REXR - 4 Great REITs At Deep Discounts To My Targets

2023-08-24 17:55:22 ET

Summary

- Listicles have become popular due to readers' preference for shorter content.

- Alexandria Real Estate and Camden Property Trust are highlighted as great REITs for investors.

- Sun Communities and Rexford are mentioned as top REIT picks with strong growth potential.

Listicles have become exceptionally popular. From BuzzFeed to Seeking Alpha, readers tend to want shorter content. You ask, I deliver.

Let's talk about some great REITs.

Medical Properties Trust

How about Medical Properties Trust ( MPW )?

Nope, not a great REIT. Doesn't belong here. I can't even blame someone who saw that name at the top and jumped to the comments section.

I agreed with cutting the dividend, but it should've been done earlier. It wasn't a dividend problem this year. It was a dividend problem for multiple years. They pushed that payout ratio way too high, and it didn't leave them with enough retained cash flow.

That's without getting into the jets or taking "rent" in the form of illiquid equity investments. Nope. Let's try again.

Alexandria Real Estate

Alexandria Real Estate ( ARE ) is a great REIT for investors interested in healthcare. It focuses on lab space rather than on hospitals and the company has delivered outstanding returns to shareholders over a very long period. They did that by growing NAV (Net Asset Value) and AFFO per share.

ARE strives to be transparent, and presentations include quite a bit of detail that many REITs don't provide. Beyond that, management has a solid history of making good decisions. For instance, when share prices went down and interest rates went up, they accelerated dispositions (at quite reasonable cap rates) to free up cash flow. That enabled them to continue developing properties (at a healthy profit) without taking out expensive debt or issuing dilutive equity.

There's nothing wrong with issuing equity at the right price, but that price definitely isn't under $120.

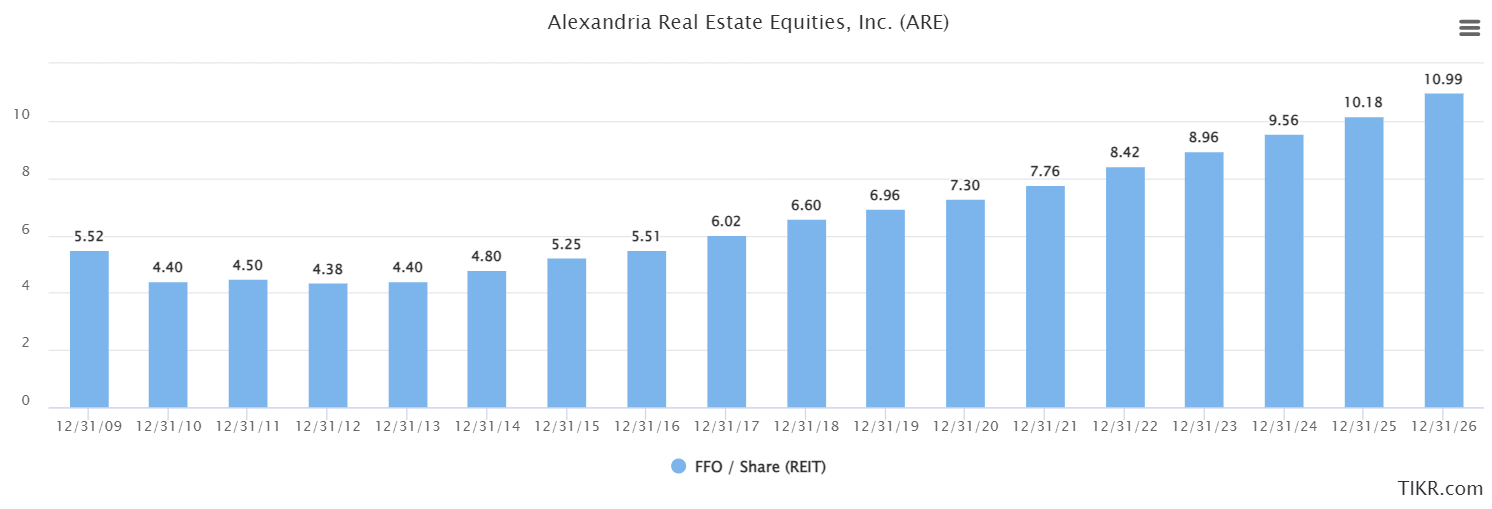

You'll notice FFO trends higher as we move to the right:

{kind=link}

That's common for great REITs. Extremely common. Basically, you can't be a great REIT without doing that.

