CSWC - 4 Hefty Dividends With Up To 10% Yield

2023-08-28 11:30:54 ET

Summary

- There are great deals to be had among dividend stocks despite the tech-fueled market runup.

- All four picks in this article pay big, well-covered dividend yields to help investors make money while they sleep.

- They carry diversified and/or essential business models and are undervalued, resulting in potential for strong total returns in addition to income.

It's no secret that building a growing income stream is a viable path to financial independence, and many investors have done it. Having extra cash flow is not just about quitting one's job, but rather about having flexibility to do what one wants to do in life, whether it be upgrading to a better car, treating yourself to fine dining, or taking the family out for a nice vacation every now and then.

Having that flexibility can also result in peace of mind in knowing that you own a part of a business that's working hard to kick income back to you. To paraphrase Warren Buffett, if you don't find a way to make money while you sleep, you will work forever. This brings me to the following 4 businesses that throw off durable high yields that could be appealing to investors of different stripes, so let's dig in!

Pick #1: EPD - 7.6% Yield

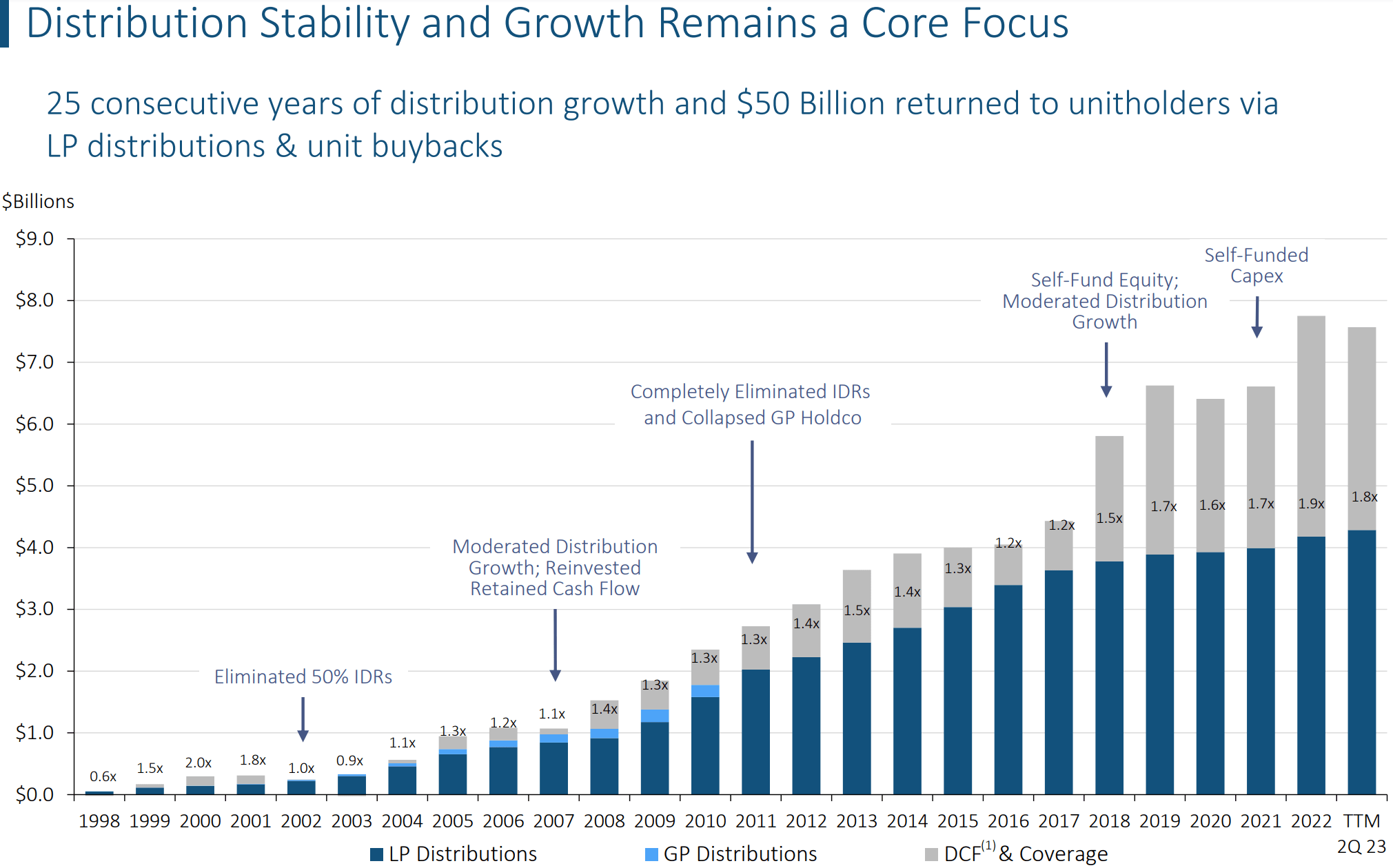

Enterprise Products Partners ( EPD ) is arguably the highest quality midstream company out there, with 25 years of distribution increases under its belt. It's also come a long way over the years, having done away with its incentive distribution rights and reliance on issuing equity to fund growth.

