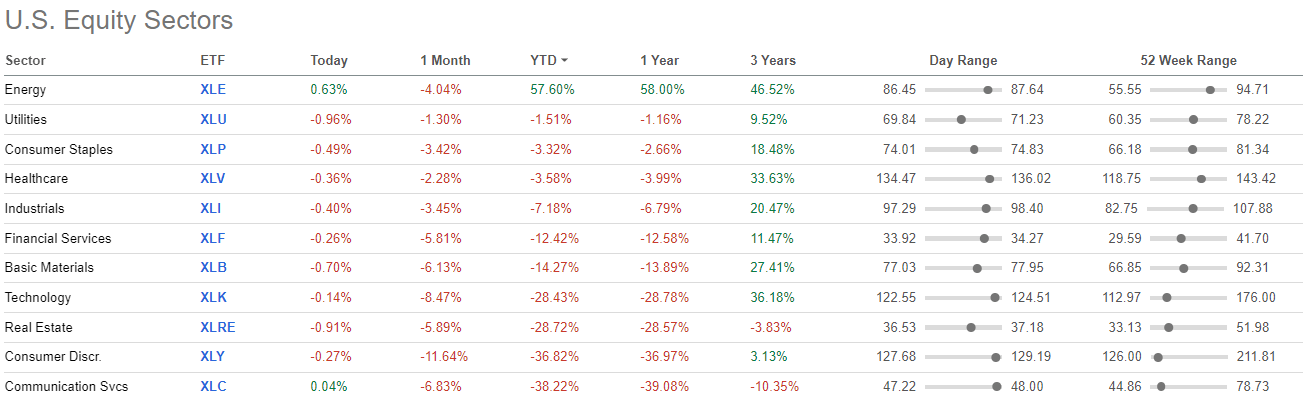

The energy sector was the leading sector for the year. In fact, it was the only sector that finished in the green. Defensive sectors such as utilities, consumer staples and healthcare made a good run but ultimately fell short.

{kind=link}

On sectors in my article last year, here is what I mentioned.

With that, some snapback of the [energy] sector seemed almost inevitable at some point. Real estate was also another strong contender for the year. Utilities and consumer staples were the laggards and could represent interesting choices to put additional capital to work as we enter 2022.

Communication services, consumer discretionary and real estate are the worst performers this year; I think they have a good chance of being fairly decent places to put capital to work. Real estate, in particular, is a sector I tend to lean towards. Interesting to note that communication services and real estate are now showing negative results over the last three years. Putting capital to work there through CEFs or individual REIT names makes sense to me. Although there isn't a CEF that I'm aware of that invests primarily in the communication services sector.

With deep losses for the S&P 500 and the Nasdaq, much of the damage could already be in. Historically, the S&P 500 has only fallen in back-to-back years a minority of the time. Most years are positive following a drop. Every time is different, so that might be a small consolation, but with losses also come opportunities.

For those that can reinvest a portion of their dividends and income, doing so now means we are getting much better prices than at the start of the year. Those with longer-term time frames and still in the accumulation phase should also be buying at these levels. I add new capital and reinvest every month; these are the moves I made in December to finish up the year.

Cohen & Steers Real Estate Opportunities and Income Fund ( RLTY ) And Cohen & Steers Quality Income Realty Fund ( RQI )

After selling out of a position last month to make room for RLTY, I added even more RLTY to my portfolio. Another opportunity led to freeing up capital to invest more once again in December. I also added to RQI, which is already my largest personal position when factoring in the weighting I carry in another account.

So while it's starting to become quite a hefty position now, valuations-wise, it made sense. The reason is that Cohen & Steers REIT and Preferred and Income Fund ( RNP ) became overvalued, leading to their large year-end special. RNP is a quality fund and has been a significant position in my invested capital, reflecting my confidence. However, when it touched near a 10% premium, it was uncharacteristic of the fund.

Ycharts

So when that happened, I split my RNP position into RLTY and RQI. RNP is the fund that holds the heaviest in preferreds at around 50% preferred/50% equity in its portfolio. RQI only carries a fairly slim amount of preferred, and RLTY carries a preferred allocation in the middle of these two, at around 34% preferred and 66% equity.

Ultimately, it made my investments more aggressive by allocating higher weightings to REIT equity positions. In hindsight, it was the right call. That was even though on a total NAV return basis, RNP performed better; it underperformed on a total share price basis. To be fair, it wasn't by a large margin, though.