Note: Normally, we use AFFO. However, the historical adjustments included in the data goes into the AFFO value. TIKR's data set make AFFO more volatile and less useful. That's a really rare situation, but that's why I'm using the FFO chart.

That doesn't mean you never have a down year. ARE had a rough recovery from the GFC (Great Financial Crisis). Why was it rough? ARE made mistakes leading up to the GFC and entered an exceptionally hard period with materially too much debt. Management has been committed to not repeating that mistake. They've been careful with debt leverage, and they were proactively locking in long-term financing for the debt they do use. Good REIT.

There's one headwind. Is it tenants all moving out? No. Is it cell phone data showing fewer people in the buildings? No, having some admin staff working from home doesn't invalidate the need for labs. The headwind is new supply over the next few years. Low rates and higher profit margins resulted in more new development.

However, office conversion is also a risk. Converting offices into lab space can be very expensive, but when office real estate values plummet, the cost of giving up that office space is much smaller.

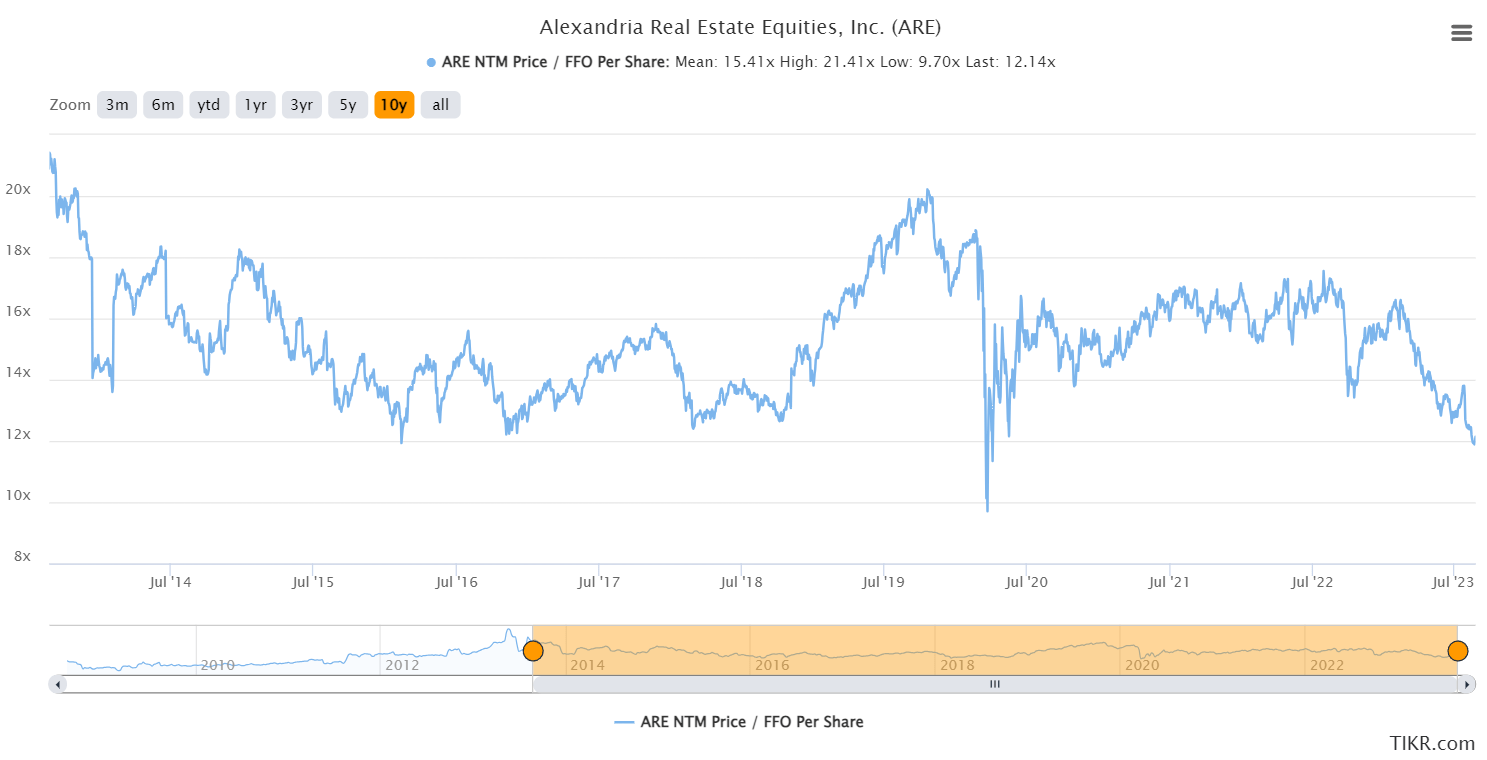

Price to FFO multiples look cheap:

{kind=link}

That was way too many words about one REIT. I won't do it again.