This means that EPD is no longer reliant on the whims of its share price to dictate its future. Rather, it's fully capable of self-funding its growth plans. This is reflected by the $1.7 billion in distributable cash flow that was generated during the second quarter, resulting in a 1.6x DCF to distribution coverage ratio (1.8x coverage on a TTM basis). This gives EPD plenty of retained capital, at $639 million in the last quarter and $3.3 billion over the trailing 12 reported month. EPD has a long track record of covering its distribution, and this coverage has only gotten stronger since 2018, as shown below.

{kind=link}

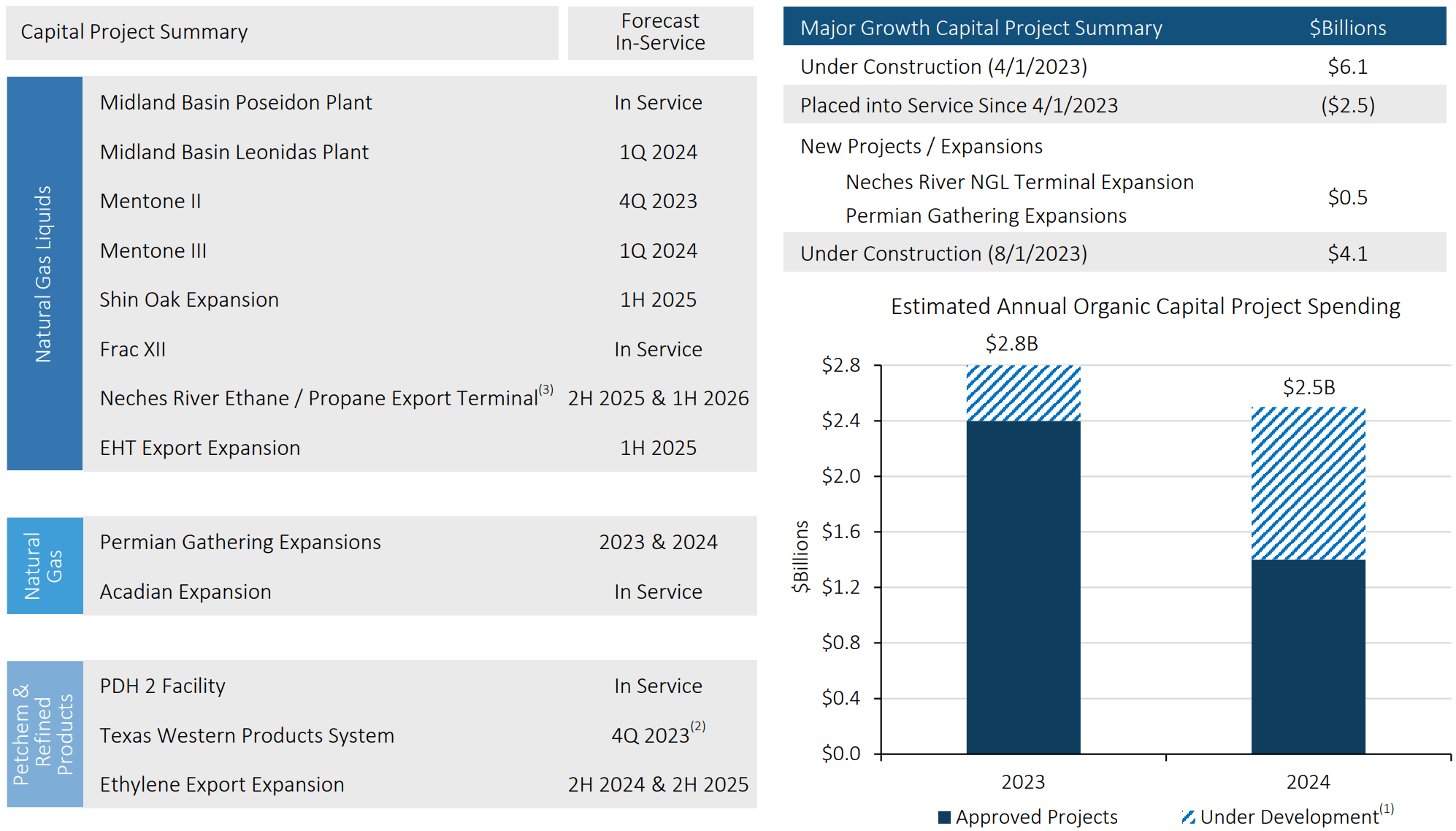

This retained capital provides substantial funding for its $4.1 billion worth of approved major projects that are currently under construction. This includes a number of NGL, Natural Gas, and Petrochemical and Refined products projects that are slated for in-service periods ranging from the end of this year to the first half of 2025, as shown below.

{kind=link}

Risks to EPD include a seemingly incessant parade of news around climate change, and what that means for fossil fuels. Also, higher interest rates have resulted in pressures around "leveraged" industries such as REITs and MLPs.