Ycharts

I would still view RQI and RLTY as being the more attractively valued funds and don't plan to switch back yet. However, should RNP come to a discount again, I would definitely put capital back to work in the name. Ideally, I'm looking for a 5% discount, and a 10% discount would have me buying aggressively.

Eaton Vance Tax-Managed Buy-Write Opportunities Fund ( ETV )

It has been a long while since ETV's been in my portfolio, but it finally made sense to boot Eaton Vance Tax-Managed Buy-Write Strategy Fund ( EXD ) out. The valuation difference between the two became quite wide. The tip-off of this was thanks to Stanford Chemist's trade alert .

This wasn't an equal switch for me, though, as I added capital and my ETV position became relatively larger than my EXD position had been.

The main reason it would seem this happened is that ETV recently announced a distribution cut, along with most of the Eaton Vance equity funds. However, EXD held steady. With the fund having a lower distribution yield, it likely didn't make sense to trim EXD. No one likes cuts, but the yield was becoming quite elevated.

In fact, it's still at a fairly high distribution yield, and if the market continues lower, we could see another cut.

Ycharts

The call-writing premium helps provide capital gains. Interestingly, in their last semi-annual report , they pulled in ~$111.4 million in options premiums. At the same time, they paid out $71.4 million. So it was enough to cover the distribution to shareholders, but unrealized losses and realized losses meant that net assets dropped $309.3 anyway.

After these cuts, it was later announced the intention that it would merge EXD into ETV. These funds are virtually identical, and EXD is a tiny fund, relatively speaking. Since making the swap trade, EXD has come down sharply to meet ETV.

Ycharts

Given that the merger is likely to happen (these things are almost always approved,) this makes sense. EXD investors are eventually going to become ETV shareholders at a lower valuation. There is no sense in holding onto EXD if it's at a higher valuation. Now, trading at almost parity with each other, the difference is minimal. This means that, at this point, a swap is no longer required.

DoubleLine Yield Opportunities Fund ( DLY )

I also took the chance to average down on my DLY position. I covered this fund quite recently , and the main takeaway is that the fund's discount combined with the underlying bond pricing discount on the fund makes it attractive. The underlying average market price for DLY's portfolio was last reported at $81.21. The discount of the fund's share price relative to its NAV is also trading near the lower levels since its inception.

Ycharts

This isn't the first time I've added to DLY; earlier in May of this year and also last December , I also bought some. Before writing this, I hadn't realized I bought DLY last December too. That being said, each time has proven to be too early to buy. Overall, the fund hasn't performed well, but neither has fixed-income in general.

The leverage on the fund's portfolio amplified the downside moves. That meant that while being mostly allocated to high-yield debt, the fund performed more similarly to investment-grade debt. It is worth noting that investment-grade debt performed worse this year than high-yield because of its interest rate sensitivity.

Below is a comparison of DLY with iShares iBoxx $ High Yield Corporate Bond ( HYG ) and iShares iBoxx $ Investment Grade Corporate Bond ( LQD ). This helps provide the context of the performance comparison between DLY and high-yield vs. investment-grade bonds.

Ycharts

DLY has been the weaker performer on a total share price return basis, but much of that is with the discount widening. If fixed-income rebounds, it is possible that DLY will rebound even harder - due to the employment of its leverage and discount contraction. That's yet to be determined and a big "if" heading into 2023.

Conclusion

2022 was bad; 2023 could be bad. Longer-term investors can take this opportunity to add. For me, 2022 was great as I've kept minimal cash on the sidelines as I put my 2021 cash hoard to work. I also reinvested everything coming in. That made me more aggressive with buying throughout the year and growing my income in the future at a faster clip.

At this point, the distribution trims have been quite minimal and offset by some of the boosts in my floating rate exposed funds. Although, we should be fully aware that more distribution cuts could be coming for equities if things don't turn around or if they get worse from here that would about guarantee cuts.

Fixed-income funds aren't necessarily off the hook either. While the income should continue flowing in, those leveraged are at risk. Their income will take a hit if they have to deleverage their portfolio due to declining prices. Thus, potential distribution cuts could also be in the cards for credit funds. That's even though income streams aren't impacted just by lower prices.

For further details see:

4 Closed-End Fund Buys In The Month Of December 2022