Sun Communities

Sun Communities ( SUI ) has been one of my favorite REITs for many years. My oldest open positions are in shares of SUI, SUI, SUI, and SUI again. Yeah, I like SUI. They own manufactured home parks, RV parks, and marinas. That gives them a fairly captive customer base and the recurring capitalized expenditures are low.

They were able to use cash to do small-scale development projects (like adding a few pads for manufactured homes) in existing properties with very attractive yields on cost.

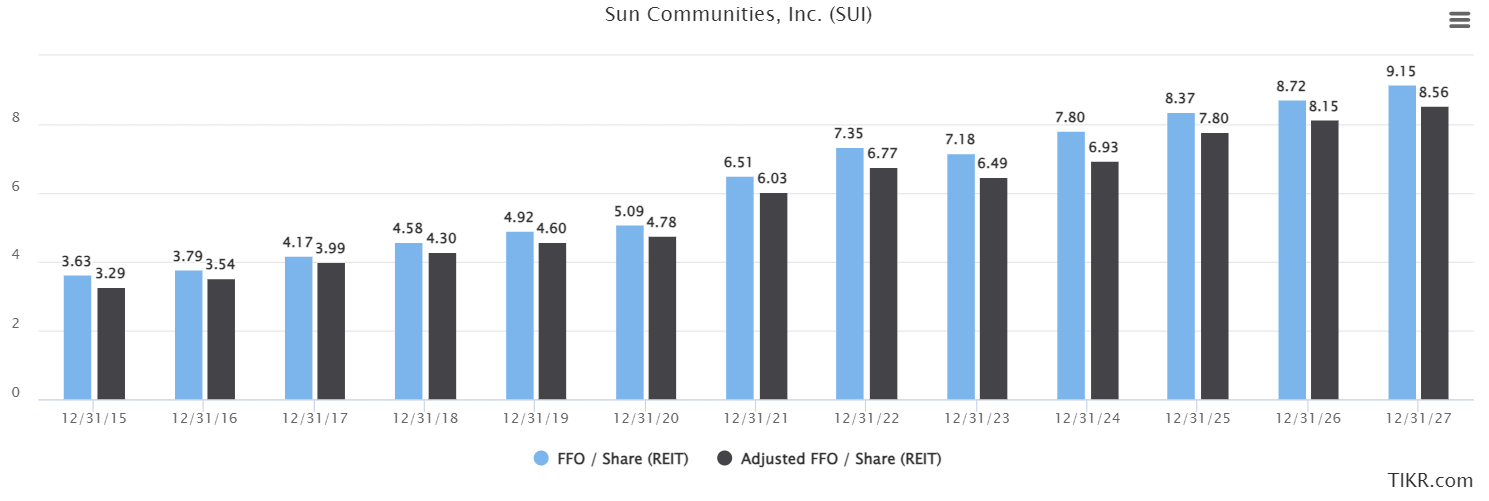

Just like with other great REITs, you'll see values trend up and to the right:

{kind=link}

There's a dip in there. You'll notice that 2023 doesn't look great. I think the projected growth rate from 2023 to 2024 might be a bit too high. Who says that about one of their favorite REITs?

SUI made a mistake in 2021. They didn't get aggressive about locking in rates on their debt. They had significantly too much variable-rate debt, and it created a huge headwind for growth rates. That was a huge factor impacting SUI's growth rate from 2022 to 2023. Several months ago, the yield curve implied interest rates would fall in the latter half of 2023. That's been disappearing. Consequently, interest rates entering 2024 could still present a headwind.