However, it's important not to paint all fossil fuels in the same corner, as natural gas remains a highly viable lower carbon alternative compared to coal in the U.S. and in much of the world, particularly in Asia. Moreover, EPD is led by a seasoned management, whose senior leadership and director group own a combined 32% of outstanding units. Management has also guided EPD through various financial and energy shocks, including the oil price collapse and the COVID-19 pandemic, with an ROIC that's ranged from 10% to 13% between 2005 and 2022.

Importantly, EPD's self-funding model is supported by a strong balance sheet with a net debt to EBITDA ratio of 3.0x, the lowest among midstream companies. It also carries A-/Baa1 credit ratings from S&P and Moody's, helping to ensure that it is able to refinance debt at relatively lower interest rates compared to peers.

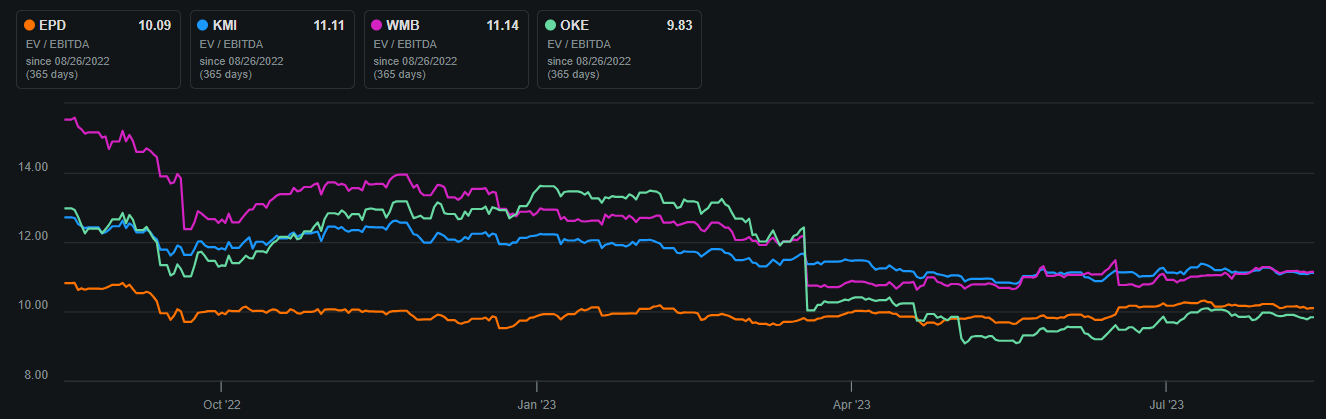

Lastly, EPD trades at a meaningful discount to its peers with an EV/EBITDA of 10.1, sitting below that of Kinder Morgan ( KMI ) and Williams Companies ( WMB ), and just slightly above that of ONEOk ( OKE ). Perhaps one of the reasons is because EPD issues a K-1 instead of a 1099 during tax time. As such, investors who don't mind a little extra work during tax time may want to considering into this appealing stock while it yields 7.6%.

{kind=link}

Pick #2: CSWC - 10.3% Yield

Capital Southwest ( CSWC ) is a lesser known internally-managed BDC due to its far smaller size compared to Main Street Capital ( MAIN ). What it lacks in size, however, it makes up for with a consistent track record of rewarding shareholders.