Camden Property Trust

Camden Property Trust ( CPT ) is an apartment REIT. They have a mixture between the bigger markets and the sunbelt markets. Given how few REITs have much sunbelt exposure, they get classified as sunbelt.

I don't usually do a bunch of images of properties, but I think it's appropriate here. Investors seem to be forgetting about the appeal of being a landlord.

Properties like this are a great source of recurring revenue streams that grow year after year:

{kind=link}

How about a property in Dallas? Try to tell me you have zero interest in owning this complex:

{kind=link}

That's a very nice complex. To compete with it, you'd need something like this:

{kind=link}

That's another beautiful complex that's driving more cash flow for shareholders.

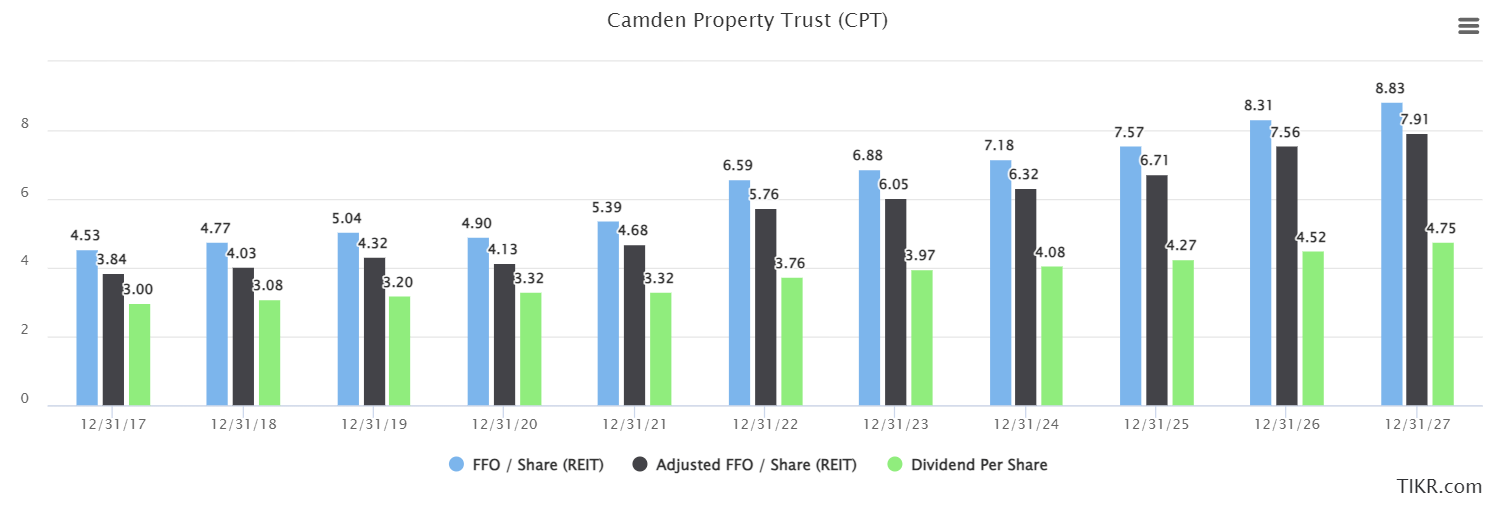

But are they actually growing cash flow per share? Absolutely.

{kind=link}

FFO, AFFO, and dividends have all been trending higher. You also might notice that dividends didn't grow as fast as the other values. CPT has a very reasonable payout ratio that leaves it with cash on hand.

Some investors hate a responsible board of directors, but not me. I'm a happy shareholder. The value of the REIT doesn't magically increase the day the board declares a bigger dividend. I'm still very confident management is using that cash to increase value for shareholders. They do that with techniques like building another great apartment building.

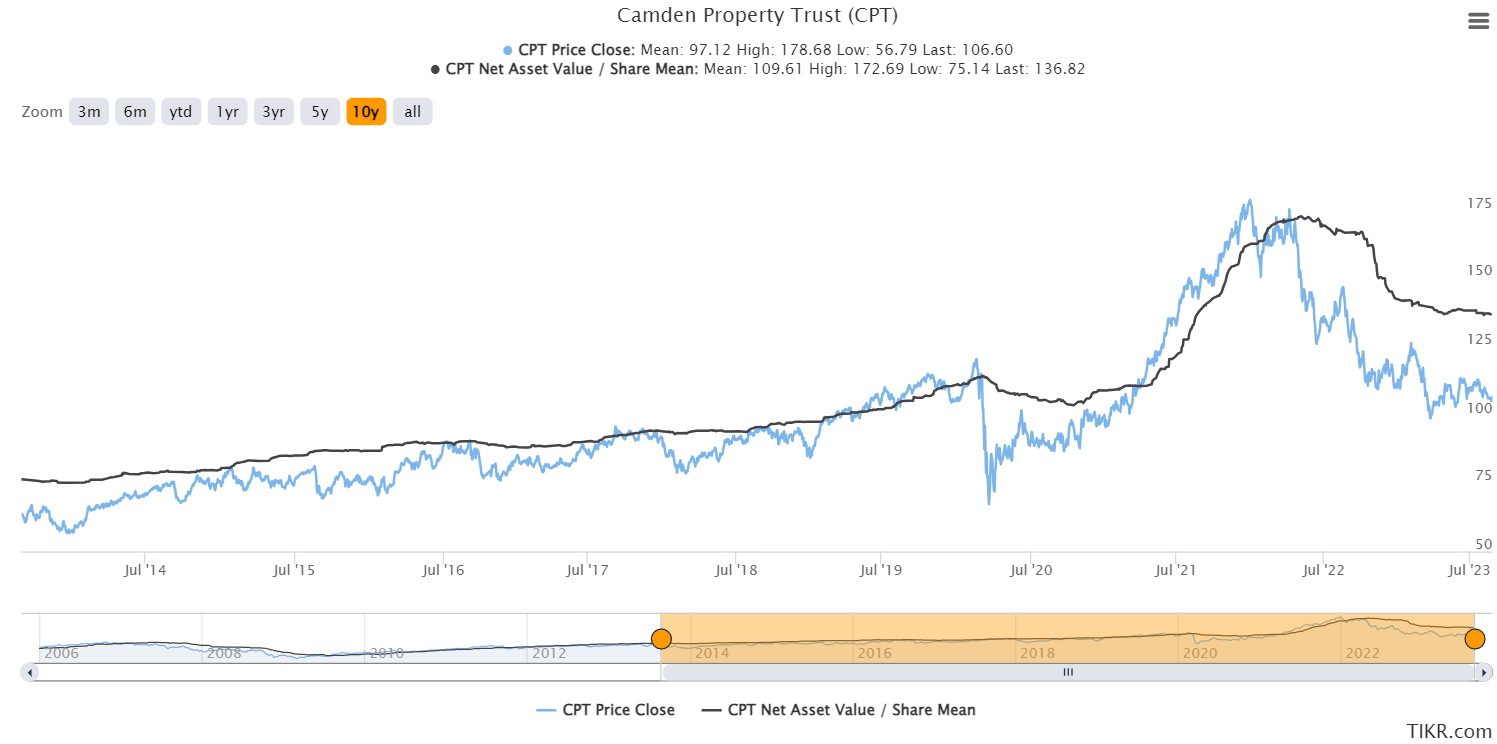

If you like those apartment buildings, you might like to know that they are available at a substantial discount to the fair market value of the real estate:

{kind=link}

Those NAV estimates appear to have stabilized, and they're still far above the share price. I call that a margin of safety. Why would I want to invest directly in the apartment buildings when I could get it at a huge discount, get great management, and have the REIT access much cheaper debt than I could because of their great balance sheet?