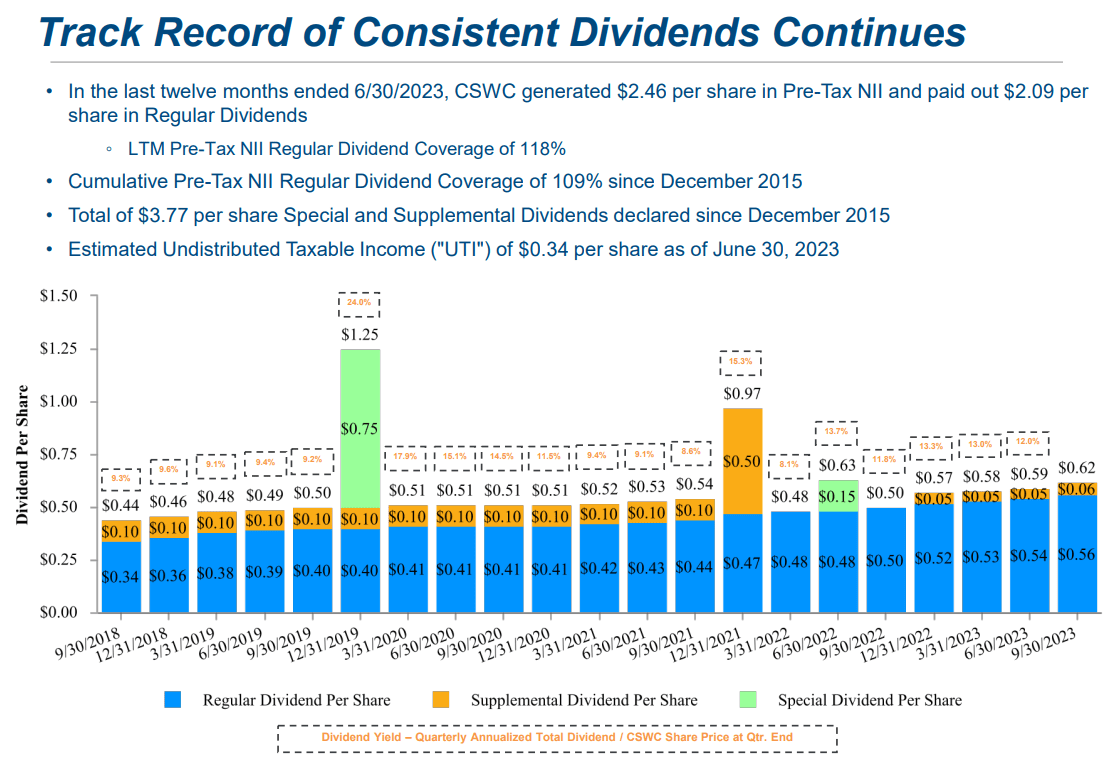

This is supported by CSWC's strong history of raising its regular dividend and paying out special dividends since 2018. This includes the recent 3.7% dividend bump in the regular dividend to $0.56, marking CSWC's 5th consecutive quarterly raise, along with a $0.06 special dividend. Notably, the current dividend rate is well-covered at a dividend-to-NII payout ratio of 83.5%.

{kind=link}

CSWC's strategy is to invest in the lower middle market, as defined by those companies with annual EBITDA between $3-$20 million, with typical leverage of 2.0x to 4.0x debt to EBITDA through CSWC's debt position. This space is less competitive compared to the upper middle market, thereby resulting in more attractive deal pricing. This, combined with rising interest rates contributed to a weighted average yield on debt investments of 12.9%. As shown below, this compares favorably to CSWC's cost of debt, which ranges from 4.1% to 7.7% (SOFR + 2.41%).

Moreover, CSWC's portfolio is backed by primarily first lien investments, which represent 97% of the credit portfolio. The $1.3 billion portfolio is also well diversified with an average hold size of 1.2%, and is diversified across industries, with business services, media/marketing, healthcare, and consumer products/services representing half the portfolio, as shown below.

Investor Presentation

Meanwhile, its portfolio is in good shape, with 96% of all debt investments currently rated as a '1' or '2' on a scale from 1-4, with 1 being the lowest risk, and non-accruals are low, at 1.7% of the total investment portfolio. CSWC as insiders collectively own 5.3% of the company, and insiders have only made 1 sale of CSWC stock in the open market over the past 3.5 years.

Besides alignment of interest with shareholders, since management isn't directly incentivized to grow AUM just for the sake of growth, CSWC also benefits from low operating costs. Operating costs as a percentage of total assets have trended down from 4.9% in 2016 to 1.9% at present. While there is still room for improvement to get to MAIN's 1.4% , it sits lower than that of most externally managed BDCs, enabling management to return more capital to shareholders.