Rexford

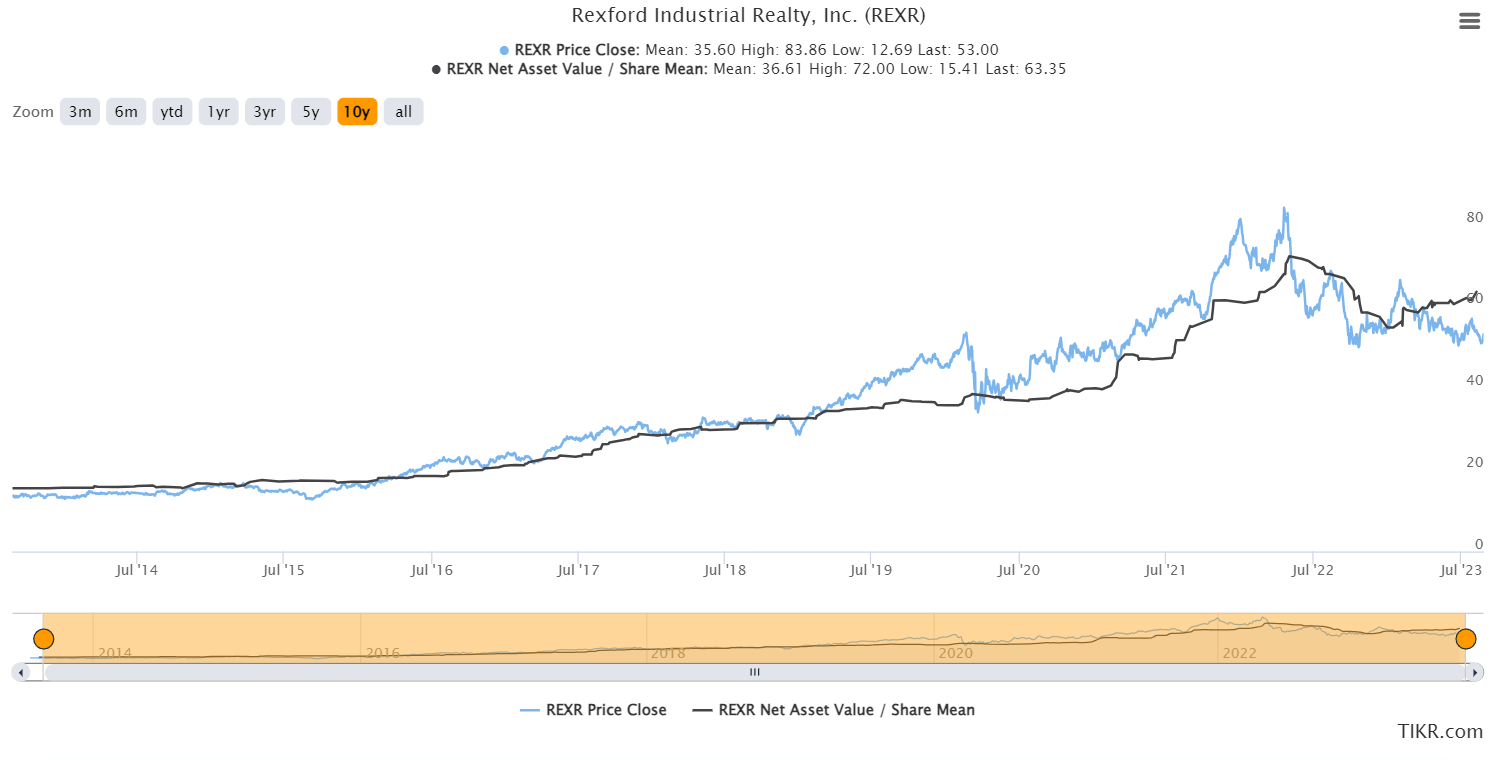

Rexford ( REXR ) is a great industrial REIT. They grew NAV and cash flow for shareholders. Analysts reacted to the drop in share prices in mid-2022 by lowering NAV estimates. That's not how NAV estimates are supposed to work, but such is life.

{kind=link}

Those NAV estimates have been trending back up again even though REXR is only about 5% off their lowest close in the last two-plus years.