Risks to CSWC include lower interest rates, since 97% of CSWC's debt portfolio is floating rate. That's probably not a concern for the near term, especially considering that the Fed Chairman just last week stated that that they are prepared to raise rates further. Another risk is the potential for a recession, which may pressure some borrowers. However, CSWC has the benefit of a strong balance sheet with a regulatory debt to equity ratio of just 0.87x, sitting below that of most BDCs, which carry leverage ratios above 1.0x. This gives CSWC some buffer room as it's able to take advantage of economic tightness to make investments at attractive prices should those opportunities arise.

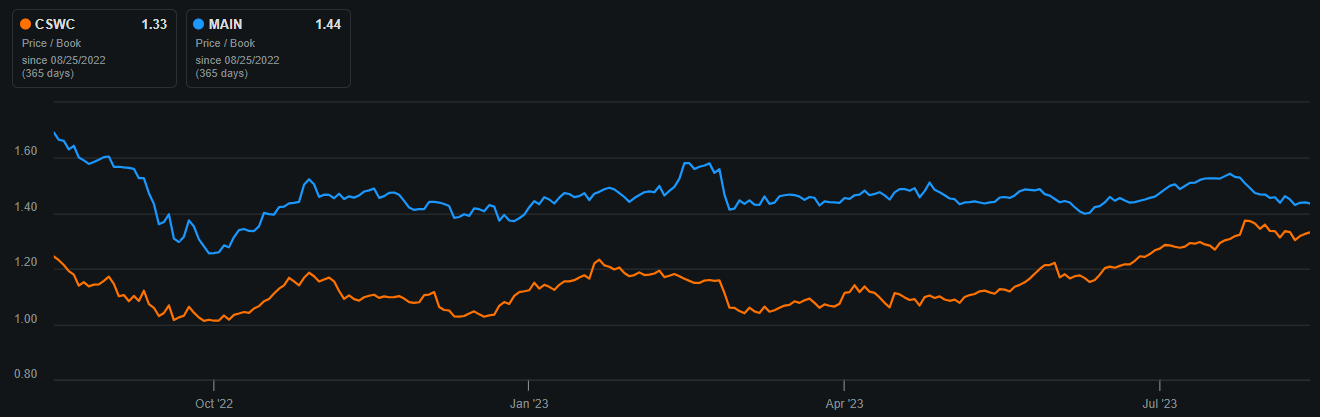

Lastly, while CSWC is no longer cheap, it does trade at a reasonable forward PE ratio of 8.3x. CSWC also carries a price to book ratio of 1.33x, which sits below the 1.44x of MAIN. While some investors may not want to pay such a high premium for a BDC, it's worth keeping in mind that internally-managed BDCs with low operating cost structures deserve to trade at a premium. That's how CSWC is still able to pay out a well-covered 10.3% while trading at a substantial premium to NAV.

{kind=link}

Pick #3: ARCC - 10% Yield

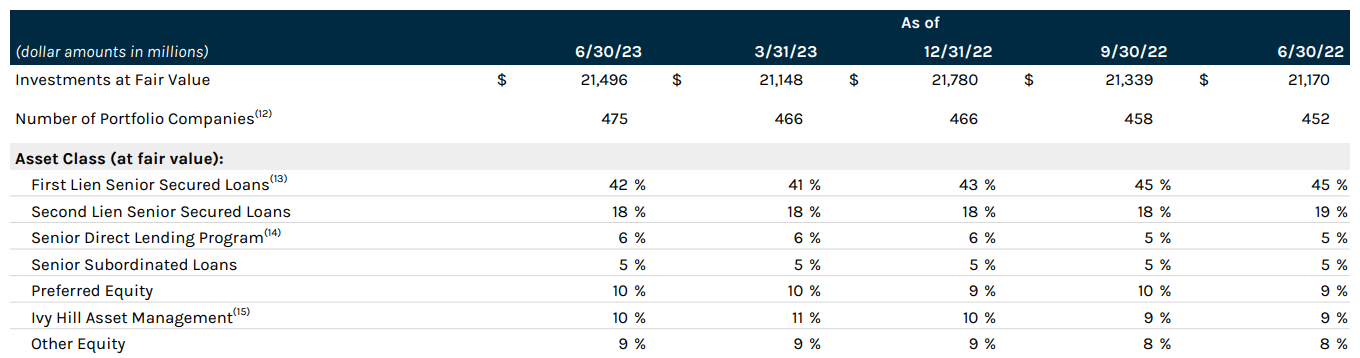

Ares Capital (ARCC) is the largest BDC by asset size, with $21.5 billion in total investments under management. It's externally managed by the well-recognized alternative asset manager Ares Management ( ARES ), which has strong expertise in the areas of credit, real estate, and private equity.

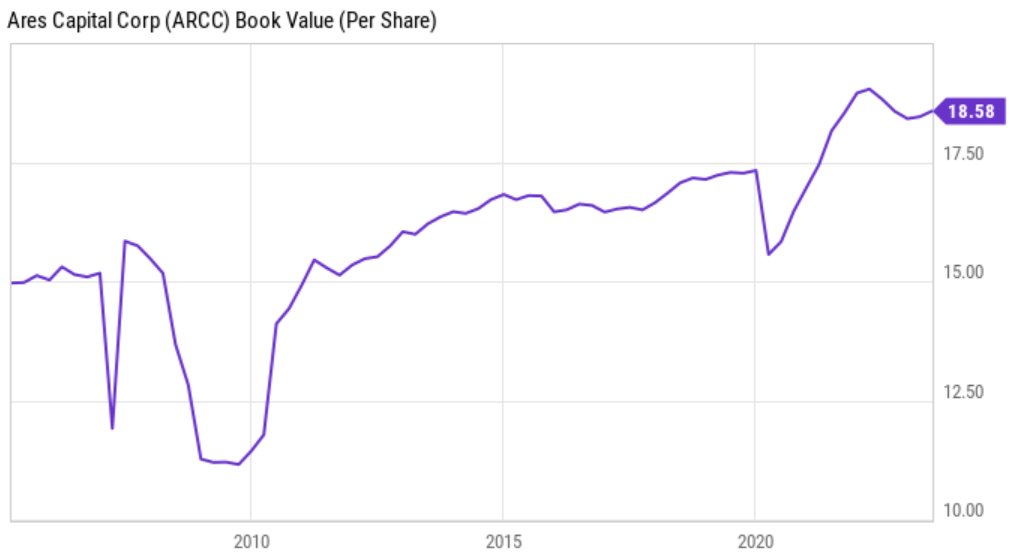

Since inception, ARCC has produced a respectable 12% annual shareholder. Over this time, it's paid steady dividends to investors and has gradually increased its book value per share. This implies accretive capital raises and investments that have benefitted shareholders over the long run. As shown below, ARCC's book value per share has steadily risen from $15 at IPO to $18.58 at present.