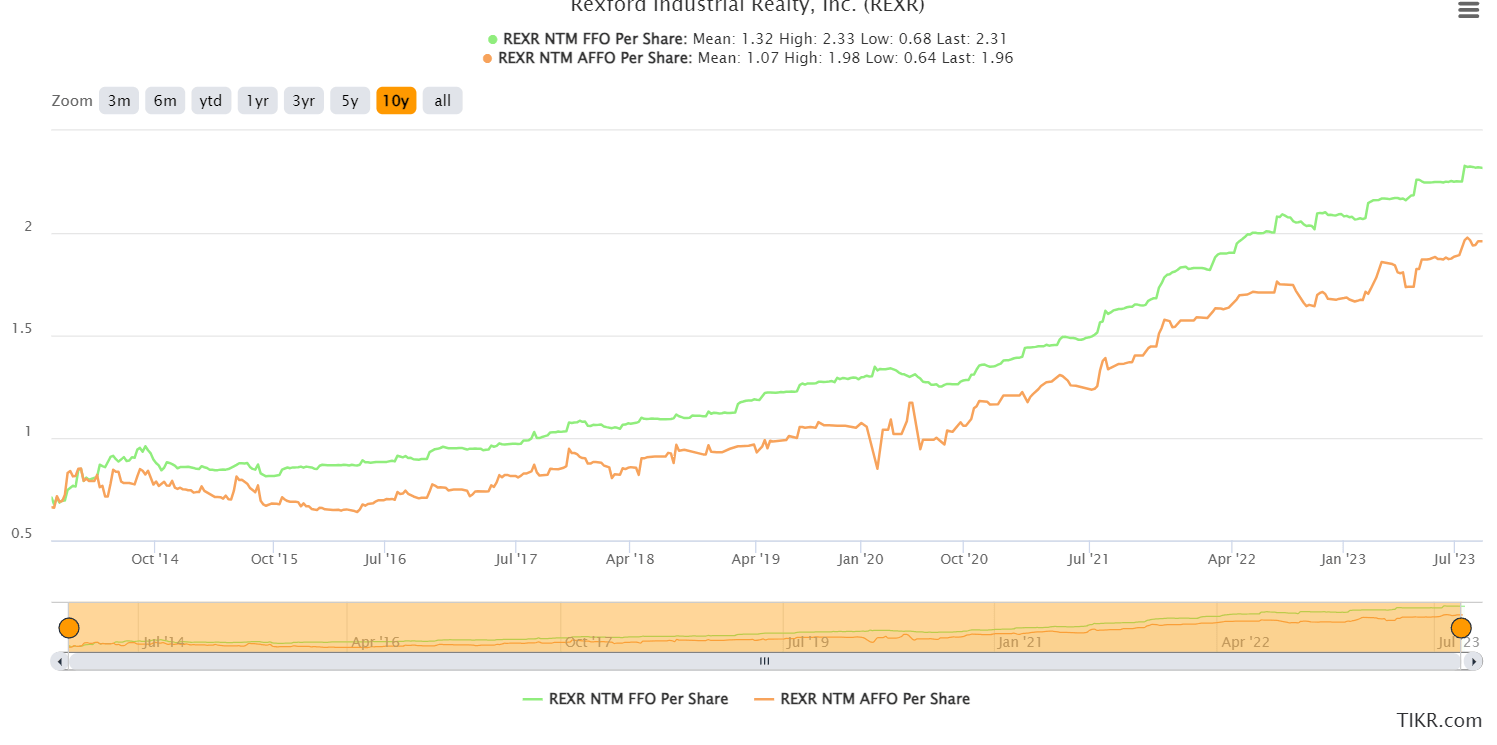

How about FFO and AFFO per share? Massive growth:

{kind=link}

You probably get the trend now. Those are the kinds of REITs I like.

Dividend Yields

Some investors won't like my picks because of low dividend yields. So be it.

Yields for the shares I mentioned:

- ARE: 4.3%.

- SUI: 3.0%.

- CPT: 3.8%.

- REXR: 2.9%.

Other REITs

I want to mention a few other REITs because I would've liked to include them. They are each great REITs in their own right. Here they are by property type:

Apartments:

Towers:

Industrial:

Net Lease:

Clearly, some of them will be more actively priced than others. However, this article doesn't deal with the valuation of each share.

Valuation

Regarding the first four great REITs, which I specify to ensure readers know I don't mean MPW, those four are all in our strong buy range. I think investors buying any of those shares today and simply holding them for the next five years will do quite well.

Conclusion

I have positions in several of these REITs (not all), including the first four great REITs. I'm not expecting to sell any of those in the near term. My goal for my equity REIT purchases is long-term allocation. We'll keep the trading for the mortgage REITs, BDCs, and preferred shares.

There are times when I close out equity REIT positions, but most of them are expected to be great picks for buy-and-hold investors.

For further details see:

4 Great REITs At Deep Discounts To My Targets