{kind=link}

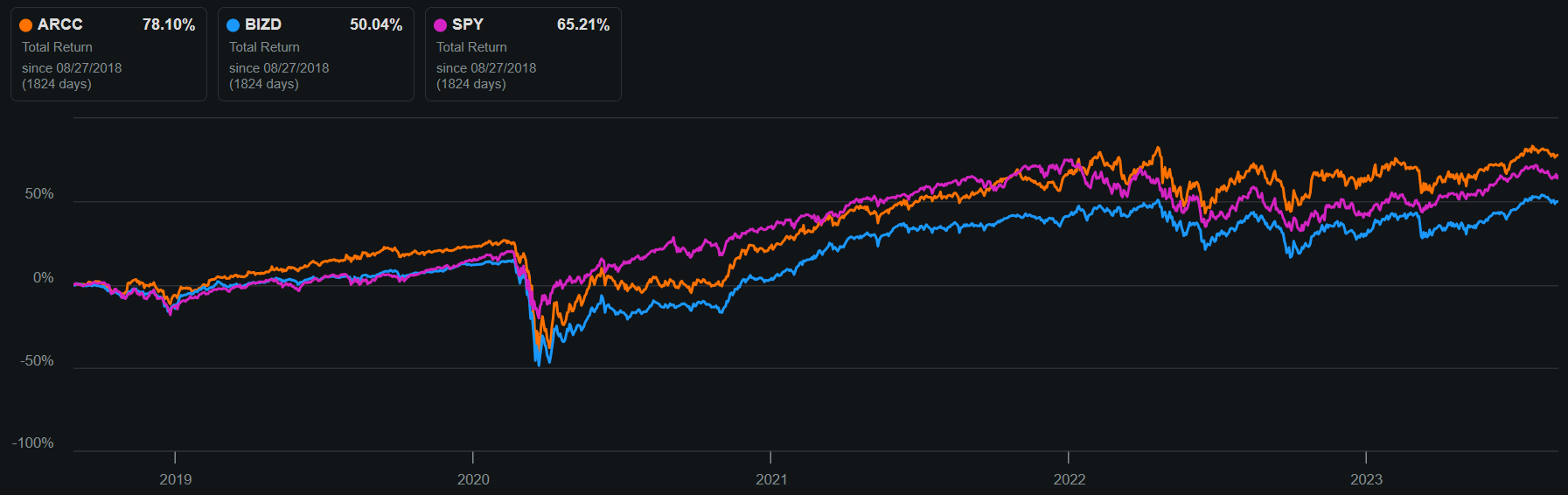

As shown below, ARCC's total return over the past 5 years has outperformed that of the S&P 500 ( SPY ), thanks to dividends, and that of the VanEck BDC Income ETF ( BIZD ).

{kind=link}

This respectable performance can be attributed to prudent portfolio management, and ARCC invests in the upper middle market, whose companies have achieved some form of scale advantages over smaller companies. This makes ARCC's portfolio less likely to default than smaller companies and given their larger asset base, ARCC is likely to recover meaningful principal in the event of a borrower default. The portfolio is also spread across 475 investments with software, healthcare, consumer durables, and financial services representing ARCC's top 4 sectors.

At present, investments on non-accrual represent just 1.1% of ARCC's portfolio fair value, and most of ARCC's investments are senior secured debt, which represent 65% of the portfolio. Another 10% is invested in a related company, Ivy Hill Asset Management, which primarily invests in senior secured debt.

{kind=link}

ARCC also benefits from higher interest rates, considering that 68% of its total portfolio is in the form of floating rate debt investments. Recent comments by the Fed Chairman last week indicated that rates could go higher due to inflation remaining too high, despite coming down from its peak. This is bullish for ARCC, as higher rates mean that it's able to charge its borrowers higher interest.

At the same time, ARCC is seeing more demand for deals amid a resilient economy, as the number of deals it reviewed during the second quarter was 20% higher than the number in the first quarter. Borrowers should also be able to withstand higher interest rates, as portfolio interest coverage ratio improved by 30% over the trailing 12 reported months to 2.1x.

Risks to ARCC include potential for a recession should global economic weakness, particularly from China, spread to the U.S. ARCC's borrowers could see indirect impacts from a global recession. Moreover, increased competition from other large BDCs such as Blue Owl Capital ( OBDC ) could result in yield compression down the line.

Meanwhile, ARCC maintains a respectable balance sheet with a debt to equity ratio of 1.1x as of the second quarter, sitting below the 1.27x from the prior year period. This gives ARCC plenty of flexibility with which to invest in opportunistic deals.

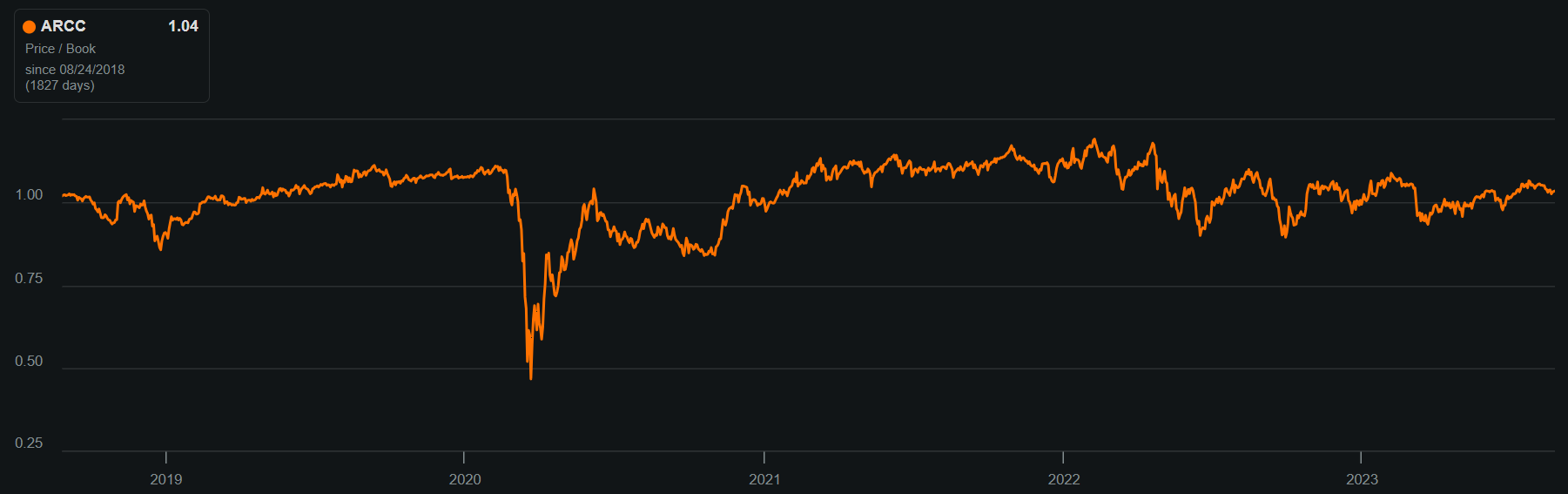

Importantly, ARCC currently yields 10% and its dividend is well covered by Core EPS at a 83% payout ratio. It also trades at a reasonable price-to-book value of just 1.04x, which sits toward the low end of its trading range since 2021, as shown below. In my opinion, this makes the current price of $19.24 an attractive entry point on this 10%-yielding stock.

{kind=link}

Pick #4: SRC - 7% Yield

Spirit Realty Capital (SRC) is a self-managed net lease REIT that carries many attributes like that of industry leader, Realty Income Corp. ( O ), due to its wide asset base and strong fundamentals. This includes 2,064 owned properties with 99.8% occupancy, and a weighted average lease term of 10.3 years, which is on par with that of other high quality net leases REITs.

SRC's asset base is well-diversified across 49 states and 37 different industries. This includes tenants in experiential industries (think e-commerce resistance) such as fitness and lifestyle clubs, as well as quick service restaurants, discount retailers (i.e., dollar stores), and drug stores.

SRC has also made a meaningful pivot towards the durable and growing industrial sector, with distribution and manufacturing now comprising 23% of the portfolio base rents. As shown below, SRC is clearly targeting this segment with it being on the receiving end of most incremental investments over the trailing 12 months.

{kind=link}

Risks to SRC include an extended period of high inflation, since over half of its leases have contractual escalations rather being CPI-linked, and most of those leases were closed during a time of lower inflation. Plus, higher interest rates and the current relatively lower valuation (compared to historical norms) raises its cost of capital for new investments and cost of debt when its debt matures.

However, SRC does have other ways to unlock value through portfolio recycling, as it did during the second quarter, by disposition of 30 properties with a cap rate of 6.3%, and recycling proceeds into 11 properties with a higher cap rate of 8.0% and a long weighted average lease term of 15.3 years.

At the same time, SRC carries $1.6 billion worth of liquidity and has a BBB rated balance sheet that's supported by a low debt to EBITDAre ratio of 5.3x, sitting below the 6.0x level generally preferred by ratings agencies. SRC is also in a strong position to service its recurring financial obligations, with a fixed charge coverage ratio of 5.1x.

This lends support to the 7.0% dividend yield, which is well-covered by a 73% payout ratio. SRC also trades at a meaningful discount to its peers at the current price of $38.30 with a forward P/FFO of 10.5. This is meaningfully cheaper compared to Realty Income's P/FFO of 13.6, Agree Realty's ( ADC) 15.8, and NNN REIT's ( NNN ) 12.2. In fact, fellow SA analyst Brad Thomas recently floated the potential for SRC to be acquired by Realty Income, due to the large valuation gap and SRC's quality portfolio, and highlighted the upside potential in a recent piece as follows:

Spirit's AFFO (Equity) yield is now 9.5% compared with Realty Income's equity yield of 7.0%. Spirit has spun out (and liquidated) its "ugly duckling" properties (into Spirit MTA REIT) and is now ready to put the portfolio in the capable hands of Realty Income's management team. At $45.00 per share, the equity yield would translate to 8.0% AFFO yield or 20% premium to Spirit's current share price.

Considering all the above, SRC appears to be a quality net lease gem that's trading at a substantial discount to its net lease peers. I view the discount as being unwarranted, and patient investors get paid a well-covered 7% dividend yield while they wait for the current rate hike cycle to come to ease up and come to an end.

Investor Takeaway

I hope you enjoyed this piece about EPD, CSWC, ARCC, and SRC. All four have diverse and or essential business models that capture income from a large cross-section of the economy, and combine to average an 8.7% Yield. These 4 companies carry quality attributes in their own right, and have the commonality that they have the ability to throw off well-covered dividends to investors for the foreseeable future. As such, income investors ought to consider them for a potential strong boost to their income streams.

For further details see:

4 Hefty Dividends With Up To 10% Yield